Leveraged ETF Return Dispersion

Table of Contents

Introduction #

Over the past 15 years (or so), leveraged ETFs have become frequently used for trading equity indices, sectors, and other asset classes by the investor that is seeking to use leverage for excess exposure to those asset classes. The question remains, however, what happens to the returns of leveraged ETFs over an extended time horizon and is there an optimal leverage ratio for the long-term buy-and-hold investor that allows them to take advantage of leverage to increase the up-side returns, while avoiding catastrophic losses on the down-side? In this investigation, we will delve into these ideas and see what the data shows.

Python Imports #

# Standard Library

import os

import sys

import warnings

from pathlib import Path

# Data Handling

import pandas as pd

# Suppress warnings

warnings.filterwarnings("ignore")

# Add the source subdirectory to the system path to allow import config from settings.py

current_directory = Path(os.getcwd())

website_base_directory = current_directory.parent.parent.parent

src_directory = website_base_directory / "src"

sys.path.append(str(src_directory)) if str(src_directory) not in sys.path else None

# Import settings.py

from settings import config

# Add configured directories from config to path

SOURCE_DIR = config("SOURCE_DIR")

sys.path.append(str(Path(SOURCE_DIR))) if str(Path(SOURCE_DIR)) not in sys.path else None

# Add other configured directories

BASE_DIR = config("BASE_DIR")

CONTENT_DIR = config("CONTENT_DIR")

POSTS_DIR = config("POSTS_DIR")

PAGES_DIR = config("PAGES_DIR")

PUBLIC_DIR = config("PUBLIC_DIR")

SOURCE_DIR = config("SOURCE_DIR")

DATA_DIR = config("DATA_DIR")

DATA_MANUAL_DIR = config("DATA_MANUAL_DIR")

Python Functions #

Here are the functions needed for this project:

- load_data: Load data from a CSV, Excel, or Pickle file into a pandas DataFrame.

- pandas_set_decimal_places: Set the number of decimal places displayed for floating-point numbers in pandas.

- plot_histogram: Plot the histogram of a data set from a DataFrame.

- plot_scatter: Plot the data from a DataFrame for a specified date range and columns.

- plot_time_series: Plot the timeseries data from a DataFrame for a specified date range and columns.

- run_regression: Run a linear regression using statsmodels OLS and return the results.

- summary_stats: Generate summary statistics for a series of returns.

- yf_pull_data: Download daily price data from Yahoo Finance and export it.

from load_data import load_data

from pandas_set_decimal_places import pandas_set_decimal_places

from plot_histogram import plot_histogram

from plot_scatter import plot_scatter

from plot_time_series import plot_time_series

from run_regression import run_regression

from summary_stats import summary_stats

from yf_pull_data import yf_pull_data

Data Overview #

For this exercise, we will investigate the long-term return relationships between the following:

- QQQ (Invesco QQQ Trust, Series 1) and TQQQ (ProShares UltraPro QQQ)

- SPY (SPDR S&P 500 ETF Trust) and UPRO (ProShares UltraPro S&P 500)

Just to clarify, any time we are referring to “close prices” in this analysis, we are referring to the partially-adjusted close prices that account for splits, but not dividends. Because we are dealing with leveraged ETFs, we want to focus on the pure returns due to change in price, but exclude the dividends, which are not leveraged in the same way as the price changes.

QQQ & TQQQ #

Acquire & Plot Data (QQQ) #

First, let’s get the data for QQQ. If we already have the desired data, we can load it from a local pickle file. Otherwise, we can download it from Yahoo Finance using the yf_pull_data function.

pandas_set_decimal_places(2)

yf_pull_data(

base_directory=DATA_DIR,

ticker="QQQ",

adjusted=False,

source="Yahoo_Finance",

asset_class="Exchange_Traded_Funds",

excel_export=True,

pickle_export=True,

output_confirmation=False,

)

qqq = load_data(

base_directory=DATA_DIR,

ticker="QQQ",

source="Yahoo_Finance",

asset_class="Exchange_Traded_Funds",

timeframe="Daily",

file_format="pickle",

)

# Rename columns to "QQQ_Close", etc.

qqq = qqq.rename(columns={

"Adj Close": "QQQ_Adj_Close",

"Close": "QQQ_Close",

"High": "QQQ_High",

"Low": "QQQ_Low",

"Open": "QQQ_Open",

"Volume": "QQQ_Volume"

})

display(qqq)

| QQQ_Adj_Close | QQQ_Close | QQQ_High | QQQ_Low | QQQ_Open | QQQ_Volume | |

|---|---|---|---|---|---|---|

| Date | ||||||

| 1999-03-10 | 43.07 | 51.06 | 51.16 | 50.28 | 51.12 | 5232000 |

| 1999-03-11 | 43.29 | 51.31 | 51.73 | 50.31 | 51.44 | 9688600 |

| 1999-03-12 | 42.23 | 50.06 | 51.16 | 49.66 | 51.12 | 8743600 |

| 1999-03-15 | 43.44 | 51.50 | 51.56 | 49.91 | 50.44 | 6369000 |

| 1999-03-16 | 43.81 | 51.94 | 52.16 | 51.16 | 51.72 | 4905800 |

| ... | ... | ... | ... | ... | ... | ... |

| 2026-06-10 | 693.69 | 693.69 | 711.28 | 692.93 | 701.66 | 65334300 |

| 2026-06-11 | 717.12 | 717.12 | 718.37 | 695.00 | 699.29 | 71798900 |

| 2026-06-12 | 721.34 | 721.34 | 724.01 | 711.28 | 717.61 | 51168400 |

| 2026-06-15 | 744.00 | 744.00 | 744.76 | 737.38 | 738.10 | 46710200 |

| 2026-06-16 | 729.86 | 729.86 | 744.22 | 729.64 | 742.25 | 45348700 |

6860 rows × 6 columns

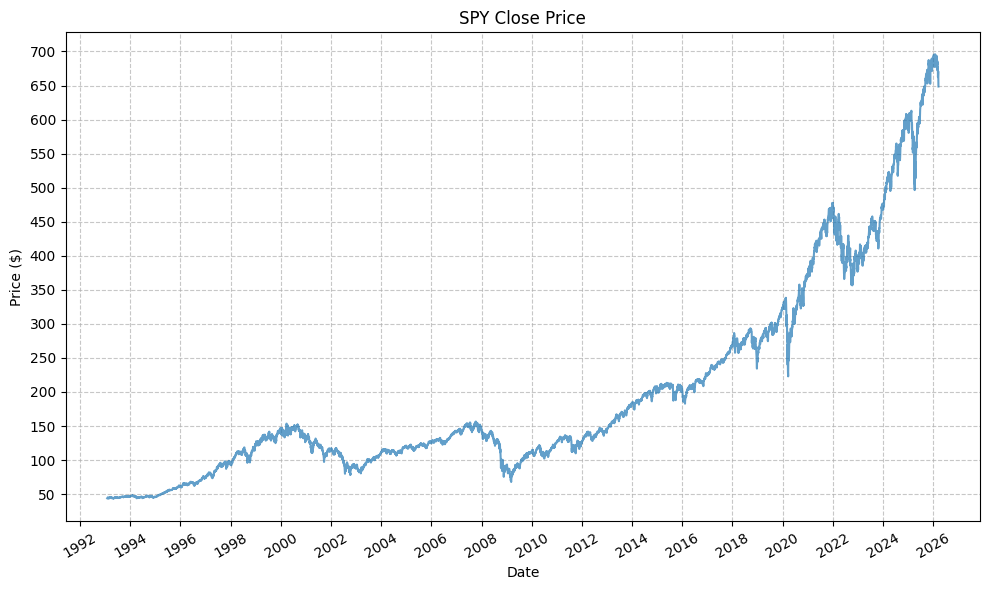

And the plot of the time series of partially adjusted close prices:

plot_time_series(

df=qqq,

plot_start_date=None,

plot_end_date=None,

plot_columns=["QQQ_Adj_Close"],

title="QQQ Adjusted Close Price",

x_label="Date",

x_format="Year",

x_tick_spacing=2,

x_tick_start=None,

x_tick_rotation=30,

y_label="Price ($)",

y_format="Decimal",

y_format_decimal_places=0,

y_tick_spacing="Auto",

y_tick_rotation=0,

grid=True,

legend=False,

export_plot=False,

plot_file_name=None,

)

Acquire & Plot Data (TQQQ) #

Next, TQQQ:

yf_pull_data(

base_directory=DATA_DIR,

ticker="TQQQ",

adjusted=False,

source="Yahoo_Finance",

asset_class="Exchange_Traded_Funds",

excel_export=True,

pickle_export=True,

output_confirmation=False,

)

tqqq = load_data(

base_directory=DATA_DIR,

ticker="TQQQ",

source="Yahoo_Finance",

asset_class="Exchange_Traded_Funds",

timeframe="Daily",

file_format="pickle",

)

# Rename columns to "TQQQ_Close", etc.

tqqq = tqqq.rename(columns={

"Adj Close": "TQQQ_Adj_Close",

"Close": "TQQQ_Close",

"High": "TQQQ_High",

"Low": "TQQQ_Low",

"Open": "TQQQ_Open",

"Volume": "TQQQ_Volume"

})

display(tqqq)

| TQQQ_Adj_Close | TQQQ_Close | TQQQ_High | TQQQ_Low | TQQQ_Open | TQQQ_Volume | |

|---|---|---|---|---|---|---|

| Date | ||||||

| 2010-02-11 | 0.21 | 0.22 | 0.22 | 0.20 | 0.20 | 6912000 |

| 2010-02-12 | 0.21 | 0.22 | 0.22 | 0.21 | 0.21 | 17203200 |

| 2010-02-16 | 0.21 | 0.23 | 0.23 | 0.22 | 0.22 | 19238400 |

| 2010-02-17 | 0.22 | 0.23 | 0.23 | 0.23 | 0.23 | 38361600 |

| 2010-02-18 | 0.22 | 0.23 | 0.24 | 0.23 | 0.23 | 77721600 |

| ... | ... | ... | ... | ... | ... | ... |

| 2026-06-10 | 69.27 | 69.27 | 74.70 | 69.00 | 71.68 | 91465200 |

| 2026-06-11 | 76.01 | 76.01 | 76.60 | 69.59 | 70.89 | 116288800 |

| 2026-06-12 | 77.52 | 77.52 | 78.36 | 74.29 | 76.34 | 94070700 |

| 2026-06-15 | 84.59 | 84.59 | 85.03 | 82.64 | 82.88 | 59758000 |

| 2026-06-16 | 79.93 | 79.93 | 84.83 | 79.86 | 84.19 | 67086700 |

4111 rows × 6 columns

And the plot of the time series of partially adjusted close prices:

plot_time_series(

df=tqqq,

plot_start_date=None,

plot_end_date=None,

plot_columns=["TQQQ_Adj_Close"],

title="TQQQ Adjusted Close Price",

x_label="Date",

x_format="Year",

x_tick_spacing=1,

x_tick_start=None,

x_tick_rotation=30,

y_label="Price ($)",

y_format="Decimal",

y_format_decimal_places=0,

y_tick_spacing="Auto",

y_tick_rotation=0,

grid=True,

legend=False,

export_plot=False,

plot_file_name=None,

)

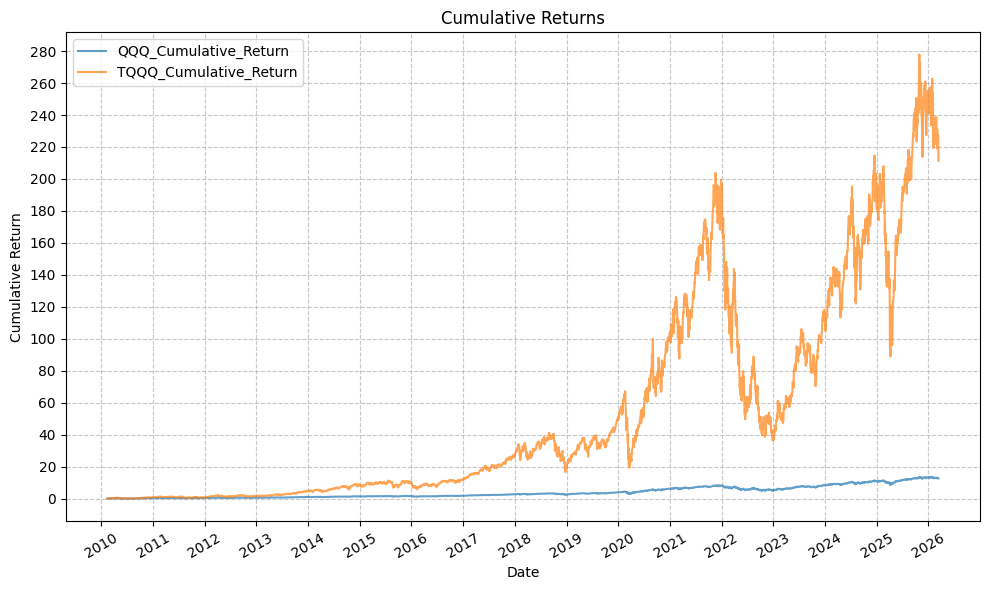

Looking at the close prices doesn’t give us a true picture of the magnitude of the difference in returns due to the leverage. In order to see that, we need to look at the cumulative returns and the drawdowns.

Calculate & Plot Cumulative Returns, Rolling Returns, and Drawdowns (QQQ & TQQQ) #

Next, we will calculate the cumulative returns, rolling returns, and drawdowns. This involves aligning the data to start with the inception of TQQQ. For this excercise, we will not extrapolate the data for QQQ back to 1999, but rather just align the data from the inception of TQQQ in 2010.

etfs = ["QQQ", "TQQQ"]

# Merge dataframes and drop rows with missing values

qqq_tqqq_aligned = tqqq.merge(qqq, left_index=True, right_index=True, how='left')

qqq_tqqq_aligned = qqq_tqqq_aligned.dropna()

# Calculate cumulative returns

for etf in etfs:

qqq_tqqq_aligned[f"{etf}_Return"] = qqq_tqqq_aligned[f"{etf}_Close"].pct_change()

qqq_tqqq_aligned[f"{etf}_Cumulative_Return"] = (1 + qqq_tqqq_aligned[f"{etf}_Return"]).cumprod() - 1

qqq_tqqq_aligned[f"{etf}_Cumulative_Return_Plus_One"] = 1 + qqq_tqqq_aligned[f"{etf}_Cumulative_Return"]

qqq_tqqq_aligned[f"{etf}_Rolling_Max"] = qqq_tqqq_aligned[f"{etf}_Cumulative_Return_Plus_One"].cummax()

qqq_tqqq_aligned[f"{etf}_Drawdown"] = qqq_tqqq_aligned[f"{etf}_Cumulative_Return_Plus_One"] / qqq_tqqq_aligned[f"{etf}_Rolling_Max"] - 1

qqq_tqqq_aligned.drop(columns=[f"{etf}_Cumulative_Return_Plus_One", f"{etf}_Rolling_Max"], inplace=True)

# Define rolling windows in trading days

rolling_windows = {

'1d': 1, # 1 day

'1w': 5, # 1 week (5 trading days)

'1m': 21, # 1 month (~21 trading days)

'3m': 63, # 3 months (~63 trading days)

'6m': 126, # 6 months (~126 trading days)

'1y': 252, # 1 year (~252 trading days)

'2y': 504, # 2 years (~504 trading days)

'3y': 756, # 3 years (~756 trading days)

'4y': 1008, # 4 years (~1008 trading days)

'5y': 1260, # 5 years (~1260 trading days)

}

# Calculate rolling returns for each ETF and each window

for etf in etfs:

for period_name, window in rolling_windows.items():

qqq_tqqq_aligned[f"{etf}_Rolling_Return_{period_name}"] = (

qqq_tqqq_aligned[f"{etf}_Close"].pct_change(periods=window)

)

display(qqq_tqqq_aligned)

| TQQQ_Adj_Close | TQQQ_Close | TQQQ_High | TQQQ_Low | TQQQ_Open | TQQQ_Volume | QQQ_Adj_Close | QQQ_Close | QQQ_High | QQQ_Low | ... | TQQQ_Rolling_Return_1d | TQQQ_Rolling_Return_1w | TQQQ_Rolling_Return_1m | TQQQ_Rolling_Return_3m | TQQQ_Rolling_Return_6m | TQQQ_Rolling_Return_1y | TQQQ_Rolling_Return_2y | TQQQ_Rolling_Return_3y | TQQQ_Rolling_Return_4y | TQQQ_Rolling_Return_5y | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||||||||||||

| 2010-02-11 | 0.21 | 0.22 | 0.22 | 0.20 | 0.20 | 6912000 | 37.90 | 43.67 | 43.79 | 42.76 | ... | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 2010-02-12 | 0.21 | 0.22 | 0.22 | 0.21 | 0.21 | 17203200 | 37.98 | 43.76 | 43.88 | 43.16 | ... | 0.00 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 2010-02-16 | 0.21 | 0.23 | 0.23 | 0.22 | 0.22 | 19238400 | 38.47 | 44.32 | 44.35 | 43.85 | ... | 0.04 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 2010-02-17 | 0.22 | 0.23 | 0.23 | 0.23 | 0.23 | 38361600 | 38.69 | 44.57 | 44.57 | 44.26 | ... | 0.02 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 2010-02-18 | 0.22 | 0.23 | 0.24 | 0.23 | 0.23 | 77721600 | 38.93 | 44.85 | 44.93 | 44.45 | ... | 0.02 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 2026-06-10 | 69.27 | 69.27 | 74.70 | 69.00 | 71.68 | 91465200 | 693.69 | 693.69 | 711.28 | 692.93 | ... | -0.06 | -0.20 | -0.10 | 0.40 | 0.24 | 0.86 | 1.05 | 2.75 | 2.97 | 1.80 |

| 2026-06-11 | 76.01 | 76.01 | 76.60 | 69.59 | 70.89 | 116288800 | 717.12 | 717.12 | 718.37 | 695.00 | ... | 0.10 | -0.11 | 0.01 | 0.62 | 0.36 | 1.00 | 1.26 | 3.12 | 3.73 | 1.92 |

| 2026-06-12 | 77.52 | 77.52 | 78.36 | 74.29 | 76.34 | 94070700 | 721.34 | 721.34 | 724.01 | 711.28 | ... | 0.02 | 0.06 | 0.00 | 0.69 | 0.37 | 1.06 | 1.31 | 3.43 | 3.76 | 1.96 |

| 2026-06-15 | 84.59 | 84.59 | 85.03 | 82.64 | 82.88 | 59758000 | 744.00 | 744.00 | 744.76 | 737.38 | ... | 0.09 | 0.11 | 0.07 | 0.78 | 0.51 | 1.24 | 1.49 | 3.68 | 4.08 | 2.22 |

| 2026-06-16 | 79.93 | 79.93 | 84.83 | 79.86 | 84.19 | 67086700 | 729.86 | 729.86 | 744.22 | 729.64 | ... | -0.06 | 0.08 | 0.06 | 0.66 | 0.51 | 1.19 | 1.31 | 3.37 | 3.90 | 2.04 |

4111 rows × 38 columns

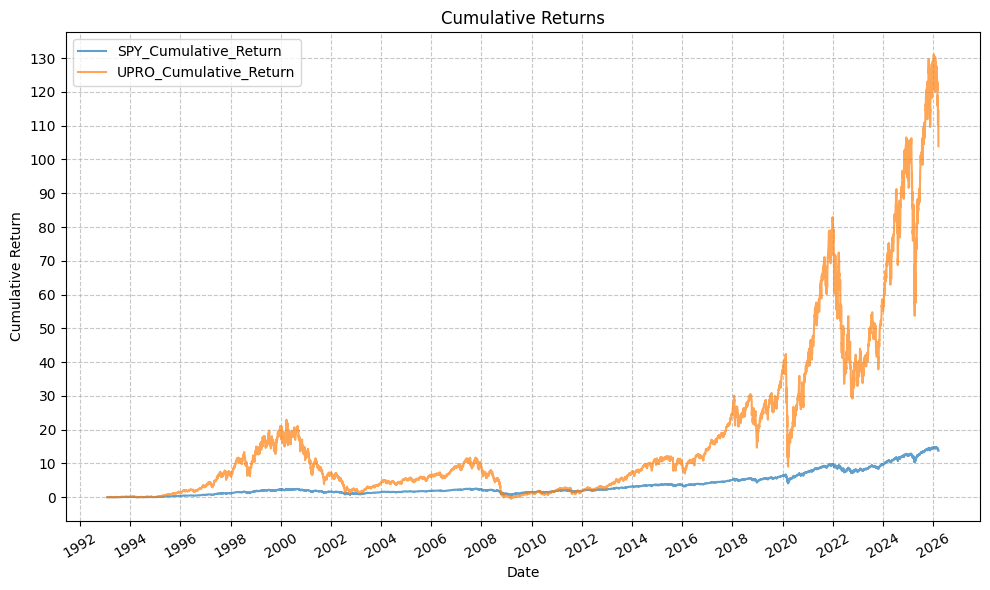

And now the plot for the cumulative returns:

plot_time_series(

df=qqq_tqqq_aligned,

plot_start_date=None,

plot_end_date=None,

plot_columns=["QQQ_Cumulative_Return", "TQQQ_Cumulative_Return"],

title="Cumulative Returns",

x_label="Date",

x_format="Year",

x_tick_spacing=1,

x_tick_start=None,

x_tick_rotation=30,

y_label="Cumulative Return",

y_format="Decimal",

y_format_decimal_places=0,

y_tick_spacing="Auto",

y_tick_rotation=0,

grid=True,

legend=True,

export_plot=False,

plot_file_name=None,

)

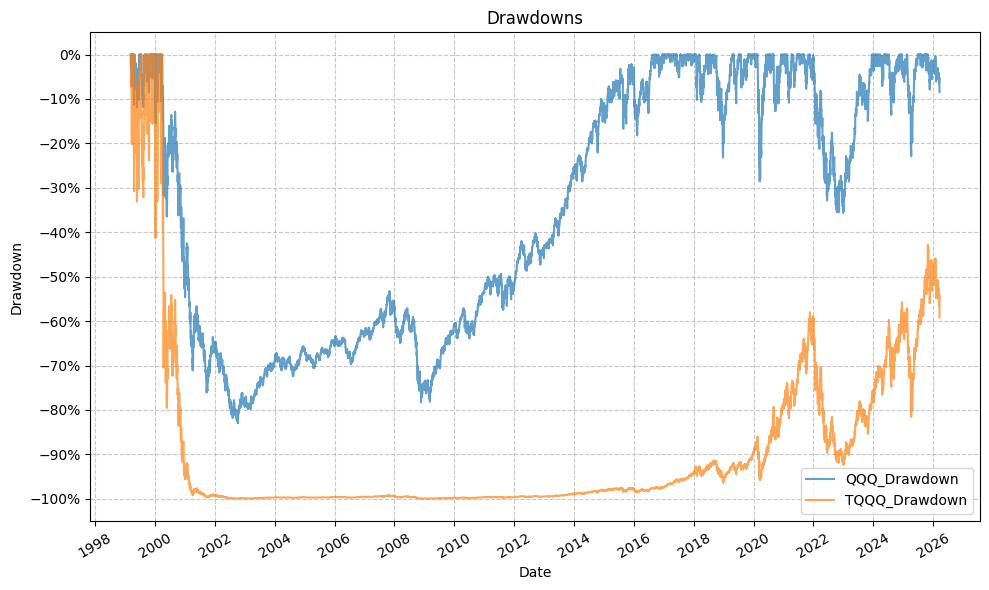

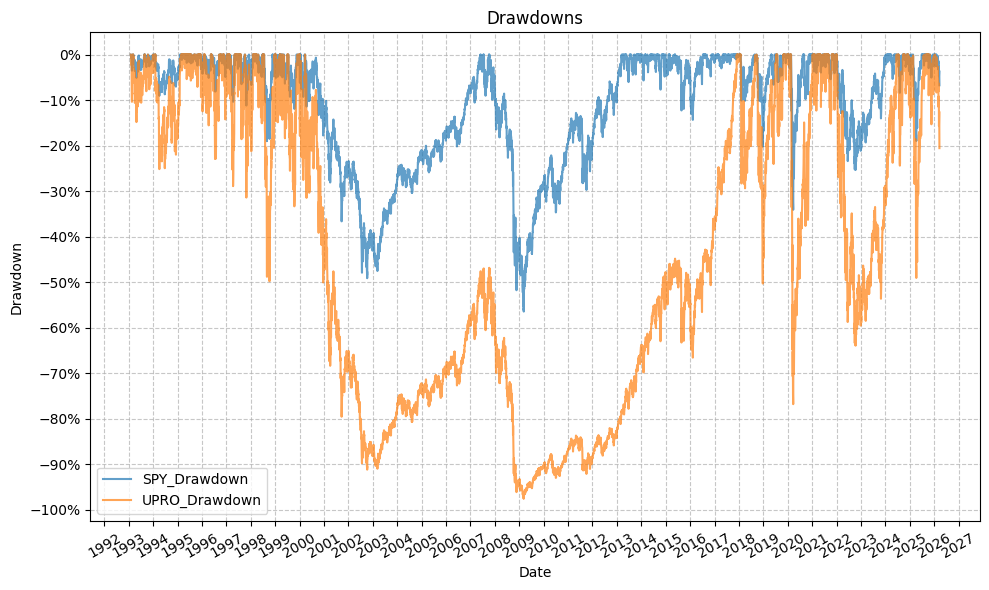

And the drawdown plot:

plot_time_series(

df=qqq_tqqq_aligned,

plot_start_date=None,

plot_end_date=None,

plot_columns=["QQQ_Drawdown", "TQQQ_Drawdown"],

title="Drawdowns",

x_label="Date",

x_format="Year",

x_tick_spacing=1,

x_tick_start=None,

x_tick_rotation=30,

y_label="Drawdown",

y_format="Percentage",

y_format_decimal_places=0,

y_tick_spacing="Auto",

y_tick_rotation=0,

grid=True,

legend=True,

export_plot=False,

plot_file_name=None,

)

Here is where we truly see the volatility of TQQQ relative to QQQ. In the past 5 years, TQQQ has had drawdowns of 50%, 60%, 70%, and 80%. While it has recovered to make new highs (with the exception of the current ~25% drawdown as of mid-March 2026), very few investors can endure those drawdowns and continue to hold their position. At the same time, we can see from the plot that a ~35% drawdown in QQQ equated to a ~80% drawdown in TQQQ, which is not in fact, 3x. So this tells us (which we already knew) that there is dispersion in the long-term returns relative to the short-term returns between the non-leveraged QQQ and 3x leveraged TQQQ. This idea is well documented in the financial literature as “volatility decay” or “volatility drag”. But, and this is the question we are trying to answer, how significant is this effect over various time horizons?

Summary Statistics (QQQ & TQQQ) #

Looking at the summary statistics further confirms our intuitions about the volatility and drawdowns.

qqq_sum_stats = summary_stats(

fund_list=["QQQ"],

df=qqq_tqqq_aligned[["QQQ_Return"]],

period="Daily",

use_calendar_days=False,

excel_export=False,

pickle_export=False,

output_confirmation=False,

)

tqqq_sum_stats = summary_stats(

fund_list=["TQQQ"],

df=qqq_tqqq_aligned[["TQQQ_Return"]],

period="Daily",

use_calendar_days=False,

excel_export=False,

pickle_export=False,

output_confirmation=False,

)

sum_stats = pd.concat([qqq_sum_stats, tqqq_sum_stats])

display(sum_stats)

| Annual Mean Return (Arithmetic) | Annualized Volatility | Annualized Sharpe Ratio | CAGR (Geometric) | Daily Max Return | Daily Max Return (Date) | Daily Min Return | Daily Min Return (Date) | Max Drawdown | Peak | Trough | Recovery Date | Calendar Days to Recovery | MAR Ratio | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| QQQ_Return | 0.19 | 0.21 | 0.94 | 0.19 | 0.12 | 2025-04-09 | -0.12 | 2020-03-16 | -0.36 | 2021-11-19 | 2022-12-28 | 2023-12-15 | 352 | 0.53 |

| TQQQ_Return | 0.55 | 0.61 | 0.90 | 0.44 | 0.35 | 2025-04-09 | -0.34 | 2020-03-16 | -0.82 | 2021-11-19 | 2022-12-28 | 2024-12-11 | 714 | 0.53 |

Note that these statistics are being run on the partially-adjusted close prices, which are not the true returns (due to not accounting for dividends), but they do give us a picture of the relative volatility and drawdowns of the two ETFs. The mean return for TQQQ is much higher than that of QQQ, but the volatility is also much higher, which is consistent with the idea of leverage amplifying both the up-side and down-side. The maximum drawdown for TQQQ is also much higher than that of QQQ, which again confirms our observations from the drawdown plot.

Also note that the daily maximum return for both funds occured during “Liberation Day” and the daily minimum return for both funds occured early on during the COVID-19 pandemic.

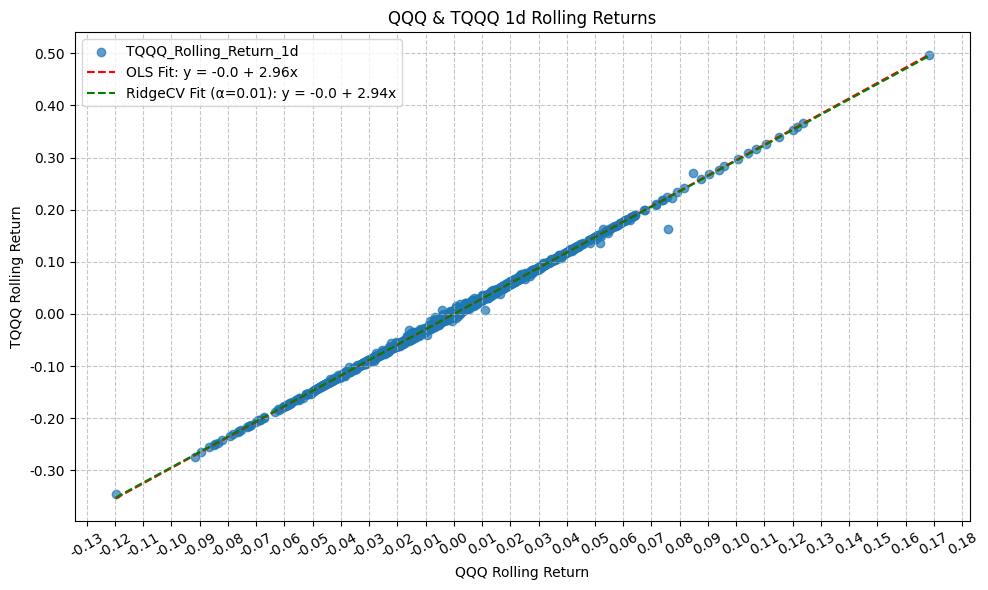

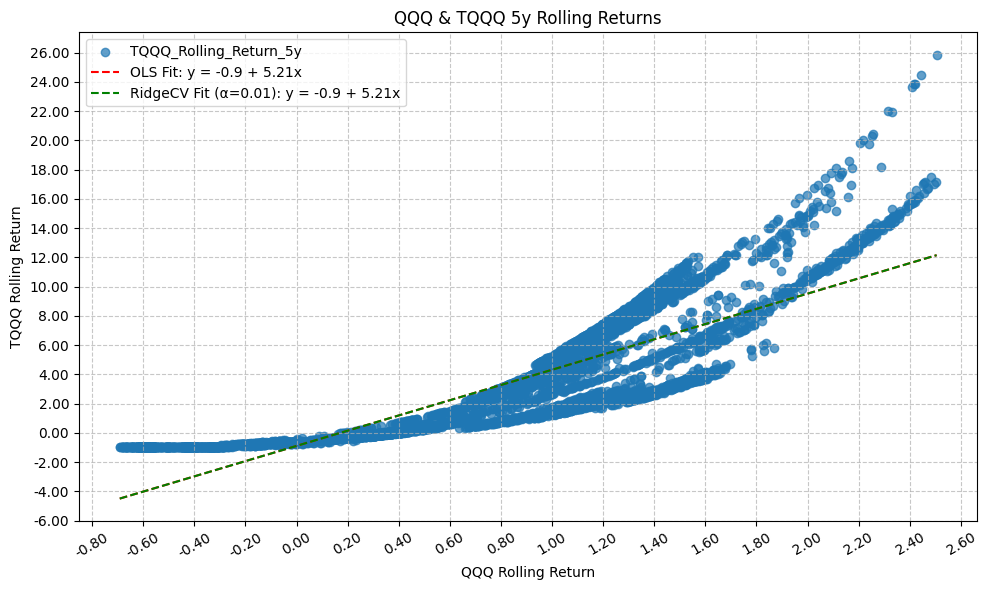

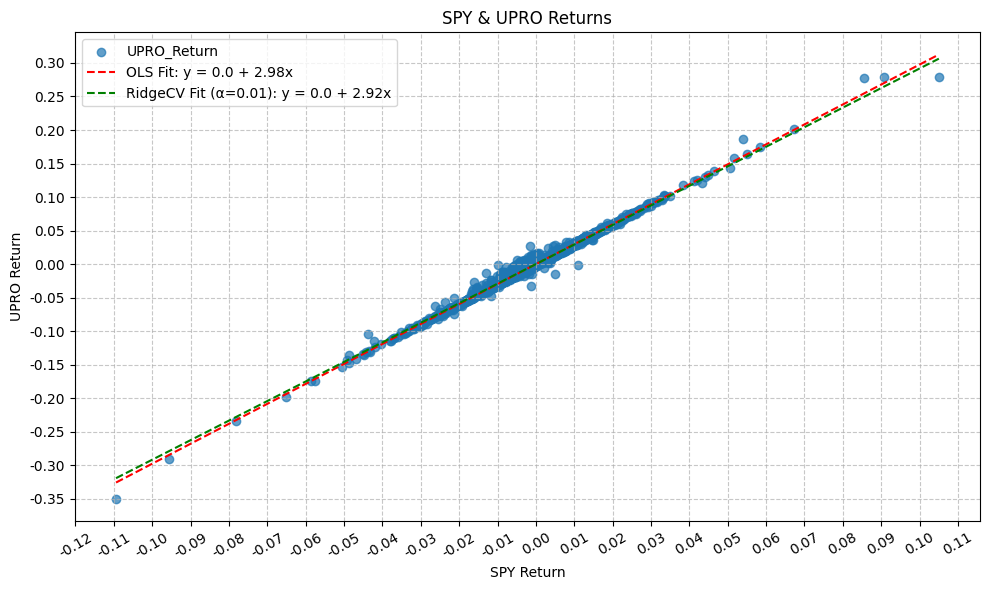

Plot Returns & Verify Beta (QQQ & TQQQ) #

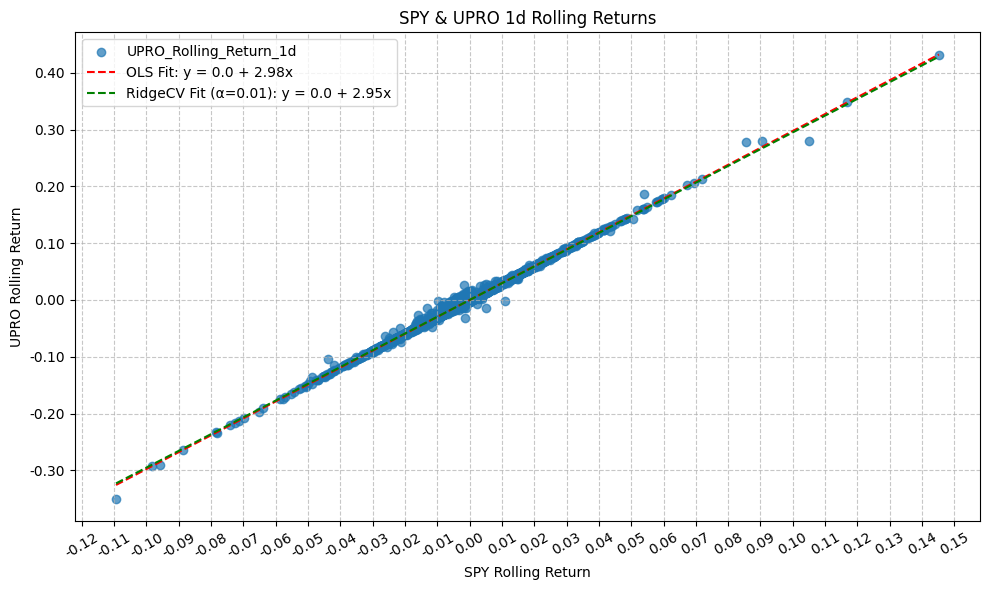

Before we look at the rolling returns, let us first verify that the daily returns for TQQQ are in fact ~3x those of QQQ. We can do that by plotting the daily returns for both funds against each other and running a linear regression to see if the beta is indeed ~3.

plot_scatter(

df=qqq_tqqq_aligned,

x_plot_column="QQQ_Return",

y_plot_columns=["TQQQ_Return"],

title="QQQ & TQQQ Returns",

x_label="QQQ Return",

x_format="Decimal",

x_format_decimal_places=2,

x_tick_spacing="Auto",

x_tick_start=None,

x_tick_rotation=30,

y_label="TQQQ Return",

y_format="Decimal",

y_format_decimal_places=2,

y_tick_spacing="Auto",

y_tick_rotation=0,

plot_OLS_regression_line=True,

OLS_column="TQQQ_Return",

plot_Ridge_regression_line=False,

Ridge_column=None,

plot_RidgeCV_regression_line=True,

RidgeCV_column="TQQQ_Return",

regression_constant=True,

grid=True,

legend=True,

export_plot=False,

plot_file_name=None,

)

model = run_regression(

df=qqq_tqqq_aligned,

x_plot_column="QQQ_Return",

y_plot_column="TQQQ_Return",

regression_model="OLS-statsmodels",

regression_constant=True,

)

print(model.summary())

OLS Regression Results

==============================================================================

Dep. Variable: TQQQ_Return R-squared: 0.997

Model: OLS Adj. R-squared: 0.997

Method: Least Squares F-statistic: 1.540e+06

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:31:49 Log-Likelihood: 19741.

No. Observations: 4110 AIC: -3.948e+04

Df Residuals: 4108 BIC: -3.946e+04

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const -8.798e-05 3.1e-05 -2.836 0.005 -0.000 -2.72e-05

QQQ_Return 2.9553 0.002 1240.806 0.000 2.951 2.960

==============================================================================

Omnibus: 5361.302 Durbin-Watson: 2.568

Prob(Omnibus): 0.000 Jarque-Bera (JB): 9467735.605

Skew: -6.352 Prob(JB): 0.00

Kurtosis: 237.786 Cond. No. 76.9

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Visually, this plot makes sense and we can see that there is a strong clustering of points, but we double check with the regression, regressing the TQQQ daily return (y) on the QQQ daily return (X).

Given the above result, with a coefficient of 2.96 and an R^2 of 0.997 (based on the statsmodels OLS regression), we can say that TQQQ does in fact return ~3x QQQ. We would also intuitively expect the coefficient to be 0, and it is nearly 0.

Interestingly, the coefficient varies between OLS and Ridge cross-validation, and both are less than 3.

Extrapolate Data (QQQ & TQQQ) #

With the above coefficient, we will now extrapolate the returns of QQQ to backfill the data from the inception of QQQ in 1999 to the inception of TQQQ in 2010 to expand our dataset of returns. For this, we’ll use the coefficient of 2.96 that we found in the regression results above.

# Set leverage multiplier based on regression coefficient

LEVERAGE_MULTIPLIER = model.params.iloc[1]

# Merge dataframes and extrapolate return values for QQQ back to 1999 using the leverage multiplier

qqq_tqqq_extrap = qqq[["QQQ_Close"]].merge(tqqq[["TQQQ_Close"]], left_index=True, right_index=True, how='left')

etfs = ["QQQ", "TQQQ"]

# Calculate cumulative returns

for etf in etfs:

qqq_tqqq_extrap[f"{etf}_Return"] = qqq_tqqq_extrap[f"{etf}_Close"].pct_change()

# Extrapolate TQQQ returns for missing values

qqq_tqqq_extrap["TQQQ_Return"] = qqq_tqqq_extrap["TQQQ_Return"].fillna(LEVERAGE_MULTIPLIER * qqq_tqqq_extrap["QQQ_Return"])

# Find the first valid TQQQ_Close index and value

first_valid_idx = qqq_tqqq_extrap['TQQQ_Close'].first_valid_index()

print(first_valid_idx)

first_valid_price = qqq_tqqq_extrap.loc[first_valid_idx, 'TQQQ_Close']

print(first_valid_price)

2010-02-11 00:00:00

0.21627600491046906

Before we extrapolate, let’s first look at the data we have for QQQ and TQQQ around the inception of TQQQ in 2010:

# Check values around the first valid index

pandas_set_decimal_places(4)

display(qqq_tqqq_extrap.loc["2010-02-08":"2010-02-13"])

| QQQ_Close | TQQQ_Close | QQQ_Return | TQQQ_Return | |

|---|---|---|---|---|

| Date | ||||

| 2010-02-08 | 42.6700 | NaN | -0.0072 | -0.0213 |

| 2010-02-09 | 43.1100 | NaN | 0.0103 | 0.0305 |

| 2010-02-10 | 43.0200 | NaN | -0.0021 | -0.0062 |

| 2010-02-11 | 43.6700 | 0.2163 | 0.0151 | 0.0447 |

| 2010-02-12 | 43.7600 | 0.2172 | 0.0021 | 0.0041 |

Now, backfill the data for the TQQQ close price:

# Iterate through the dataframe backwards

for i in range(qqq_tqqq_extrap.index.get_loc(first_valid_idx) - 1, -1, -1):

# The return that led to the price the next day

current_return = qqq_tqqq_extrap.iloc[i + 1]['TQQQ_Return']

# Get the next day's price

next_price = qqq_tqqq_extrap.iloc[i + 1]['TQQQ_Close']

# Price_{t} = Price_{t+1} / (1 + Return_{t})

qqq_tqqq_extrap.loc[qqq_tqqq_extrap.index[i], 'TQQQ_Close'] = next_price / (1 + current_return)

Finally, confirm the values are correct:

# Confirm values around the first valid index after extrapolation

display(qqq_tqqq_extrap.loc["2010-02-08":"2010-02-13"])

| QQQ_Close | TQQQ_Close | QQQ_Return | TQQQ_Return | |

|---|---|---|---|---|

| Date | ||||

| 2010-02-08 | 42.6700 | 0.2022 | -0.0072 | -0.0213 |

| 2010-02-09 | 43.1100 | 0.2083 | 0.0103 | 0.0305 |

| 2010-02-10 | 43.0200 | 0.2070 | -0.0021 | -0.0062 |

| 2010-02-11 | 43.6700 | 0.2163 | 0.0151 | 0.0447 |

| 2010-02-12 | 43.7600 | 0.2172 | 0.0021 | 0.0041 |

And the complete DataFrame with the extrapolated values:

pandas_set_decimal_places(2)

display(qqq_tqqq_extrap)

| QQQ_Close | TQQQ_Close | QQQ_Return | TQQQ_Return | |

|---|---|---|---|---|

| Date | ||||

| 1999-03-10 | 51.06 | 13.82 | NaN | NaN |

| 1999-03-11 | 51.31 | 14.02 | 0.00 | 0.01 |

| 1999-03-12 | 50.06 | 13.01 | -0.02 | -0.07 |

| 1999-03-15 | 51.50 | 14.12 | 0.03 | 0.08 |

| 1999-03-16 | 51.94 | 14.47 | 0.01 | 0.03 |

| ... | ... | ... | ... | ... |

| 2026-06-10 | 693.69 | 69.27 | -0.02 | -0.06 |

| 2026-06-11 | 717.12 | 76.01 | 0.03 | 0.10 |

| 2026-06-12 | 721.34 | 77.52 | 0.01 | 0.02 |

| 2026-06-15 | 744.00 | 84.59 | 0.03 | 0.09 |

| 2026-06-16 | 729.86 | 79.93 | -0.02 | -0.06 |

6860 rows × 4 columns

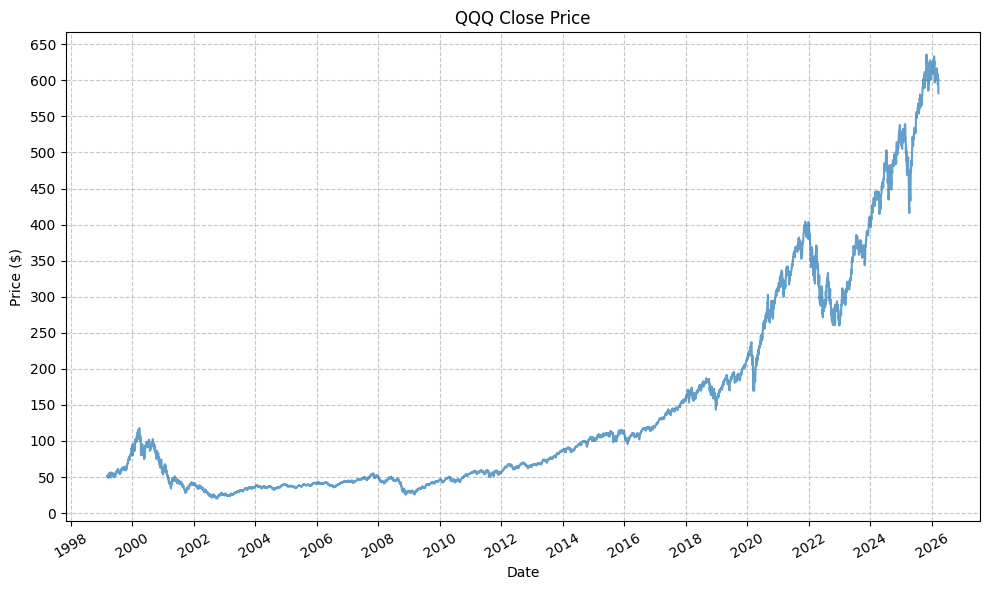

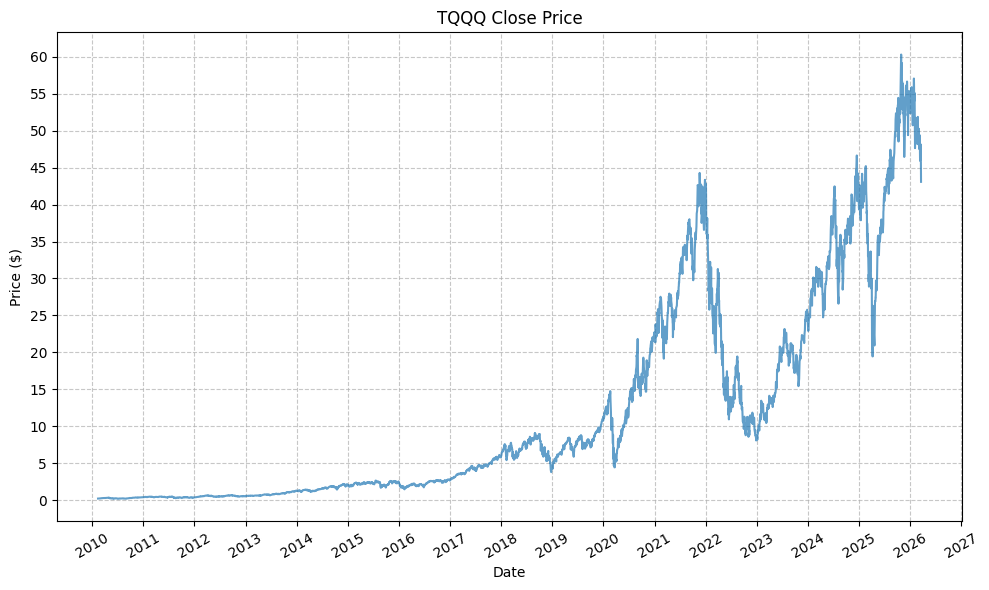

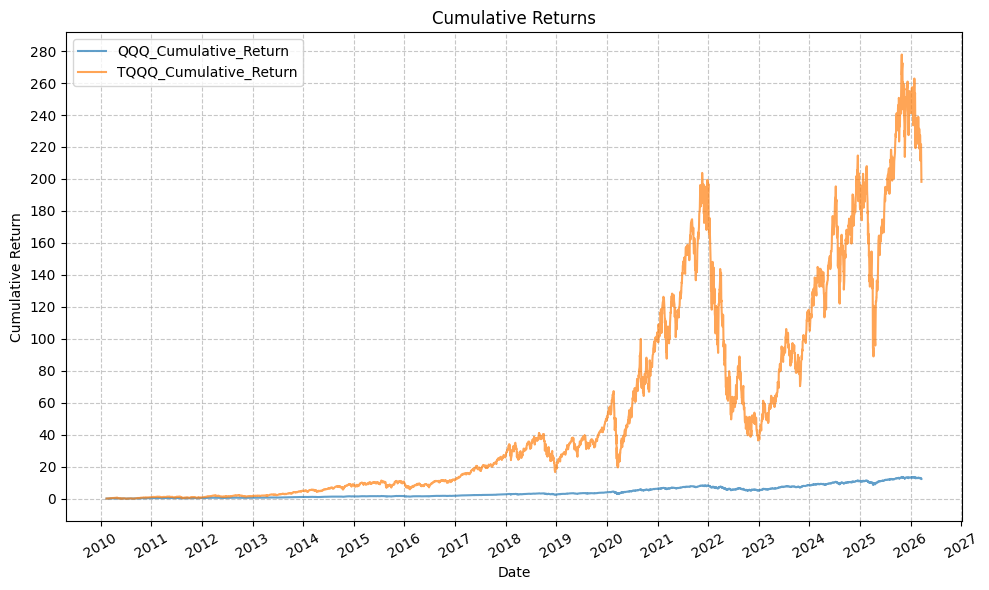

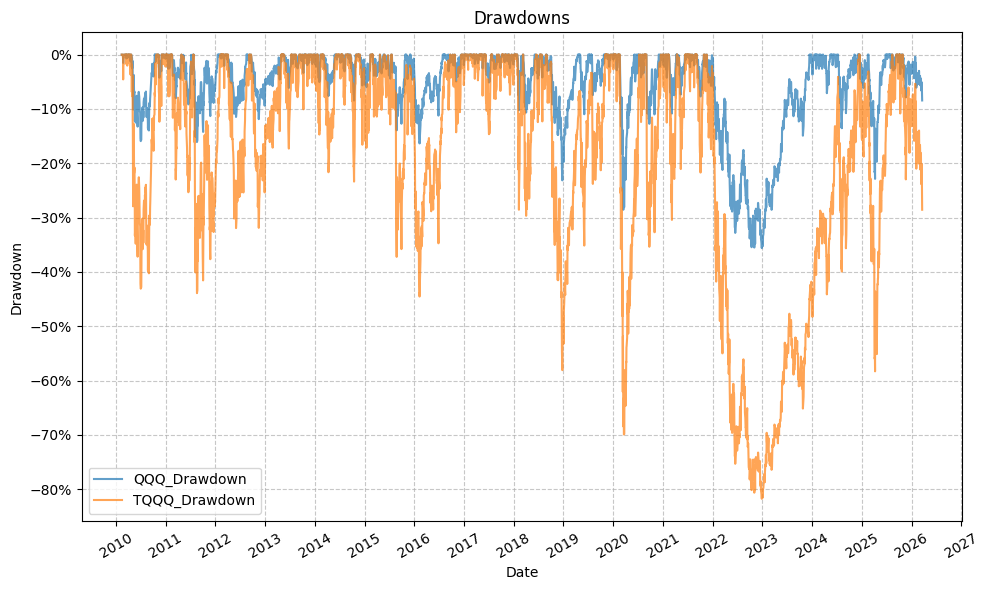

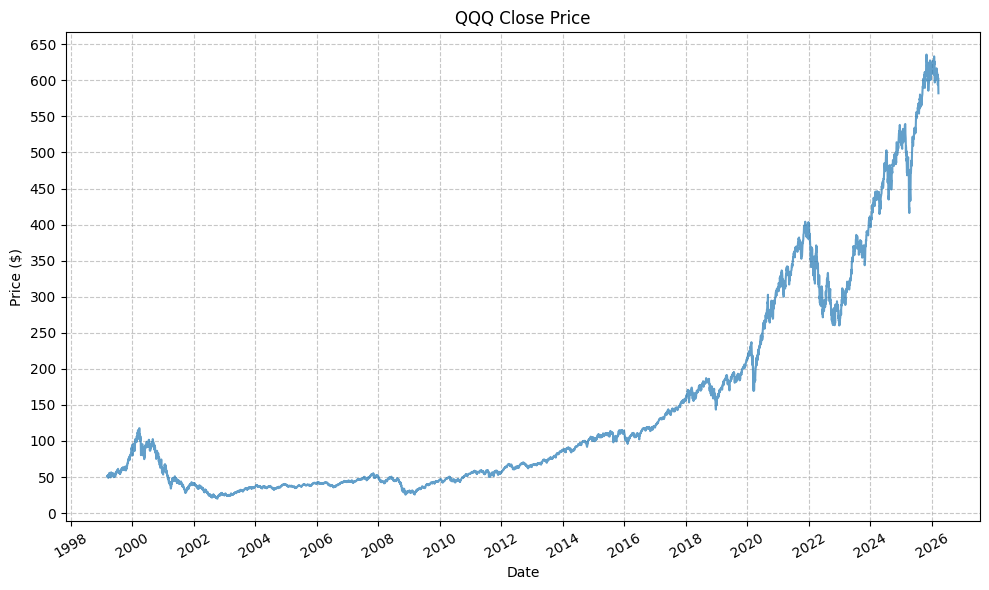

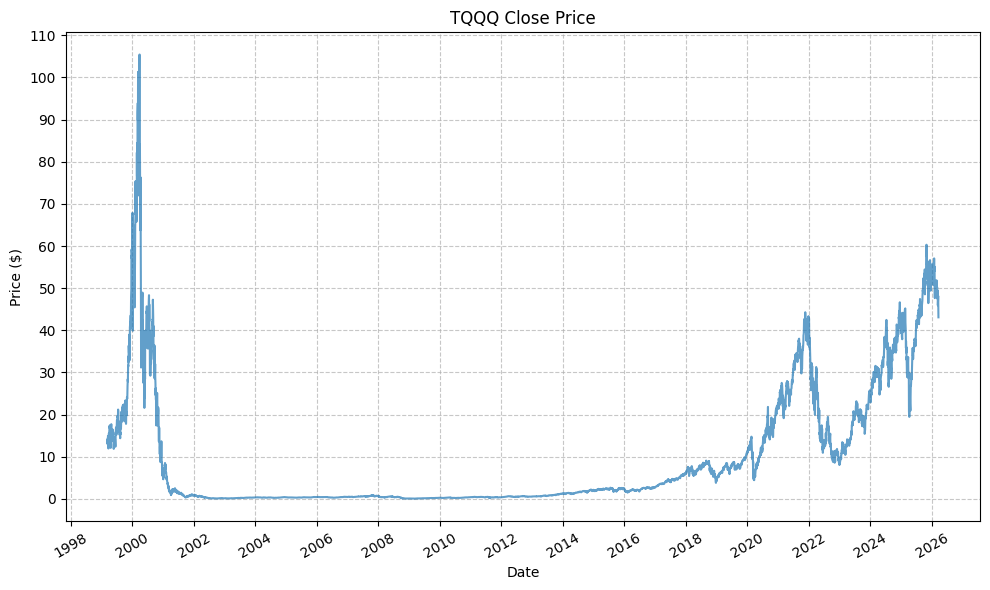

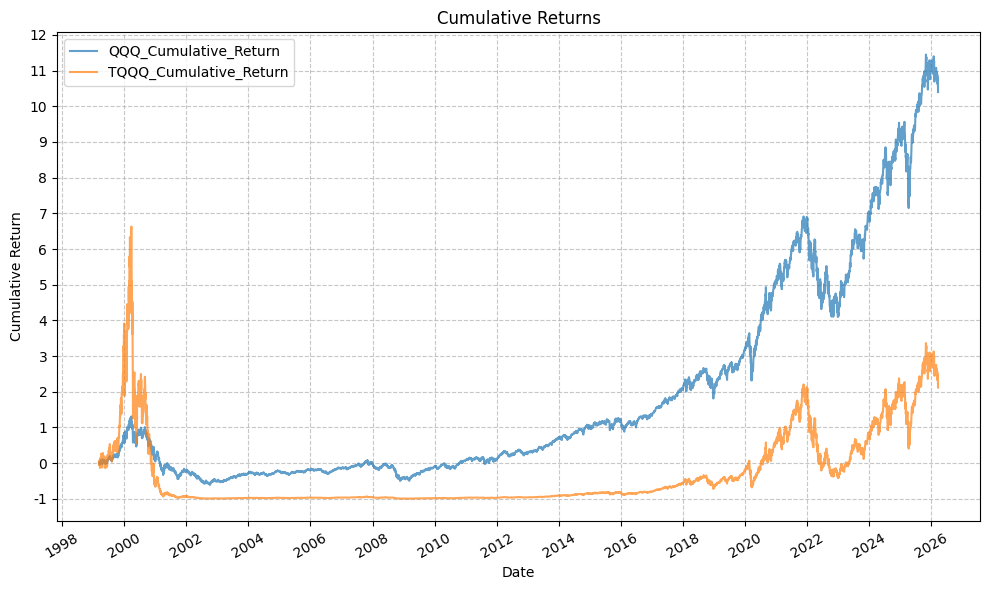

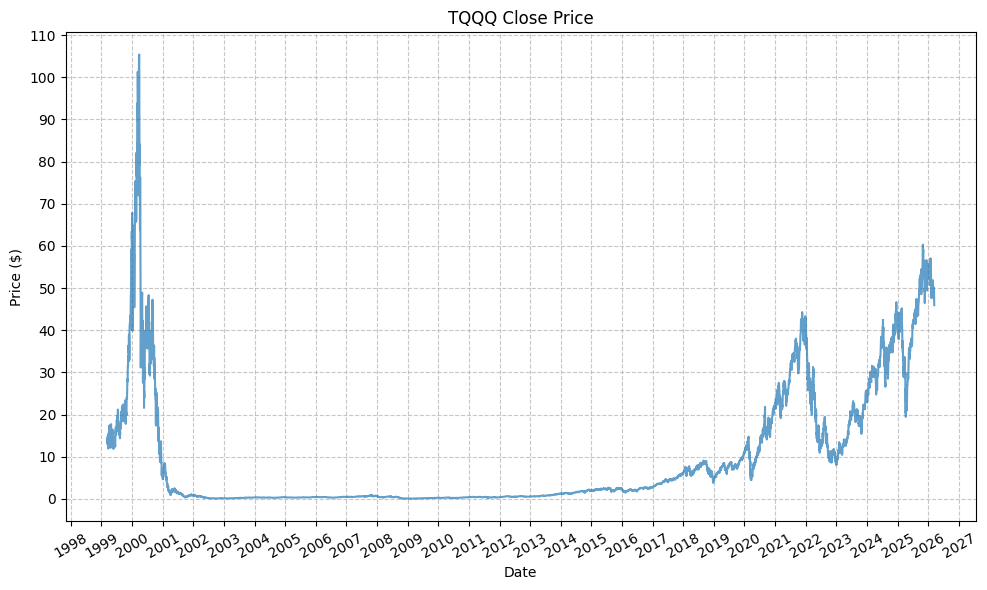

After the extrapolation, we now have the following plots for the prices, cumulative returns, and drawdowns:

etfs = ["QQQ", "TQQQ"]

# Calculate cumulative returns

for etf in etfs:

qqq_tqqq_extrap[f"{etf}_Return"] = qqq_tqqq_extrap[f"{etf}_Close"].pct_change()

qqq_tqqq_extrap[f"{etf}_Cumulative_Return"] = (1 + qqq_tqqq_extrap[f"{etf}_Return"]).cumprod() - 1

qqq_tqqq_extrap[f"{etf}_Cumulative_Return_Plus_One"] = 1 + qqq_tqqq_extrap[f"{etf}_Cumulative_Return"]

qqq_tqqq_extrap[f"{etf}_Rolling_Max"] = qqq_tqqq_extrap[f"{etf}_Cumulative_Return_Plus_One"].cummax()

qqq_tqqq_extrap[f"{etf}_Drawdown"] = qqq_tqqq_extrap[f"{etf}_Cumulative_Return_Plus_One"] / qqq_tqqq_extrap[f"{etf}_Rolling_Max"] - 1

qqq_tqqq_extrap.drop(columns=[f"{etf}_Cumulative_Return_Plus_One", f"{etf}_Rolling_Max"], inplace=True)

plot_time_series(

df=qqq_tqqq_extrap,

plot_start_date=None,

plot_end_date=None,

plot_columns=["QQQ_Close"],

title="QQQ Close Price",

x_label="Date",

x_format="Year",

x_tick_spacing=2,

x_tick_start=None,

x_tick_rotation=30,

y_label="Price ($)",

y_format="Decimal",

y_format_decimal_places=0,

y_tick_spacing="Auto",

y_tick_rotation=0,

grid=True,

legend=False,

export_plot=False,

plot_file_name=None,

)

plot_time_series(

df=qqq_tqqq_extrap,

plot_start_date=None,

plot_end_date=None,

plot_columns=["TQQQ_Close"],

title="TQQQ Close Price",

x_label="Date",

x_format="Year",

x_tick_spacing=2,

x_tick_start=None,

x_tick_rotation=30,

y_label="Price ($)",

y_format="Decimal",

y_format_decimal_places=0,

y_tick_spacing="Auto",

y_tick_rotation=0,

grid=True,

legend=False,

export_plot=False,

plot_file_name=None,

)

plot_time_series(

df=qqq_tqqq_extrap,

plot_start_date=None,

plot_end_date=None,

plot_columns=["QQQ_Cumulative_Return", "TQQQ_Cumulative_Return"],

title="Cumulative Returns",

x_label="Date",

x_format="Year",

x_tick_spacing=2,

x_tick_start=None,

x_tick_rotation=30,

y_label="Cumulative Return",

y_format="Decimal",

y_format_decimal_places=0,

y_tick_spacing="Auto",

y_tick_rotation=0,

grid=True,

legend=True,

export_plot=False,

plot_file_name=None,

)

plot_time_series(

df=qqq_tqqq_extrap,

plot_start_date=None,

plot_end_date=None,

plot_columns=["QQQ_Drawdown", "TQQQ_Drawdown"],

title="Drawdowns",

x_label="Date",

x_format="Year",

x_tick_spacing=2,

x_tick_start=None,

x_tick_rotation=30,

y_label="Drawdown",

y_format="Percentage",

y_format_decimal_places=0,

y_tick_spacing="Auto",

y_tick_rotation=0,

grid=True,

legend=True,

export_plot=False,

plot_file_name=None,

)

qqq_extrap_sum_stats = summary_stats(

fund_list=["QQQ"],

df=qqq_tqqq_extrap[["QQQ_Return"]],

period="Daily",

use_calendar_days=False,

excel_export=False,

pickle_export=False,

output_confirmation=False,

)

tqqq_extrap_sum_stats = summary_stats(

fund_list=["TQQQ"],

df=qqq_tqqq_extrap[["TQQQ_Return"]],

period="Daily",

use_calendar_days=False,

excel_export=False,

pickle_export=False,

output_confirmation=False,

)

sum_stats = pd.concat([qqq_sum_stats, tqqq_sum_stats, qqq_extrap_sum_stats, tqqq_extrap_sum_stats])

sum_stats.index = ["QQQ (2010 - Present)", "TQQQ (2010 - Present)", "QQQ (1999 - Present)", "TQQQ Extrapolated (1999 - Present)"]

display(sum_stats)

| Annual Mean Return (Arithmetic) | Annualized Volatility | Annualized Sharpe Ratio | CAGR (Geometric) | Daily Max Return | Daily Max Return (Date) | Daily Min Return | Daily Min Return (Date) | Max Drawdown | Peak | Trough | Recovery Date | Calendar Days to Recovery | MAR Ratio | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| QQQ (2010 - Present) | 0.19 | 0.21 | 0.94 | 0.19 | 0.12 | 2025-04-09 | -0.12 | 2020-03-16 | -0.36 | 2021-11-19 | 2022-12-28 | 2023-12-15 | 352.00 | 0.53 |

| TQQQ (2010 - Present) | 0.55 | 0.61 | 0.90 | 0.44 | 0.35 | 2025-04-09 | -0.34 | 2020-03-16 | -0.82 | 2021-11-19 | 2022-12-28 | 2024-12-11 | 714.00 | 0.53 |

| QQQ (1999 - Present) | 0.13 | 0.27 | 0.50 | 0.10 | 0.17 | 2001-01-03 | -0.12 | 2020-03-16 | -0.83 | 2000-03-27 | 2002-10-09 | 2016-09-06 | 5081.00 | 0.12 |

| TQQQ Extrapolated (1999 - Present) | 0.38 | 0.80 | 0.48 | 0.07 | 0.50 | 2001-01-03 | -0.34 | 2020-03-16 | -1.00 | 2000-03-27 | 2009-03-09 | NaT | NaN | 0.07 |

A few quick comments before we look at rolling returns:

- The cumulative return for TQQQ is less than that of QQQ - which is starkly different from the plot beginning in 2010 at the inception of TQQQ. So the return path really matters here.

- The drawdown for TQQQ is nearly 100%… which also represents nearly a total loss of capital for any allocation to the extrap-TQQQ. Furthermore, as we walk forward through time (2002, 2003, … etc.), there is really no reason to believe that the returns would ever recover (even partially). So while we can look at the rolling returns and see how they compare to the 3x return of QQQ, we should keep in mind that the drawdown post-1999 is so severe that it would be very difficult for any investor to hold through it.

- The recovery time for QQQ was more than 5,000 days, or ~14 years. Note that this is calendar days, not trading days. While returns have been great for QQQ since 2016, the 14 year dry spell is a reminder of just how large the tech bubble was.

- The extrapolated TQQQ data remains in a drawdown and has never recovered to make new highs (as of March 2026).

Plot Rolling Returns (QQQ & TQQQ) #

Next, we will consider the following:

- Histogram and scatter plots of the rolling returns of QQQ and TQQQ

- Regressions to establish a “leverage factor” for the rolling returns

- The deviation from a 3x return for each time period

For this set of regressions, we will also allow the constant. First, we need the rolling returns for various time periods:

# Define rolling windows in trading days

rolling_windows = {

'1d': 1, # 1 day

'1w': 5, # 1 week (5 trading days)

'1m': 21, # 1 month (~21 trading days)

'3m': 63, # 3 months (~63 trading days)

'6m': 126, # 6 months (~126 trading days)

'1y': 252, # 1 year (~252 trading days)

'2y': 504, # 2 years (~504 trading days)

'3y': 756, # 3 years (~756 trading days)

'4y': 1008, # 4 years (~1008 trading days)

'5y': 1260, # 5 years (~1260 trading days)

}

# Calculate rolling returns for each ETF and each window

for etf in etfs:

for period_name, window in rolling_windows.items():

qqq_tqqq_extrap[f"{etf}_Rolling_Return_{period_name}"] = (

qqq_tqqq_extrap[f"{etf}_Close"].pct_change(periods=window)

)

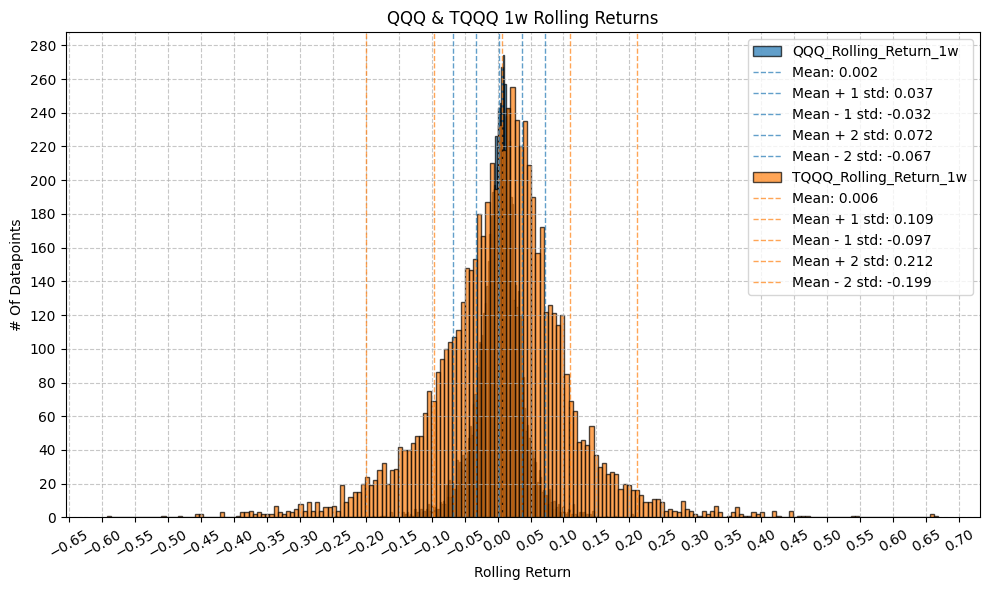

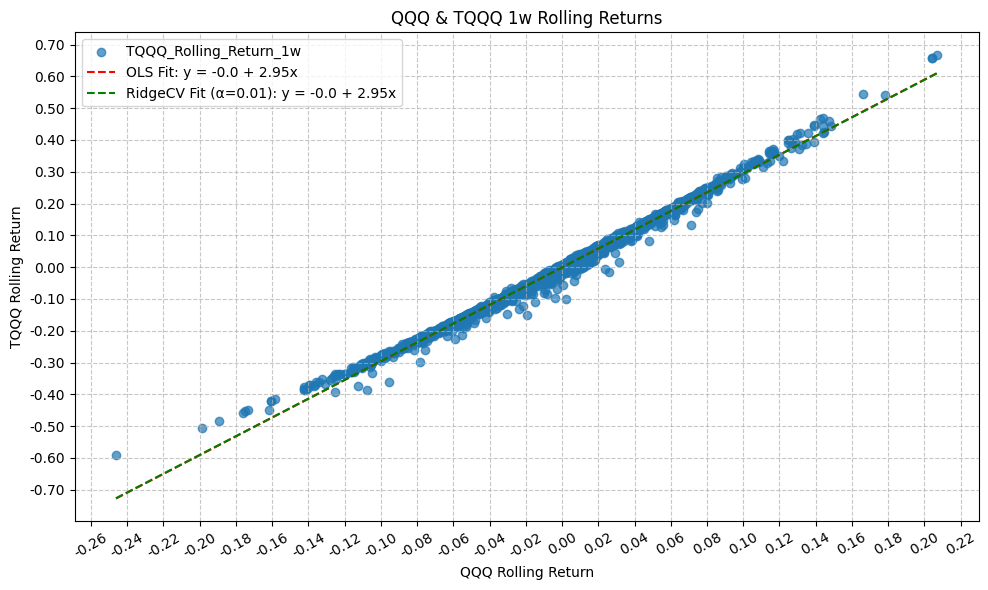

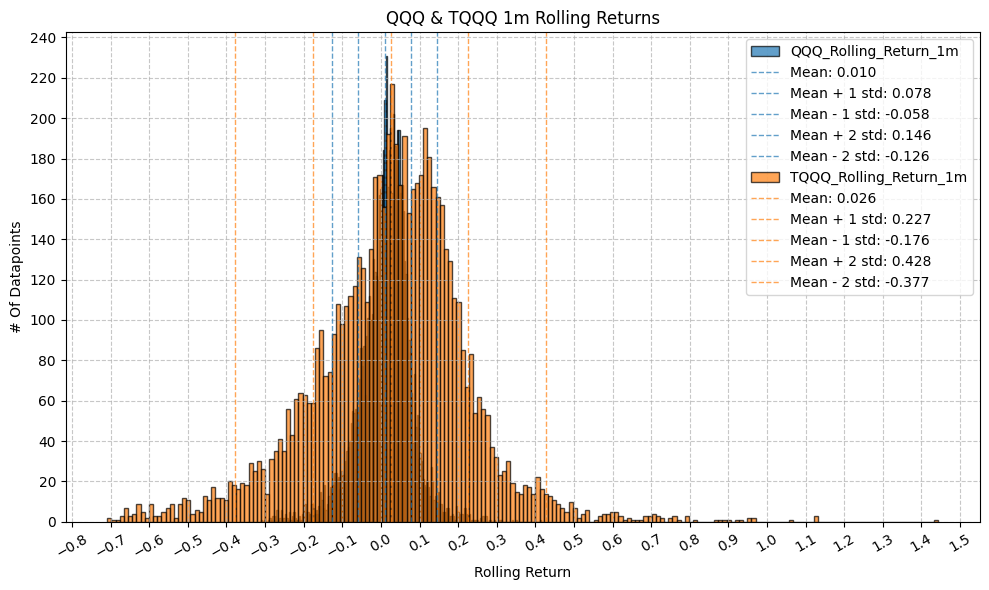

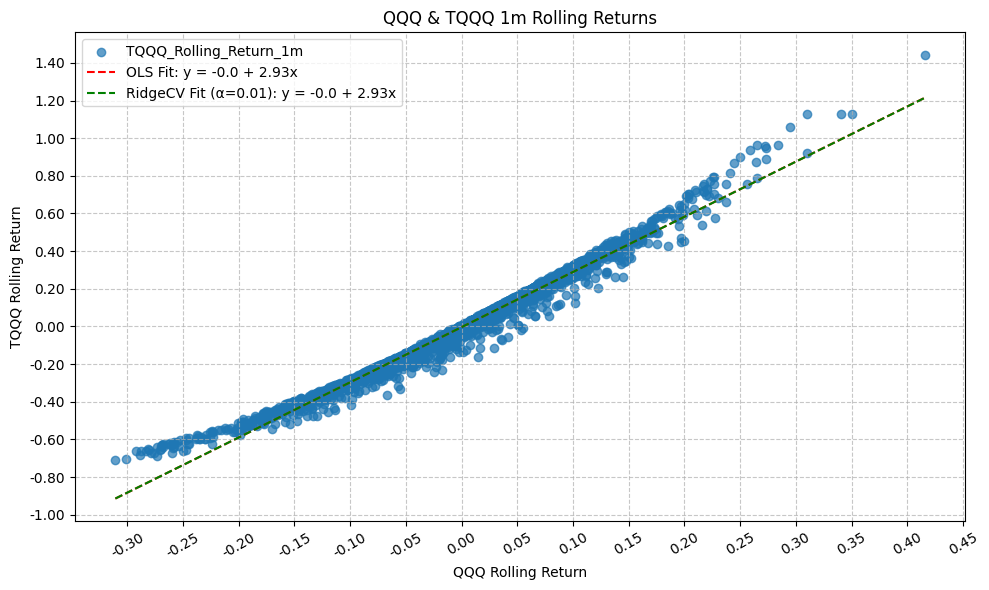

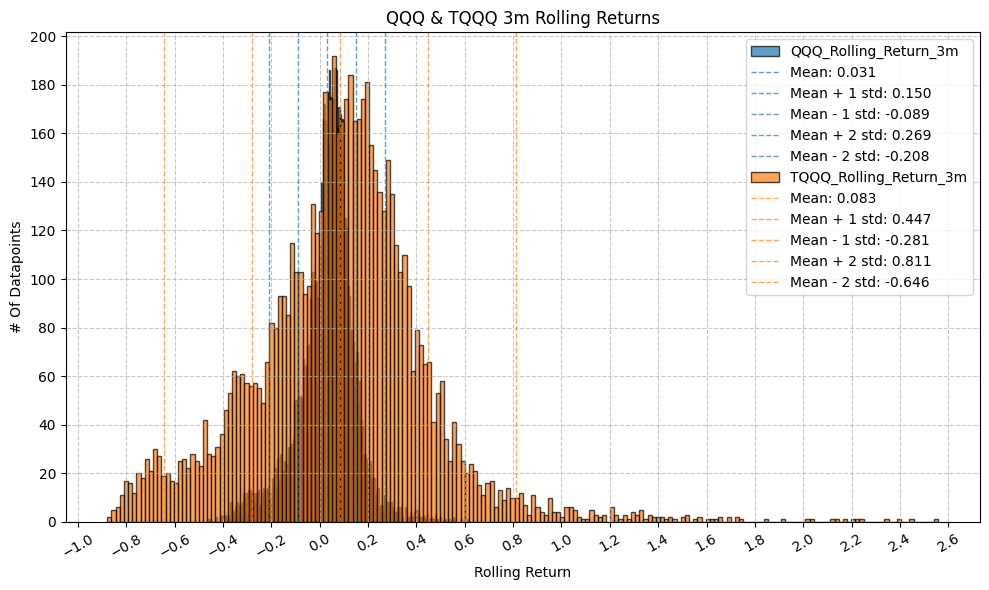

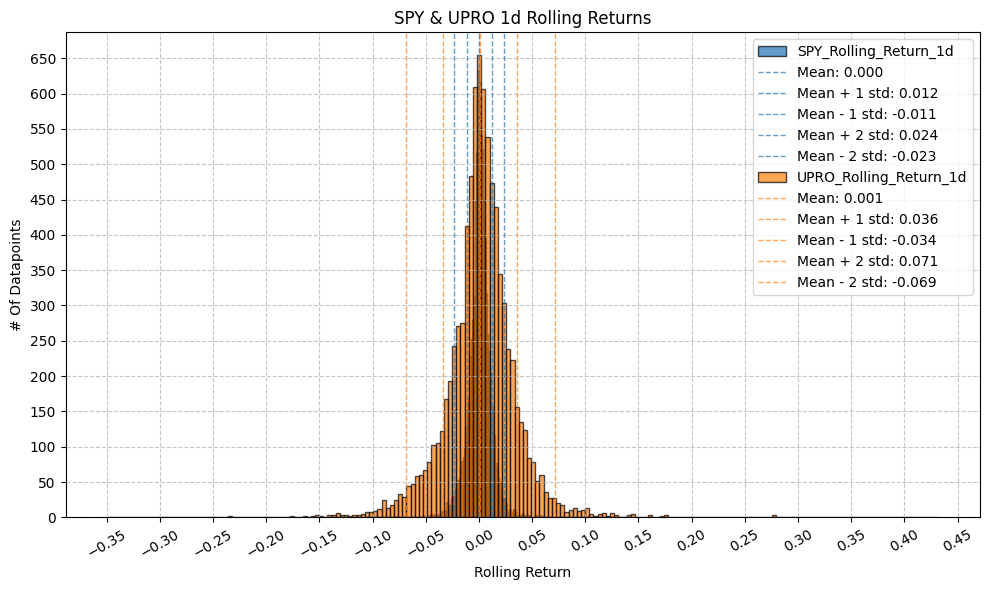

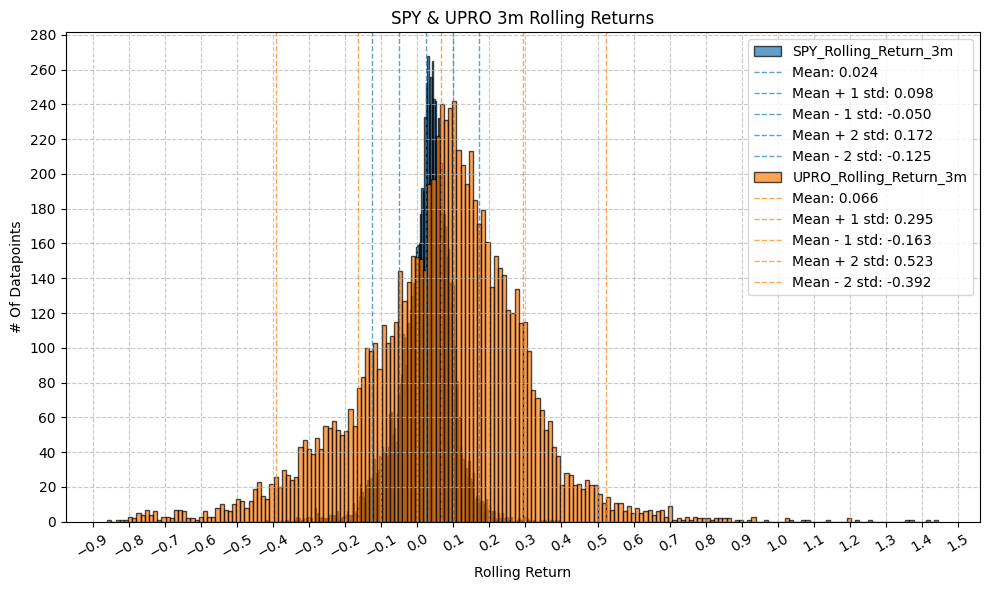

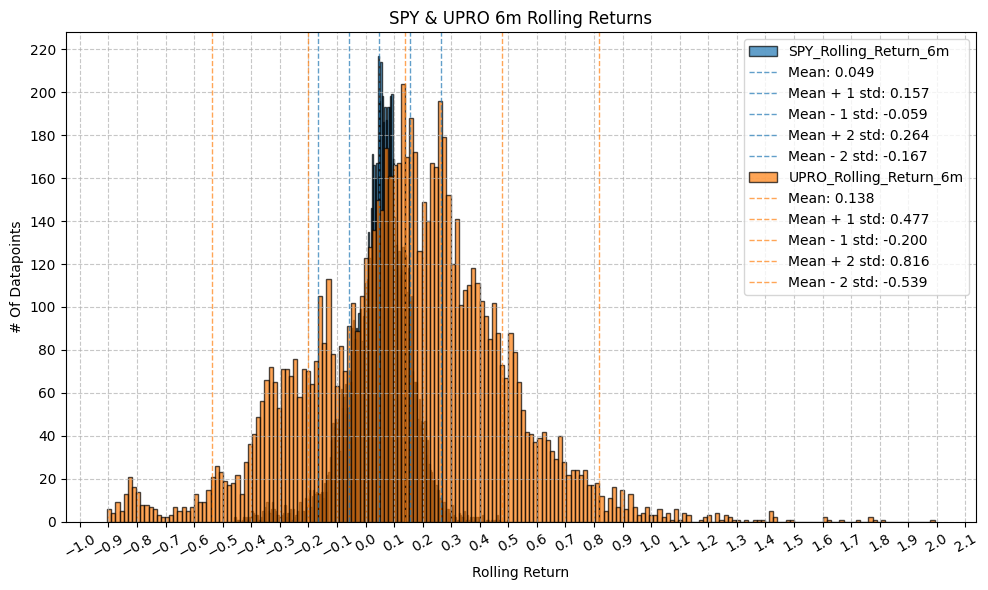

This gives us the following series of histograms, scatter plots, and regression model results:

# Create a dataframe to hold rolling returns stats

rolling_returns_stats = pd.DataFrame()

for period_name, window in rolling_windows.items():

plot_histogram(

df=qqq_tqqq_extrap,

plot_columns=[f"QQQ_Rolling_Return_{period_name}", f"TQQQ_Rolling_Return_{period_name}"],

title=f"QQQ & TQQQ {period_name} Rolling Returns",

x_label="Rolling Return",

x_tick_spacing="Auto",

x_tick_rotation=30,

y_label="# Of Datapoints",

y_tick_spacing="Auto",

y_tick_rotation=0,

grid=True,

legend=True,

export_plot=False,

plot_file_name=None,

)

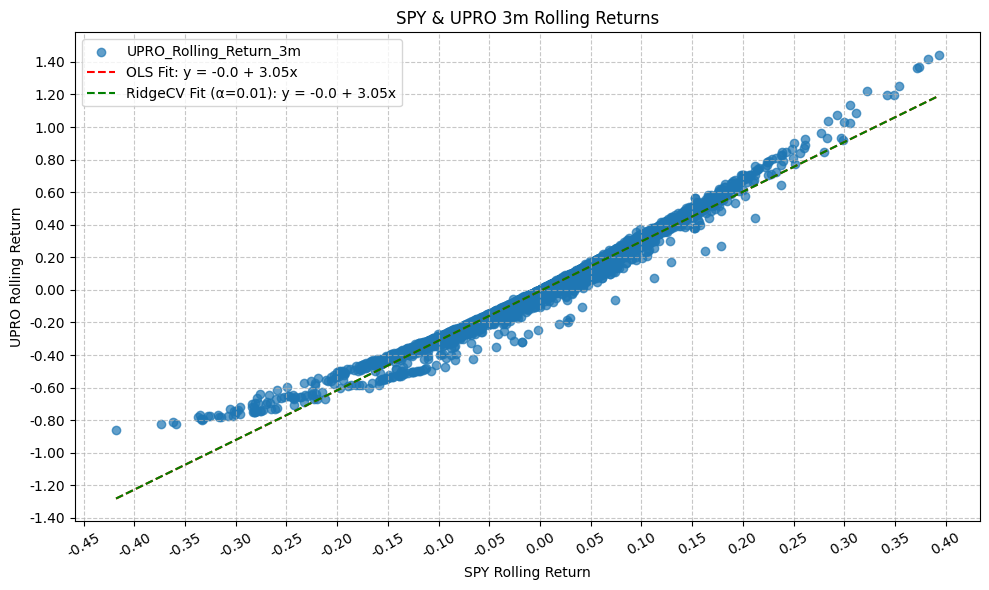

plot_scatter(

df=qqq_tqqq_extrap,

x_plot_column=f"QQQ_Rolling_Return_{period_name}",

y_plot_columns=[f"TQQQ_Rolling_Return_{period_name}"],

title=f"QQQ & TQQQ {period_name} Rolling Returns",

x_label="QQQ Rolling Return",

x_format="Decimal",

x_format_decimal_places=2,

x_tick_spacing="Auto",

x_tick_start=None,

x_tick_rotation=30,

y_label="TQQQ Rolling Return",

y_format="Decimal",

y_format_decimal_places=2,

y_tick_spacing="Auto",

y_tick_rotation=0,

plot_OLS_regression_line=True,

OLS_column=f"TQQQ_Rolling_Return_{period_name}",

plot_Ridge_regression_line=False,

Ridge_column=None,

plot_RidgeCV_regression_line=True,

RidgeCV_column=f"TQQQ_Rolling_Return_{period_name}",

regression_constant=True,

grid=True,

legend=True,

export_plot=False,

plot_file_name=None,

)

# Run OLS regression with statsmodels

model = run_regression(

df=qqq_tqqq_extrap,

x_plot_column=f"QQQ_Rolling_Return_{period_name}",

y_plot_column=f"TQQQ_Rolling_Return_{period_name}",

regression_model="OLS-statsmodels",

regression_constant=True,

)

print(model.summary())

# Add the regression results to the rolling returns stats dataframe

intercept = model.params.iloc[0]

intercept_pvalue = model.pvalues.iloc[0] # p-value for Intercept

slope = model.params.iloc[1]

slope_pvalue = model.pvalues.iloc[1] # p-value for QQQ_Return

r_squared = model.rsquared

# Calc skew

return_ratio = qqq_tqqq_extrap[f'TQQQ_Rolling_Return_{period_name}'] / qqq_tqqq_extrap[f'QQQ_Rolling_Return_{period_name}']

skew = return_ratio.skew()

# Calc conditional symmetry

up_markets = qqq_tqqq_extrap[qqq_tqqq_extrap[f'QQQ_Rolling_Return_{period_name}'] > 0]

down_markets = qqq_tqqq_extrap[qqq_tqqq_extrap[f'QQQ_Rolling_Return_{period_name}'] <= 0]

avg_beta_up = (up_markets[f'TQQQ_Rolling_Return_{period_name}'] / up_markets[f'QQQ_Rolling_Return_{period_name}']).mean()

avg_beta_down = (down_markets[f'TQQQ_Rolling_Return_{period_name}'] / down_markets[f'QQQ_Rolling_Return_{period_name}']).mean()

asymmetry = avg_beta_up - avg_beta_down

rolling_returns_slope_int = pd.DataFrame({

"Period": period_name,

"Intercept": [intercept],

# "Intercept_PValue": [intercept_pvalue],

"Slope": [slope],

# "Slope_PValue": [slope_pvalue],

"R_Squared": [r_squared],

"Return Skew": [skew],

"Average Upside Beta": [avg_beta_up],

"Average Downside Beta": [avg_beta_down],

"Asymmetry": [asymmetry]

})

rolling_returns_stats = pd.concat([rolling_returns_stats, rolling_returns_slope_int])

OLS Regression Results

==================================================================================

Dep. Variable: TQQQ_Rolling_Return_1d R-squared: 0.999

Model: OLS Adj. R-squared: 0.999

Method: Least Squares F-statistic: 7.303e+06

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:31:57 Log-Likelihood: 34698.

No. Observations: 6859 AIC: -6.939e+04

Df Residuals: 6857 BIC: -6.938e+04

Df Model: 1

Covariance Type: nonrobust

=========================================================================================

coef std err t P>|t| [0.025 0.975]

-----------------------------------------------------------------------------------------

const -5.27e-05 1.86e-05 -2.837 0.005 -8.91e-05 -1.63e-05

QQQ_Rolling_Return_1d 2.9553 0.001 2702.435 0.000 2.953 2.957

==============================================================================

Omnibus: 10277.277 Durbin-Watson: 2.566

Prob(Omnibus): 0.000 Jarque-Bera (JB): 44417091.716

Skew: -8.263 Prob(JB): 0.00

Kurtosis: 396.884 Cond. No. 58.9

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

==================================================================================

Dep. Variable: TQQQ_Rolling_Return_1w R-squared: 0.994

Model: OLS Adj. R-squared: 0.994

Method: Least Squares F-statistic: 1.134e+06

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:32:01 Log-Likelihood: 23396.

No. Observations: 6855 AIC: -4.679e+04

Df Residuals: 6853 BIC: -4.677e+04

Df Model: 1

Covariance Type: nonrobust

=========================================================================================

coef std err t P>|t| [0.025 0.975]

-----------------------------------------------------------------------------------------

const -0.0008 9.65e-05 -8.403 0.000 -0.001 -0.001

QQQ_Rolling_Return_1w 2.9532 0.003 1064.980 0.000 2.948 2.959

==============================================================================

Omnibus: 2863.007 Durbin-Watson: 0.931

Prob(Omnibus): 0.000 Jarque-Bera (JB): 576171.657

Skew: -0.858 Prob(JB): 0.00

Kurtosis: 47.881 Cond. No. 28.8

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

==================================================================================

Dep. Variable: TQQQ_Rolling_Return_1m R-squared: 0.982

Model: OLS Adj. R-squared: 0.982

Method: Least Squares F-statistic: 3.747e+05

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:32:05 Log-Likelihood: 14971.

No. Observations: 6839 AIC: -2.994e+04

Df Residuals: 6837 BIC: -2.992e+04

Df Model: 1

Covariance Type: nonrobust

=========================================================================================

coef std err t P>|t| [0.025 0.975]

-----------------------------------------------------------------------------------------

const -0.0036 0.000 -10.803 0.000 -0.004 -0.003

QQQ_Rolling_Return_1m 2.9365 0.005 612.153 0.000 2.927 2.946

==============================================================================

Omnibus: 1652.780 Durbin-Watson: 0.293

Prob(Omnibus): 0.000 Jarque-Bera (JB): 67847.108

Skew: 0.383 Prob(JB): 0.00

Kurtosis: 18.411 Cond. No. 14.6

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

==================================================================================

Dep. Variable: TQQQ_Rolling_Return_3m R-squared: 0.959

Model: OLS Adj. R-squared: 0.959

Method: Least Squares F-statistic: 1.577e+05

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:32:09 Log-Likelihood: 8045.5

No. Observations: 6797 AIC: -1.609e+04

Df Residuals: 6795 BIC: -1.607e+04

Df Model: 1

Covariance Type: nonrobust

=========================================================================================

coef std err t P>|t| [0.025 0.975]

-----------------------------------------------------------------------------------------

const -0.0083 0.001 -8.979 0.000 -0.010 -0.007

QQQ_Rolling_Return_3m 2.9871 0.008 397.059 0.000 2.972 3.002

==============================================================================

Omnibus: 3498.049 Durbin-Watson: 0.105

Prob(Omnibus): 0.000 Jarque-Bera (JB): 80662.481

Skew: 1.963 Prob(JB): 0.00

Kurtosis: 19.414 Cond. No. 8.38

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

==================================================================================

Dep. Variable: TQQQ_Rolling_Return_6m R-squared: 0.916

Model: OLS Adj. R-squared: 0.916

Method: Least Squares F-statistic: 7.321e+04

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:32:12 Log-Likelihood: 2661.5

No. Observations: 6734 AIC: -5319.

Df Residuals: 6732 BIC: -5305.

Df Model: 1

Covariance Type: nonrobust

=========================================================================================

coef std err t P>|t| [0.025 0.975]

-----------------------------------------------------------------------------------------

const -0.0102 0.002 -4.853 0.000 -0.014 -0.006

QQQ_Rolling_Return_6m 3.0396 0.011 270.569 0.000 3.018 3.062

==============================================================================

Omnibus: 3714.404 Durbin-Watson: 0.056

Prob(Omnibus): 0.000 Jarque-Bera (JB): 61899.283

Skew: 2.278 Prob(JB): 0.00

Kurtosis: 17.137 Cond. No. 5.68

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

==================================================================================

Dep. Variable: TQQQ_Rolling_Return_1y R-squared: 0.881

Model: OLS Adj. R-squared: 0.881

Method: Least Squares F-statistic: 4.869e+04

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:32:16 Log-Likelihood: -883.92

No. Observations: 6608 AIC: 1772.

Df Residuals: 6606 BIC: 1785.

Df Model: 1

Covariance Type: nonrobust

=========================================================================================

coef std err t P>|t| [0.025 0.975]

-----------------------------------------------------------------------------------------

const 0.0191 0.004 5.072 0.000 0.012 0.027

QQQ_Rolling_Return_1y 2.8417 0.013 220.652 0.000 2.816 2.867

==============================================================================

Omnibus: 3502.694 Durbin-Watson: 0.037

Prob(Omnibus): 0.000 Jarque-Bera (JB): 67965.448

Skew: 2.104 Prob(JB): 0.00

Kurtosis: 18.138 Cond. No. 3.85

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

==================================================================================

Dep. Variable: TQQQ_Rolling_Return_2y R-squared: 0.847

Model: OLS Adj. R-squared: 0.847

Method: Least Squares F-statistic: 3.529e+04

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:32:20 Log-Likelihood: -4464.1

No. Observations: 6356 AIC: 8932.

Df Residuals: 6354 BIC: 8946.

Df Model: 1

Covariance Type: nonrobust

=========================================================================================

coef std err t P>|t| [0.025 0.975]

-----------------------------------------------------------------------------------------

const 0.0068 0.007 0.923 0.356 -0.008 0.021

QQQ_Rolling_Return_2y 3.1236 0.017 187.862 0.000 3.091 3.156

==============================================================================

Omnibus: 1623.545 Durbin-Watson: 0.019

Prob(Omnibus): 0.000 Jarque-Bera (JB): 4249.364

Skew: 1.374 Prob(JB): 0.00

Kurtosis: 5.914 Cond. No. 2.90

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

==================================================================================

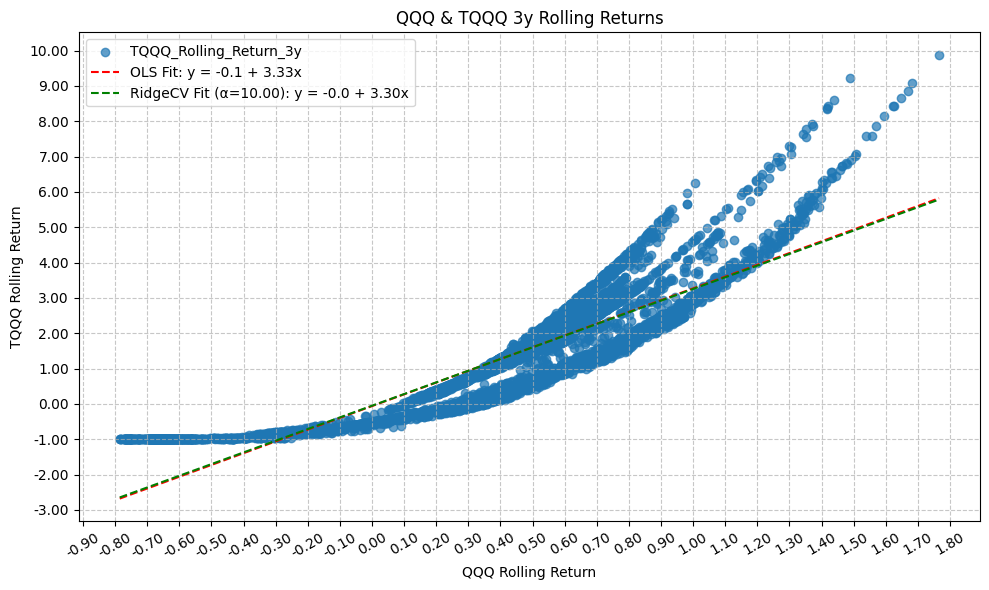

Dep. Variable: TQQQ_Rolling_Return_3y R-squared: 0.808

Model: OLS Adj. R-squared: 0.808

Method: Least Squares F-statistic: 2.565e+04

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:32:24 Log-Likelihood: -6738.8

No. Observations: 6104 AIC: 1.348e+04

Df Residuals: 6102 BIC: 1.350e+04

Df Model: 1

Covariance Type: nonrobust

=========================================================================================

coef std err t P>|t| [0.025 0.975]

-----------------------------------------------------------------------------------------

const -0.0608 0.013 -4.850 0.000 -0.085 -0.036

QQQ_Rolling_Return_3y 3.3335 0.021 160.141 0.000 3.293 3.374

==============================================================================

Omnibus: 871.091 Durbin-Watson: 0.015

Prob(Omnibus): 0.000 Jarque-Bera (JB): 1505.348

Skew: 0.941 Prob(JB): 0.00

Kurtosis: 4.541 Cond. No. 2.66

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

==================================================================================

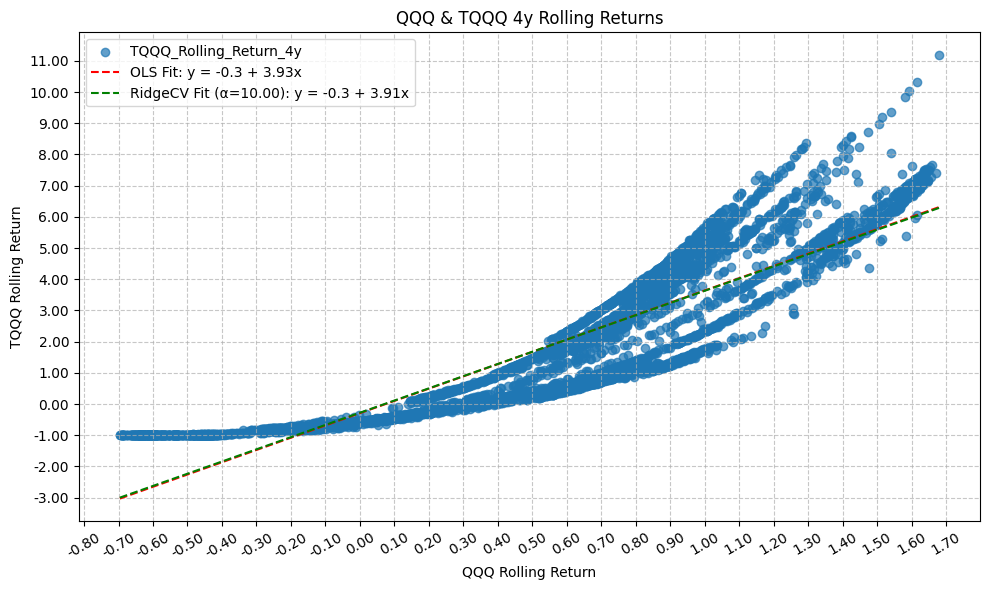

Dep. Variable: TQQQ_Rolling_Return_4y R-squared: 0.778

Model: OLS Adj. R-squared: 0.778

Method: Least Squares F-statistic: 2.048e+04

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:32:28 Log-Likelihood: -8910.6

No. Observations: 5852 AIC: 1.783e+04

Df Residuals: 5850 BIC: 1.784e+04

Df Model: 1

Covariance Type: nonrobust

=========================================================================================

coef std err t P>|t| [0.025 0.975]

-----------------------------------------------------------------------------------------

const -0.2947 0.021 -13.729 0.000 -0.337 -0.253

QQQ_Rolling_Return_4y 3.9098 0.027 143.110 0.000 3.856 3.963

==============================================================================

Omnibus: 221.269 Durbin-Watson: 0.010

Prob(Omnibus): 0.000 Jarque-Bera (JB): 114.248

Skew: 0.155 Prob(JB): 1.55e-25

Kurtosis: 2.390 Cond. No. 2.67

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

==================================================================================

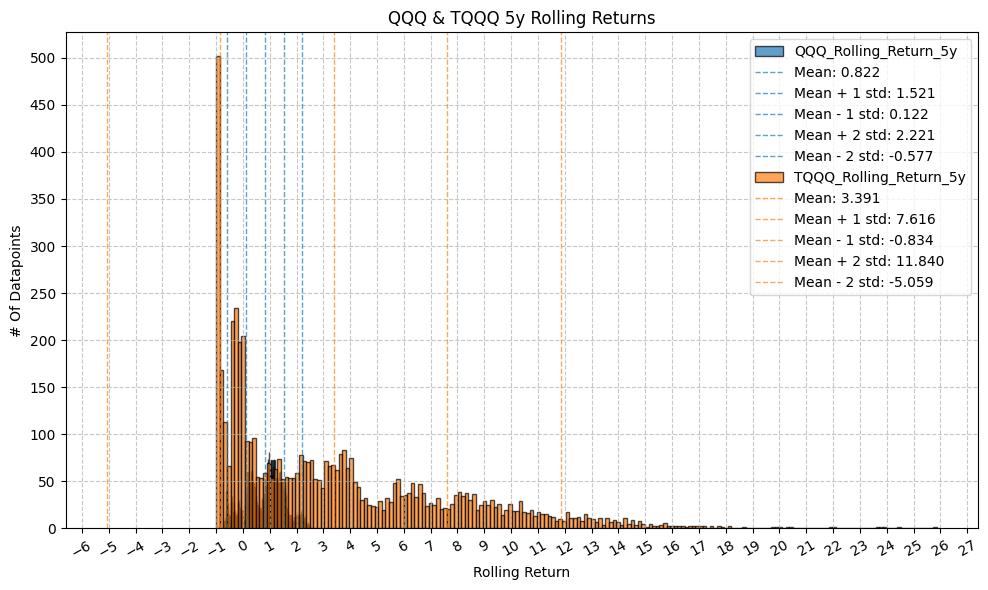

Dep. Variable: TQQQ_Rolling_Return_5y R-squared: 0.738

Model: OLS Adj. R-squared: 0.738

Method: Least Squares F-statistic: 1.579e+04

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:32:31 Log-Likelihood: -12238.

No. Observations: 5600 AIC: 2.448e+04

Df Residuals: 5598 BIC: 2.449e+04

Df Model: 1

Covariance Type: nonrobust

=========================================================================================

coef std err t P>|t| [0.025 0.975]

-----------------------------------------------------------------------------------------

const -0.9068 0.045 -20.345 0.000 -0.994 -0.819

QQQ_Rolling_Return_5y 5.1912 0.041 125.644 0.000 5.110 5.272

==============================================================================

Omnibus: 324.029 Durbin-Watson: 0.009

Prob(Omnibus): 0.000 Jarque-Bera (JB): 464.545

Skew: 0.512 Prob(JB): 1.33e-101

Kurtosis: 3.971 Cond. No. 2.74

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

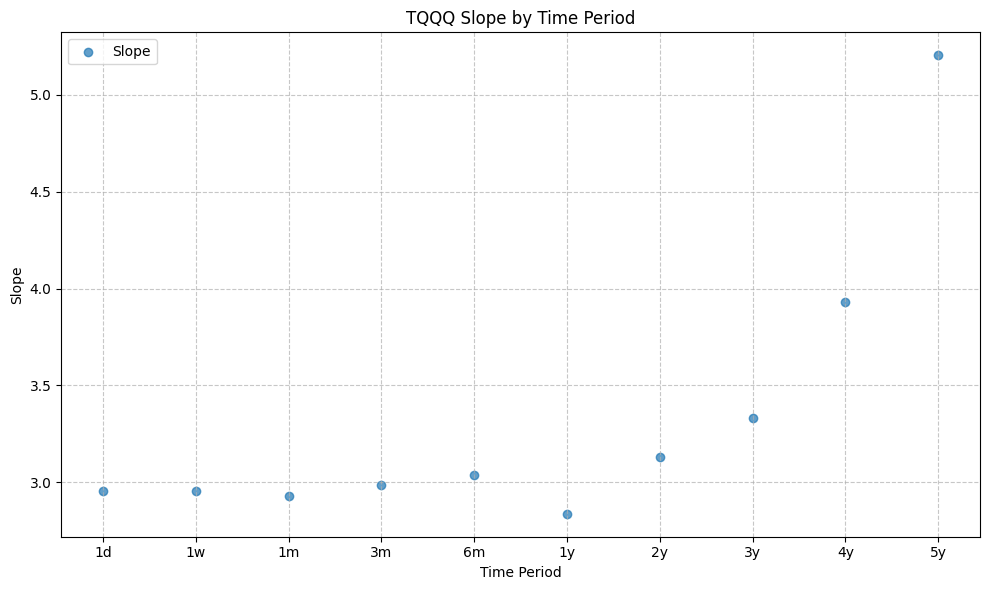

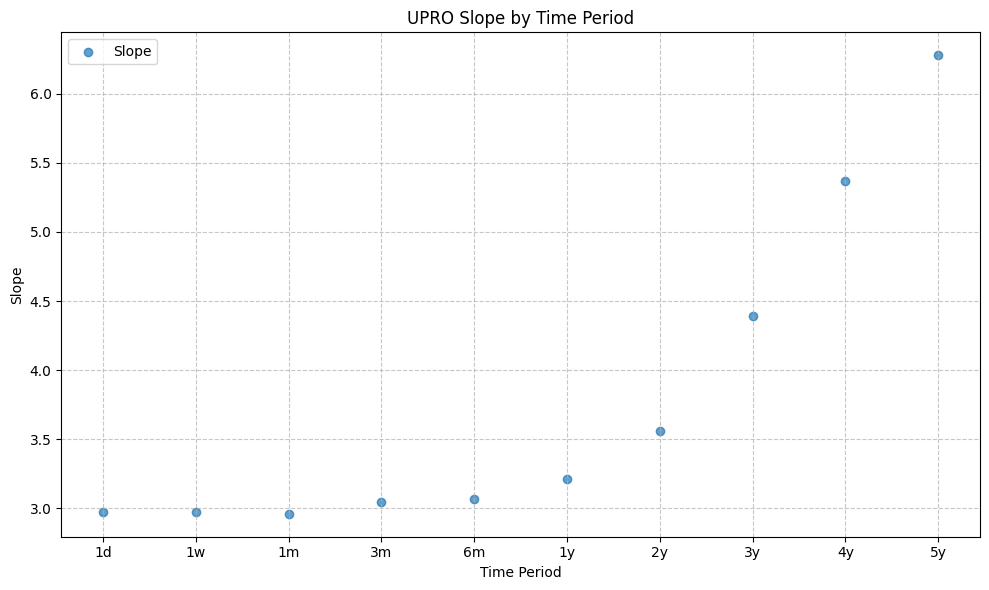

You’re welcome to digest each plot, but here’s my observations on the above results:

- 1d: TQQQ tracks QQQ as expected (it’s a 3x daily return leveraged ETF after all), with a regression coefficient of 2.96 and an R^2 of 0.997, and we extrapolated half the data with the same coefficient.

- 1w: Essentially the same as above. A few outliers, but the regression coefficient is still 2.95 with an R^2 of 0.994. We see a slight skew toward the positive in the rolling returns.

- 1m: The skew toward the positive is more pronounced, and we see more outliers. The regression coefficient has decreased to 2.93 and the R^2 has dropped to 0.98, which is still very high, but we are starting to see some dispersion in the returns.

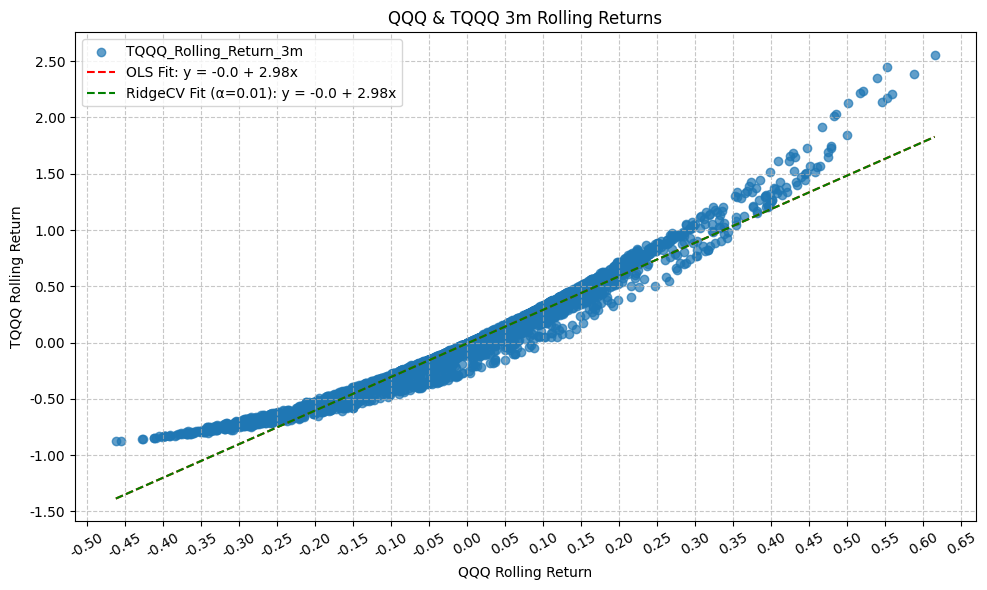

- 3m: The skew toward the positive is even more pronounced, and we see even more outliers. The regression coefficient has increased, to 2.98 and the R^2 has dropped to 0.96.

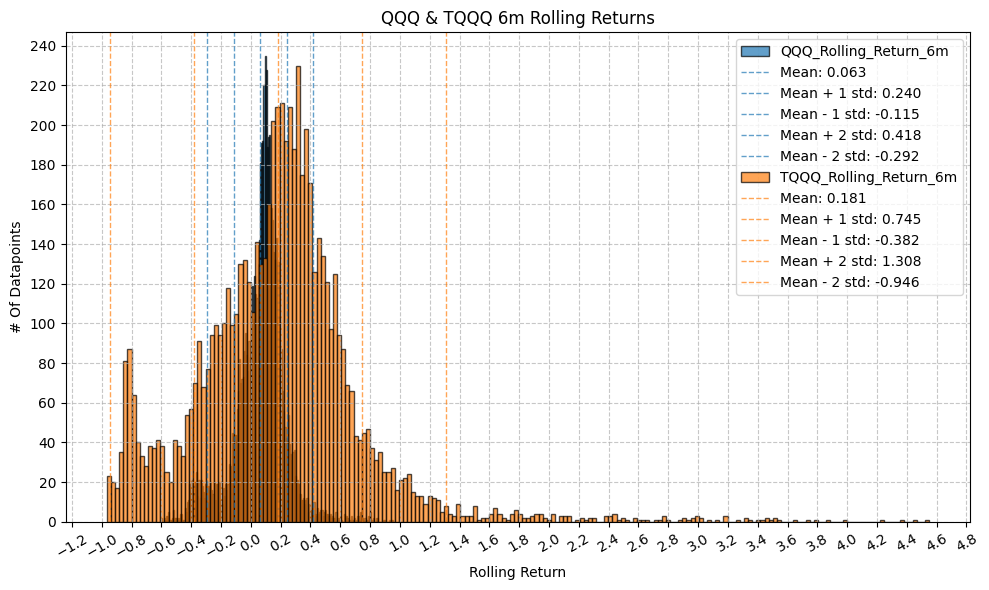

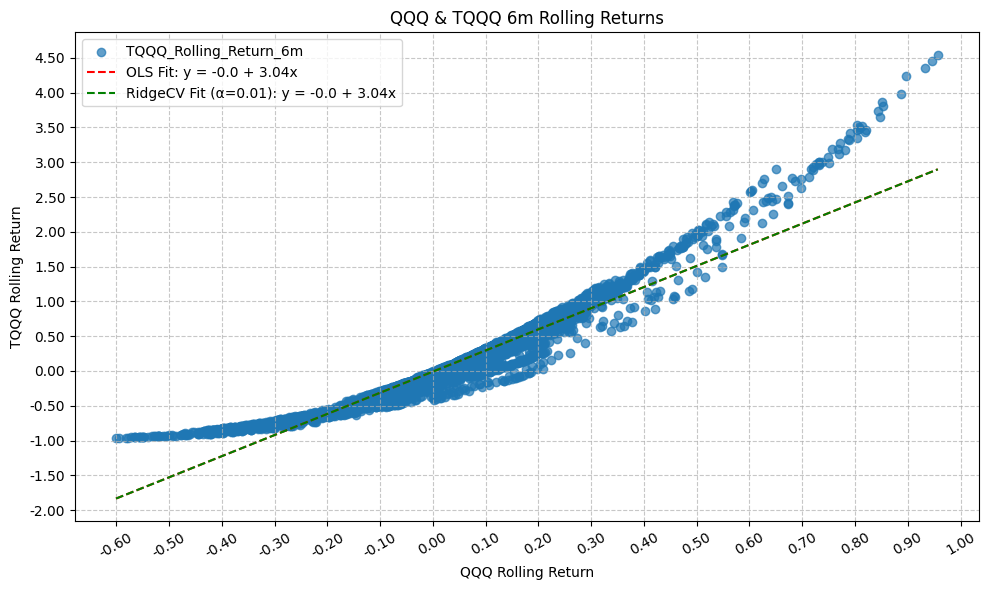

- 6m: The skew toward the positive is very pronounced, and we see a significant number of outliers with pronounced curvanture in the plot. The regression coefficient has increased again, to 3.4 and the R^2 has dropped to 0.92.

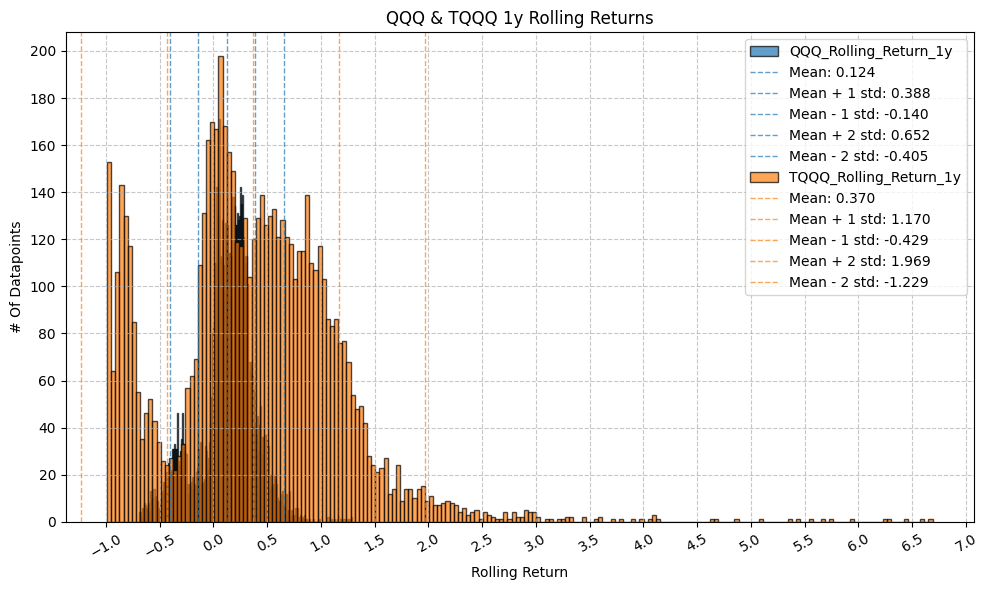

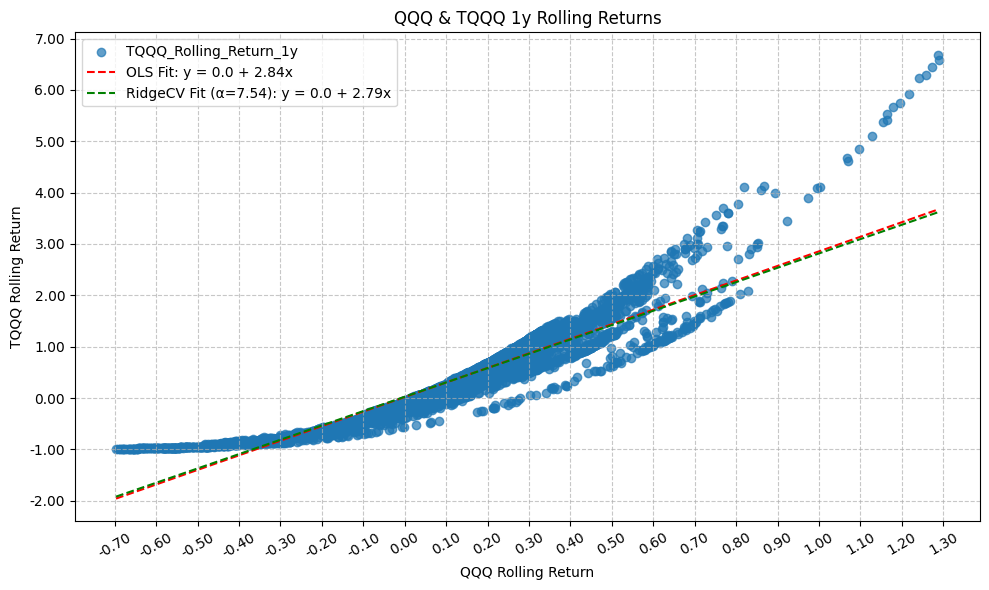

- 1y: At this point, based on the plot and the regression results, we can start to see that the returns of TQQQ are no longer tracking 3x the returns of QQQ as closely as they did in the shorter time periods. The regression coefficient has is now 2.84 and the R^2 has dropped to 0.88.

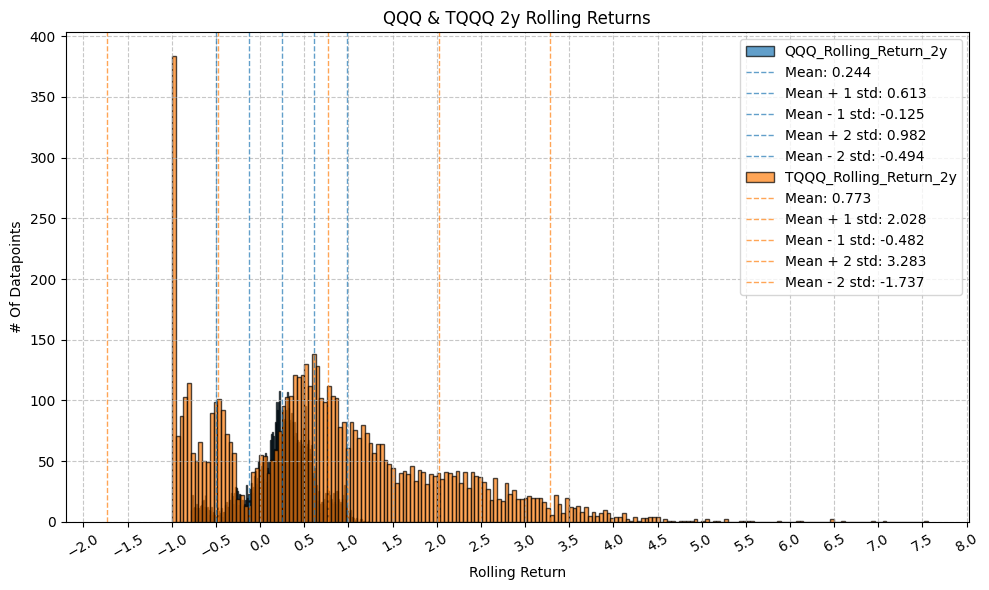

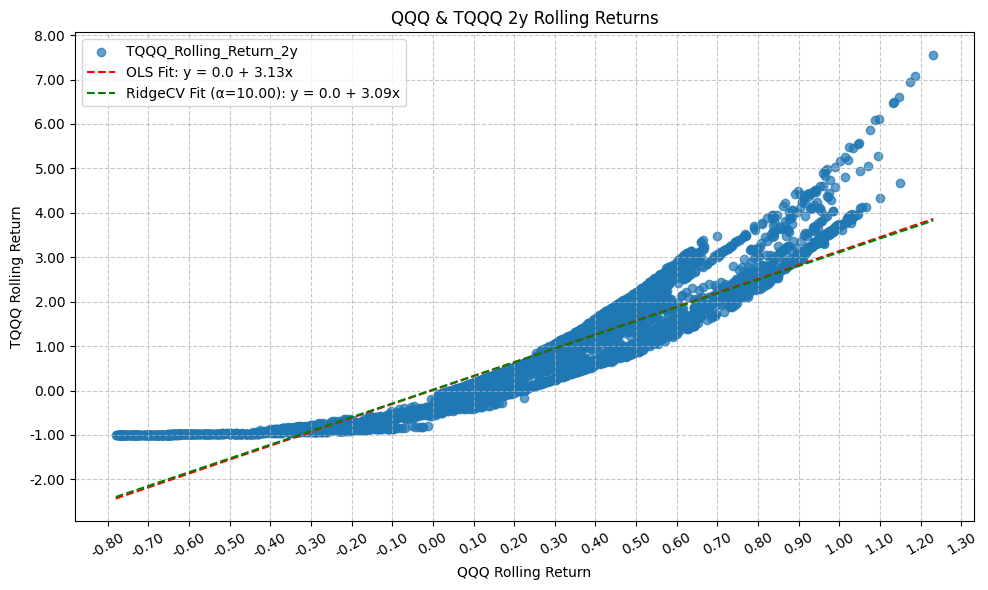

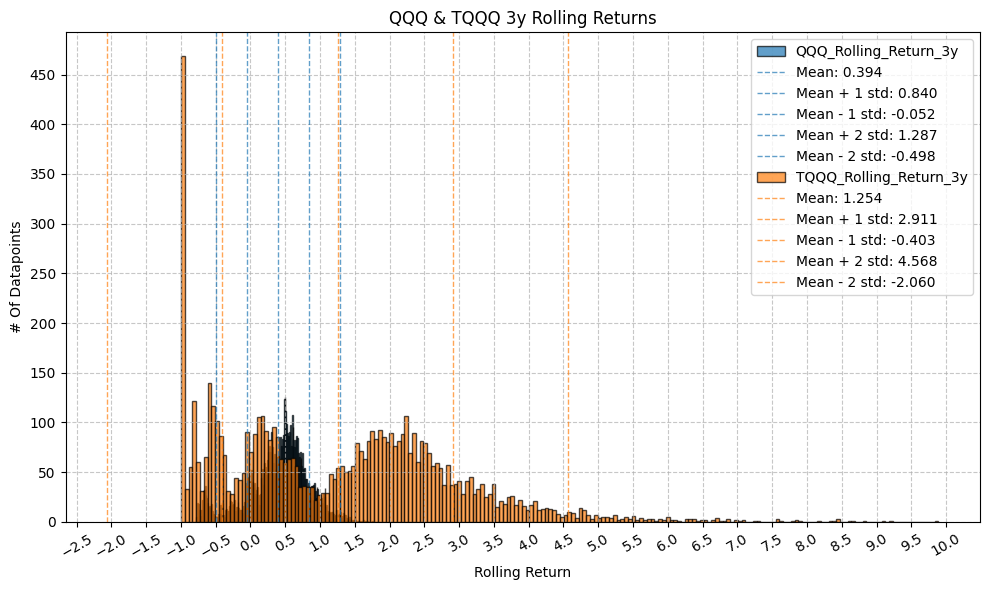

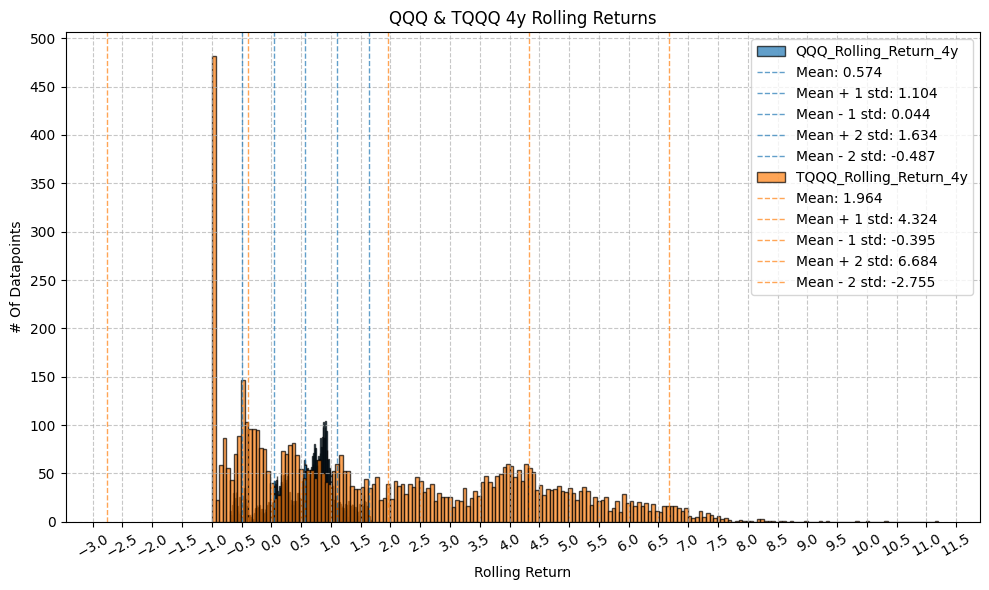

- 4y and 5y: We can see that there are periods where the rolling returns of TQQQ are significantly higher and lower than 3x the returns of QQQ, which is consistent with the idea of volatility decay.

For 4y, based on the regression results, we see that if the rolling return of QQQ was 0, then we would expect a return of -0.30 for TQQQ.

$$ r_{TQQQ} = -0.30 + 3.93 \times r_{QQQ} = -0.30 + 3.93 \times 0 = -0.30 $$

On the other end of the spectrum, if the rolling return of QQQ was 1, then we would expect a return of:

$$ r_{TQQQ} = -0.30 + 3.93 \times r_{QQQ} = -0.30 + 3.93 \times 1 = 3.63 $$

In general, the positive skew of the rolling returns of TQQQ relative to QQQ is related to the general postive return performance of QQQ. With sustained positive returns, the leverage effect of TQQQ will amplify those returns, leading to a positive skew. However, during periods of negative returns for QQQ, the leverage effect will also amplify those losses, leading to a negative skew, and to the limit of a cumulative return of -1, or a 100% loss. The overall skewness of the rolling returns will depend on the balance of these positive and negative periods.

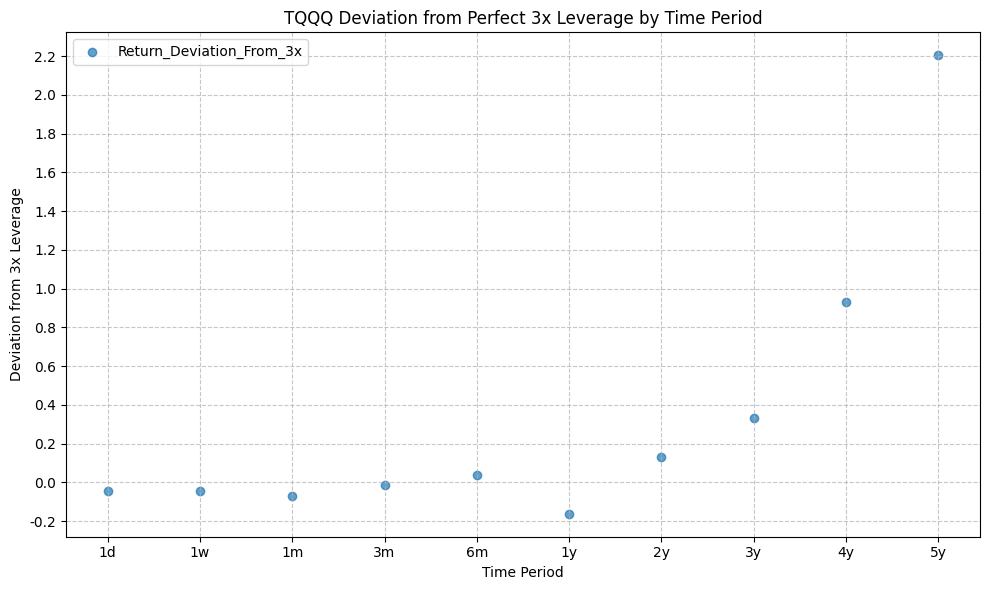

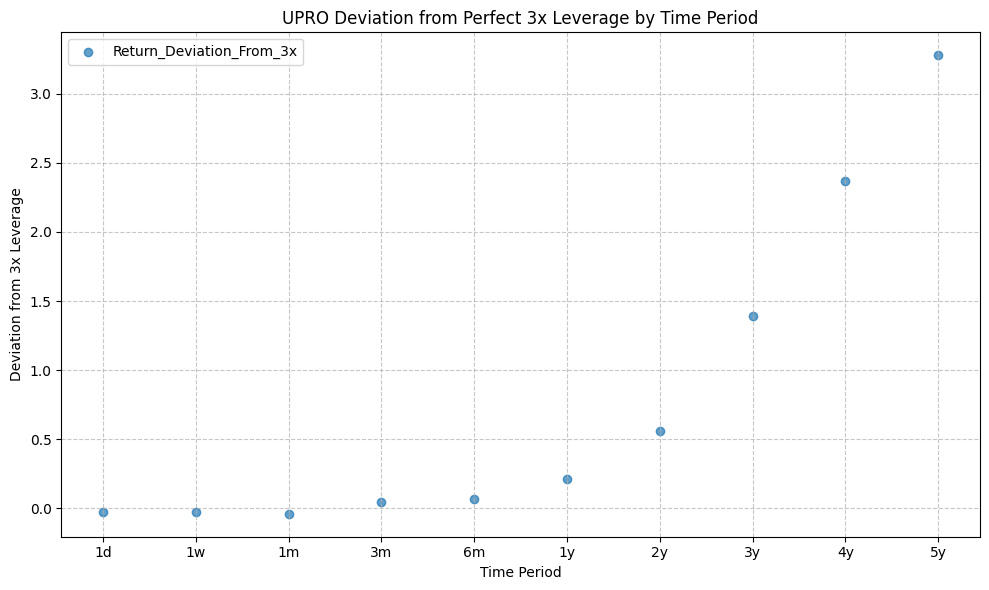

Rolling Returns Deviation (QQQ & TQQQ) #

Next, we will the rolling returns deviation from the expected 3x return for each time period. This will give us a better picture of the volatility decay effect and how it changes over different time horizons.

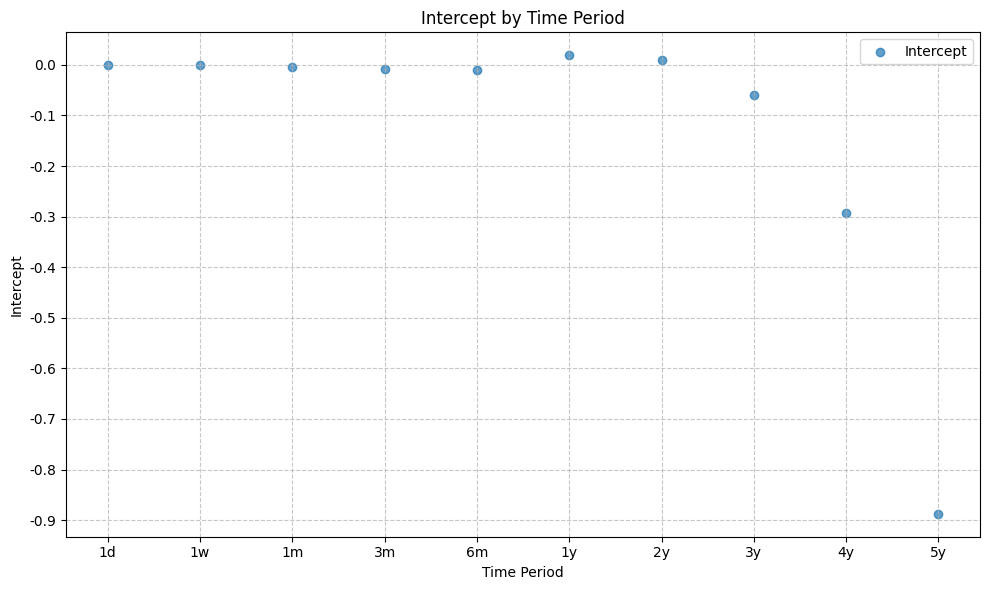

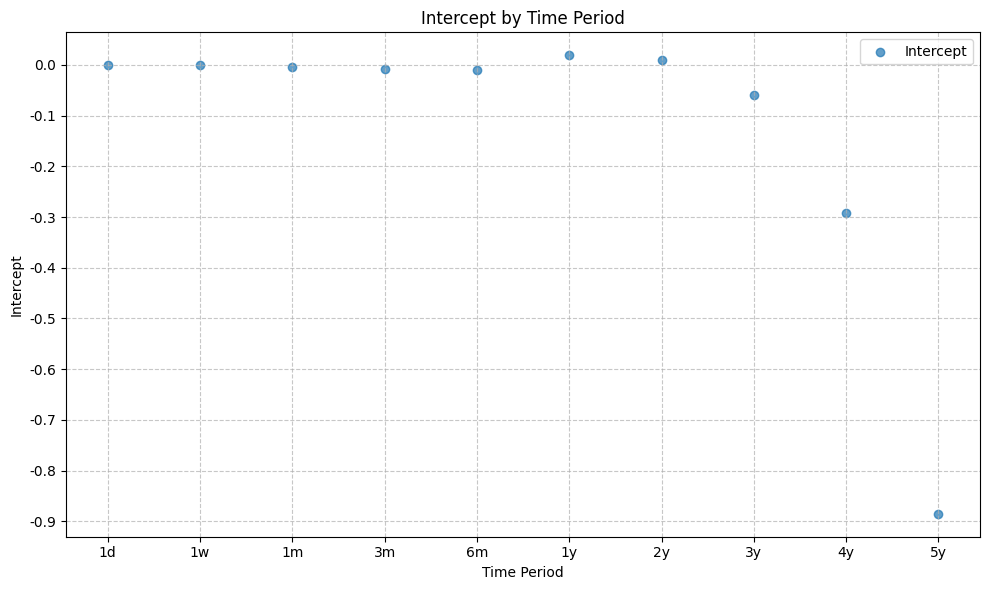

rolling_returns_stats["Return_Deviation_From_3x"] = rolling_returns_stats["Slope"] - 3.0

pandas_set_decimal_places(3)

display(rolling_returns_stats.set_index("Period"))

| Intercept | Slope | R_Squared | Return Skew | Average Upside Beta | Average Downside Beta | Asymmetry | Return_Deviation_From_3x | |

|---|---|---|---|---|---|---|---|---|

| Period | ||||||||

| 1d | -0.000 | 2.955 | 0.999 | NaN | 2.958 | NaN | NaN | -0.045 |

| 1w | -0.001 | 2.953 | 0.994 | NaN | 2.557 | NaN | NaN | -0.047 |

| 1m | -0.004 | 2.936 | 0.982 | NaN | 2.213 | NaN | NaN | -0.064 |

| 3m | -0.008 | 2.987 | 0.959 | NaN | 1.997 | -inf | inf | -0.013 |

| 6m | -0.010 | 3.040 | 0.916 | -8.109 | 1.482 | 5.521 | -4.039 | 0.040 |

| 1y | 0.019 | 2.842 | 0.881 | NaN | 1.244 | -inf | inf | -0.158 |

| 2y | 0.007 | 3.124 | 0.847 | 36.342 | 1.402 | 12.342 | -10.939 | 0.124 |

| 3y | -0.061 | 3.334 | 0.808 | NaN | -0.049 | -inf | inf | 0.334 |

| 4y | -0.295 | 3.910 | 0.778 | 19.663 | 1.763 | 7.212 | -5.449 | 0.910 |

| 5y | -0.907 | 5.191 | 0.738 | 43.272 | 2.421 | 11.480 | -9.060 | 2.191 |

plot_scatter(

df=rolling_returns_stats,

x_plot_column="Period",

y_plot_columns=["Return_Deviation_From_3x"],

title="TQQQ Deviation from Perfect 3x Leverage by Time Period",

x_label="Time Period",

x_format="String",

x_format_decimal_places=0,

x_tick_spacing=1,

x_tick_start=None,

x_tick_rotation=0,

y_label="Deviation from 3x Leverage",

y_format="Decimal",

y_format_decimal_places=1,

y_tick_spacing="Auto",

y_tick_rotation=0,

plot_OLS_regression_line=False,

OLS_column=None,

plot_Ridge_regression_line=False,

Ridge_column=None,

plot_RidgeCV_regression_line=False,

RidgeCV_column=None,

regression_constant=False,

grid=True,

legend=True,

export_plot=False,

plot_file_name=None,

)

plot_scatter(

df=rolling_returns_stats,

x_plot_column="Period",

y_plot_columns=["Slope"],

title="TQQQ Slope by Time Period",

x_label="Time Period",

x_format="String",

x_format_decimal_places=0,

x_tick_spacing=1,

x_tick_start=None,

x_tick_rotation=0,

y_label="Slope",

y_format="Decimal",

y_format_decimal_places=1,

y_tick_spacing="Auto",

y_tick_rotation=0,

plot_OLS_regression_line=False,

OLS_column=None,

plot_Ridge_regression_line=False,

Ridge_column=None,

plot_RidgeCV_regression_line=False,

RidgeCV_column=None,

regression_constant=False,

grid=True,

legend=True,

export_plot=False,

plot_file_name=None,

)

plot_scatter(

df=rolling_returns_stats,

x_plot_column="Period",

y_plot_columns=["Intercept"],

title="Intercept by Time Period",

x_label="Time Period",

x_format="String",

x_format_decimal_places=0,

x_tick_spacing=1,

x_tick_start=None,

x_tick_rotation=0,

y_label="Intercept",

y_format="Decimal",

y_format_decimal_places=1,

y_tick_spacing="Auto",

y_tick_rotation=0,

plot_OLS_regression_line=False,

OLS_column=None,

plot_Ridge_regression_line=False,

Ridge_column=None,

plot_RidgeCV_regression_line=False,

RidgeCV_column=None,

regression_constant=False,

grid=True,

legend=True,

export_plot=False,

plot_file_name=None,

)

display(rolling_returns_stats.set_index("Period"))

| Intercept | Slope | R_Squared | Return Skew | Average Upside Beta | Average Downside Beta | Asymmetry | Return_Deviation_From_3x | |

|---|---|---|---|---|---|---|---|---|

| Period | ||||||||

| 1d | -0.000 | 2.955 | 0.999 | NaN | 2.958 | NaN | NaN | -0.045 |

| 1w | -0.001 | 2.953 | 0.994 | NaN | 2.557 | NaN | NaN | -0.047 |

| 1m | -0.004 | 2.936 | 0.982 | NaN | 2.213 | NaN | NaN | -0.064 |

| 3m | -0.008 | 2.987 | 0.959 | NaN | 1.997 | -inf | inf | -0.013 |

| 6m | -0.010 | 3.040 | 0.916 | -8.109 | 1.482 | 5.521 | -4.039 | 0.040 |

| 1y | 0.019 | 2.842 | 0.881 | NaN | 1.244 | -inf | inf | -0.158 |

| 2y | 0.007 | 3.124 | 0.847 | 36.342 | 1.402 | 12.342 | -10.939 | 0.124 |

| 3y | -0.061 | 3.334 | 0.808 | NaN | -0.049 | -inf | inf | 0.334 |

| 4y | -0.295 | 3.910 | 0.778 | 19.663 | 1.763 | 7.212 | -5.449 | 0.910 |

| 5y | -0.907 | 5.191 | 0.738 | 43.272 | 2.421 | 11.480 | -9.060 | 2.191 |

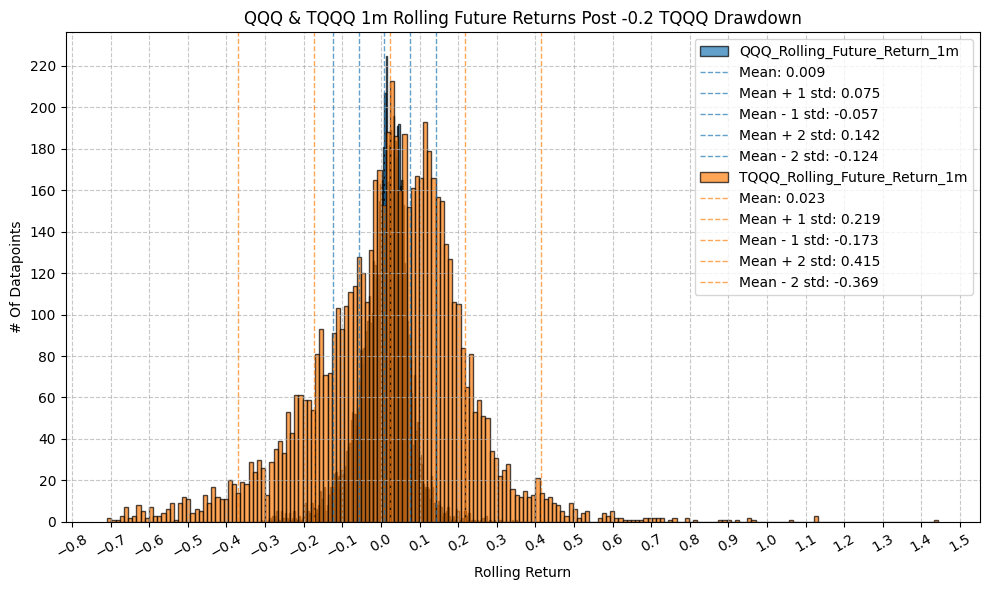

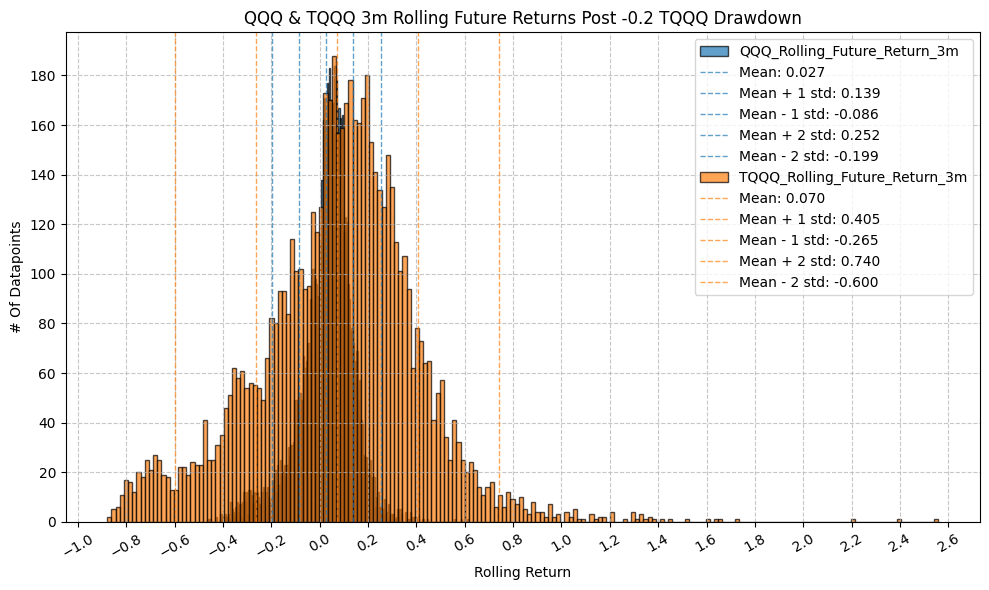

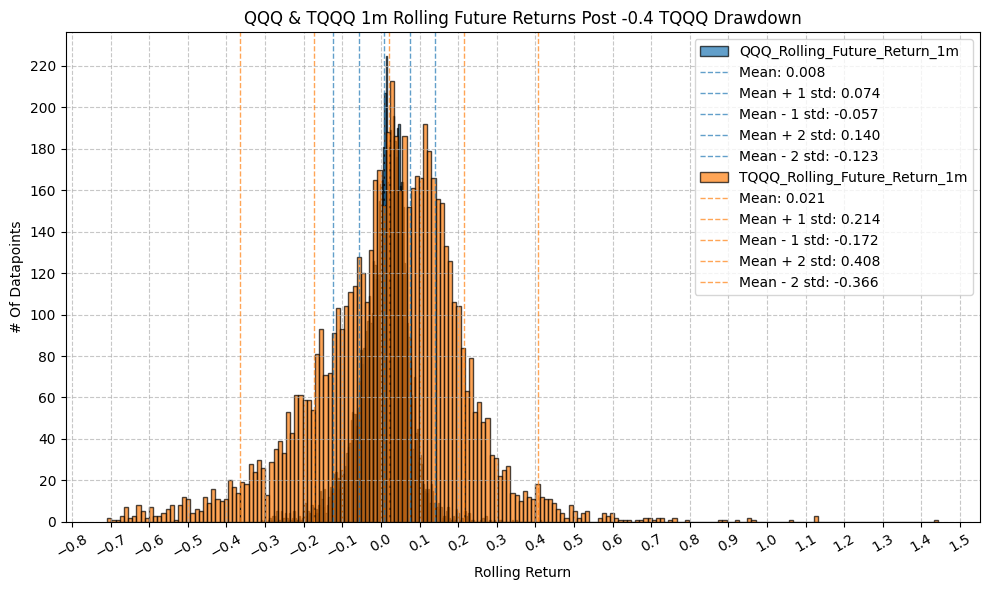

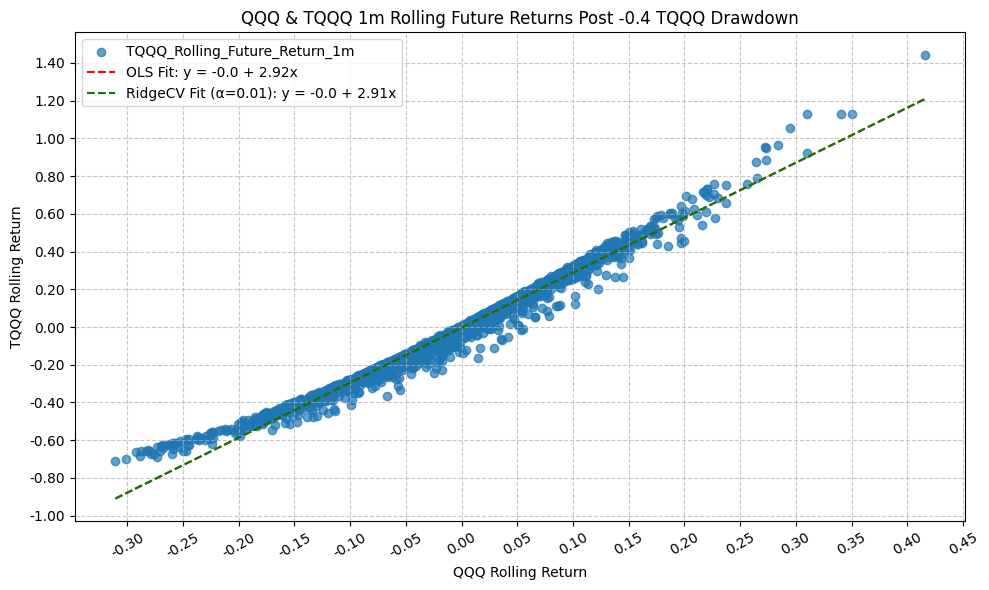

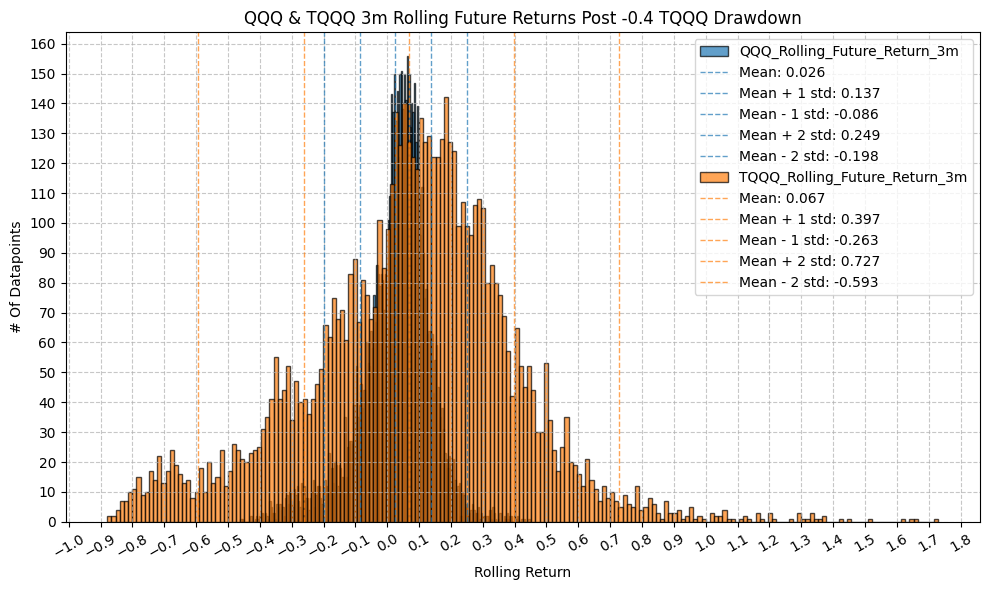

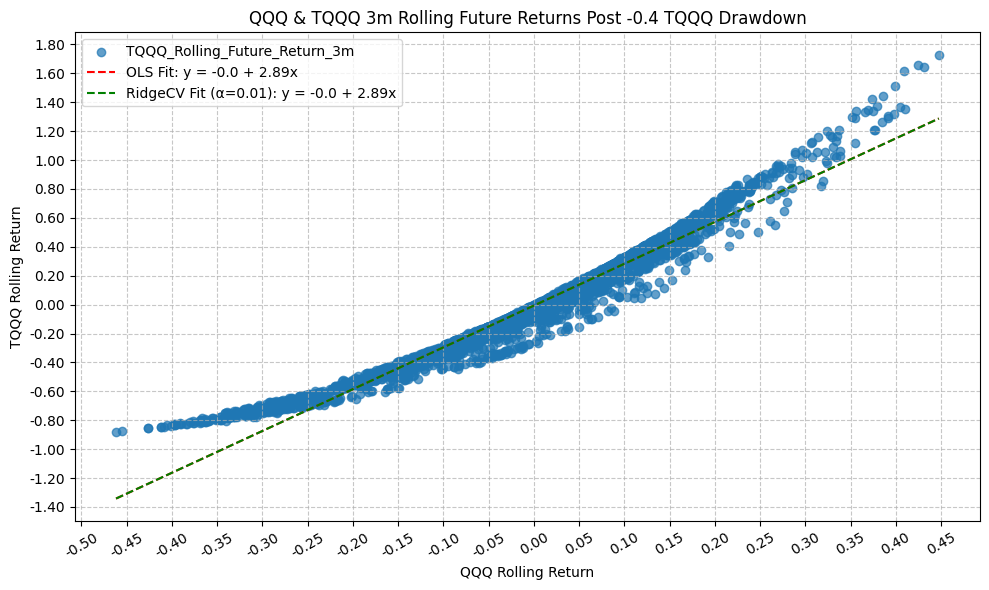

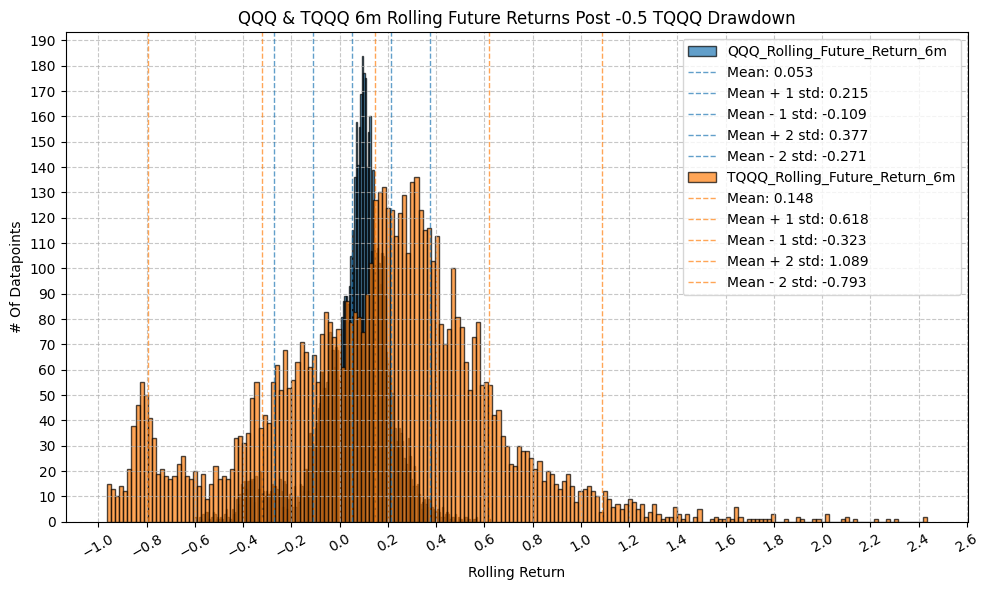

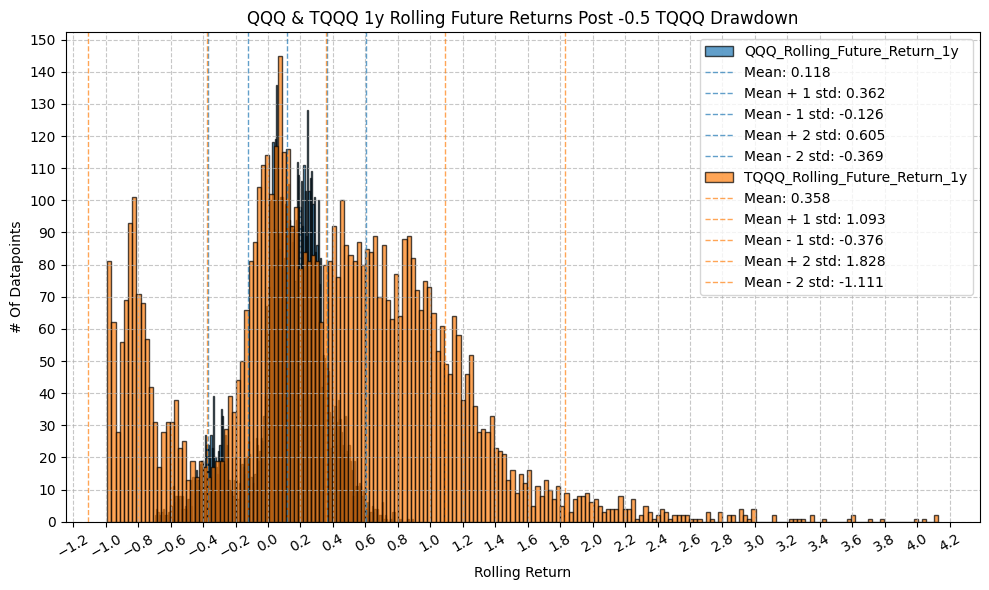

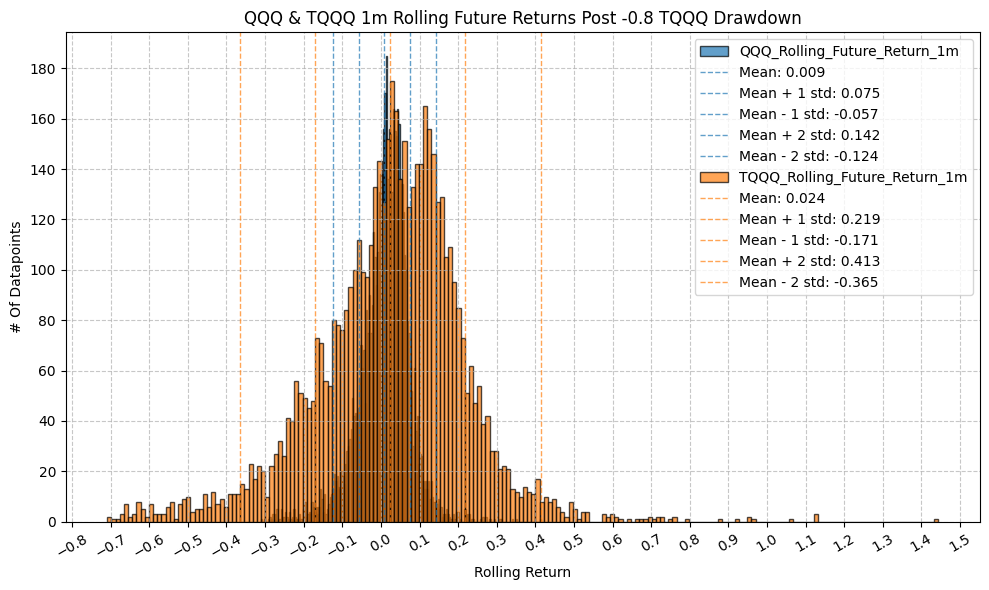

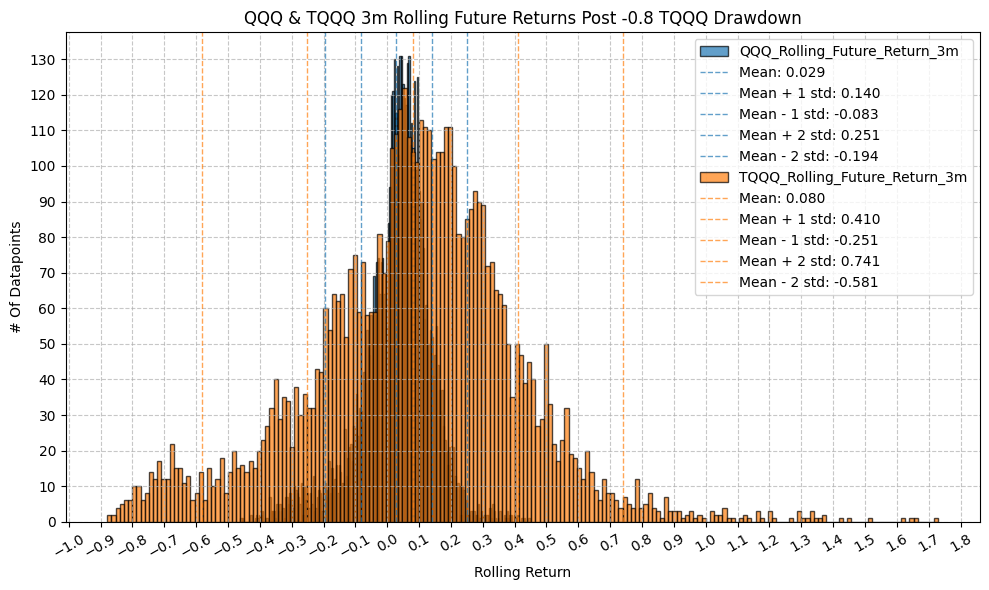

This is very interesting. Up to 1 year, there is minimal difference between the mean TQQQ 1 year rolling return and the hypothetical 3x leverage, with an R^2 of greater than 0.9.

However, as we extend the time period, we see that

- The “leverage factor” increases significantly, resulting in a deviation from the perfect 3x leverage.

- The intercept also begins to deviate significantly from 0.

The above highlight the impact of volatility magnification over longer time horizons. This phenomenon is happening likely due to the positive returns that QQQ has achieved since 2010 - resulting in TQQQ compounding at a much higher rate than 3x - but it may and likely is not exhibited by other 3x leveraged ETFs that have not had the same positive return profile as QQQ.

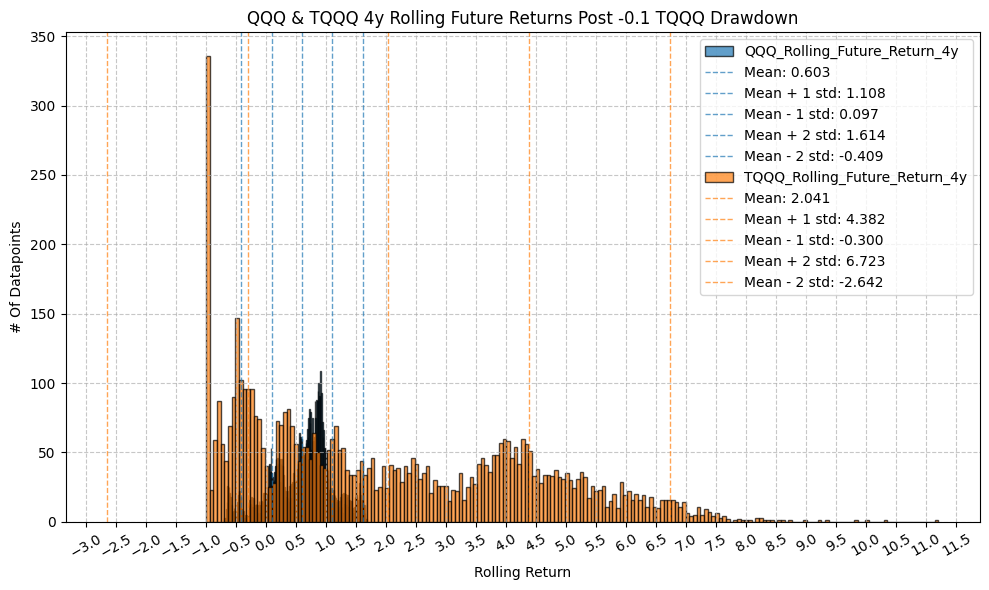

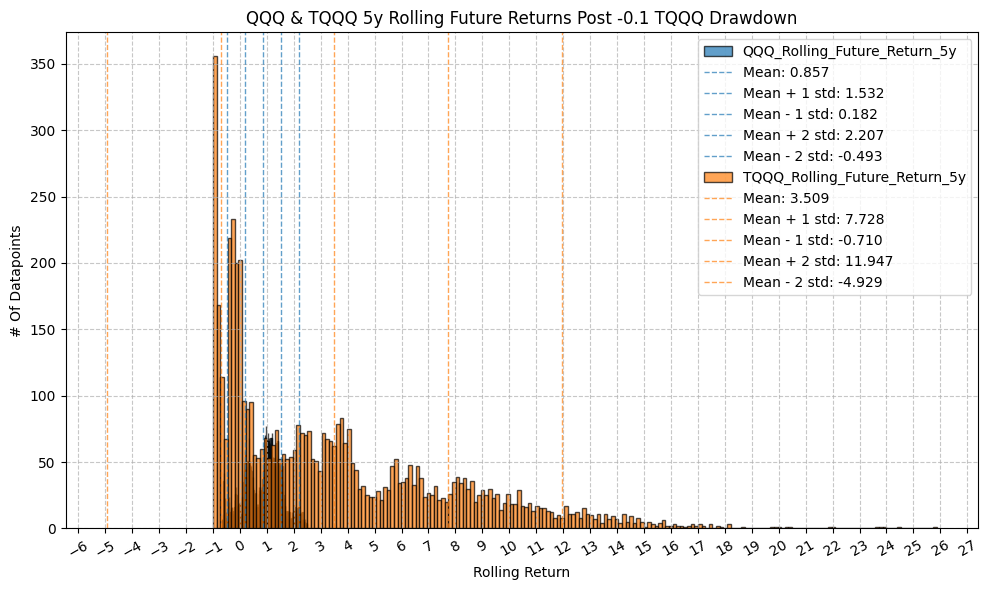

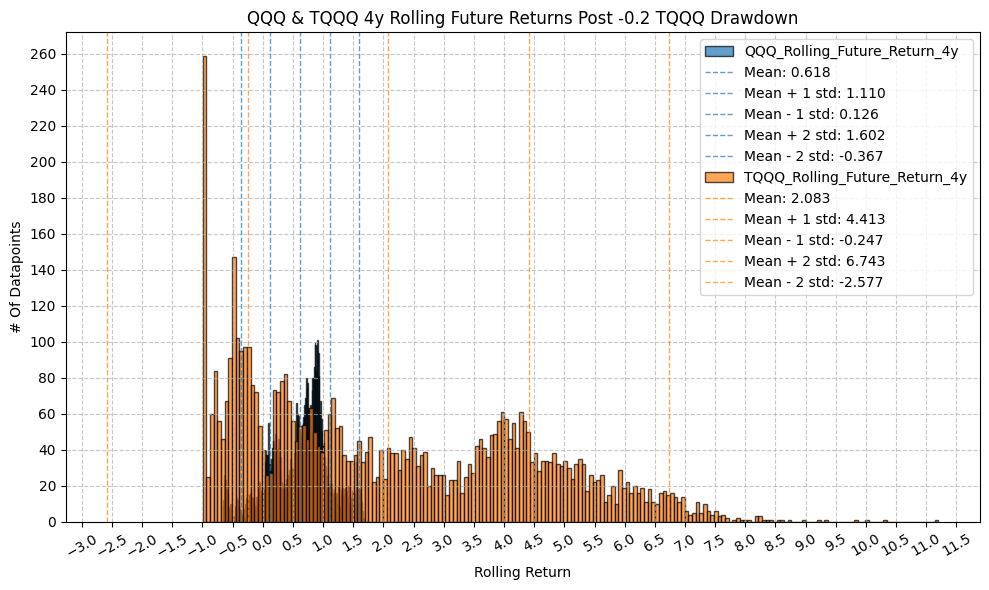

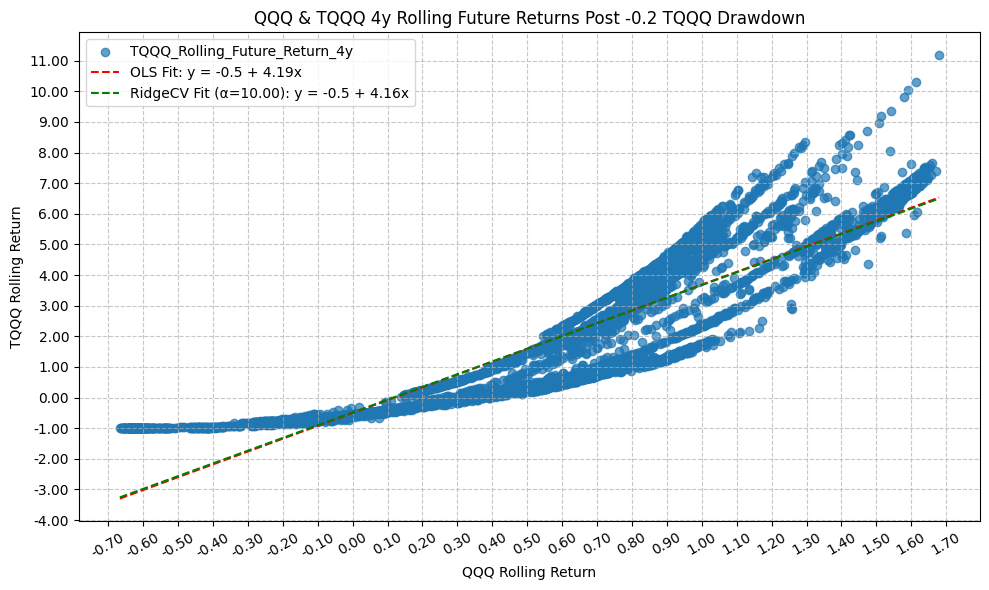

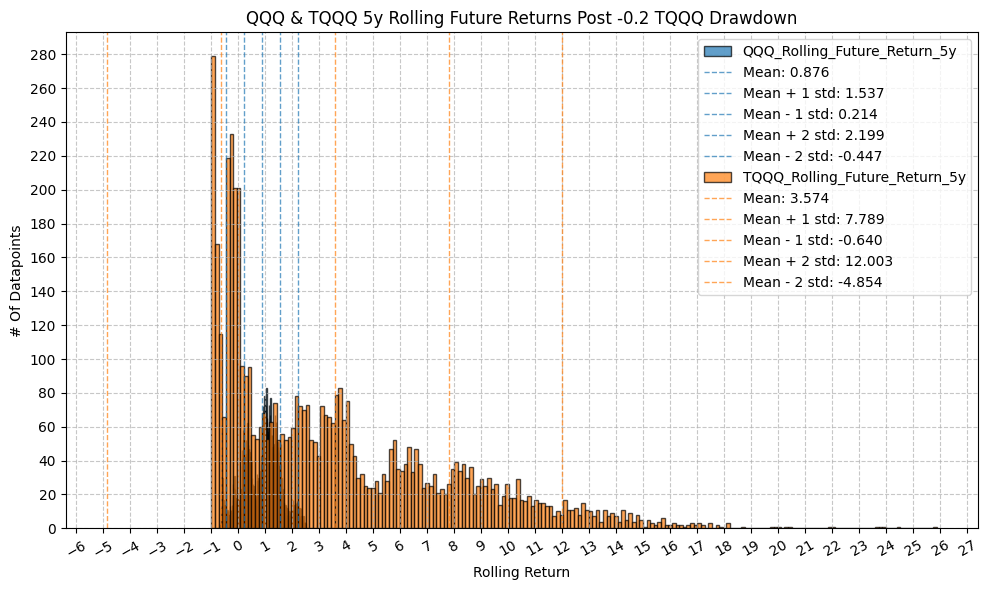

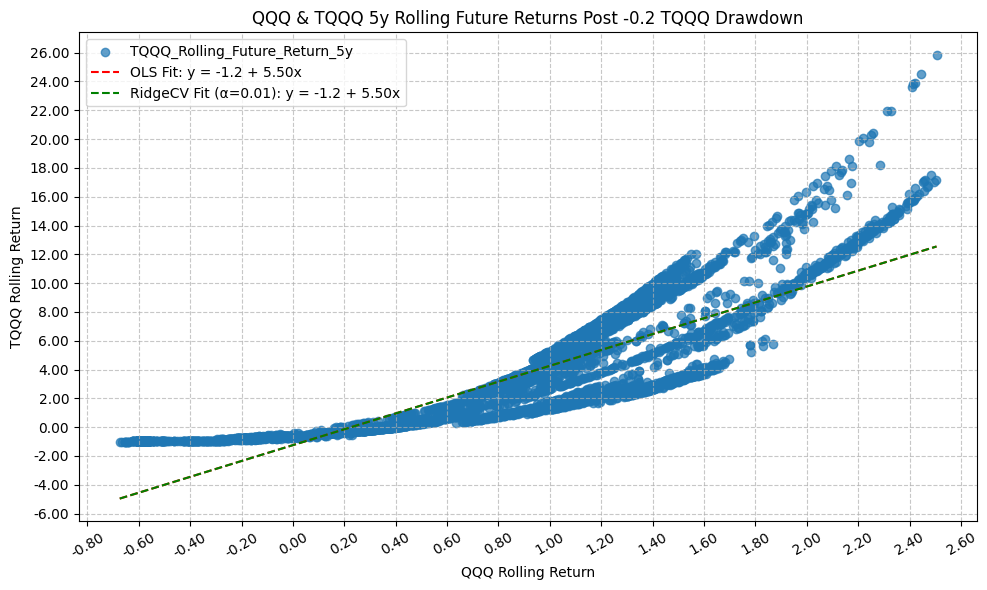

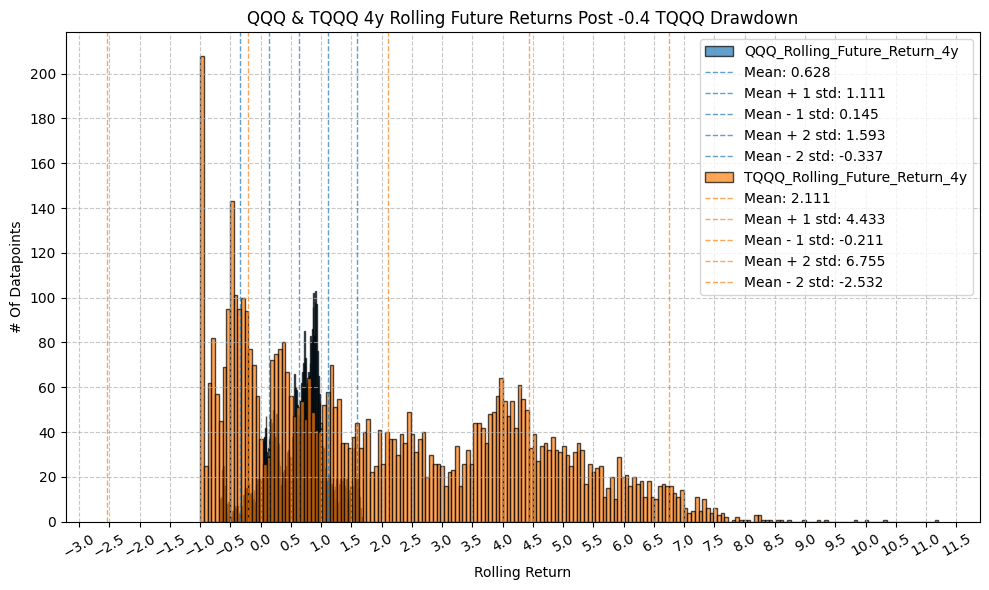

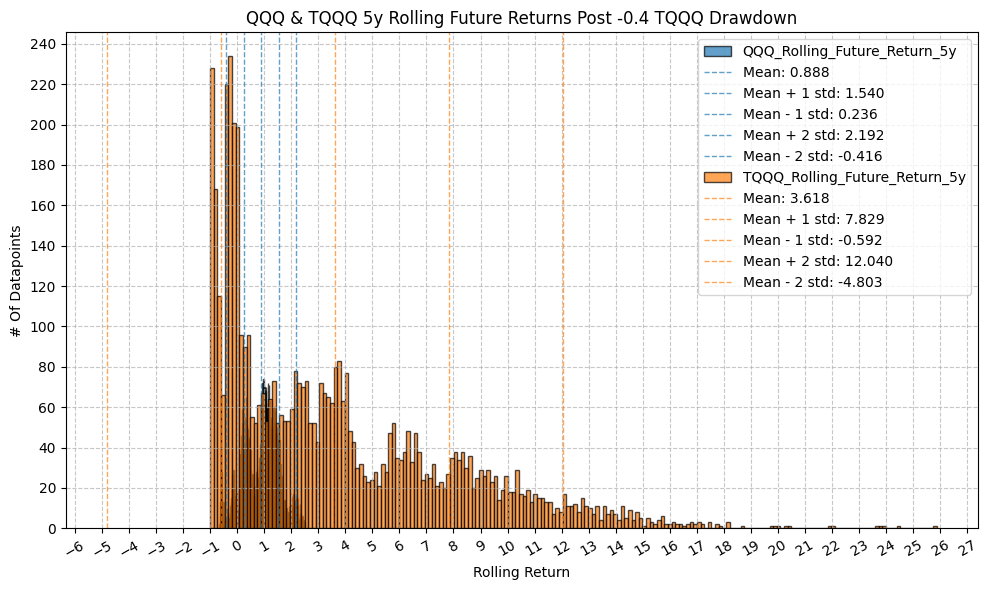

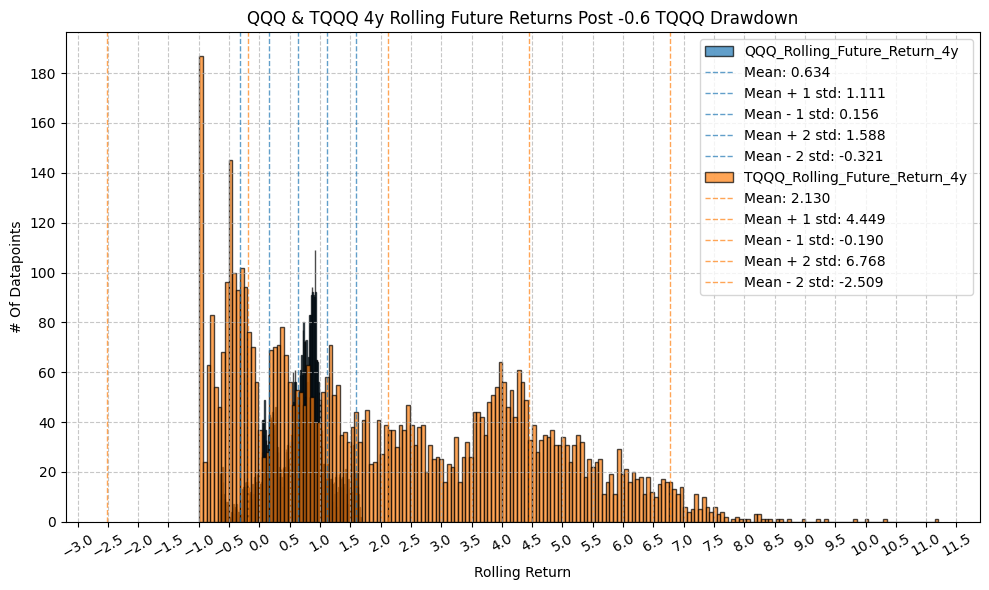

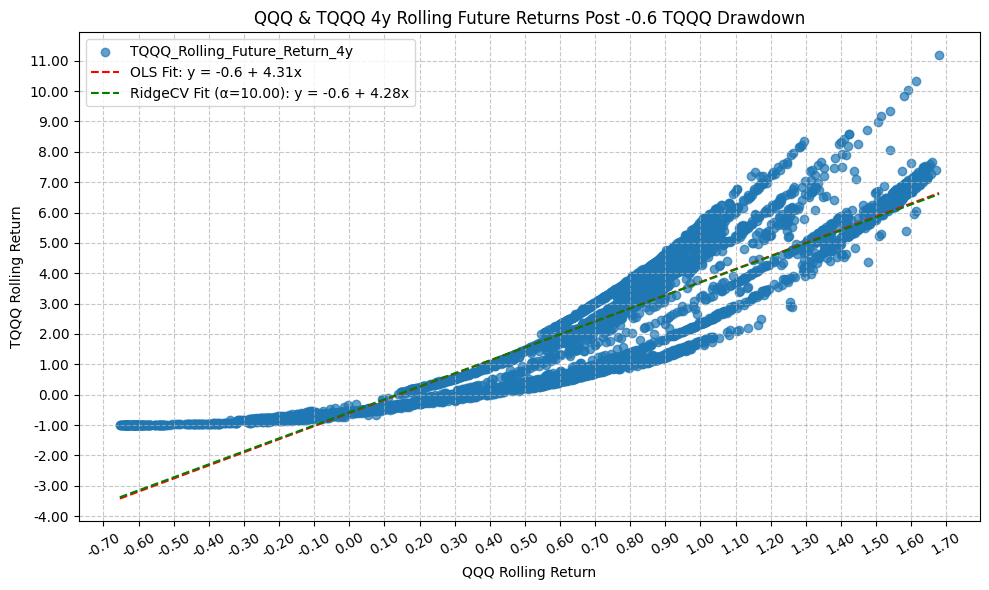

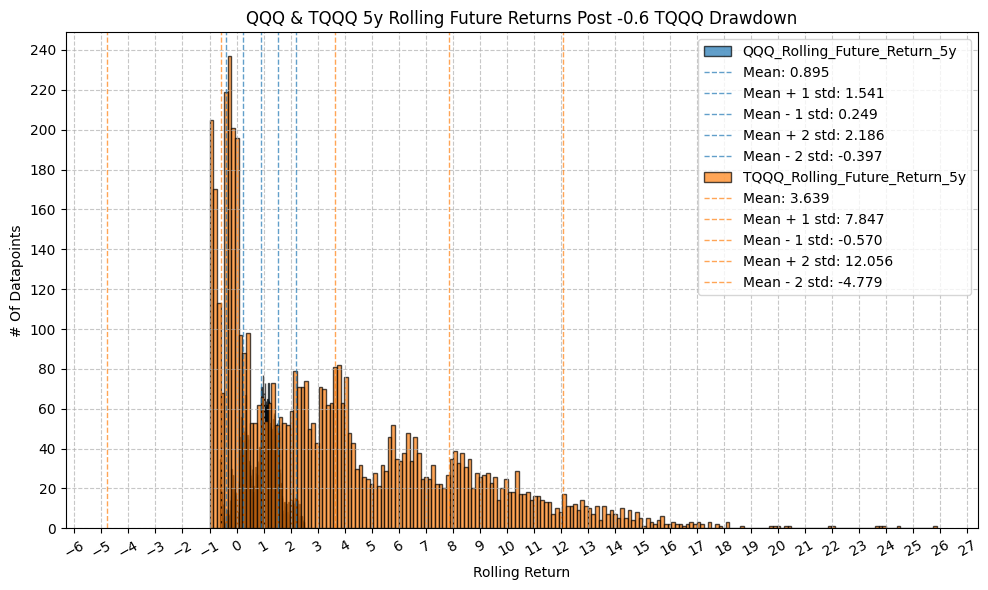

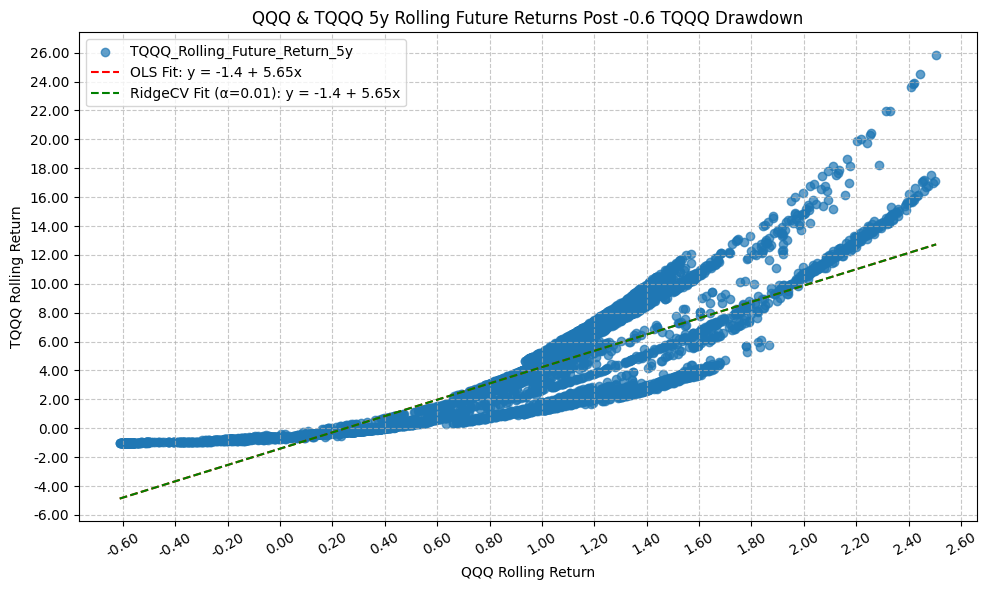

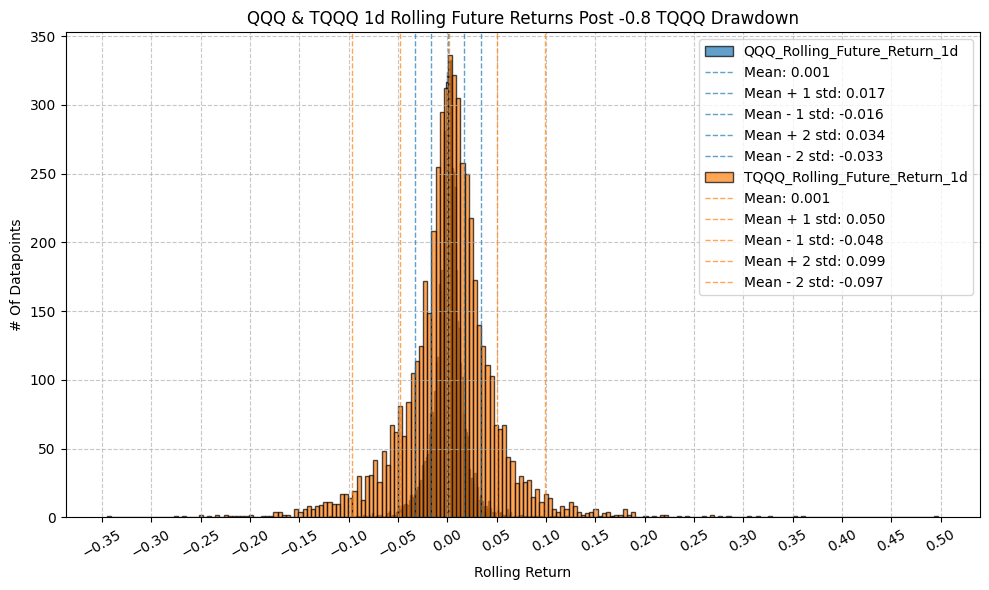

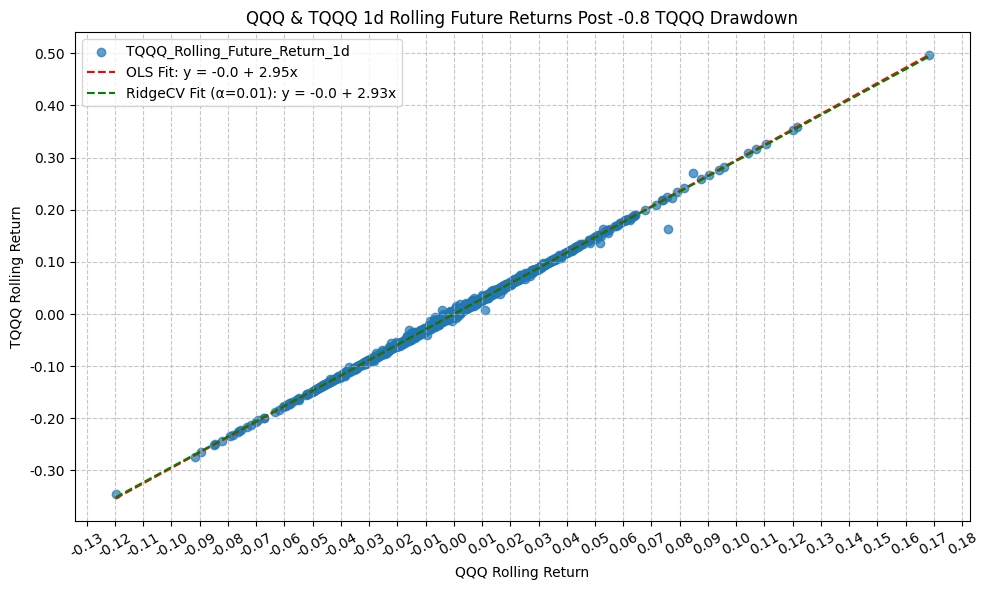

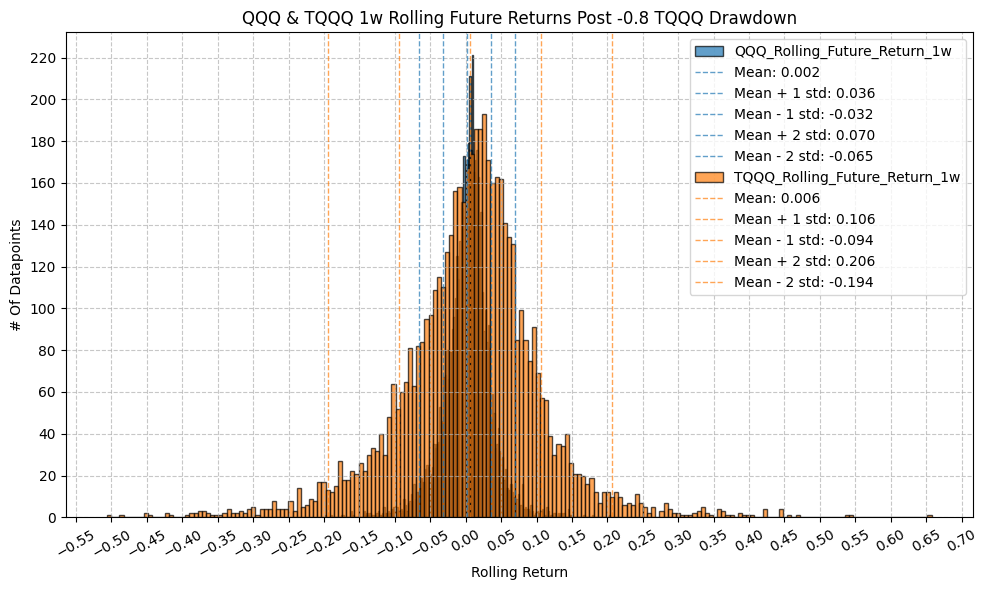

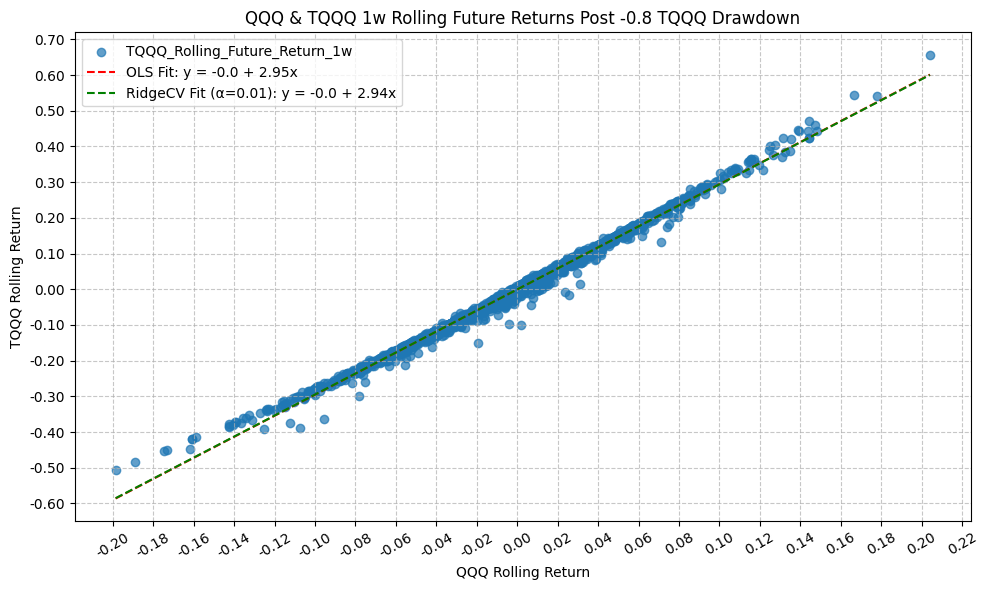

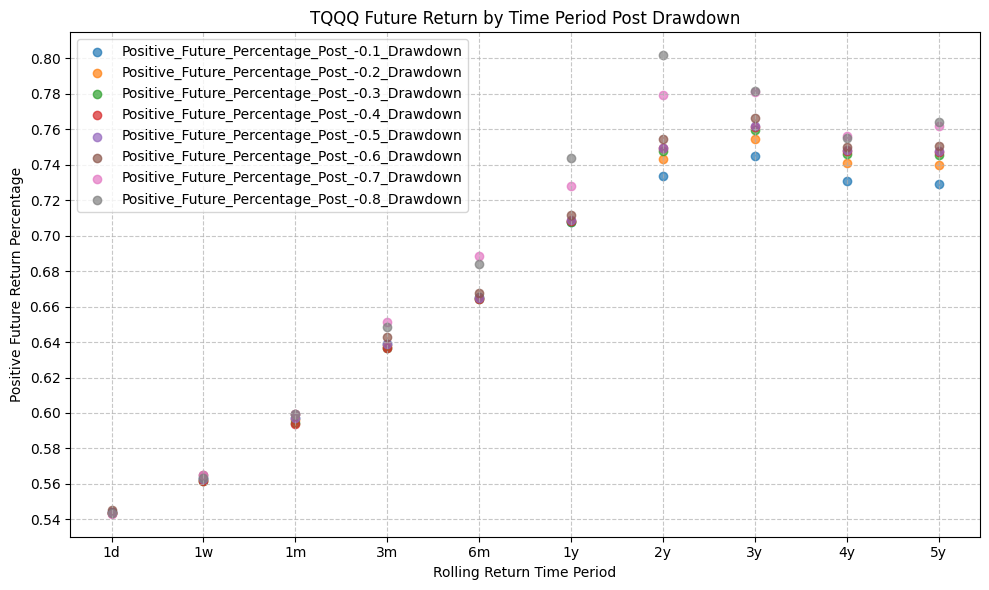

With the above results, the next logical question is, when is the opportune time to buy a 3x leveraged ETF like TQQQ? To answer this, we will look a the drawdown levels of TQQQ and the subsequent returns over various time horizons.

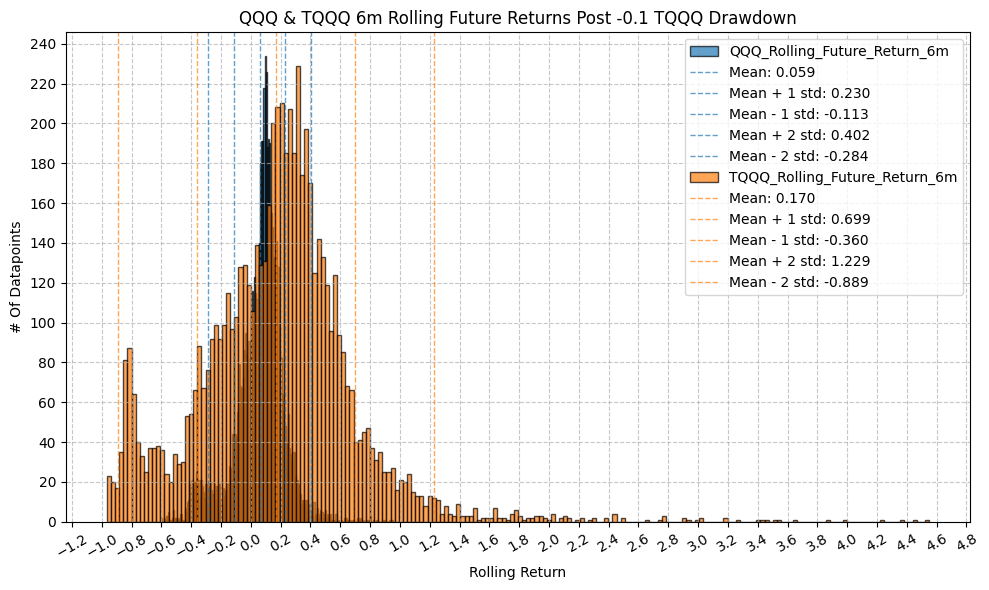

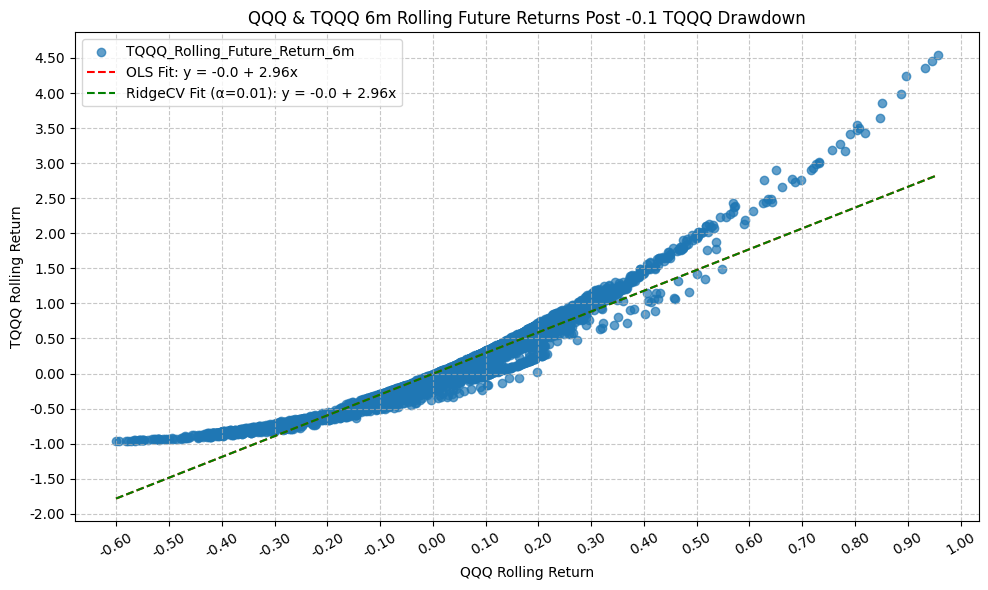

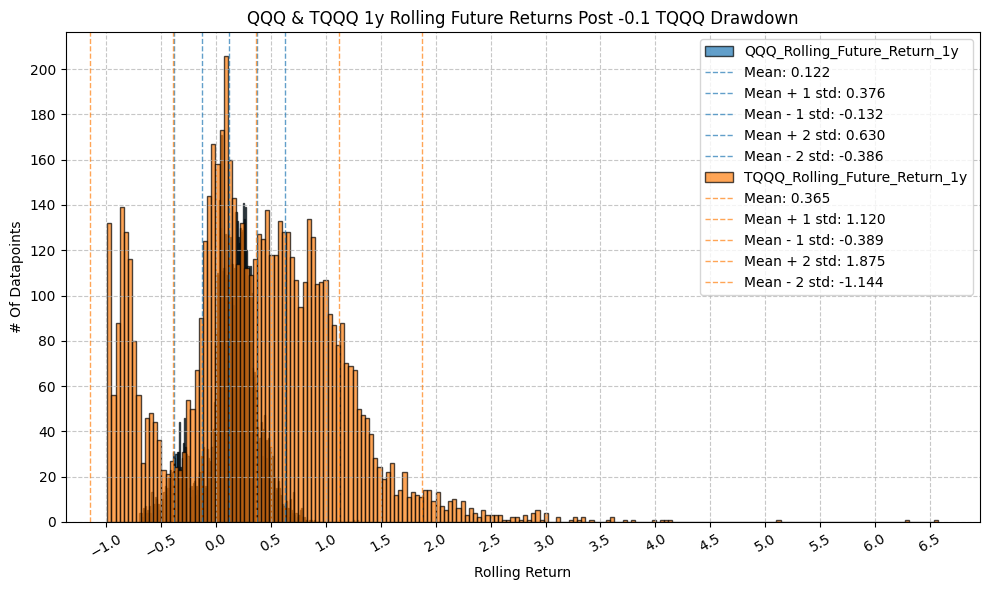

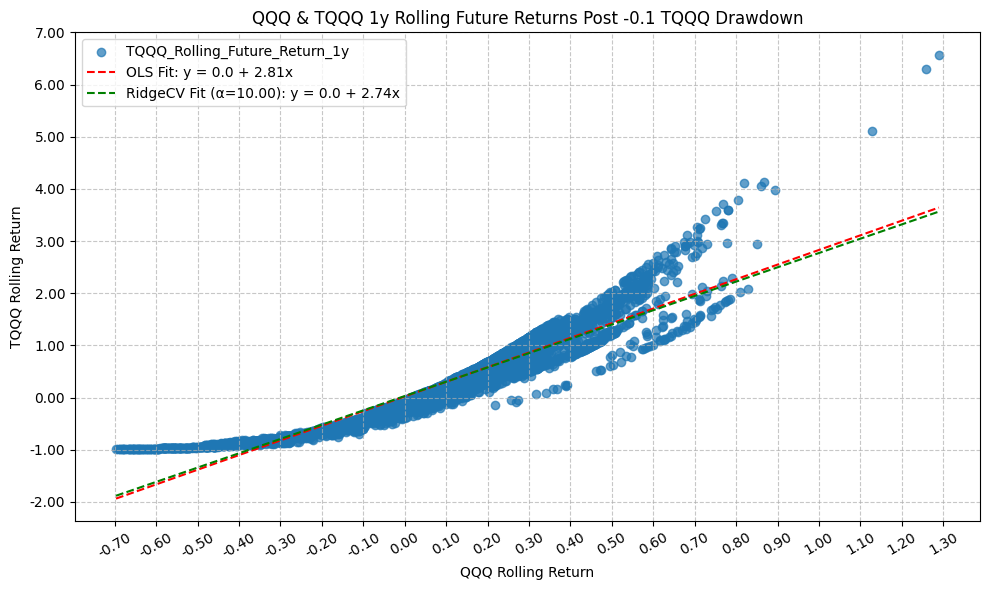

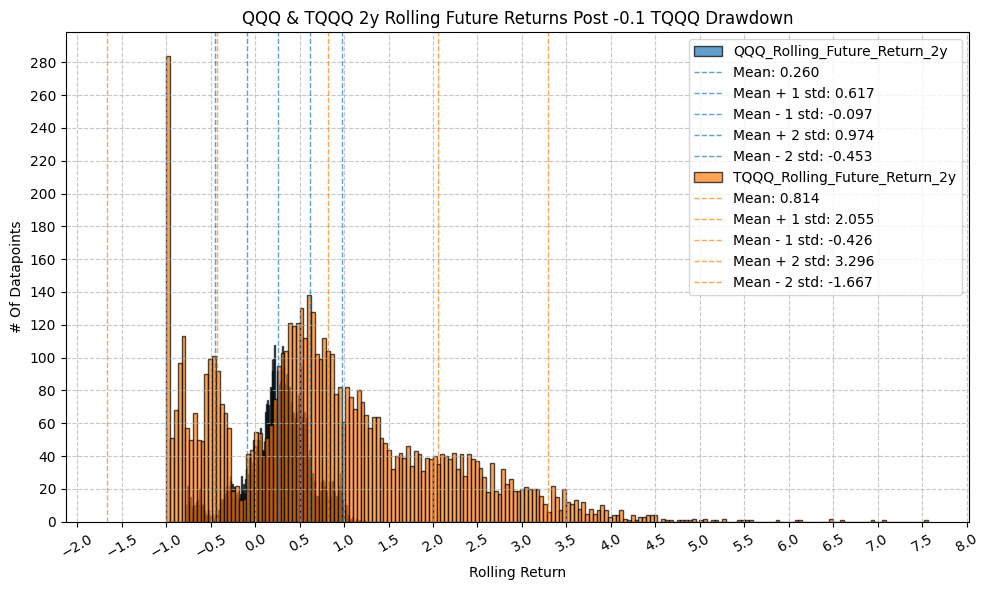

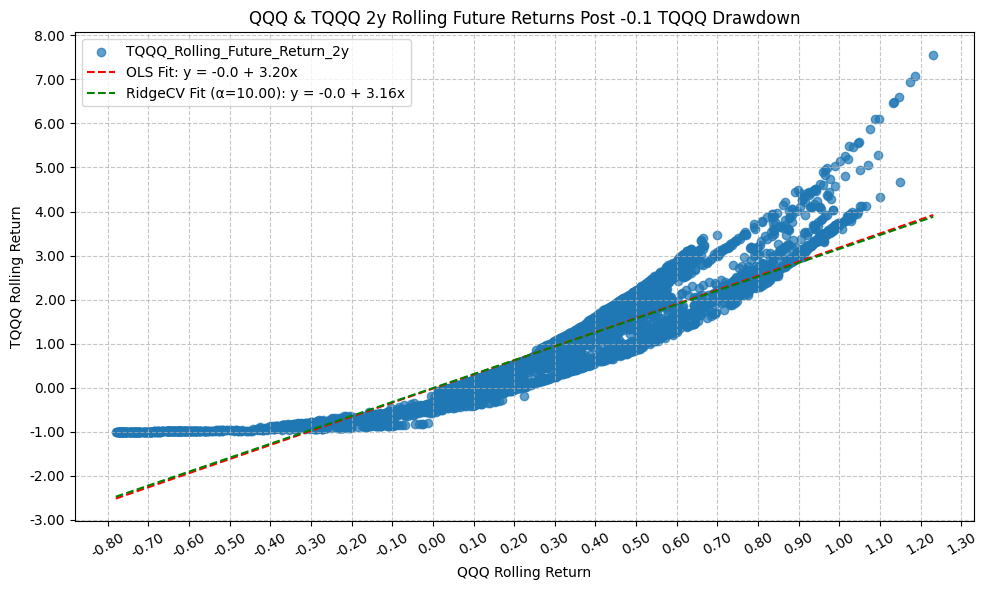

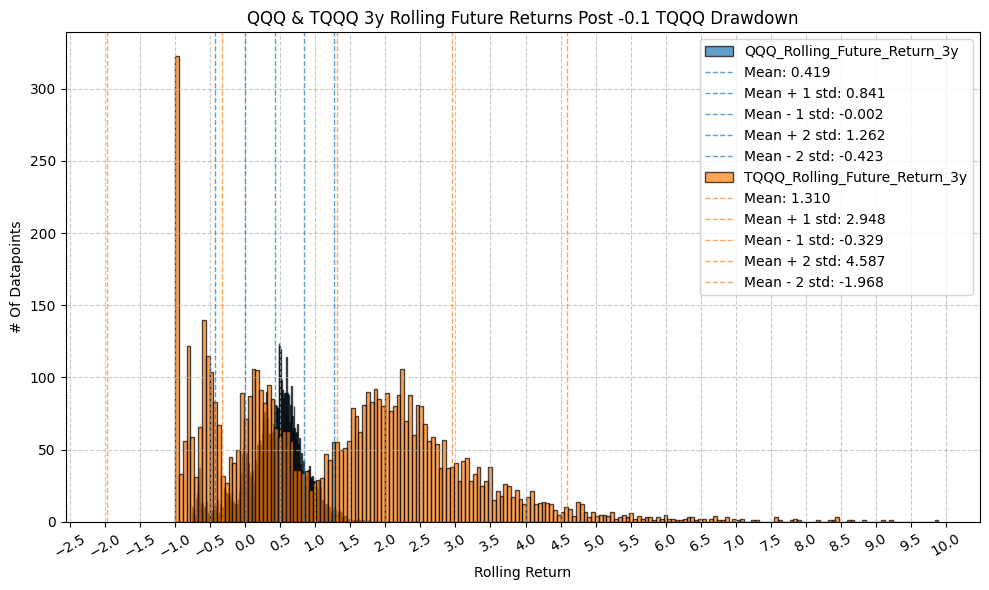

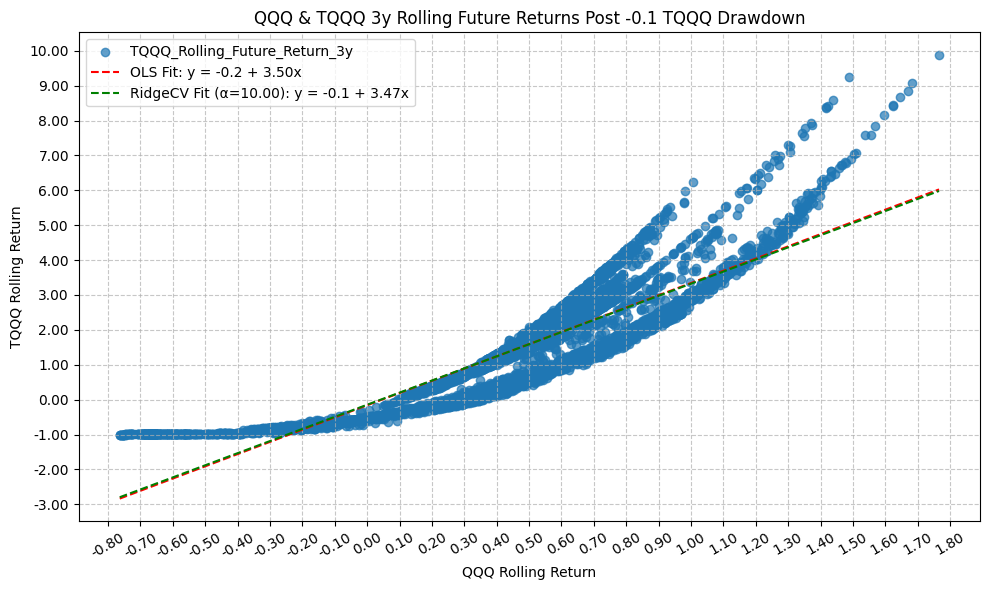

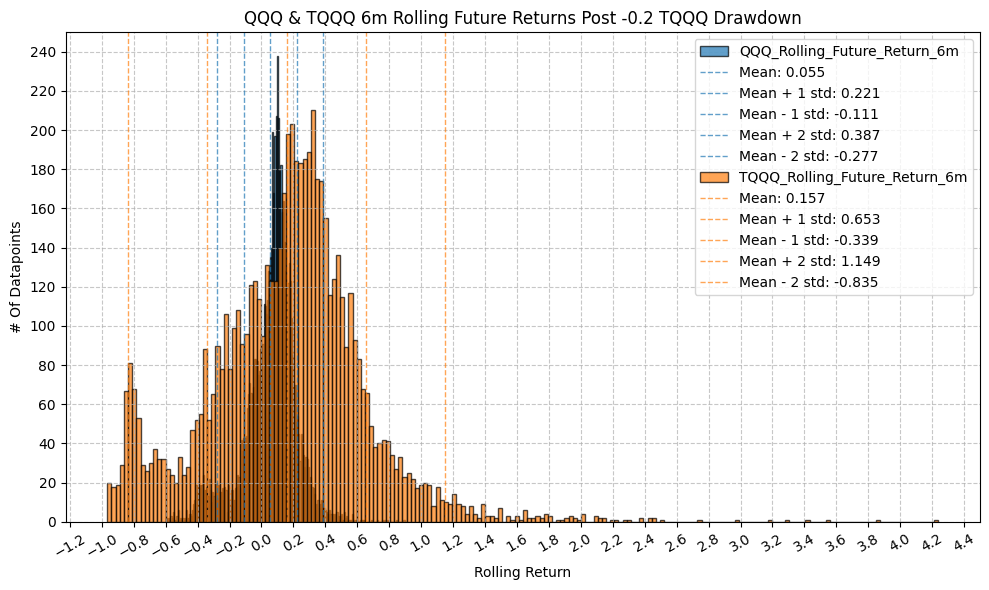

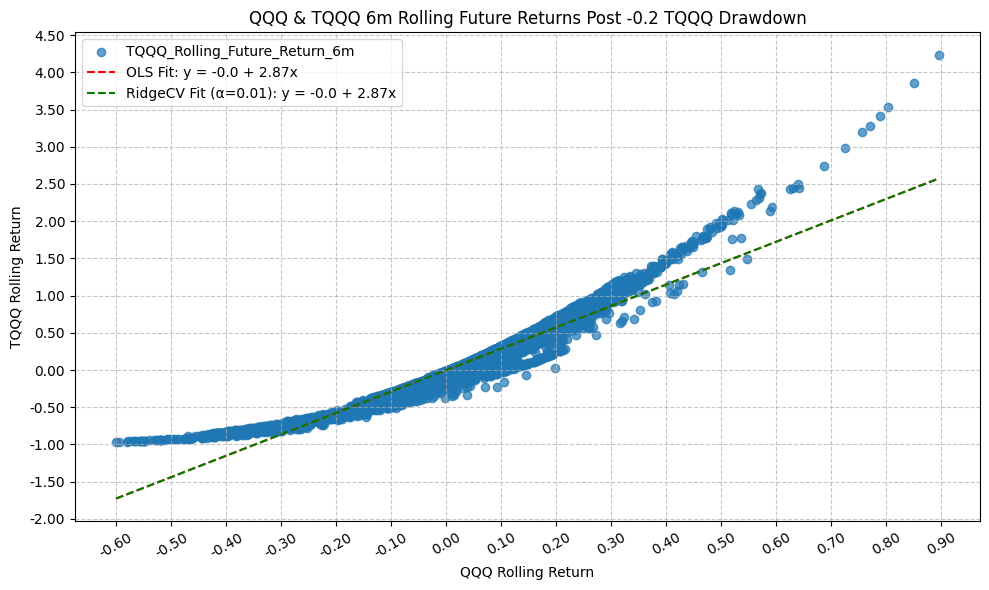

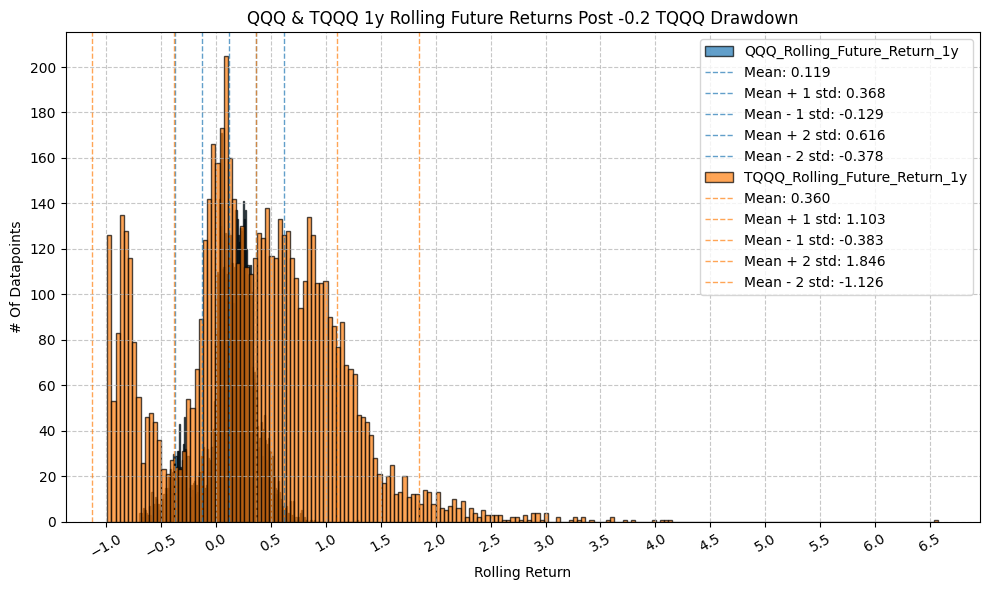

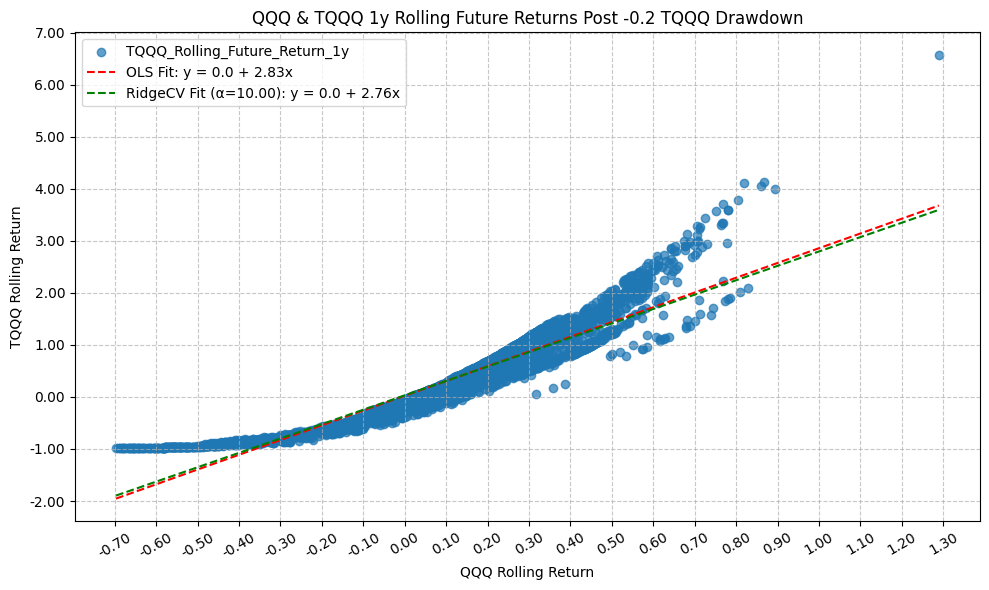

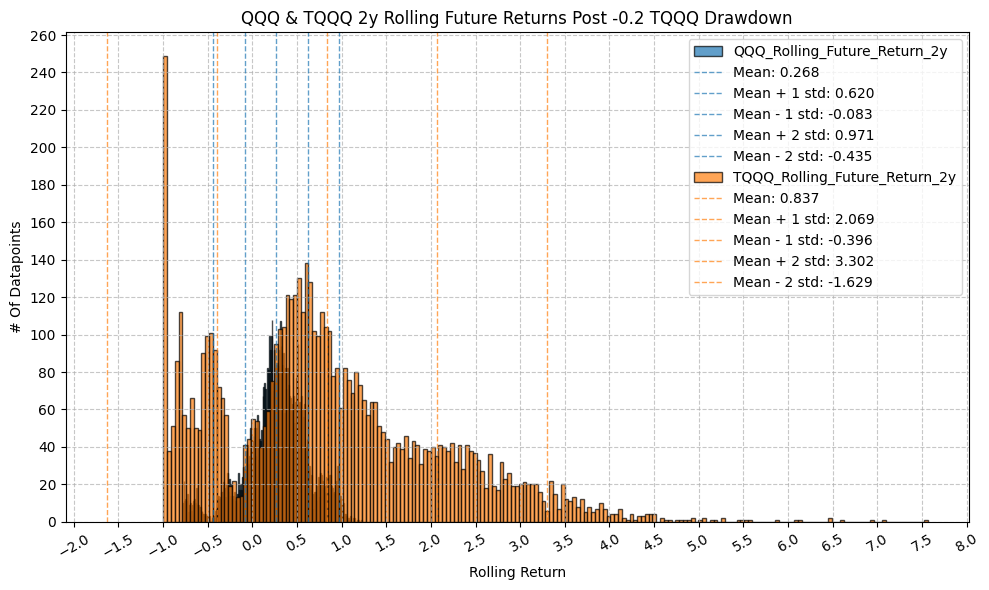

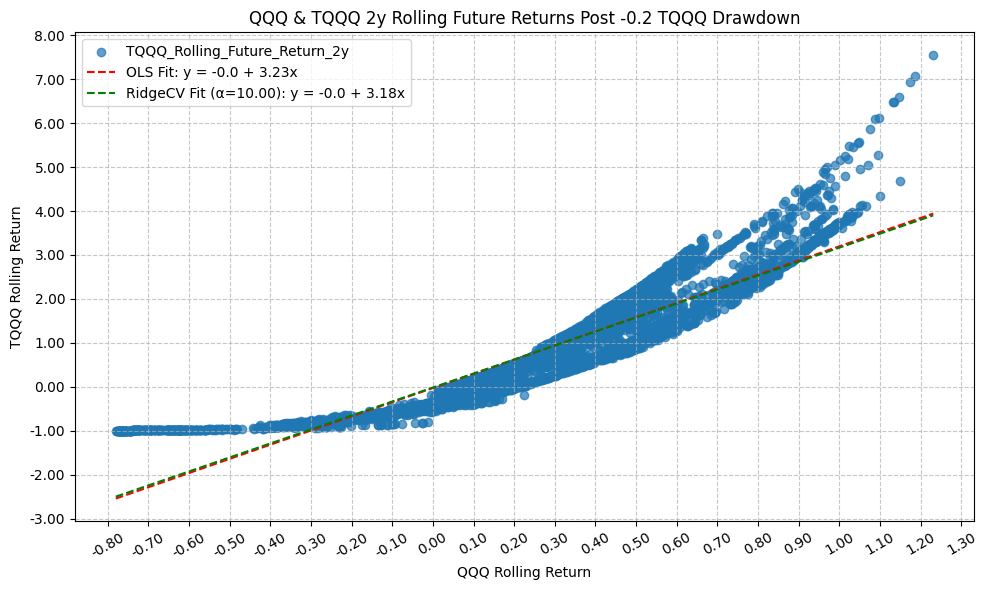

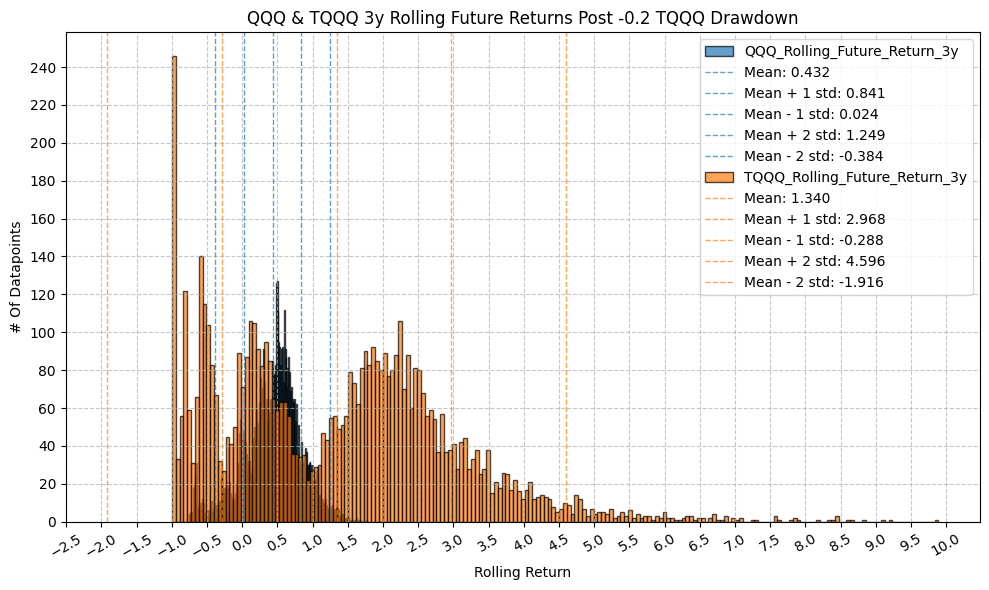

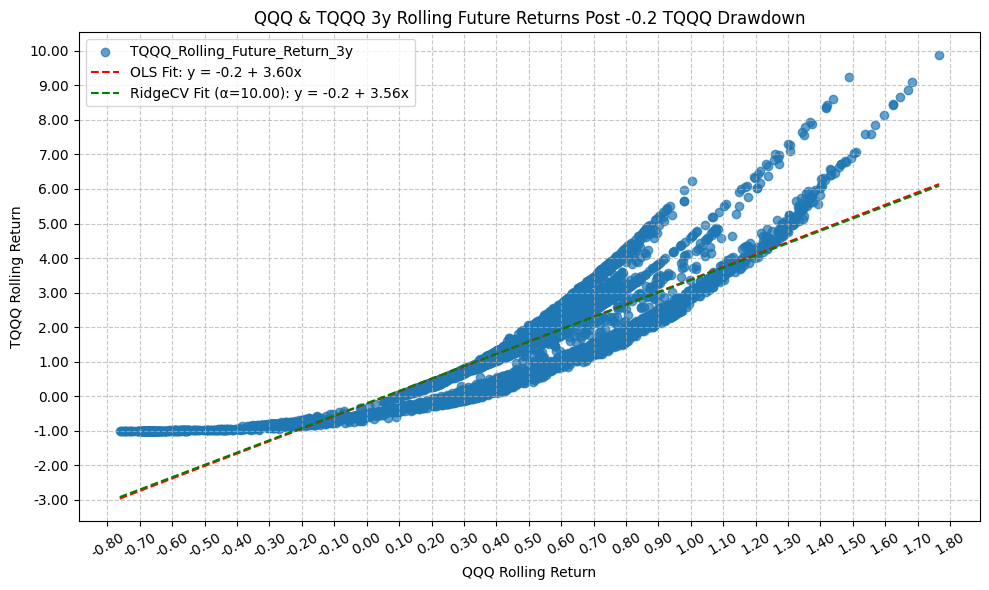

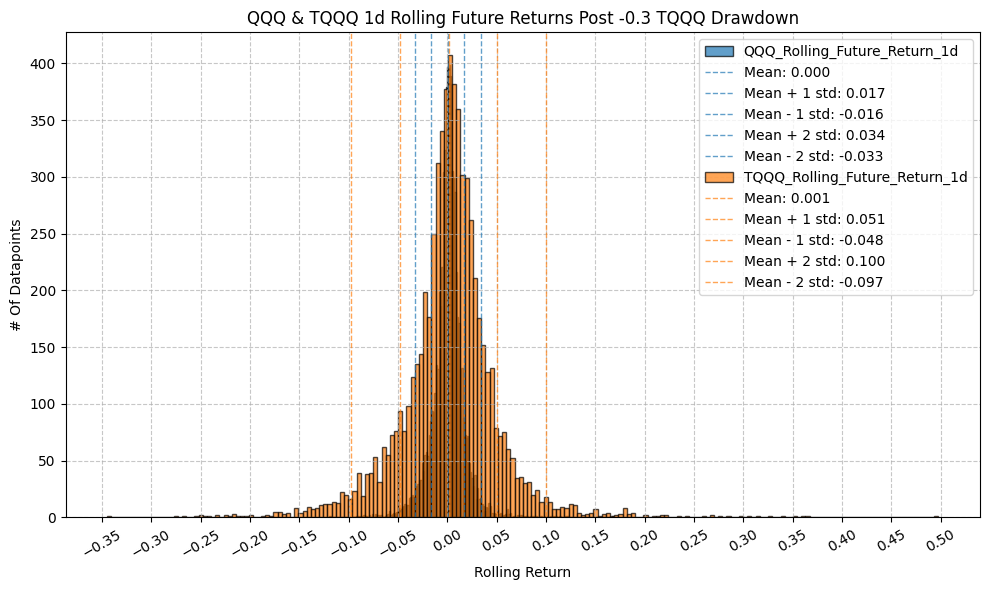

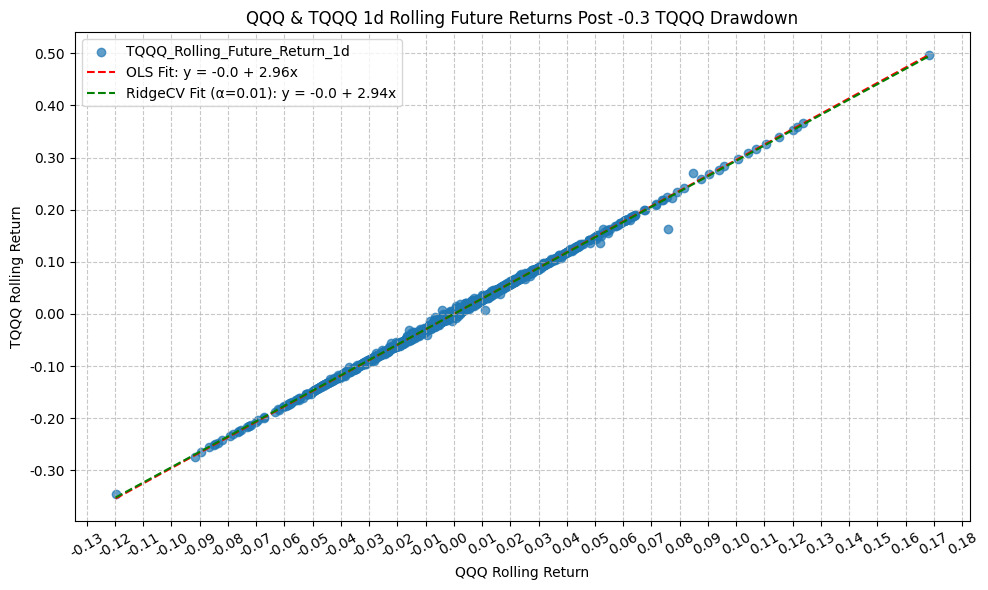

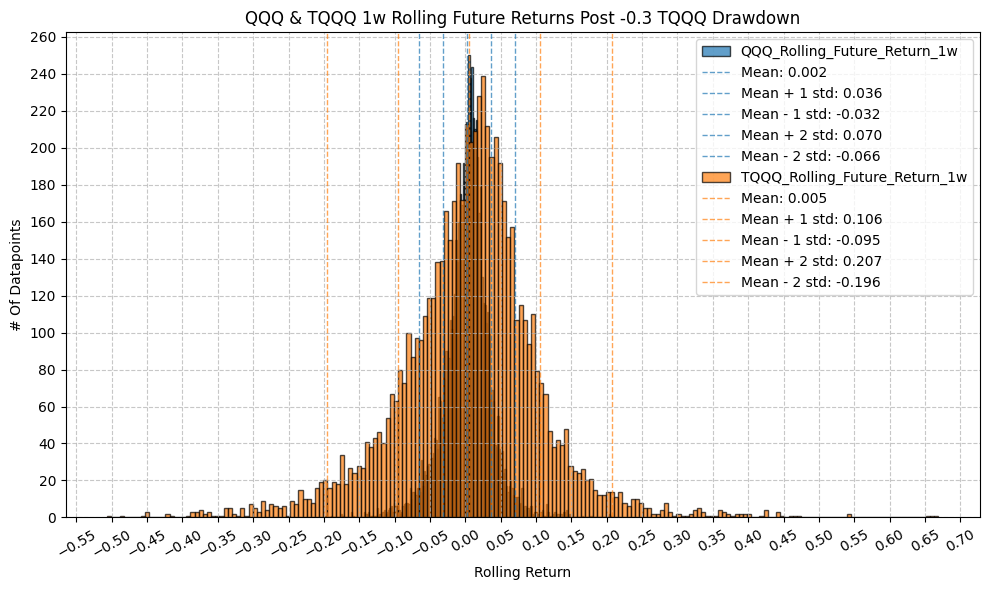

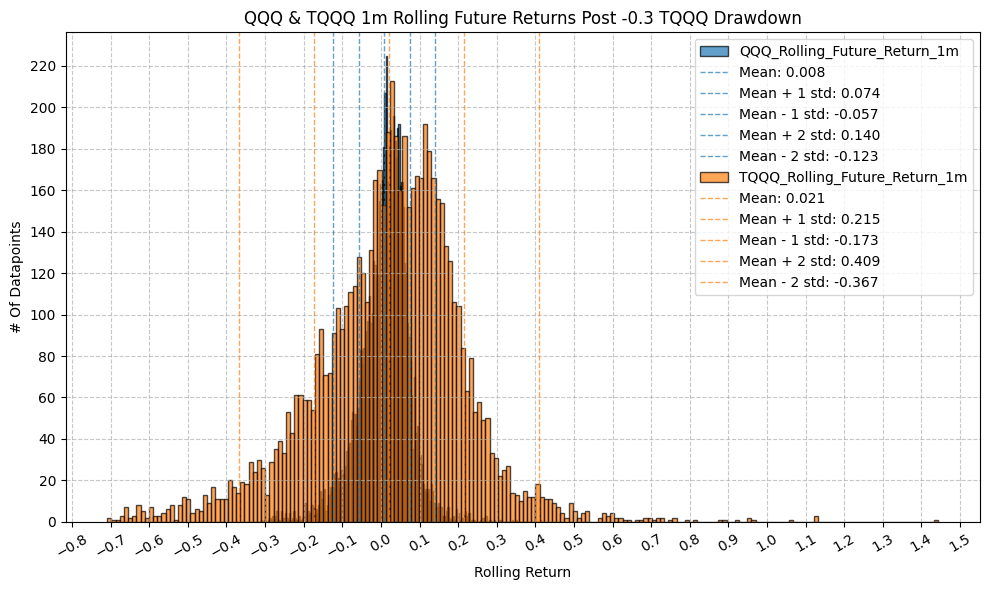

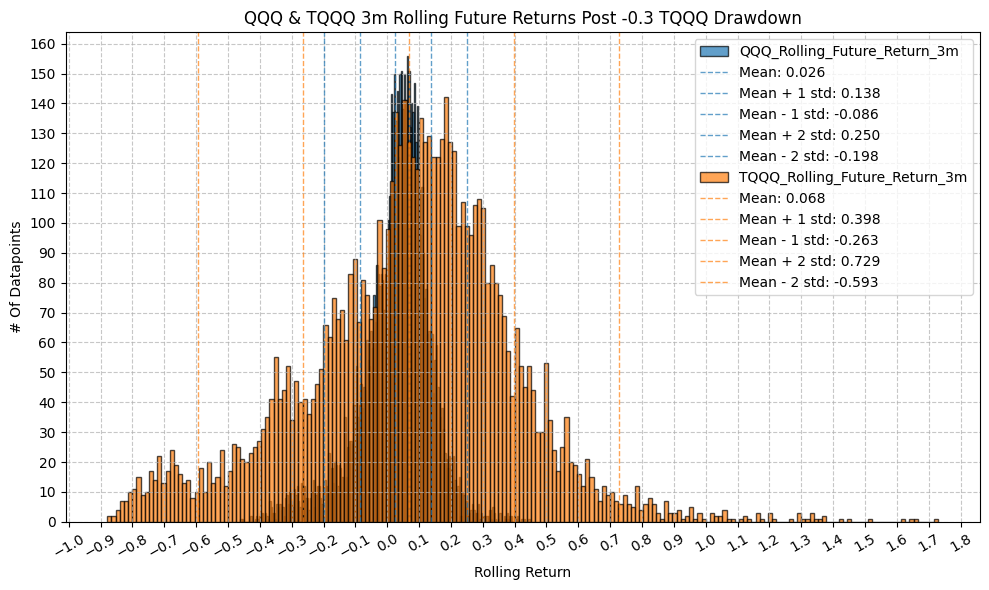

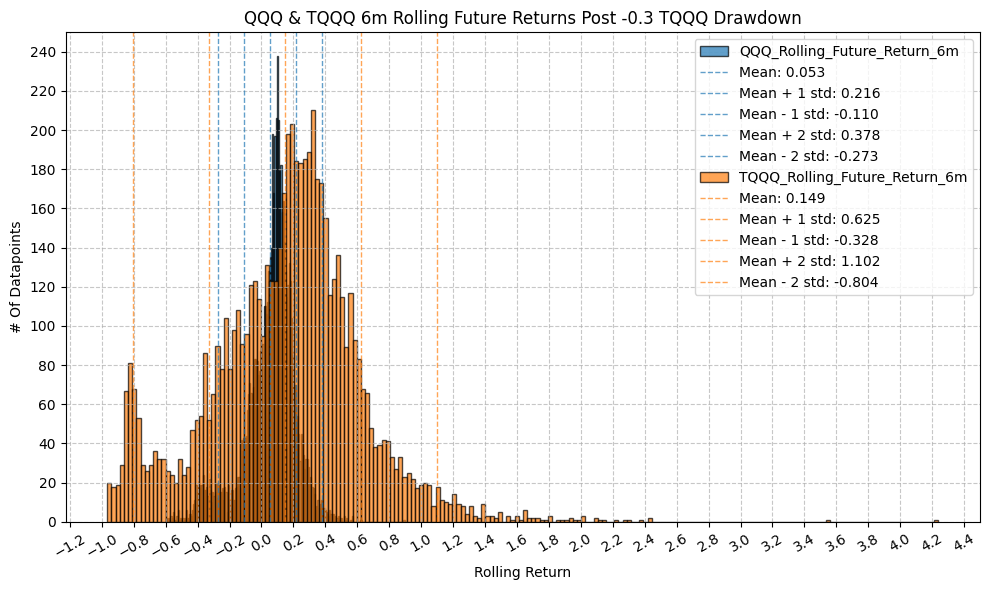

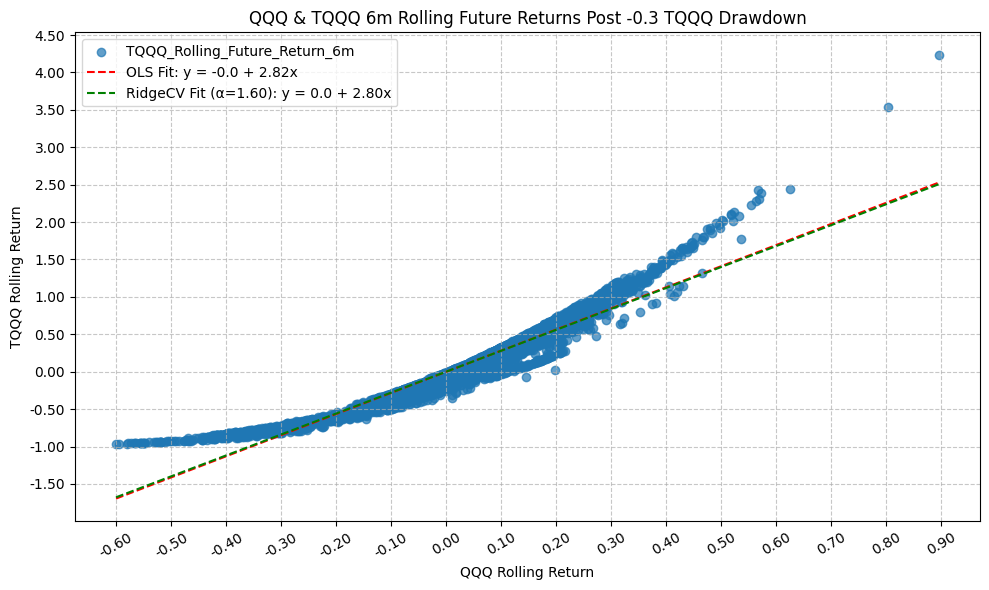

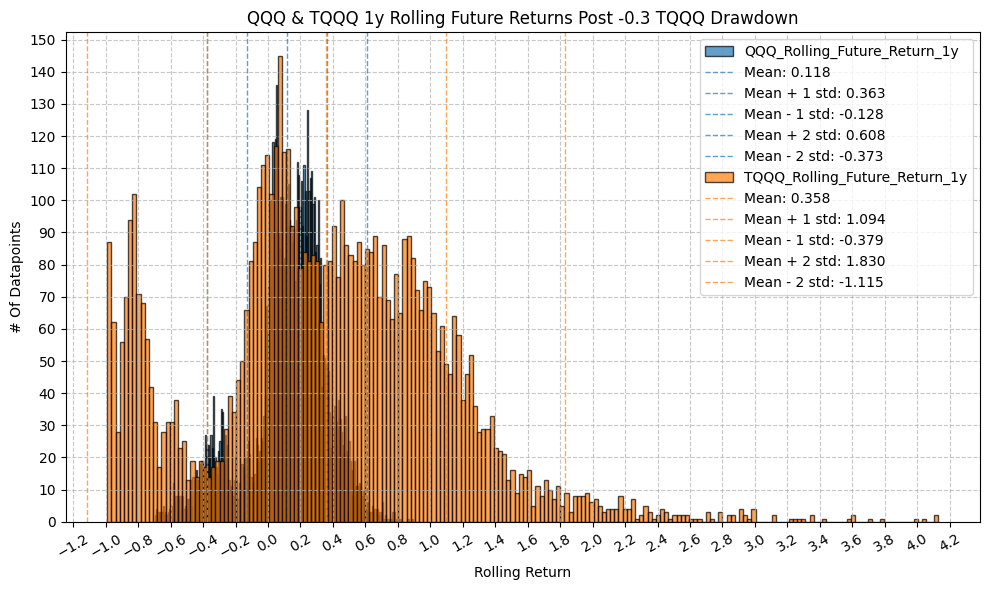

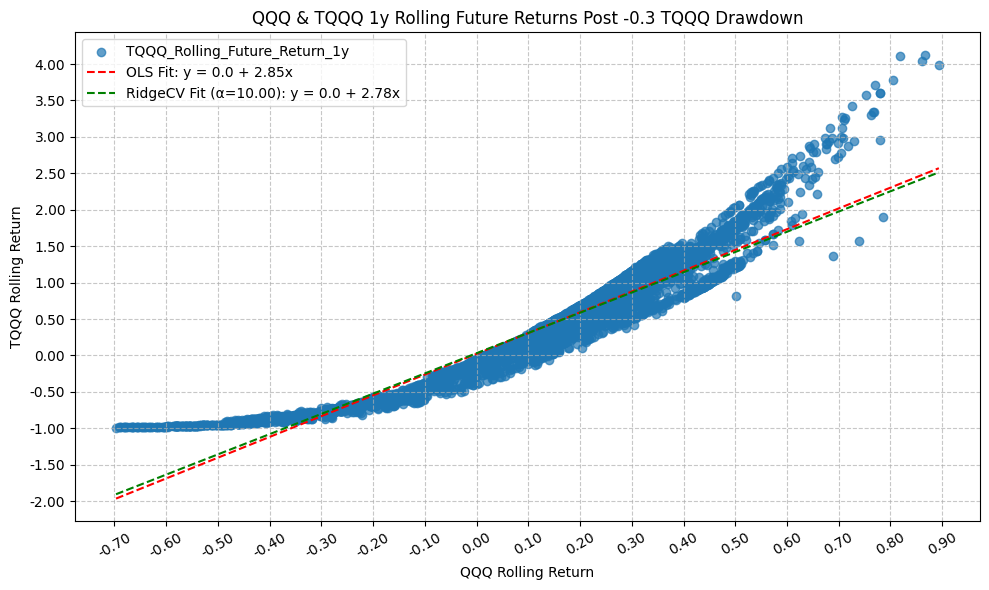

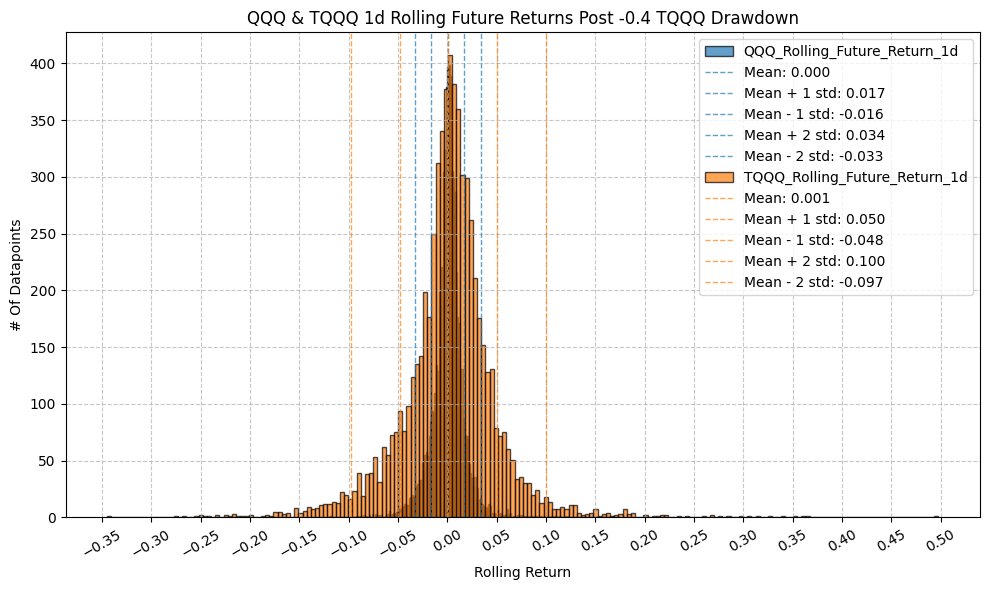

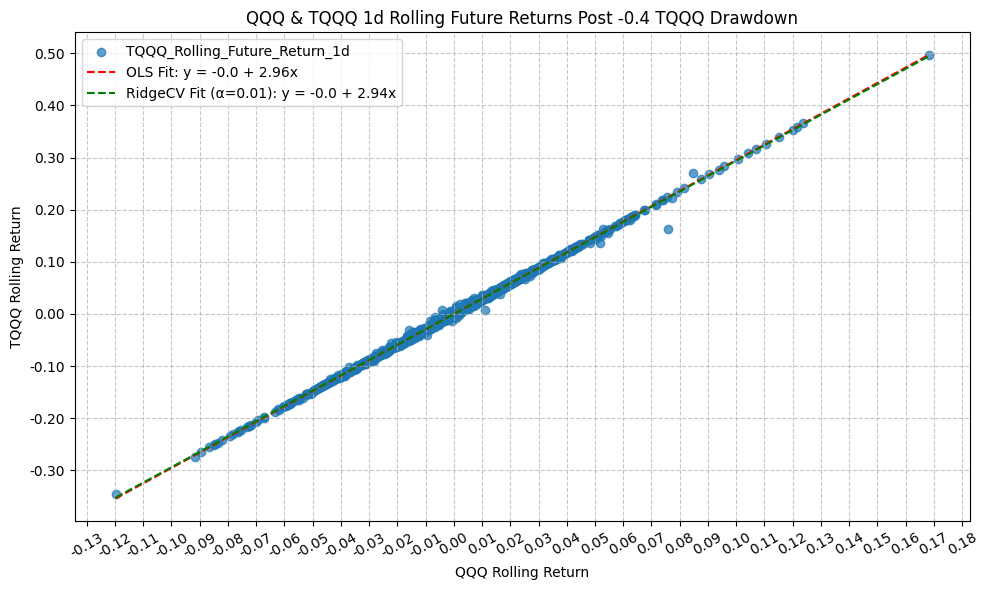

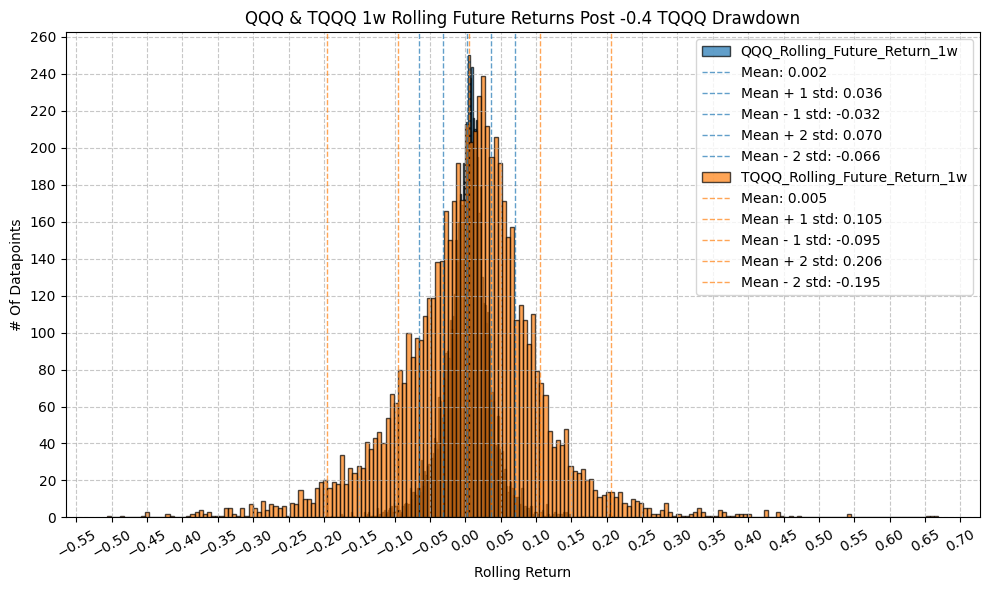

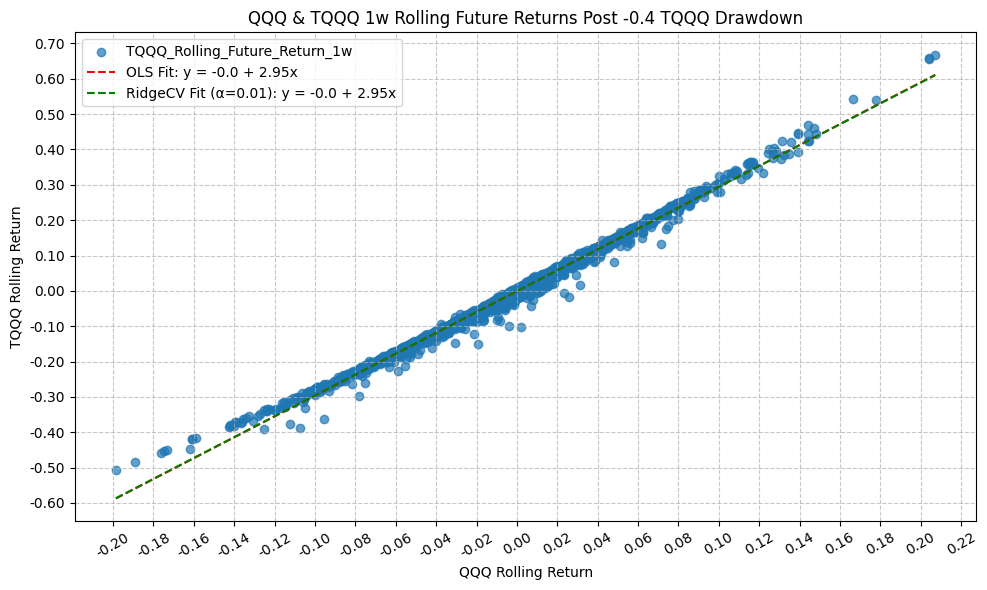

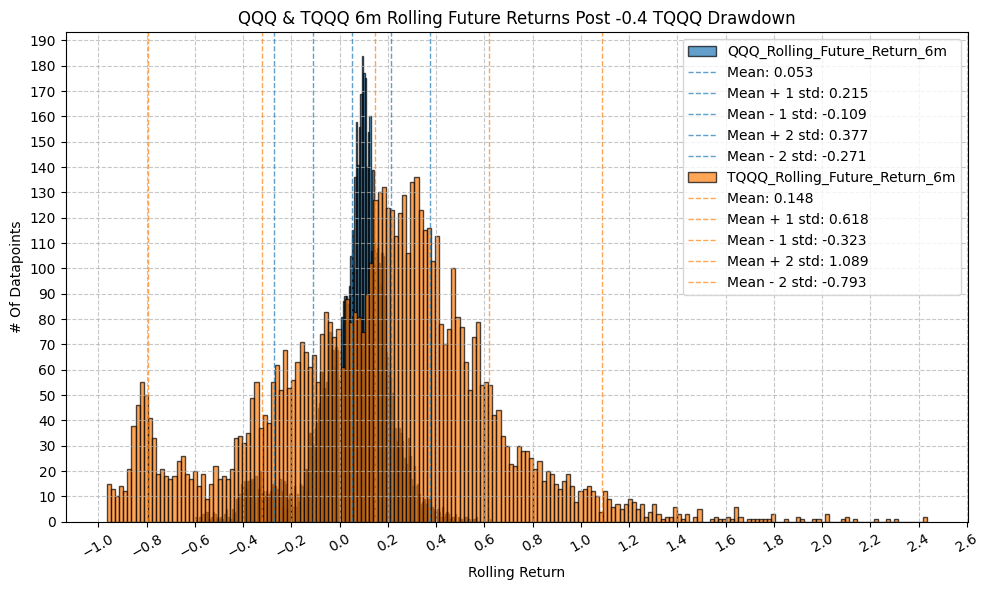

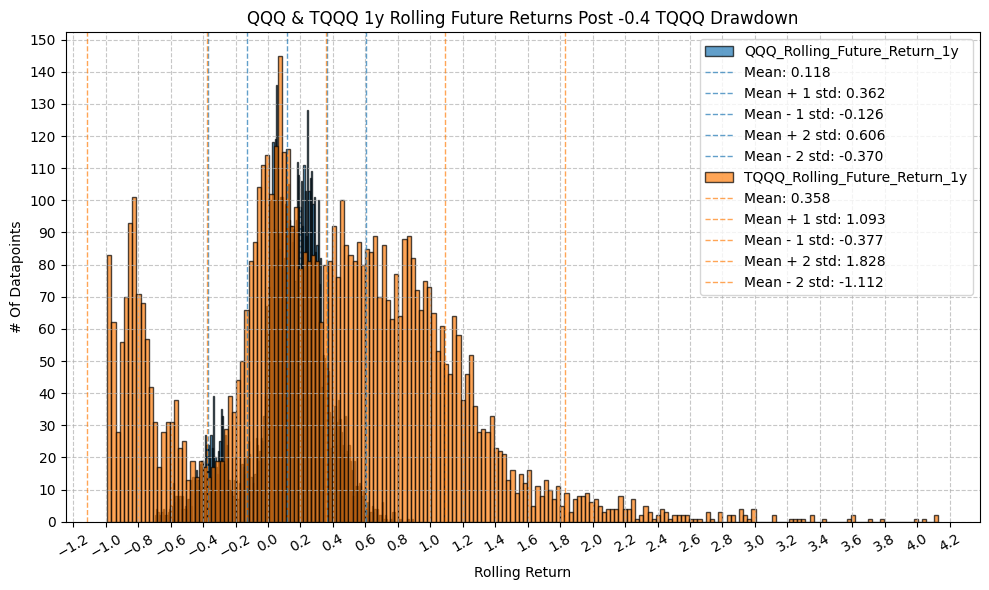

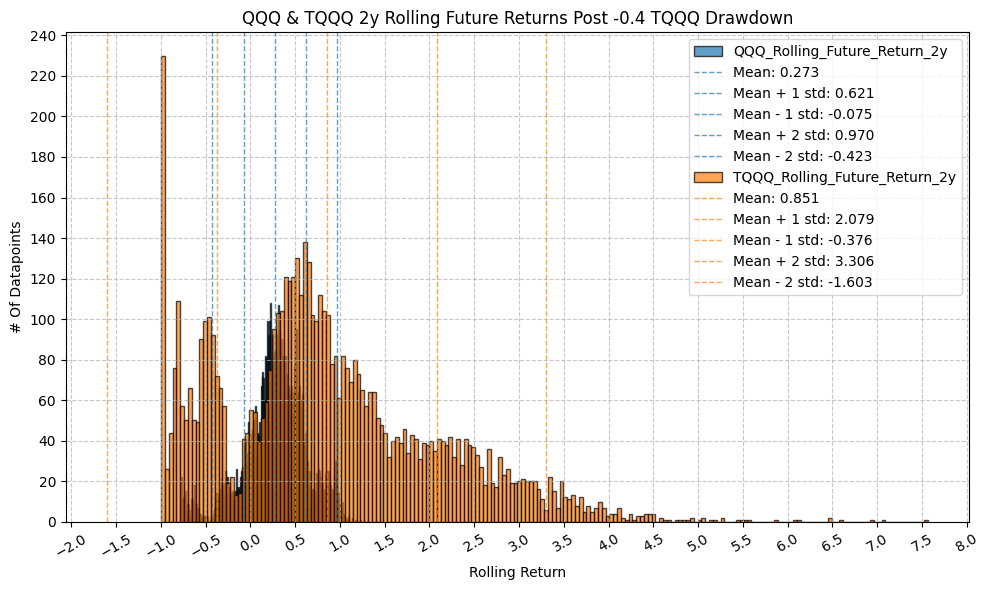

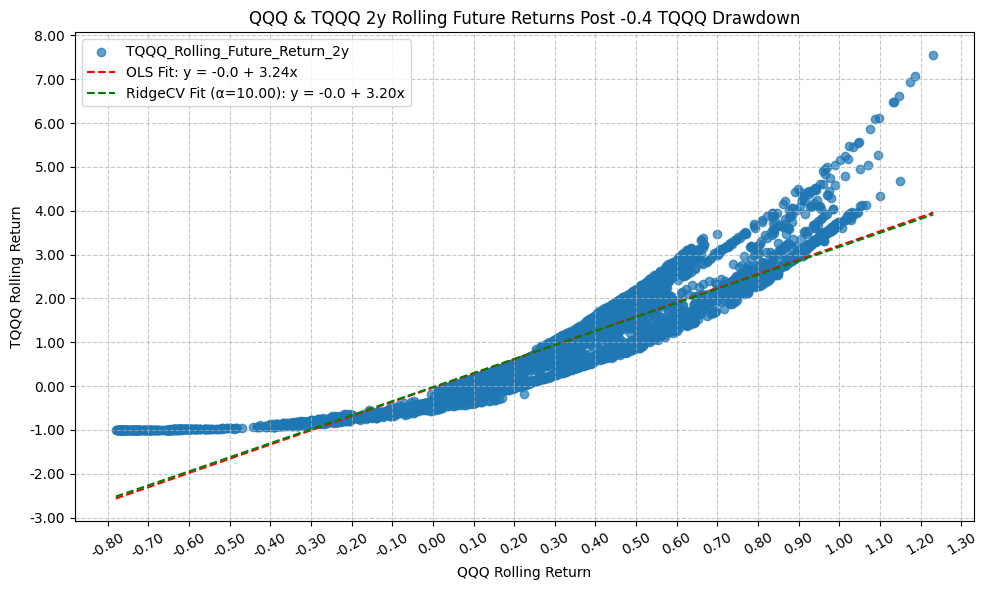

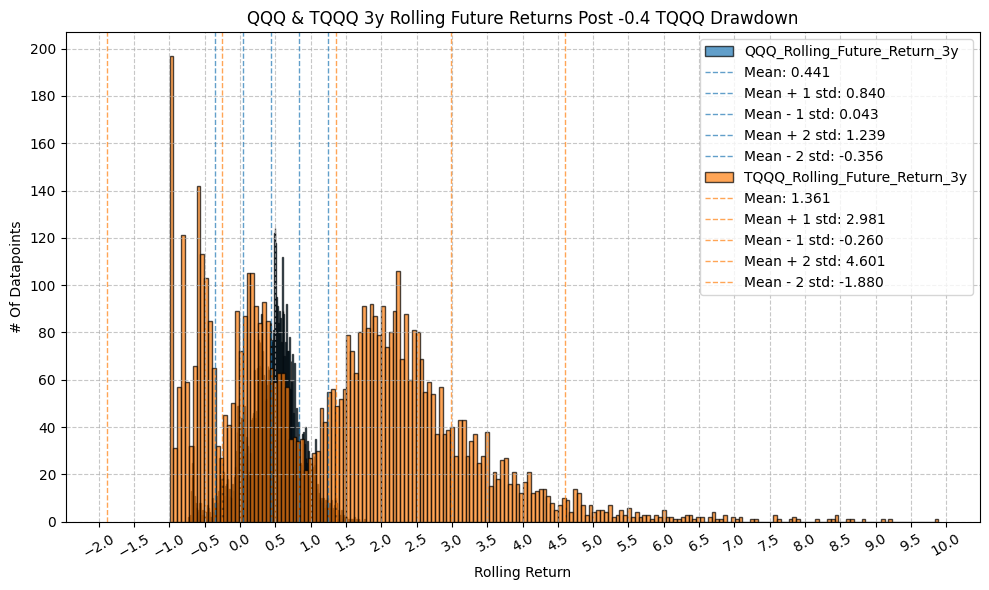

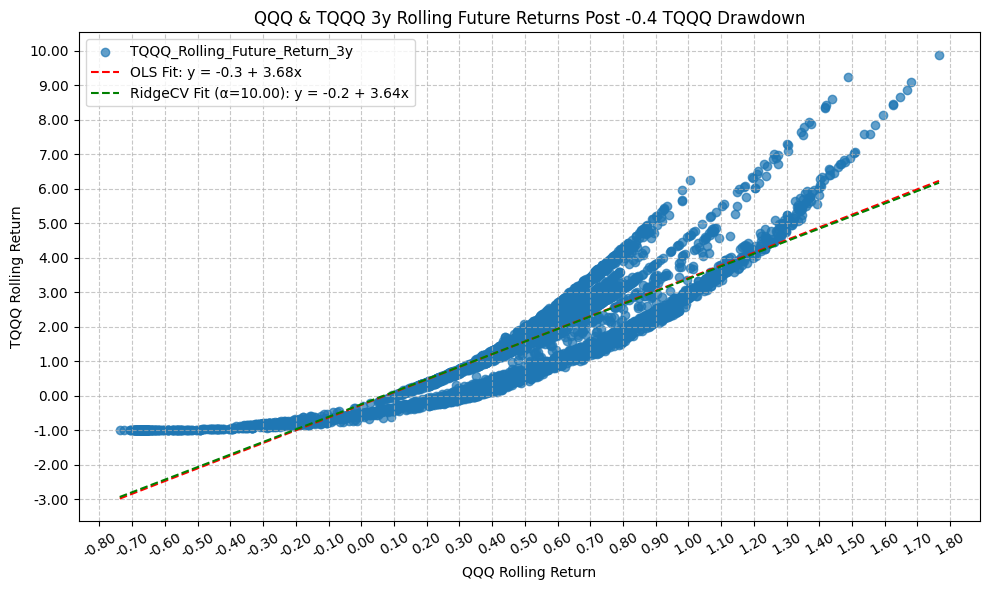

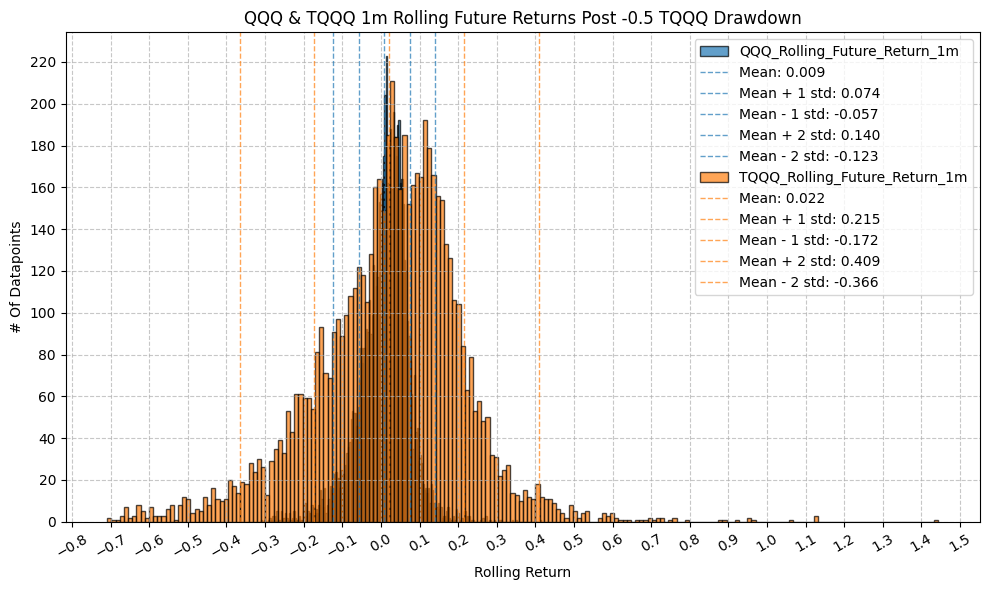

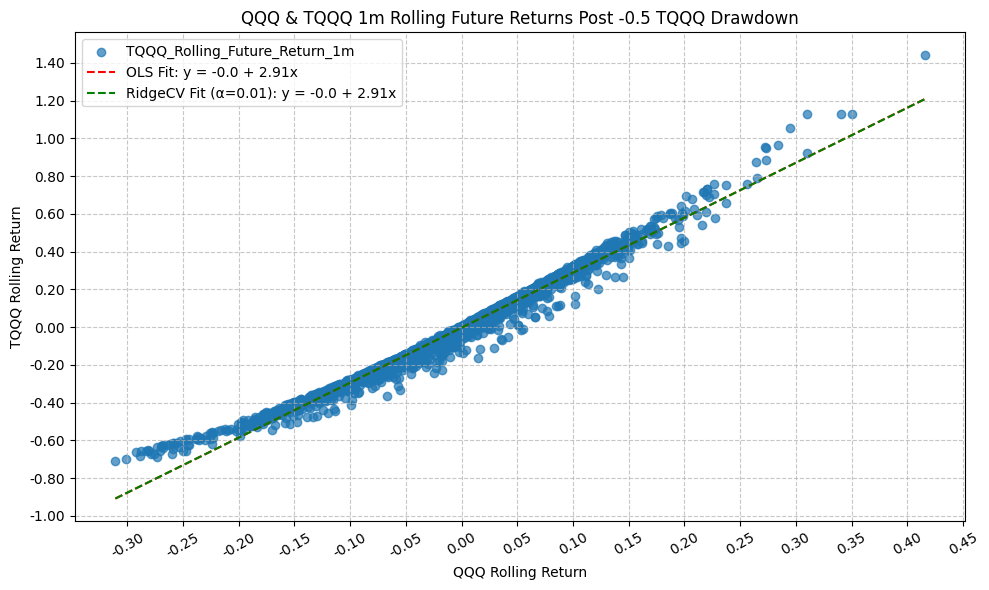

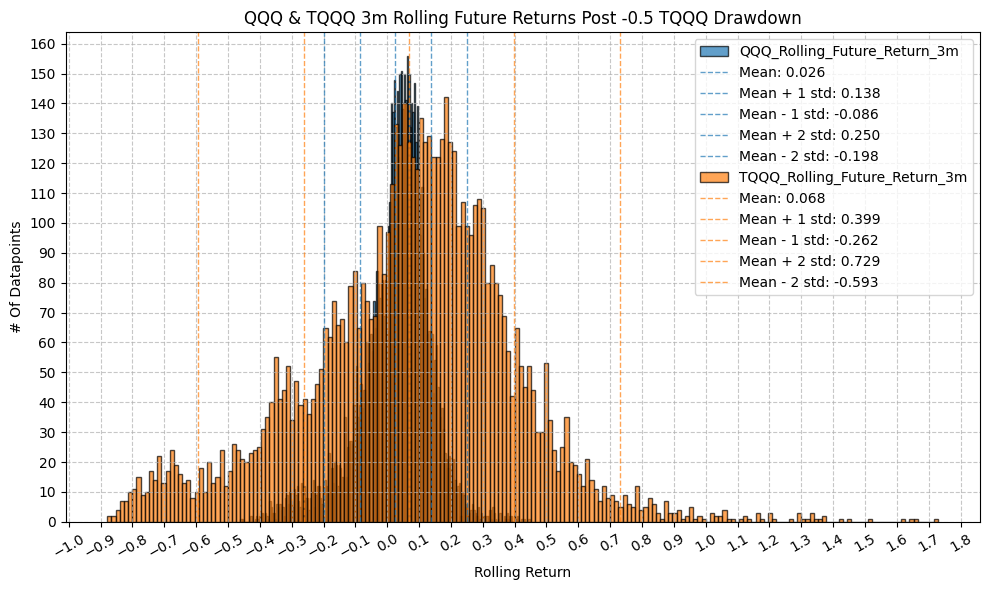

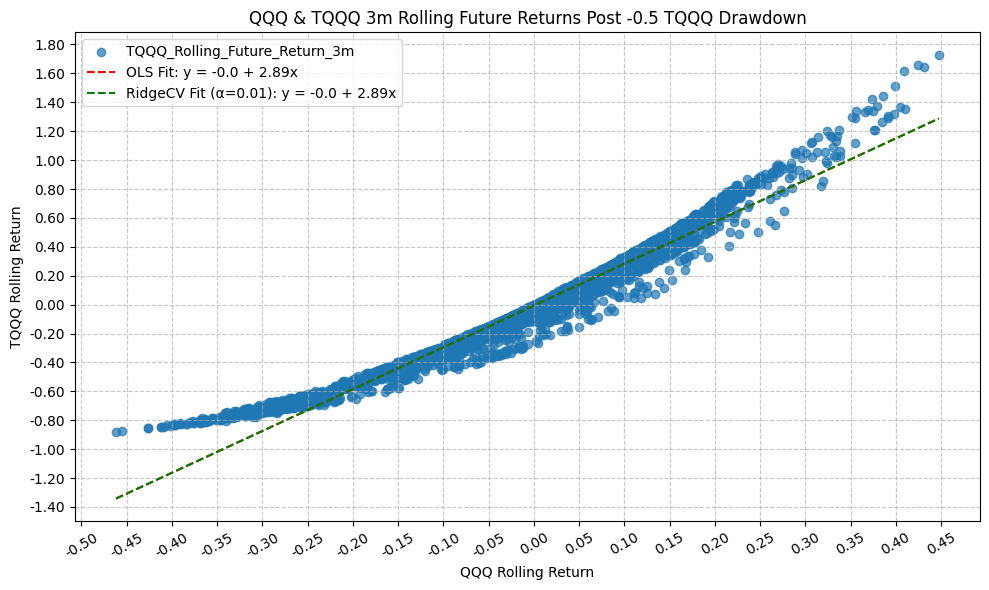

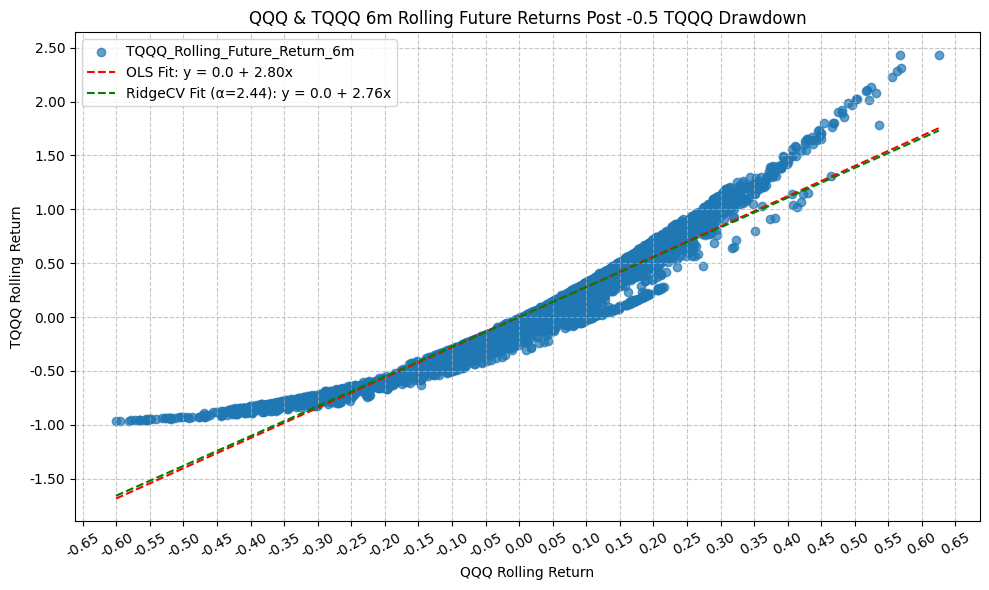

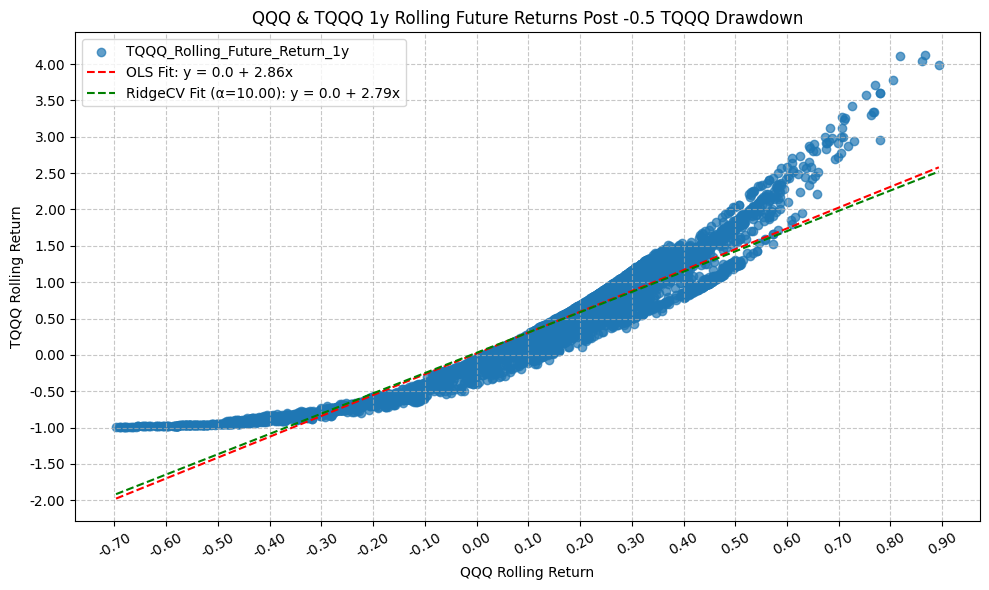

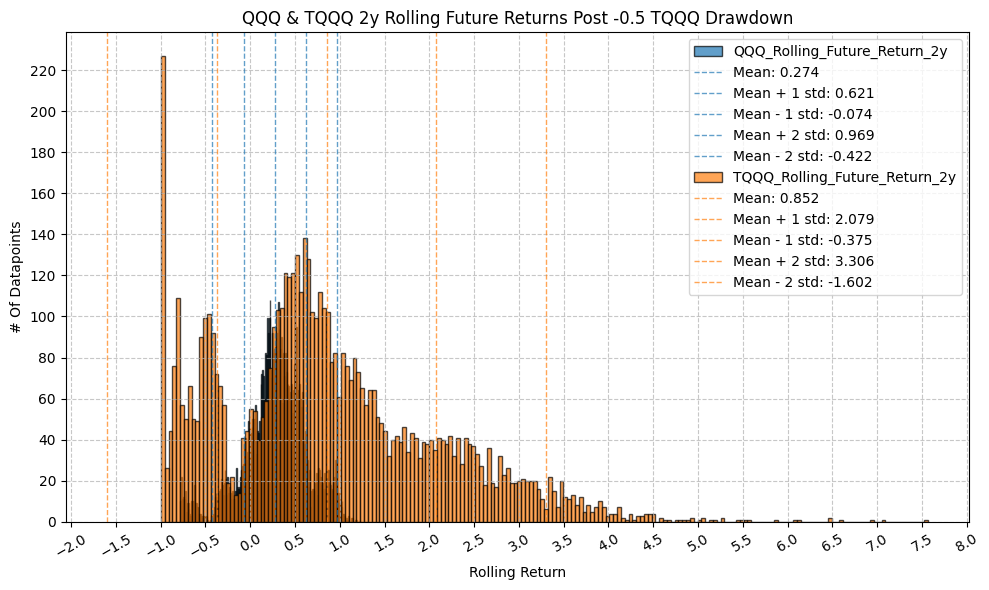

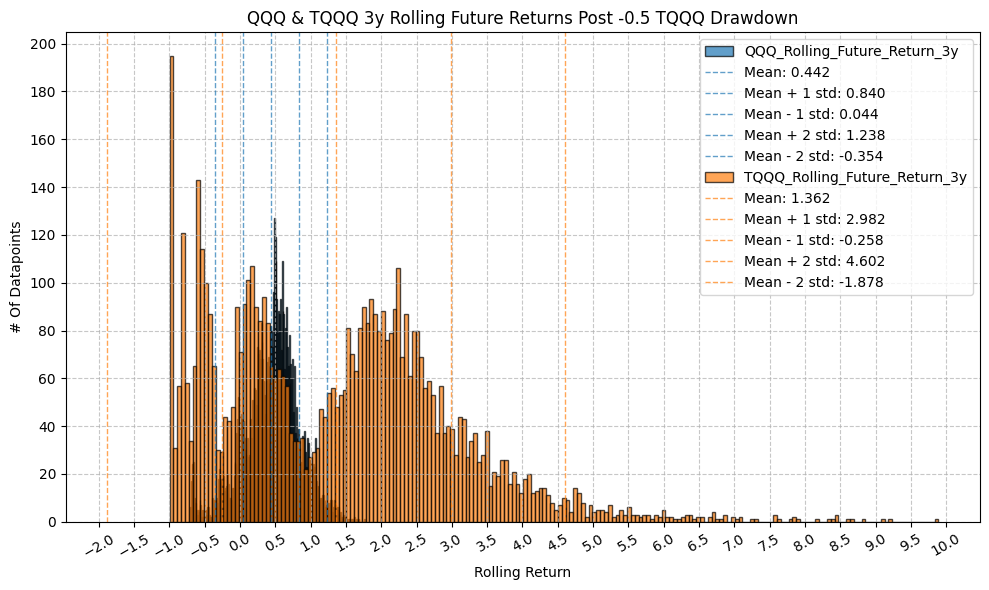

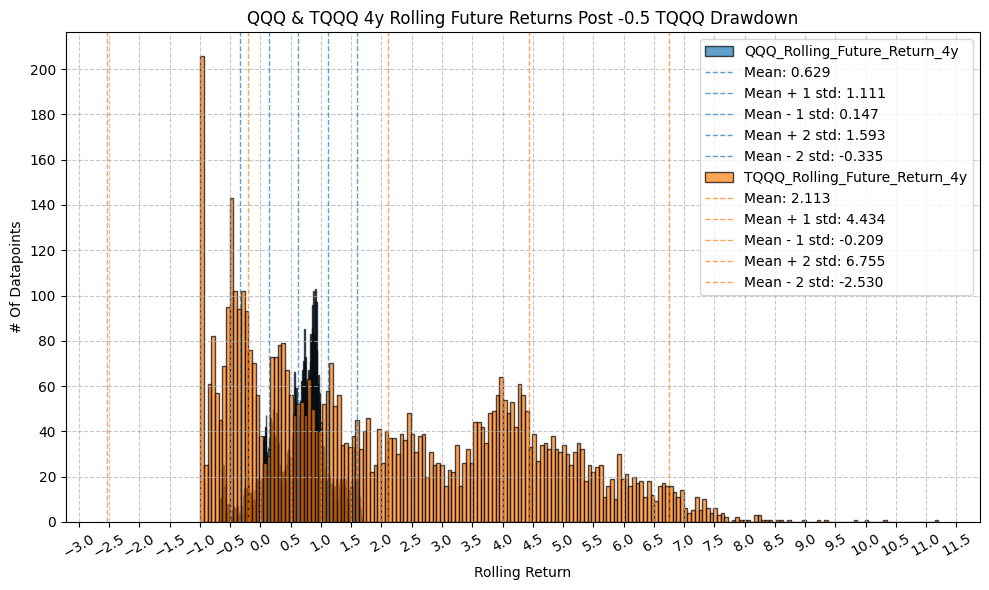

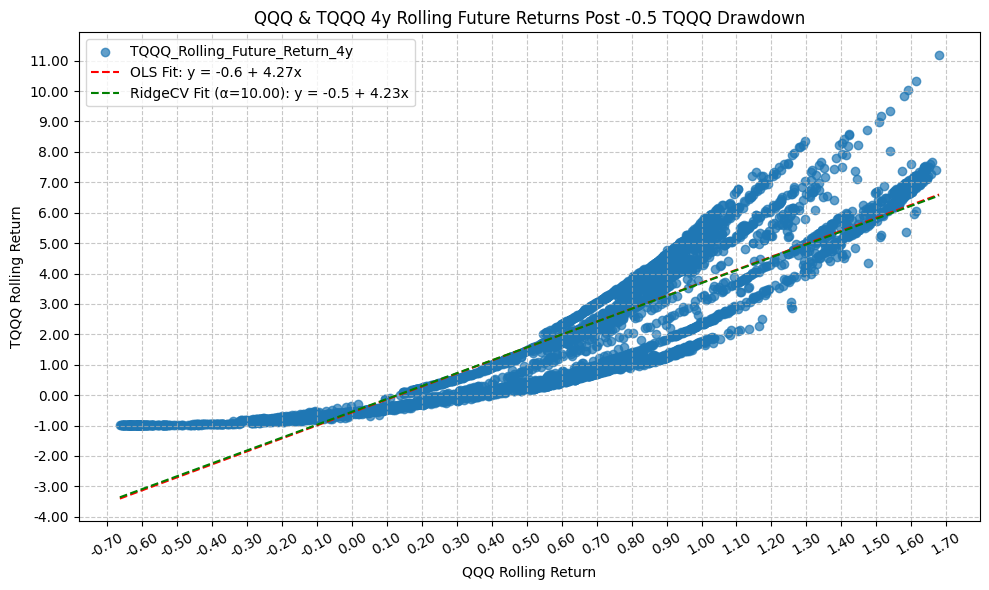

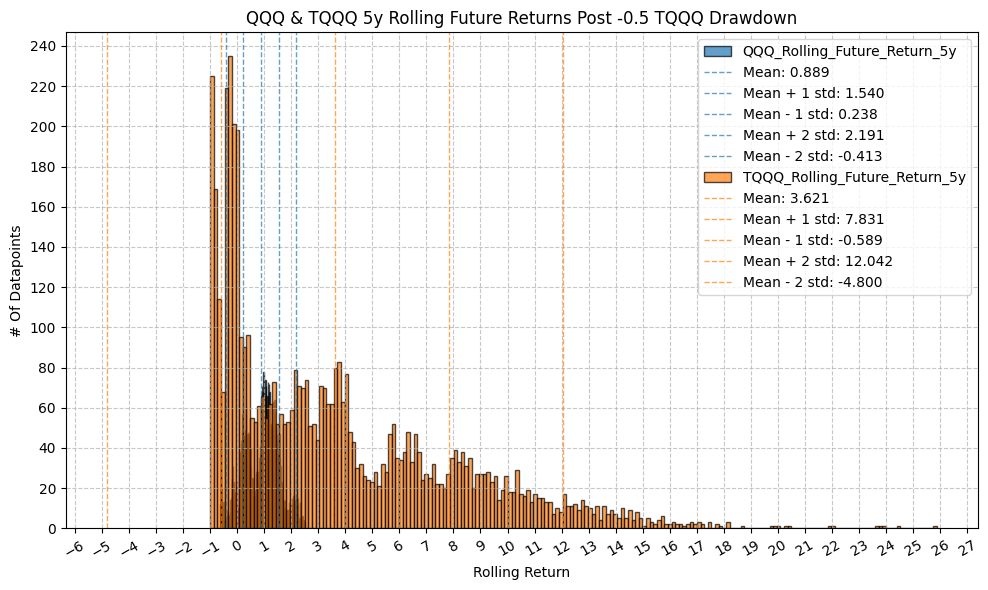

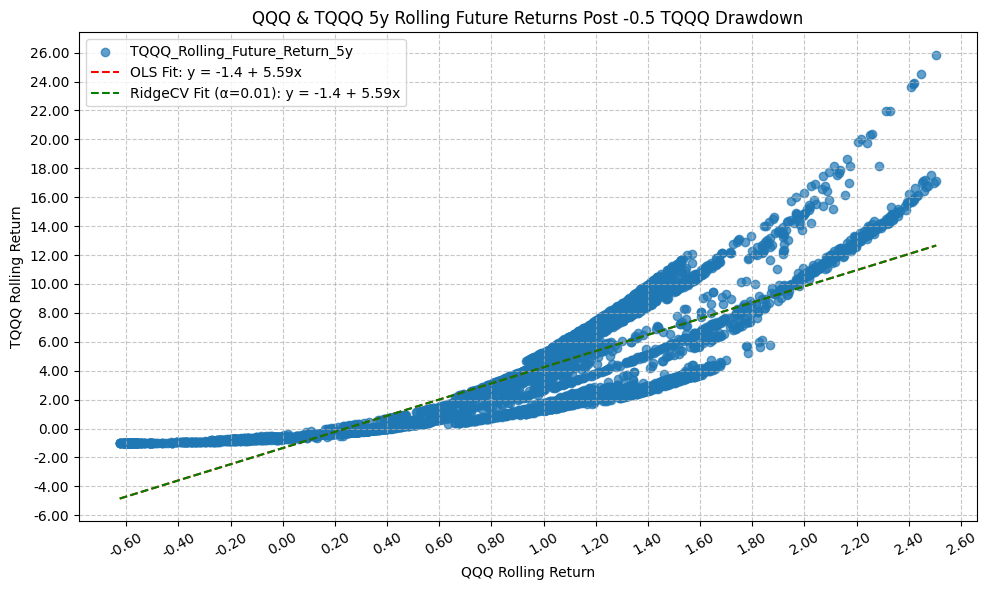

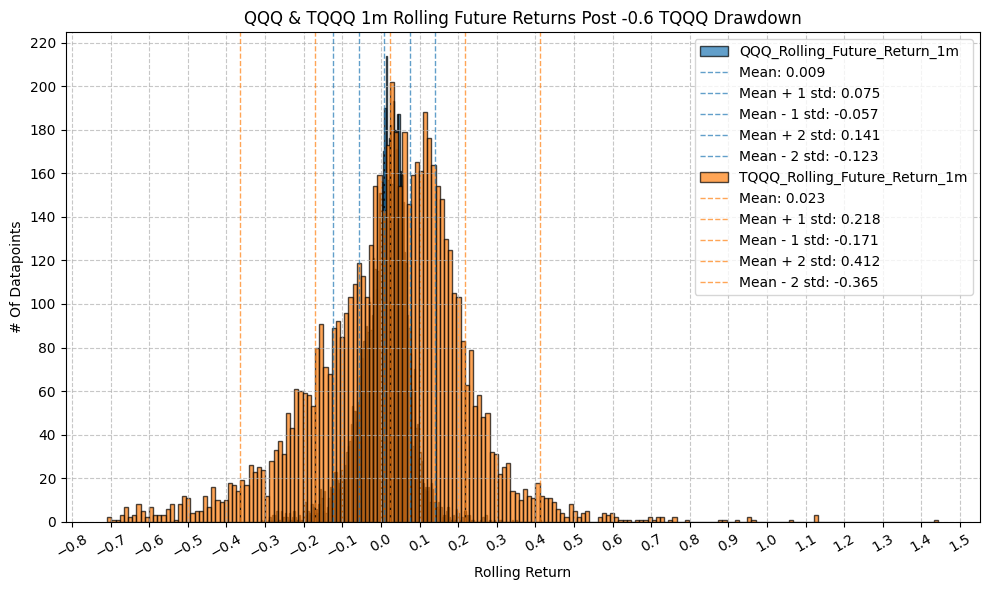

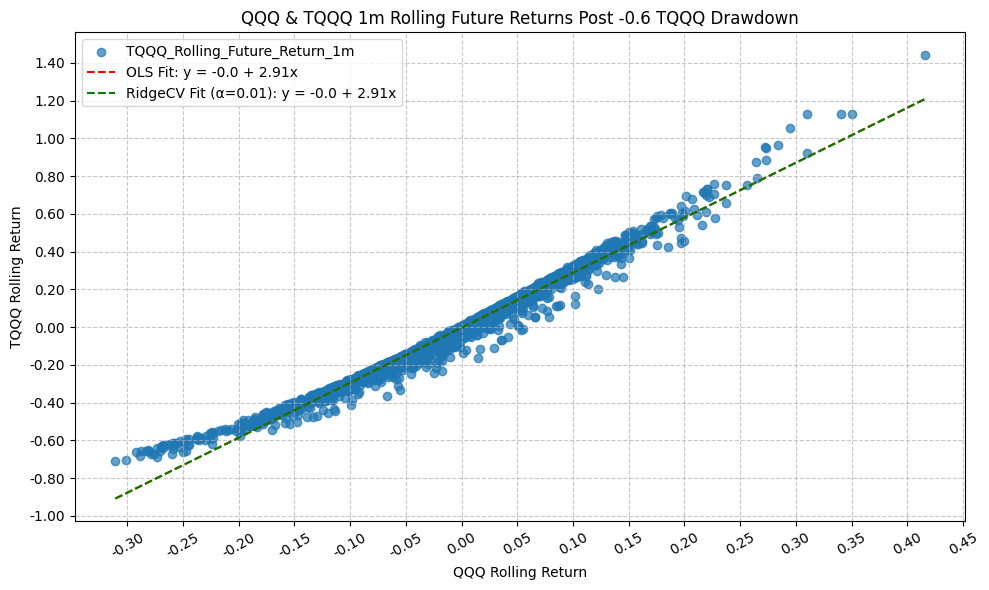

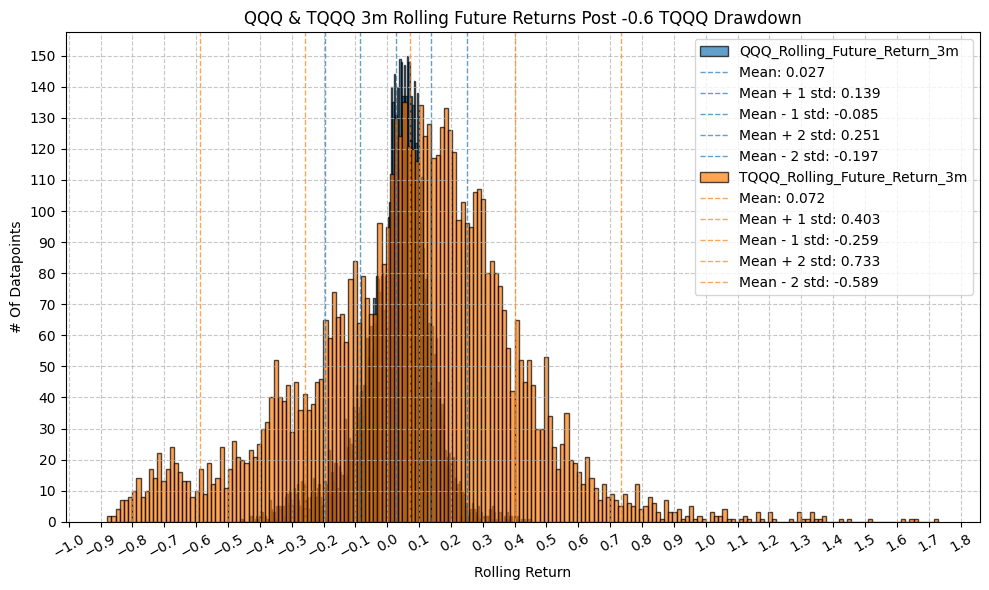

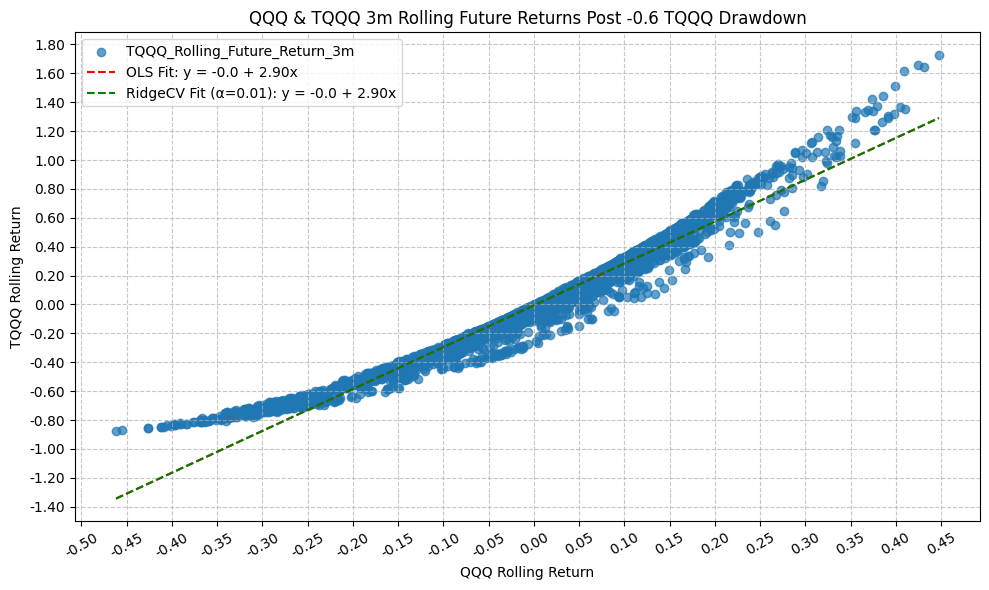

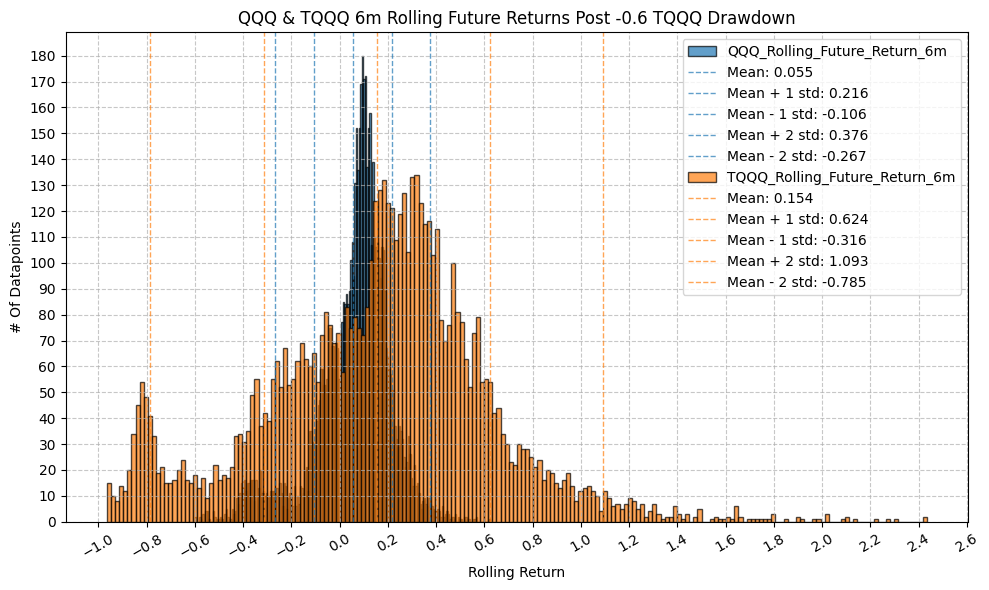

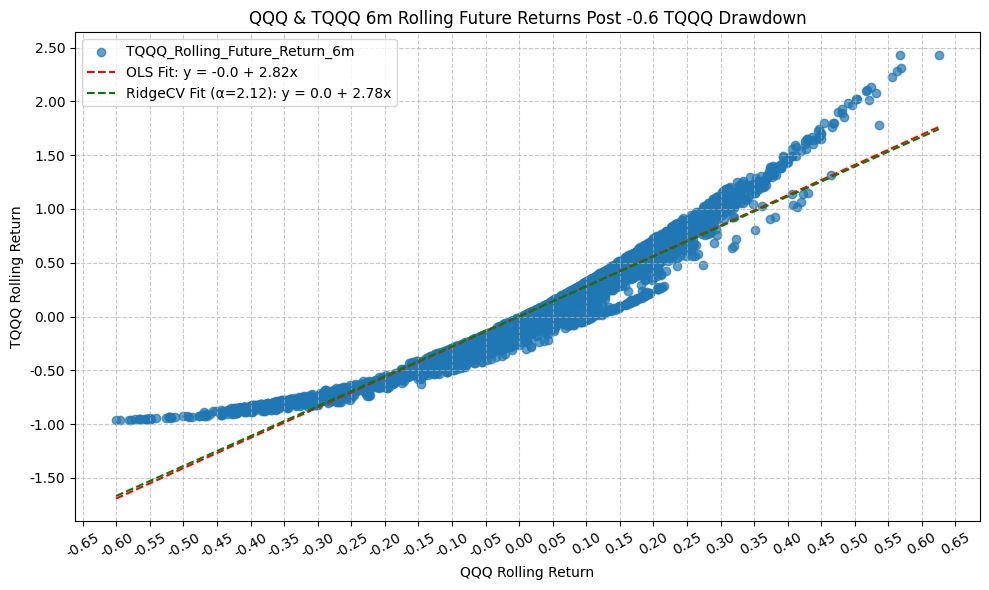

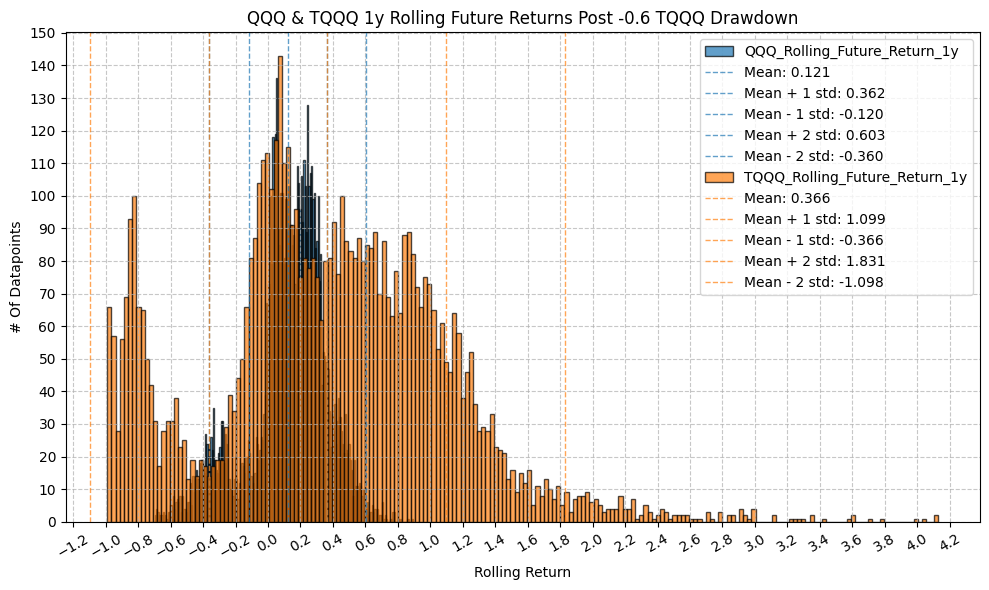

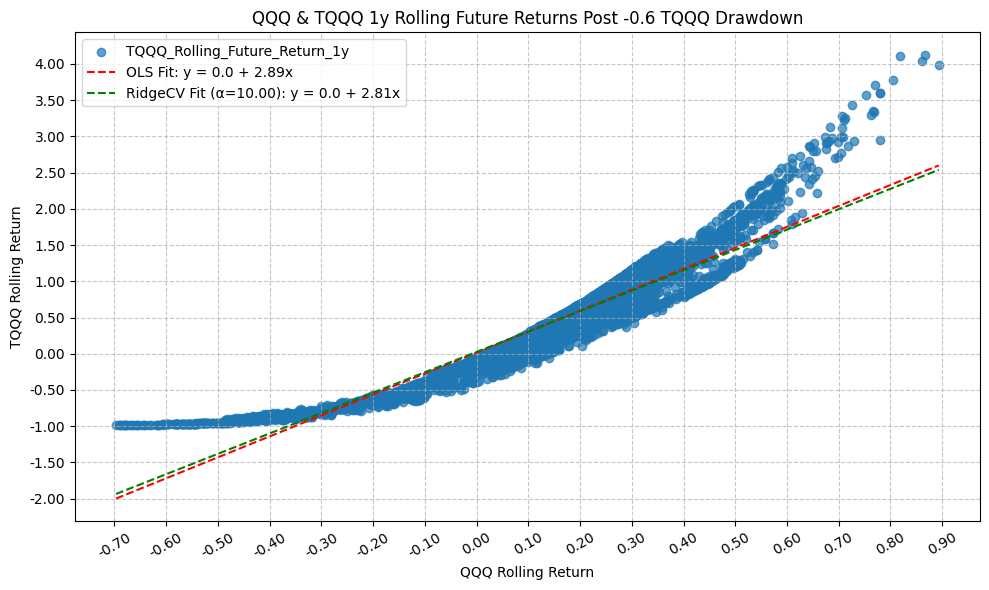

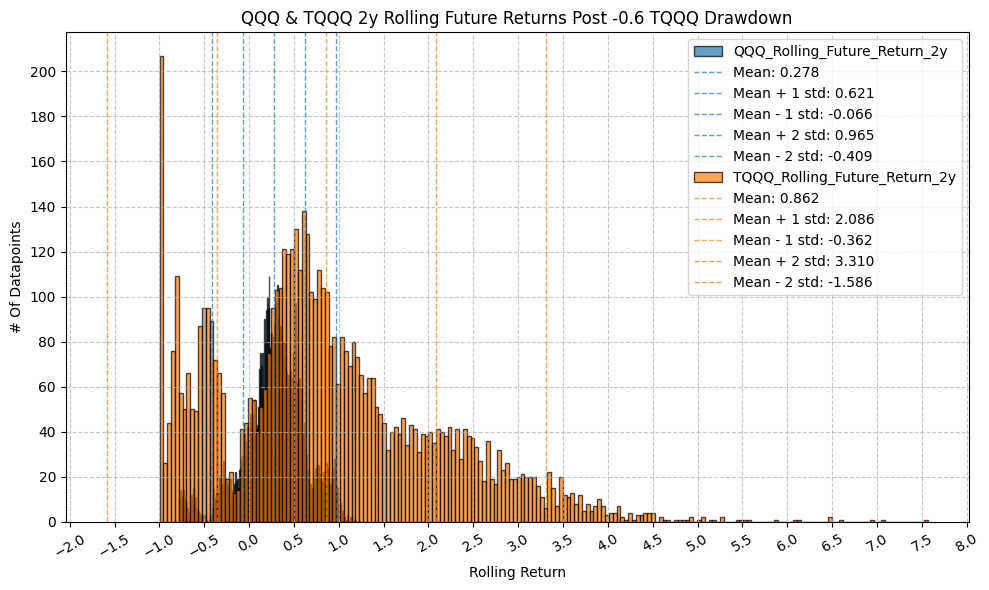

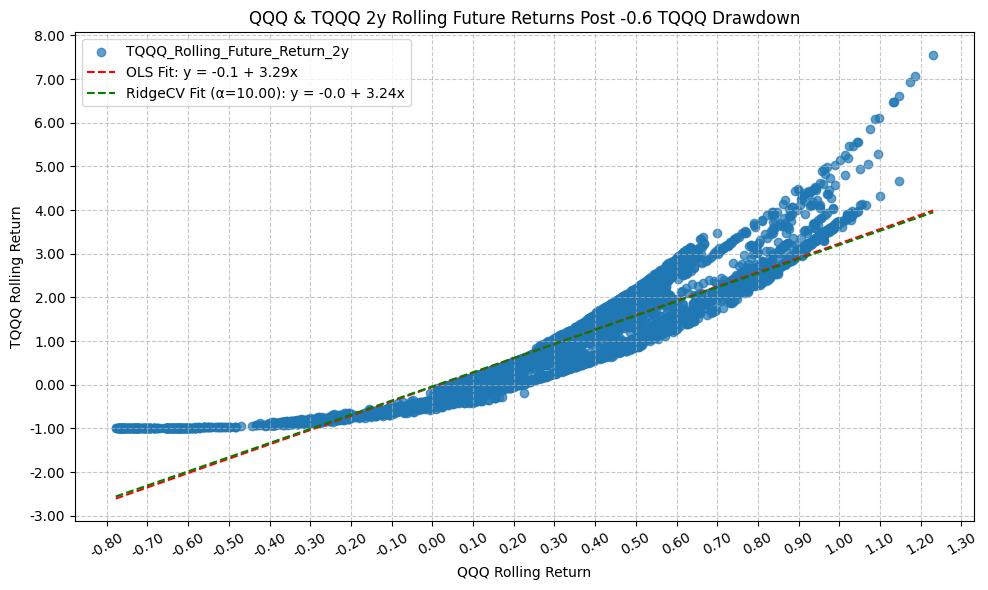

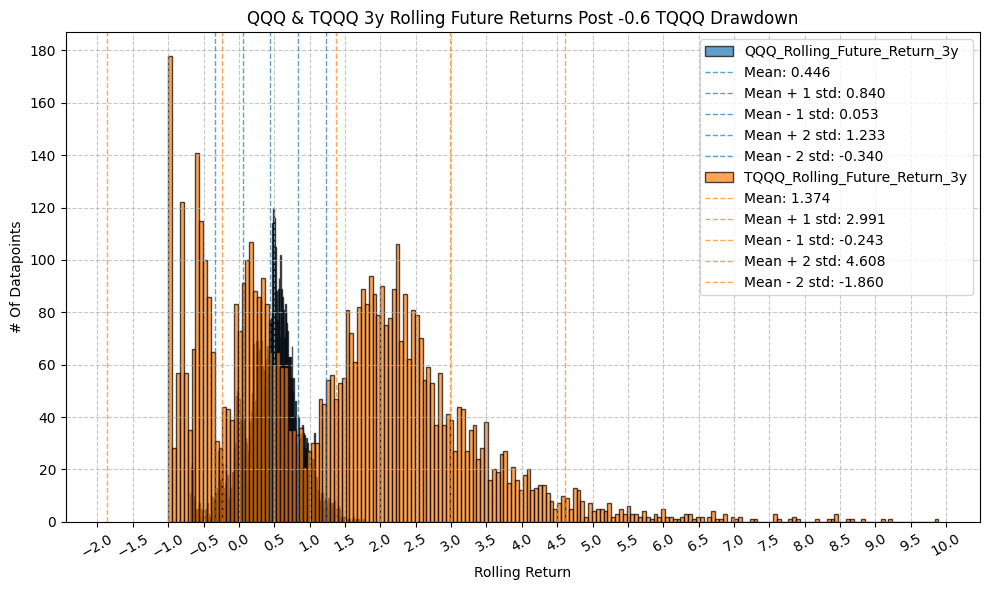

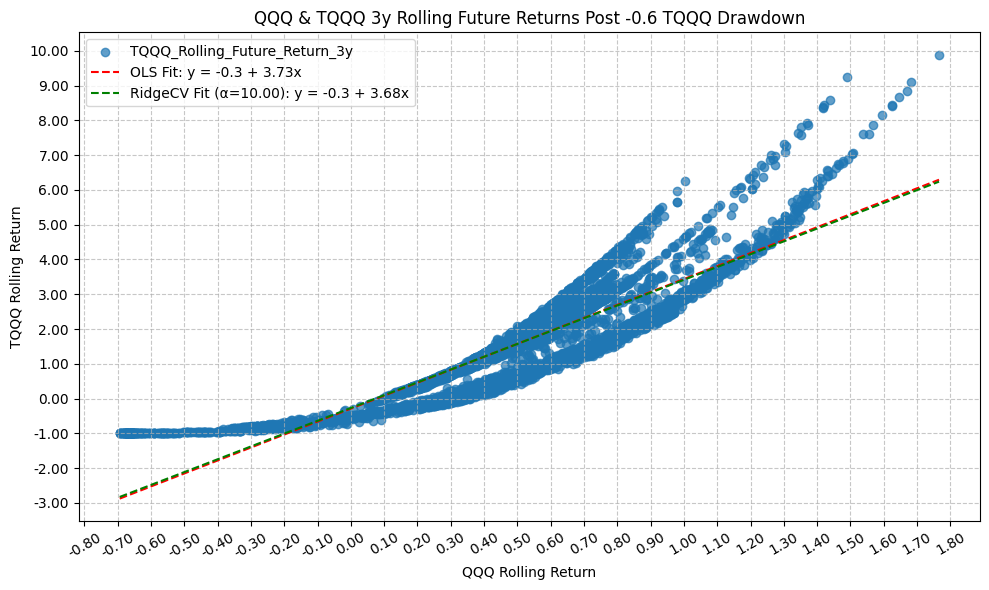

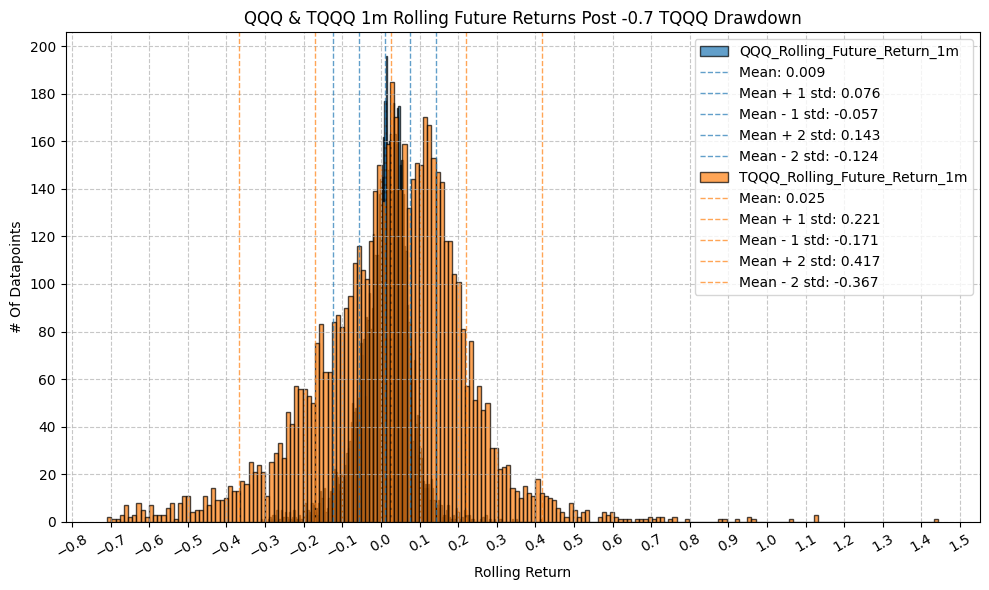

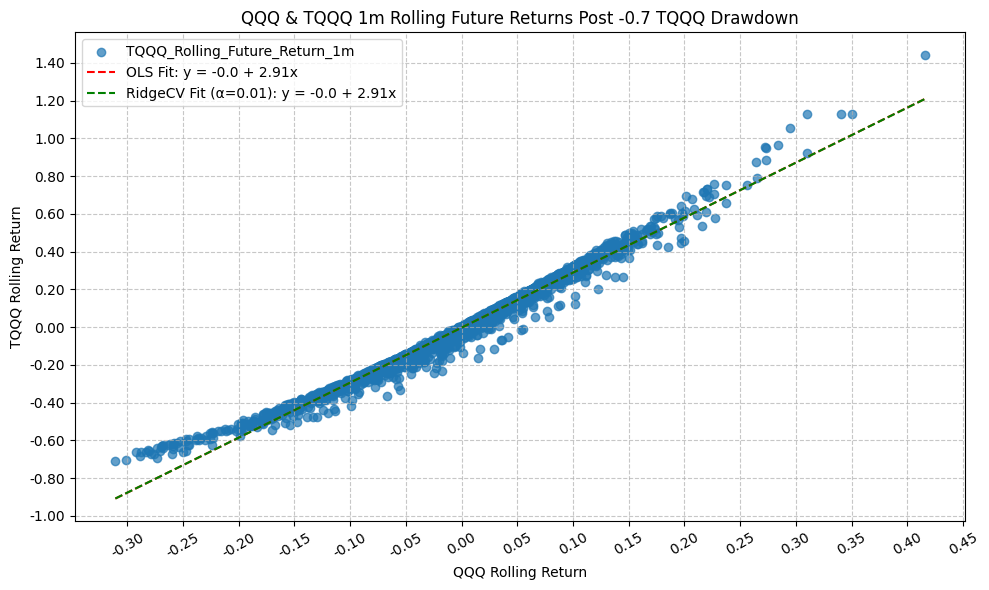

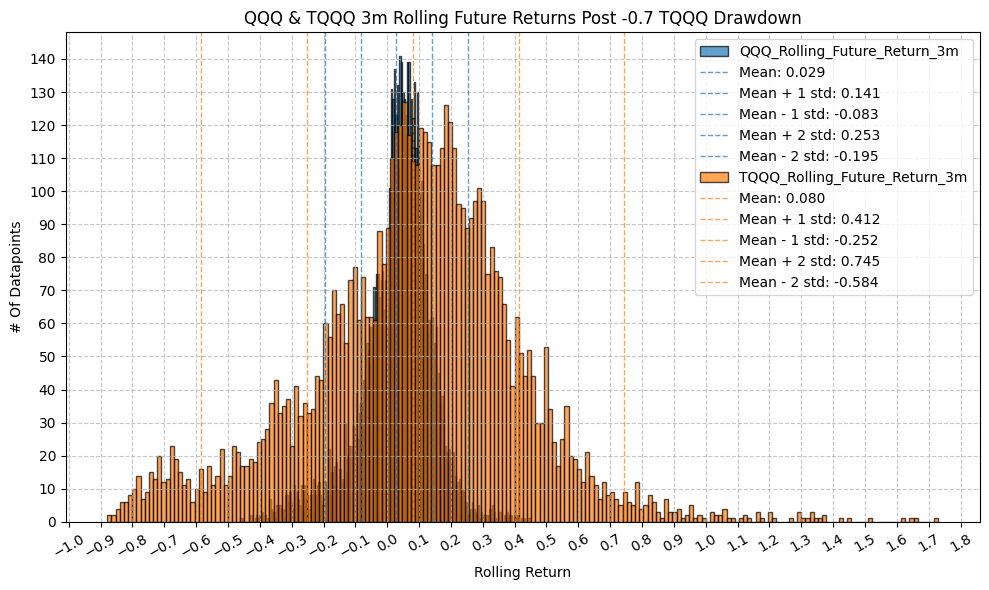

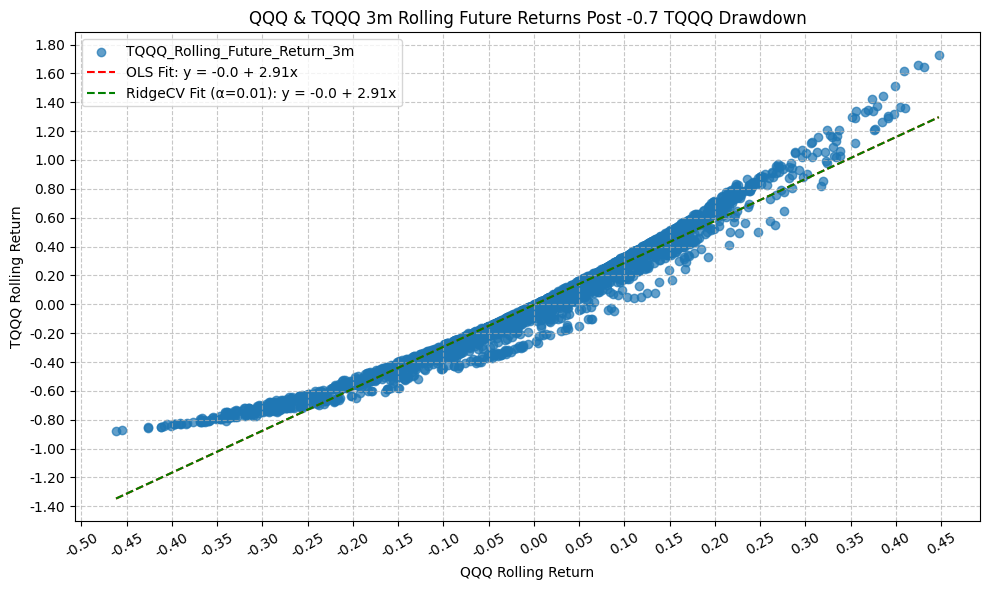

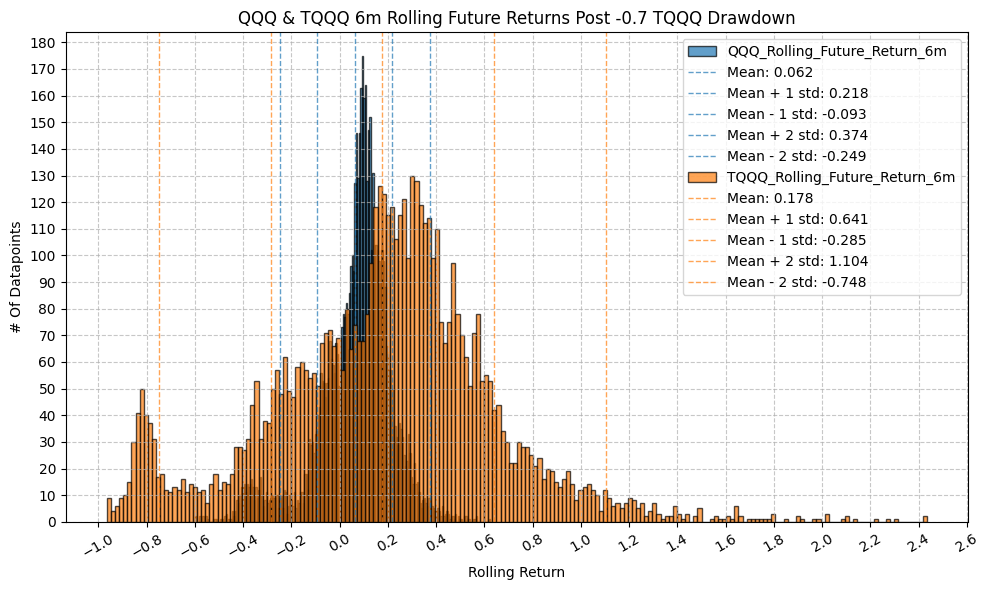

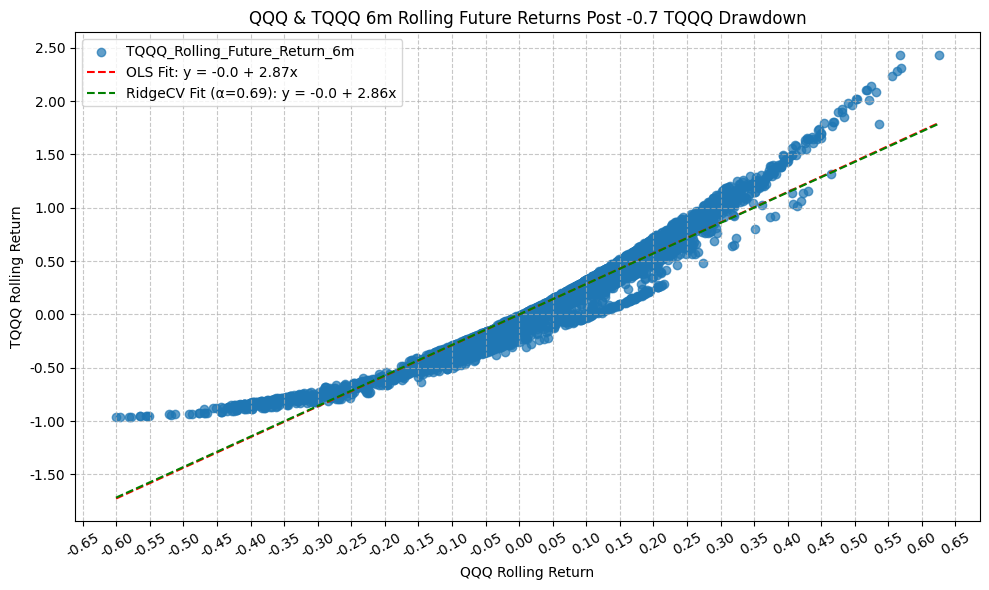

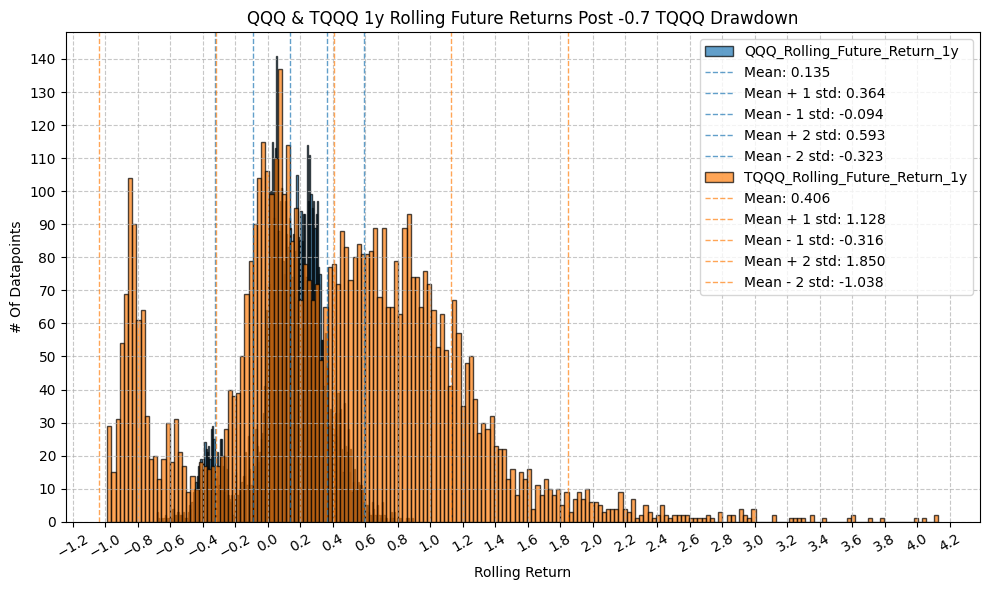

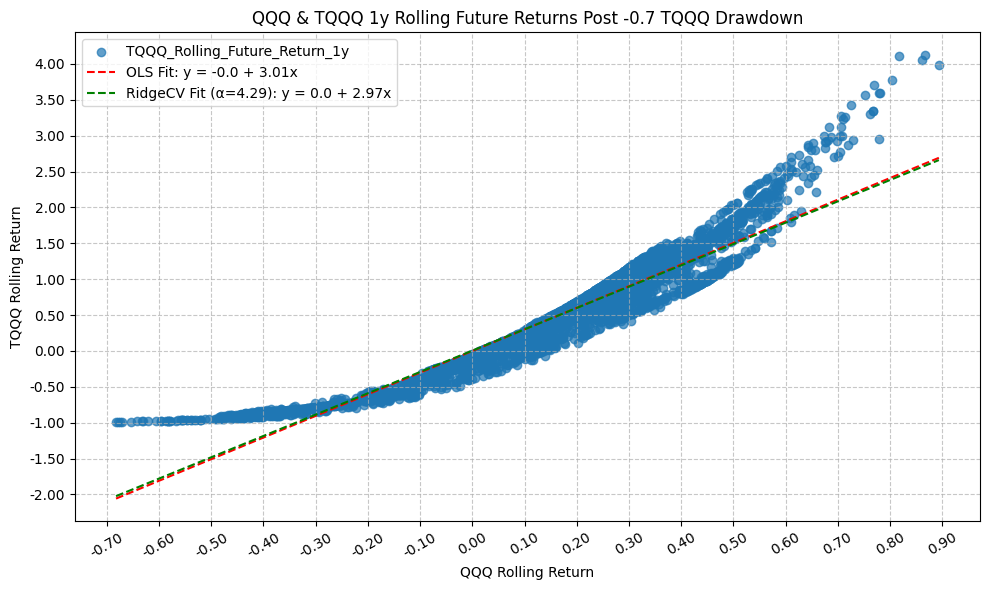

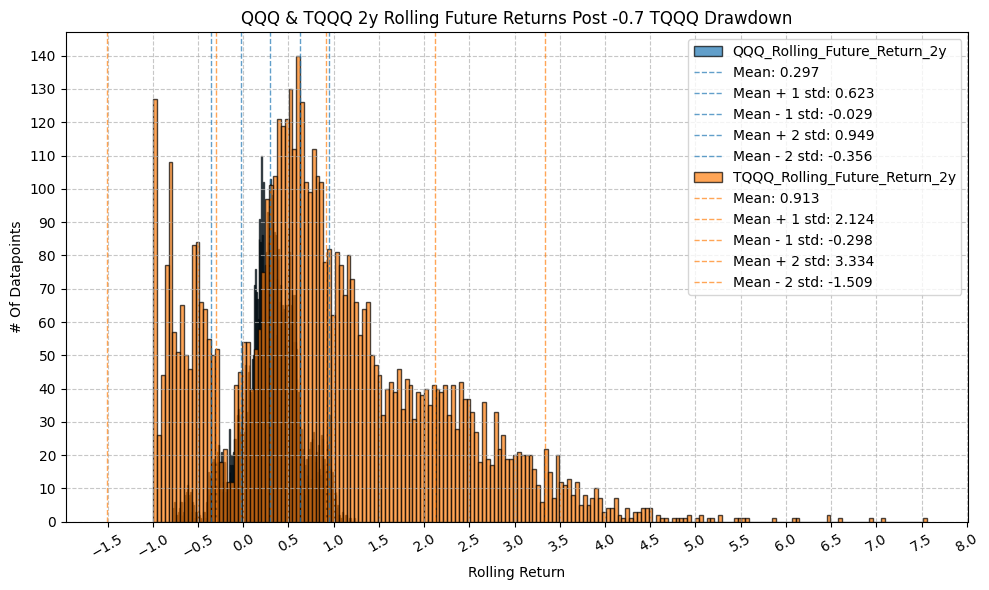

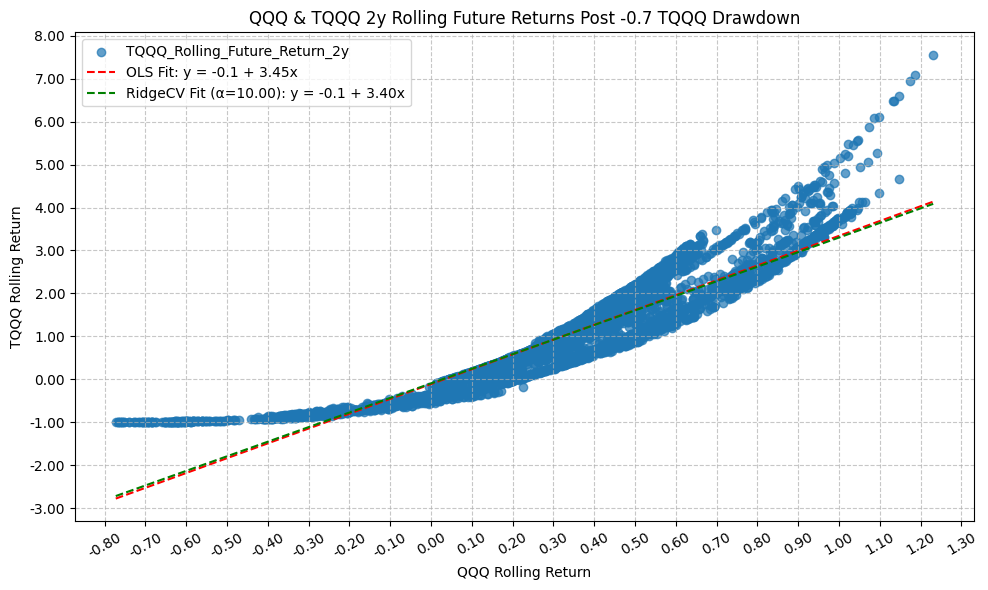

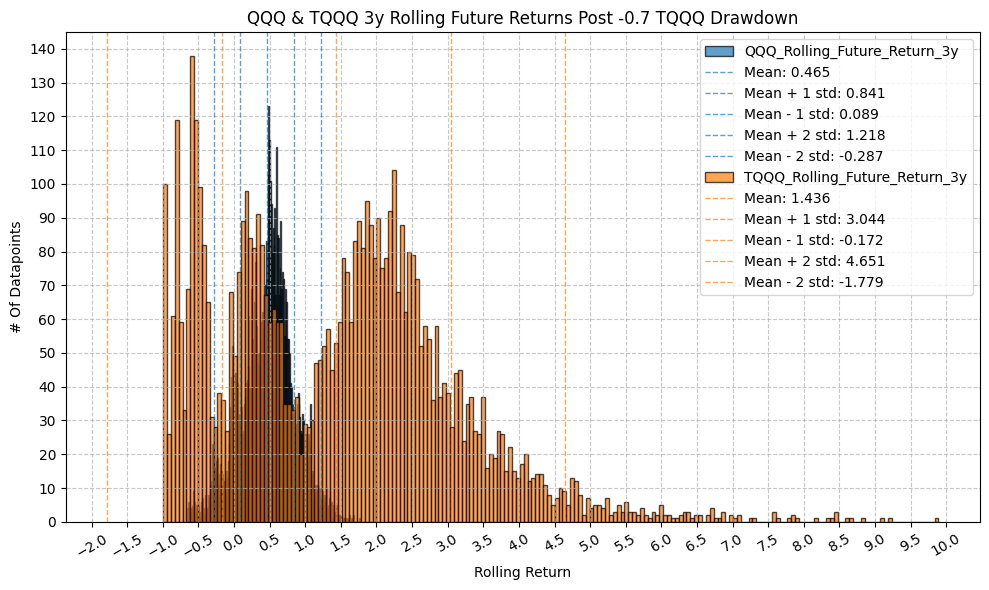

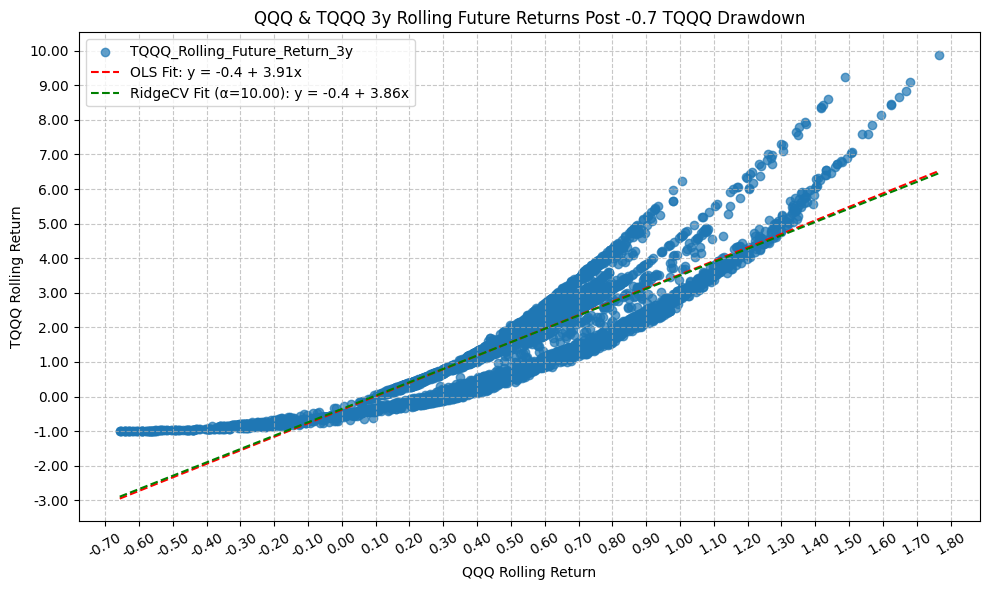

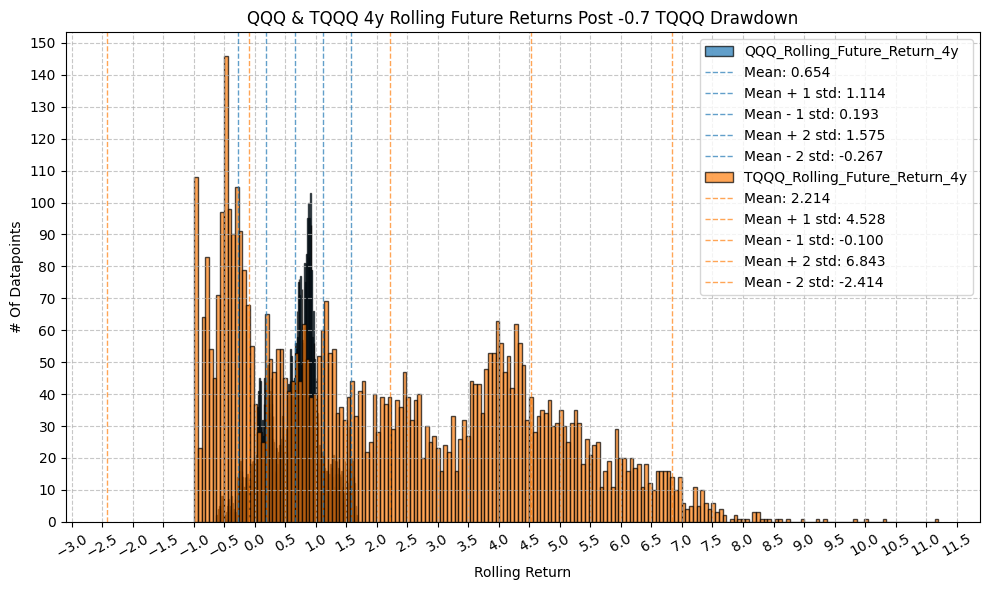

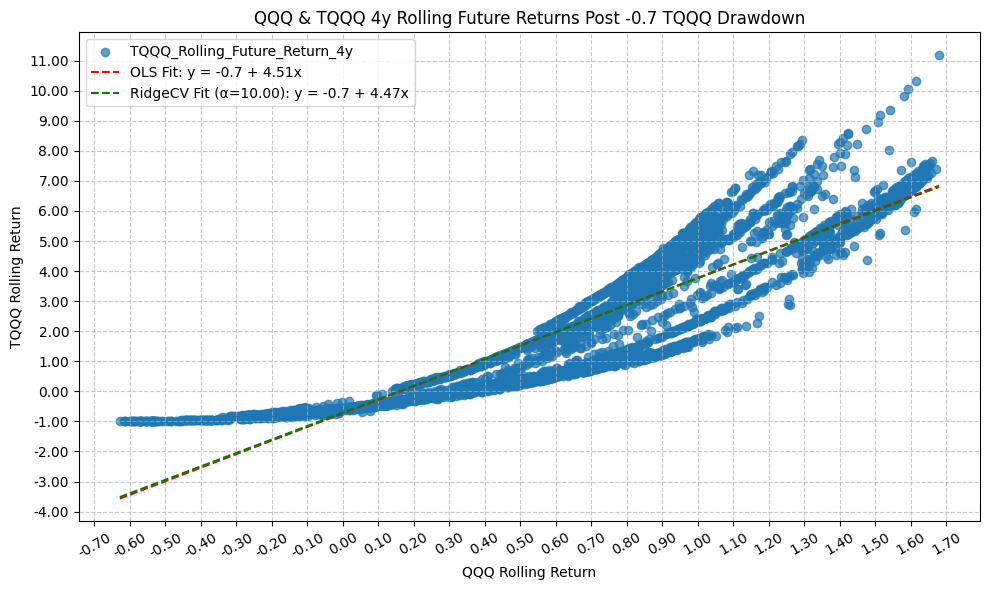

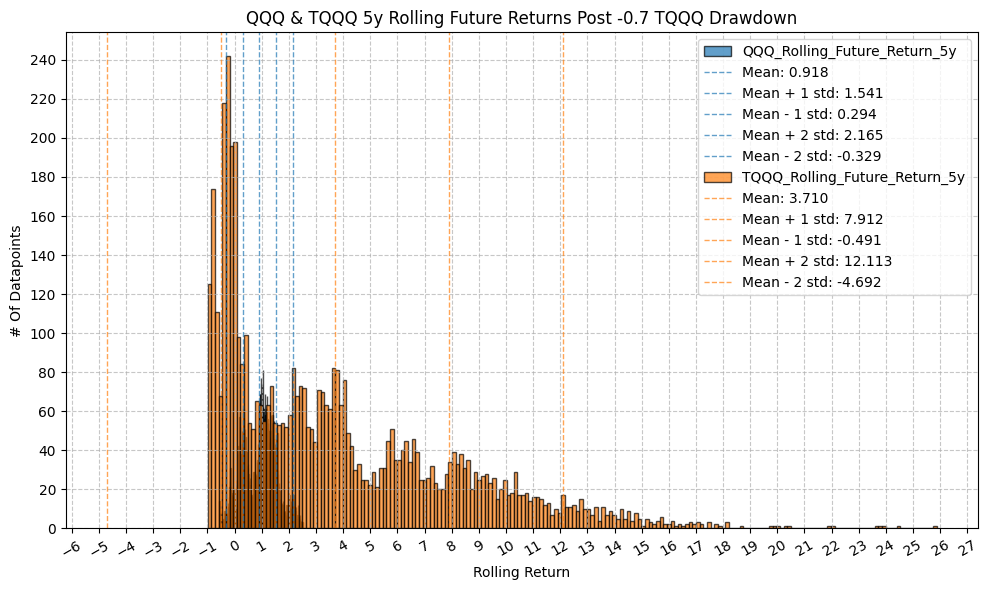

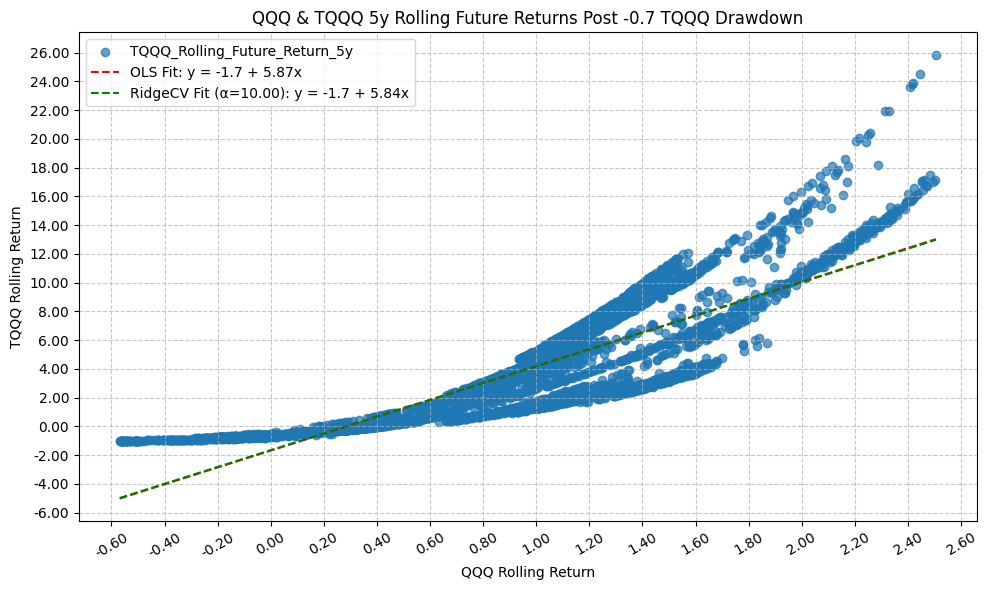

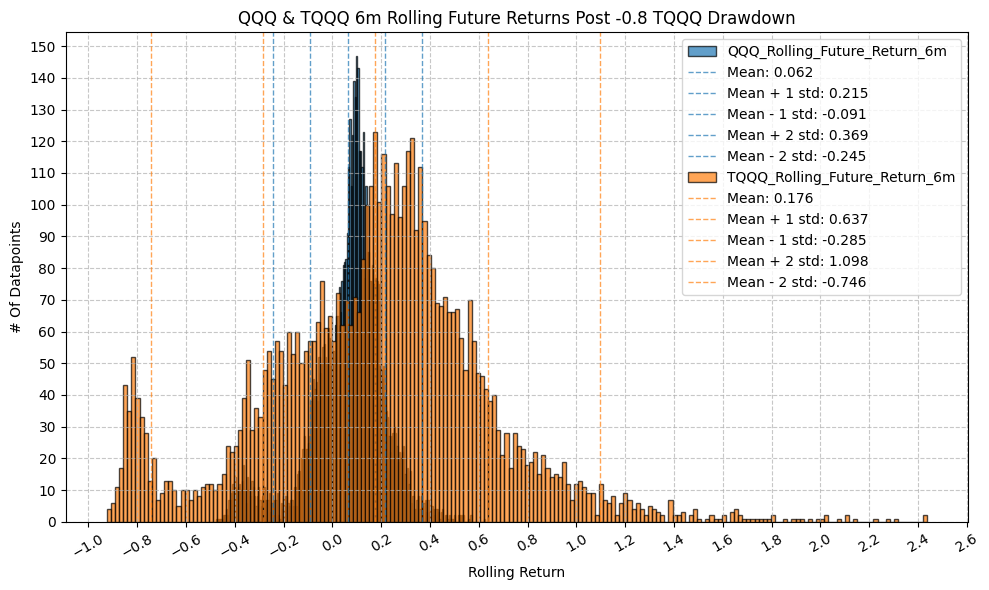

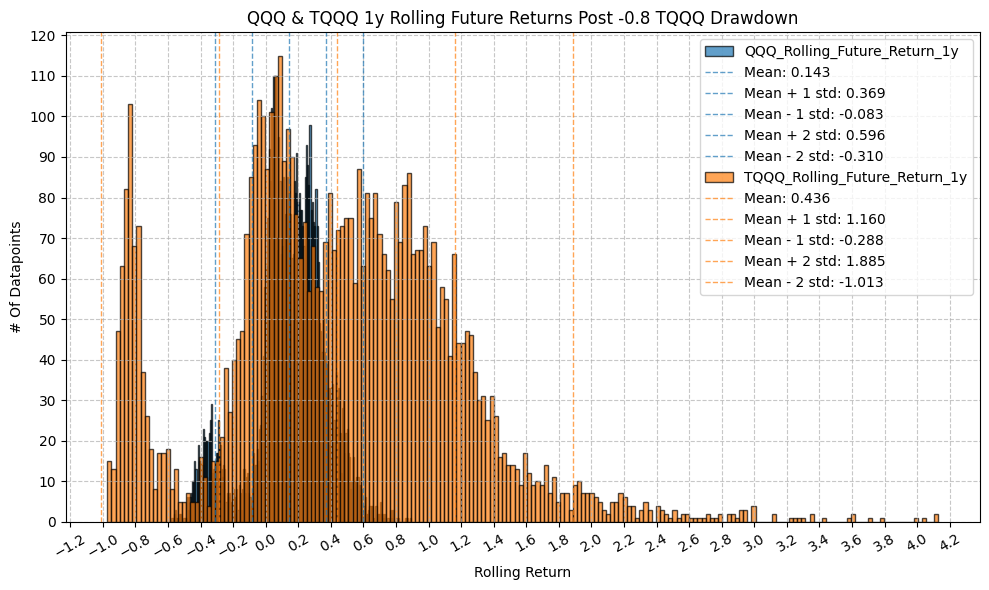

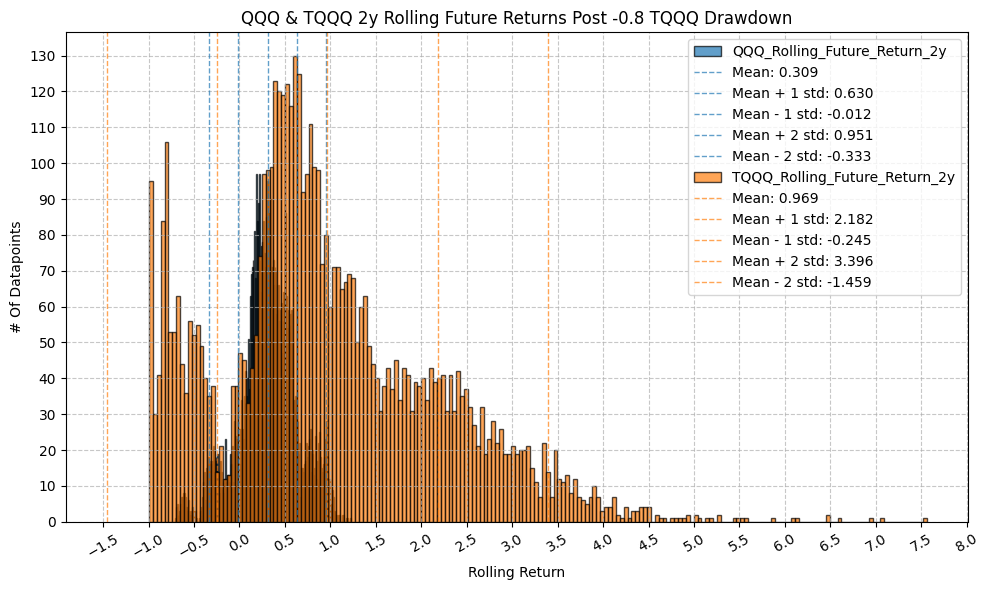

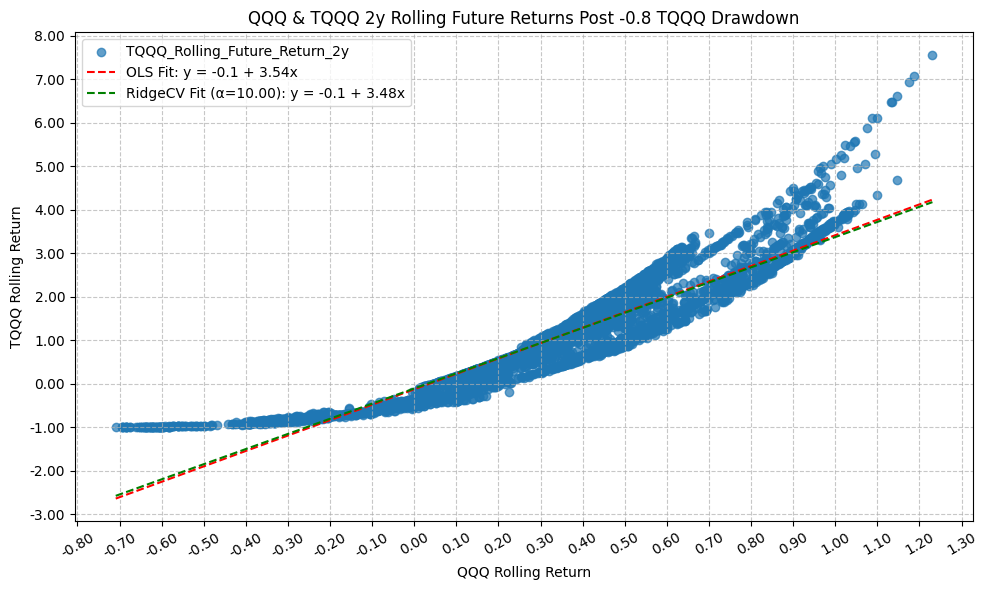

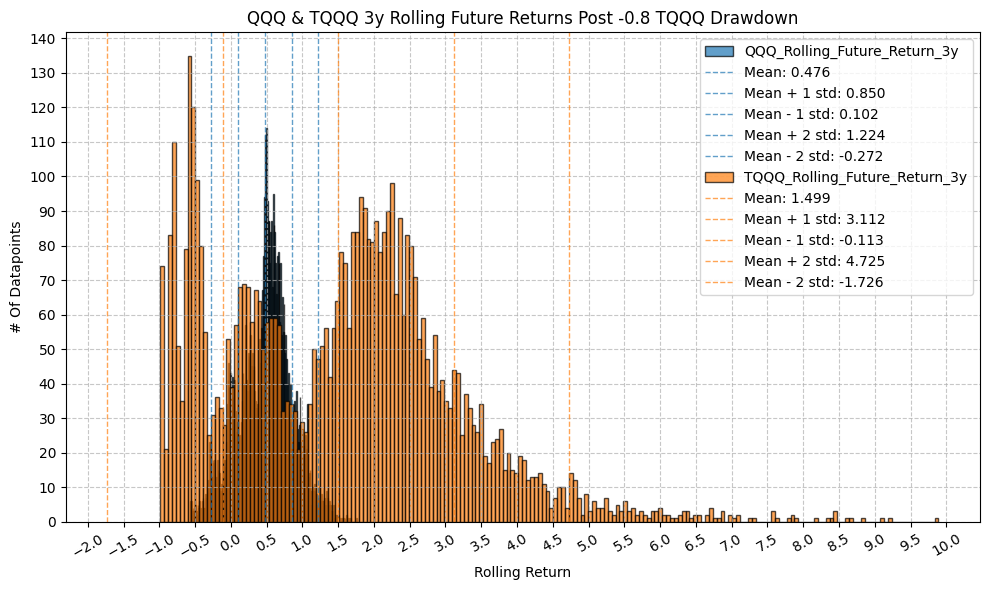

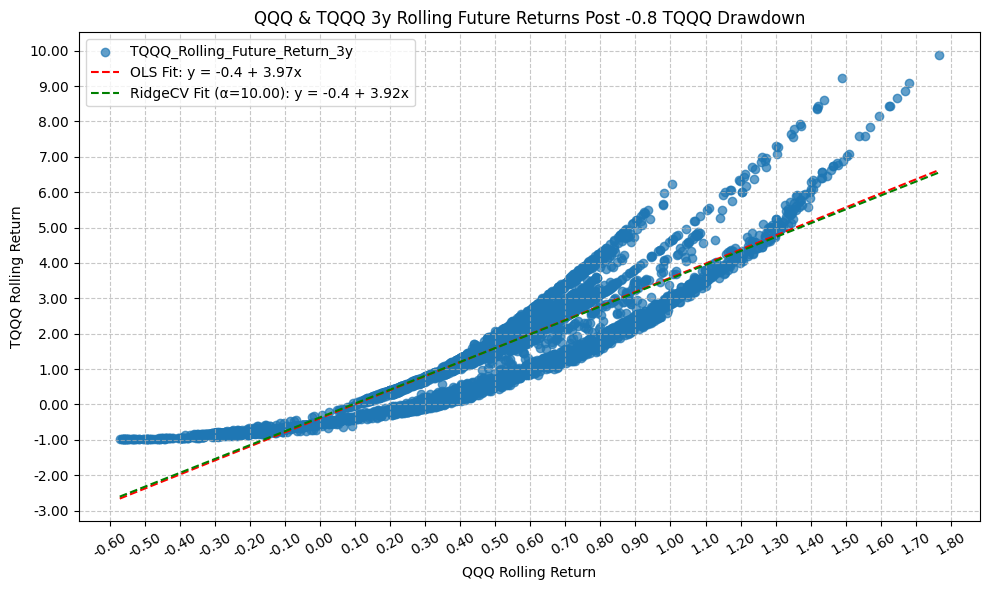

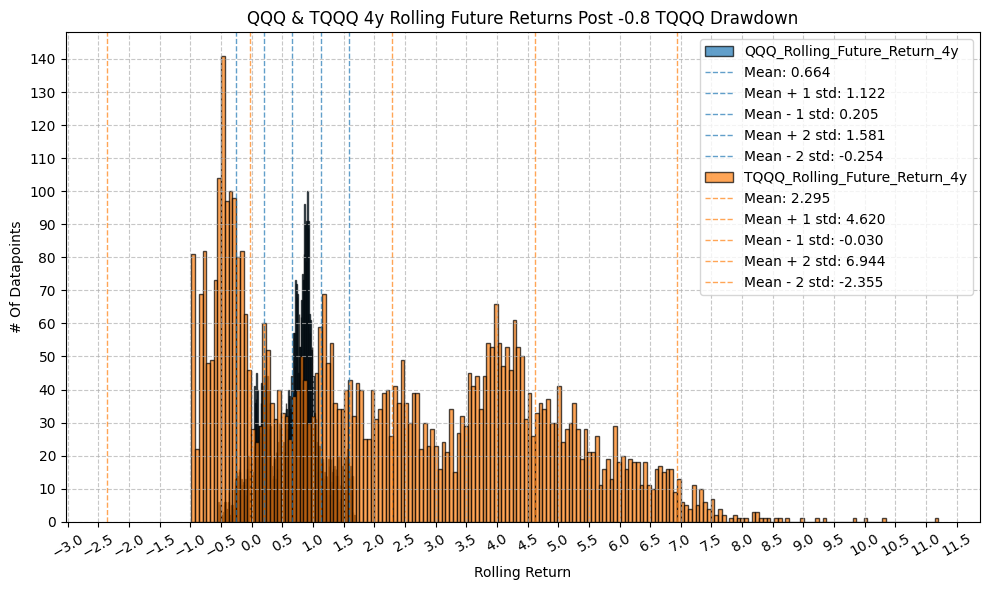

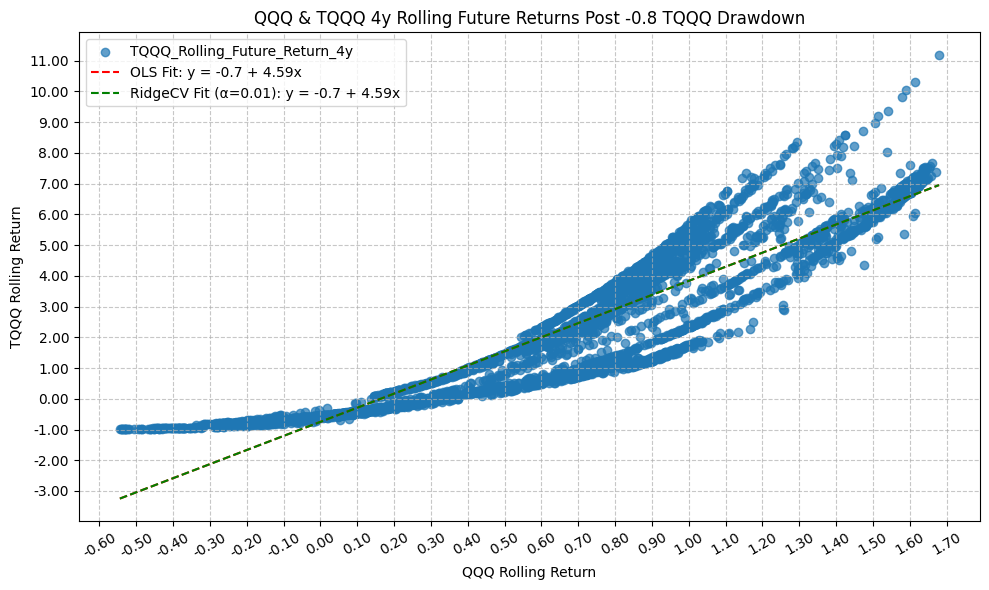

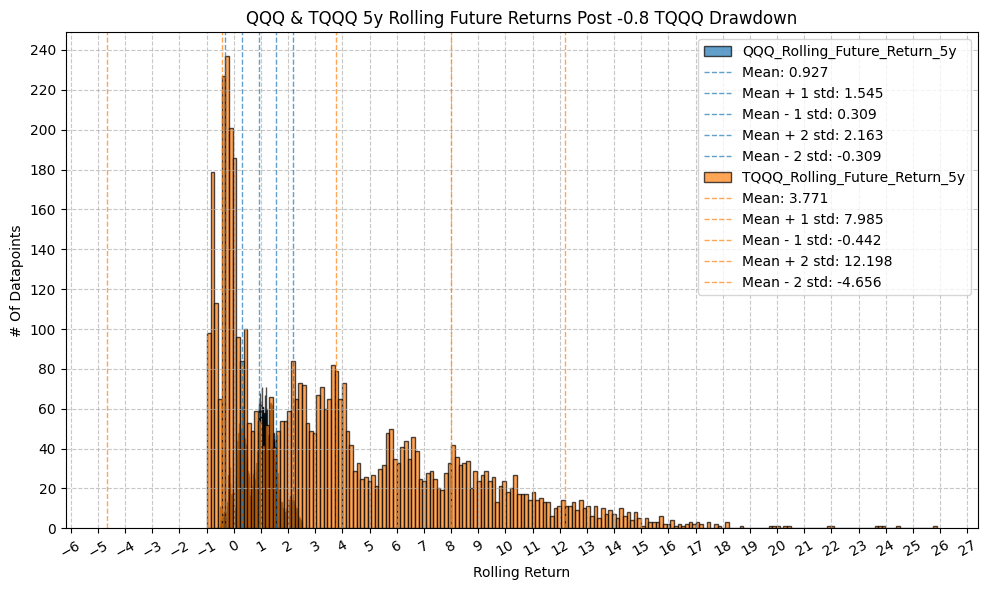

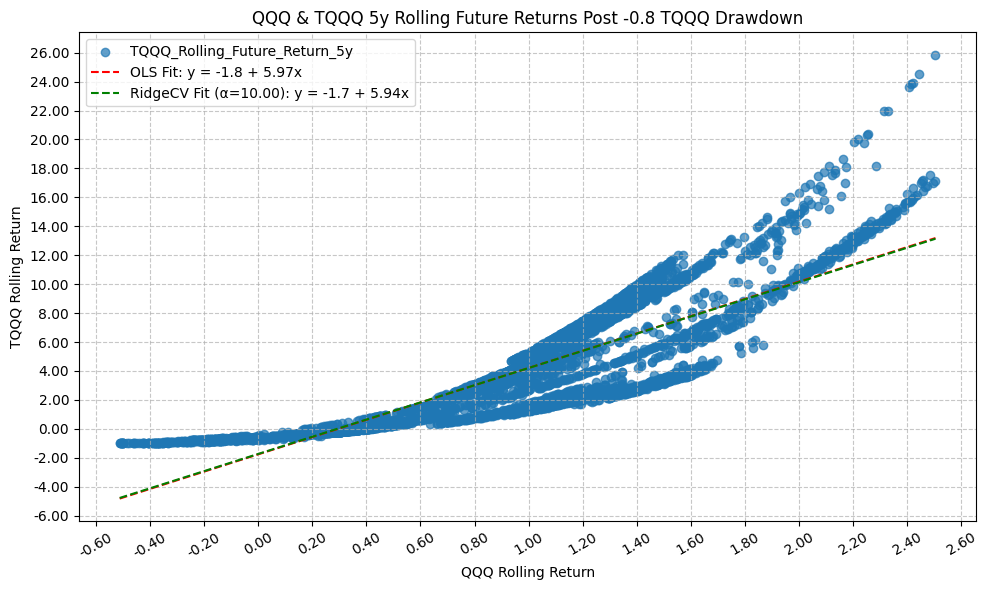

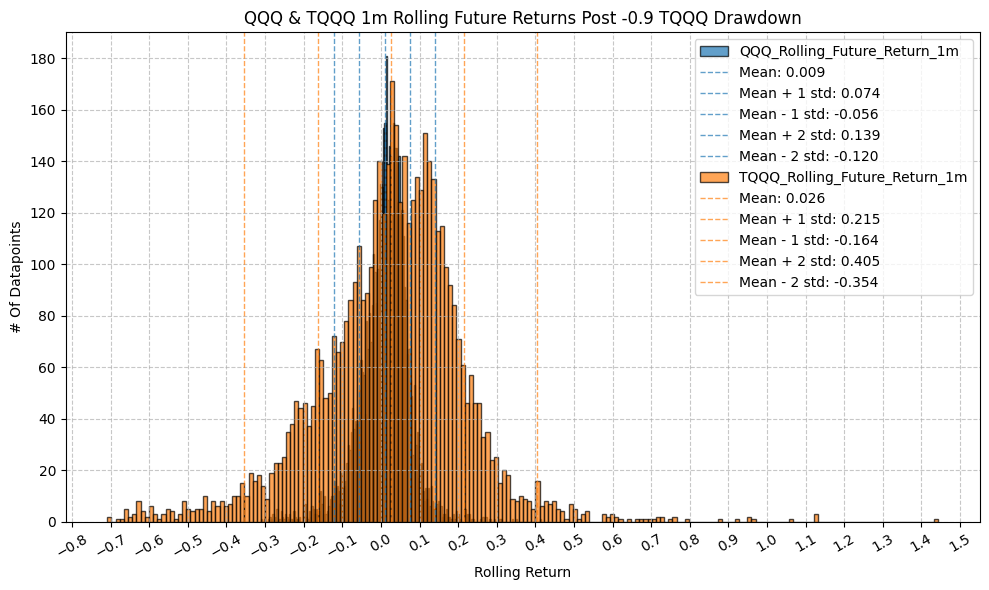

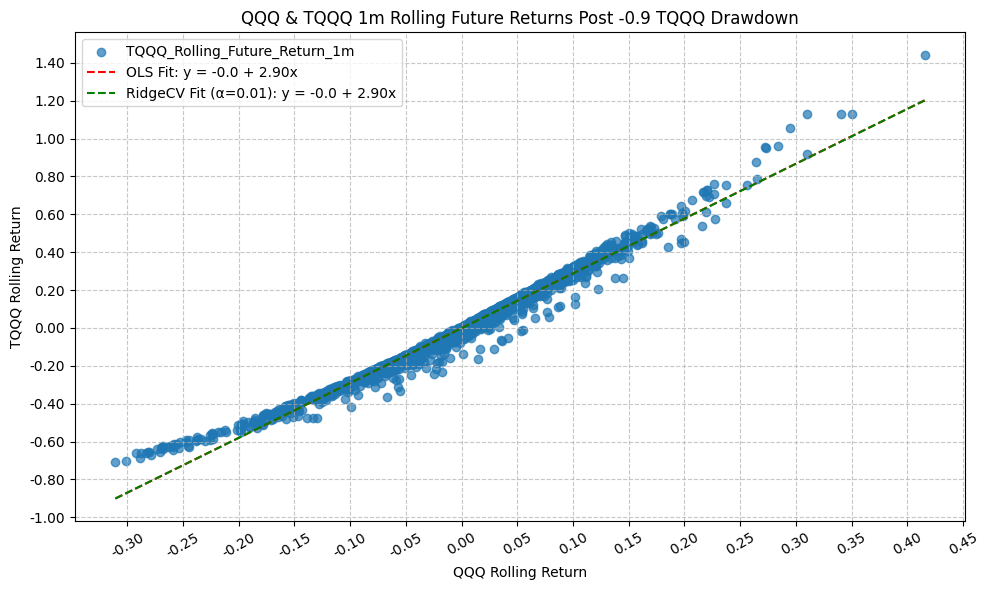

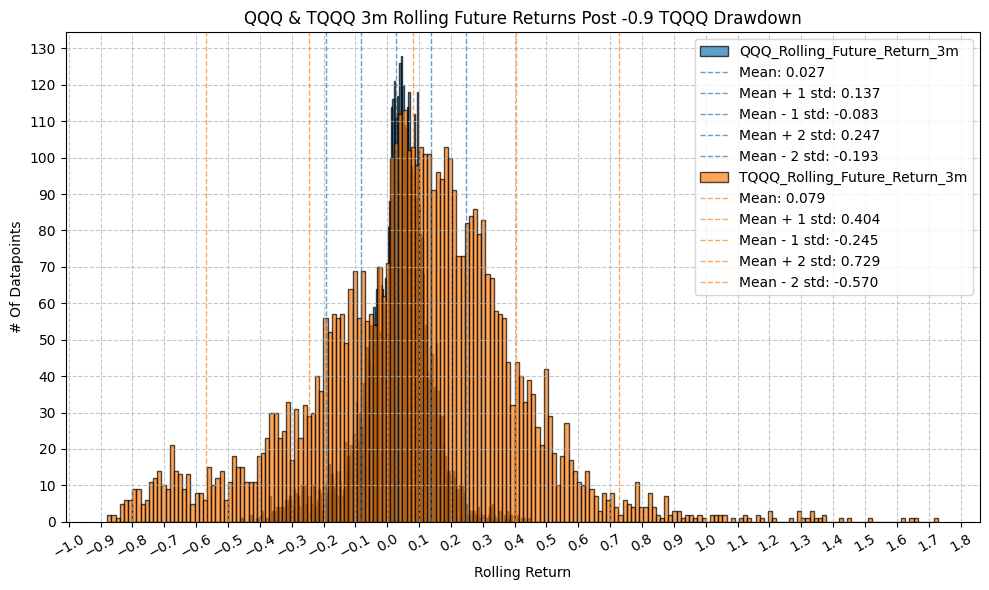

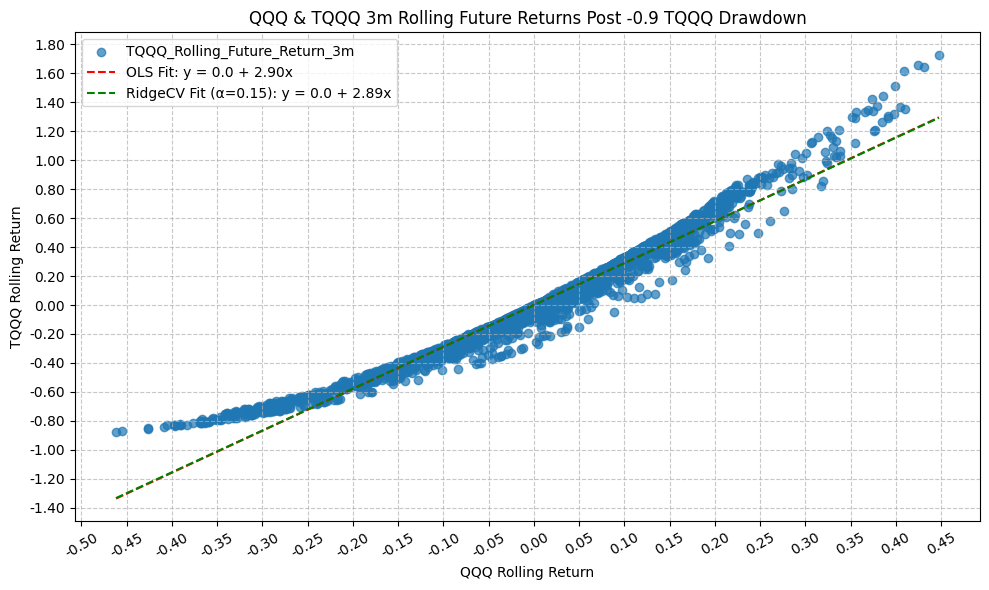

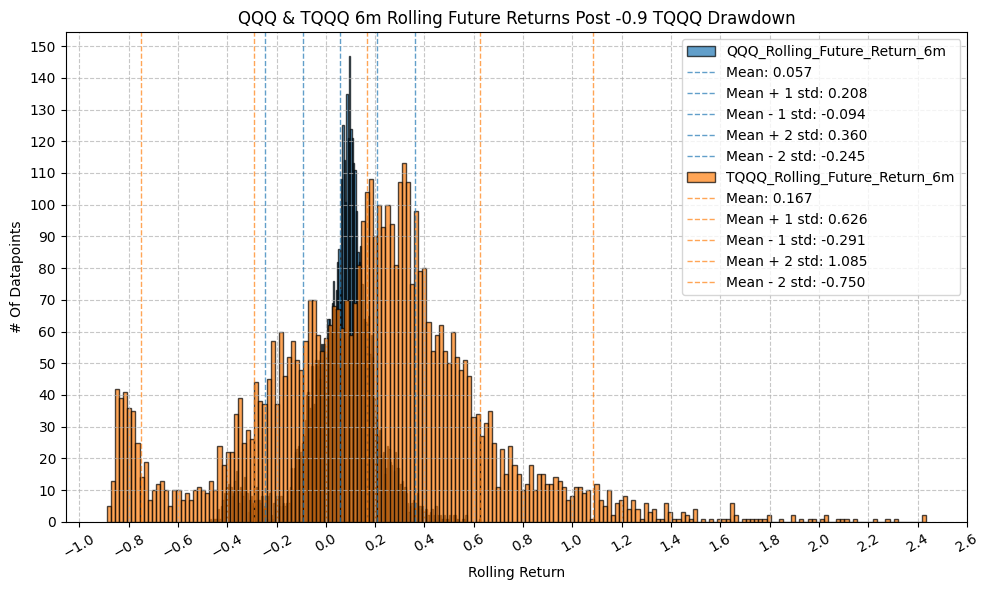

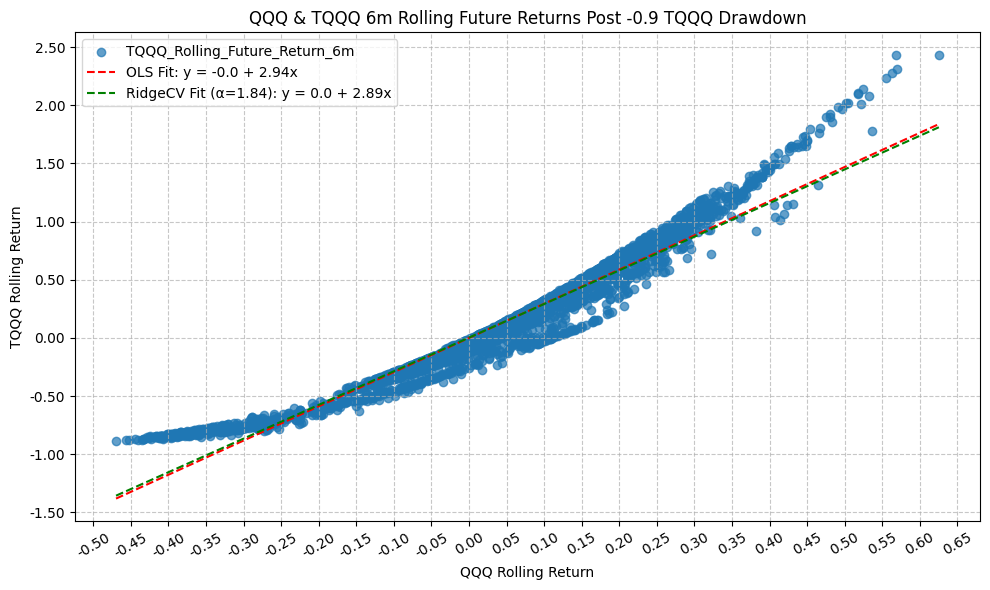

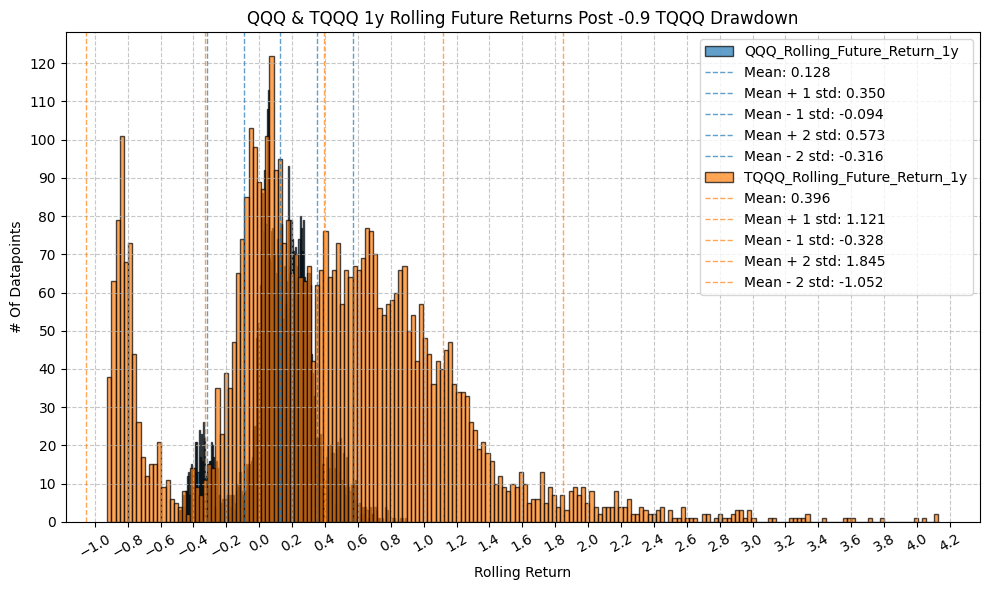

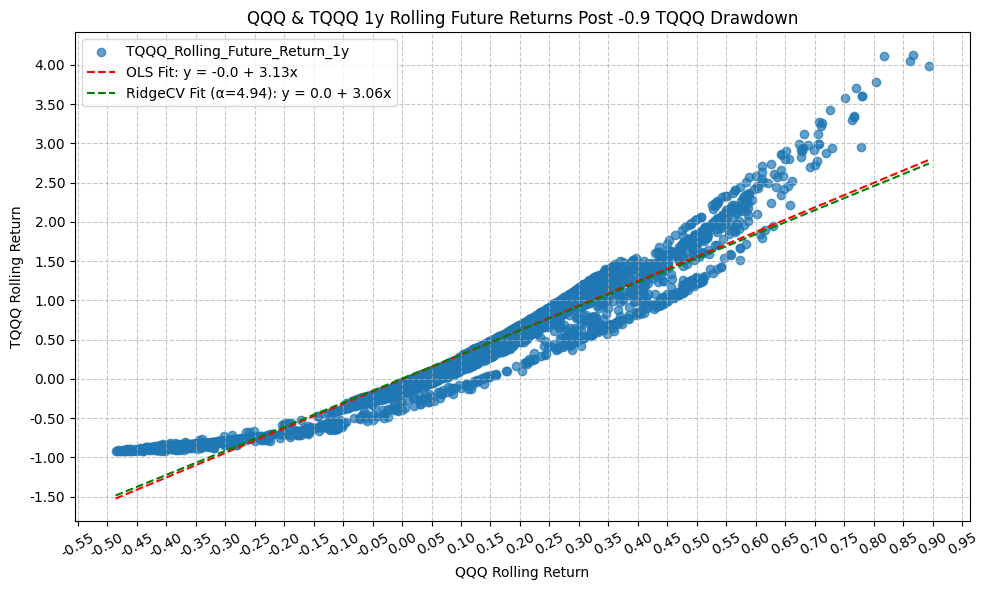

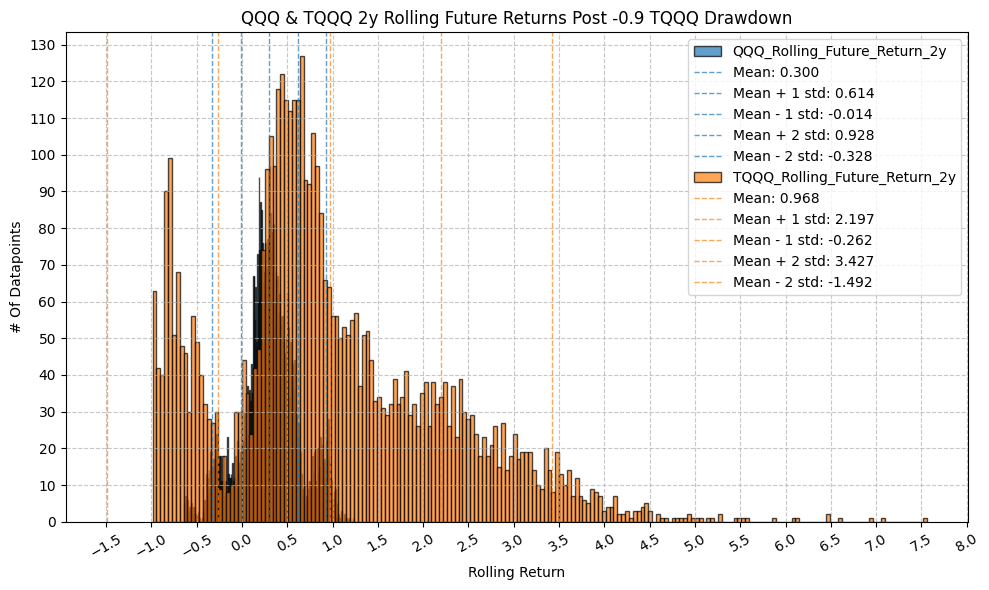

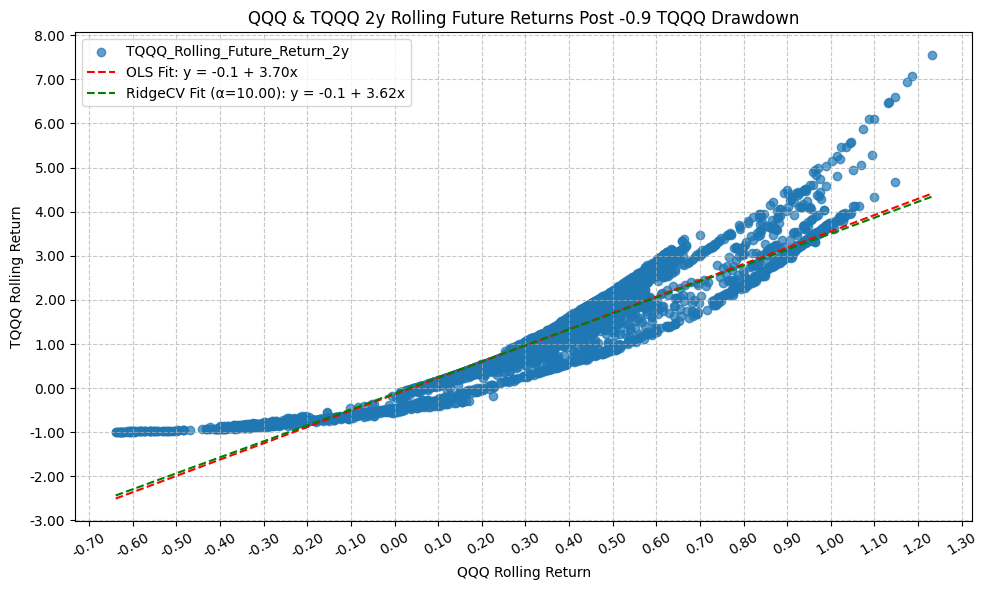

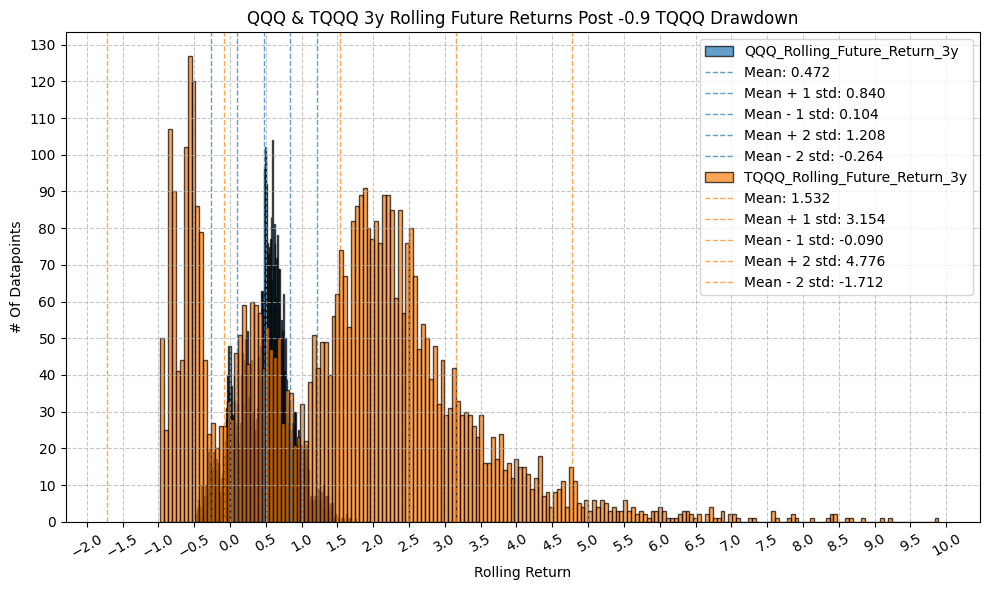

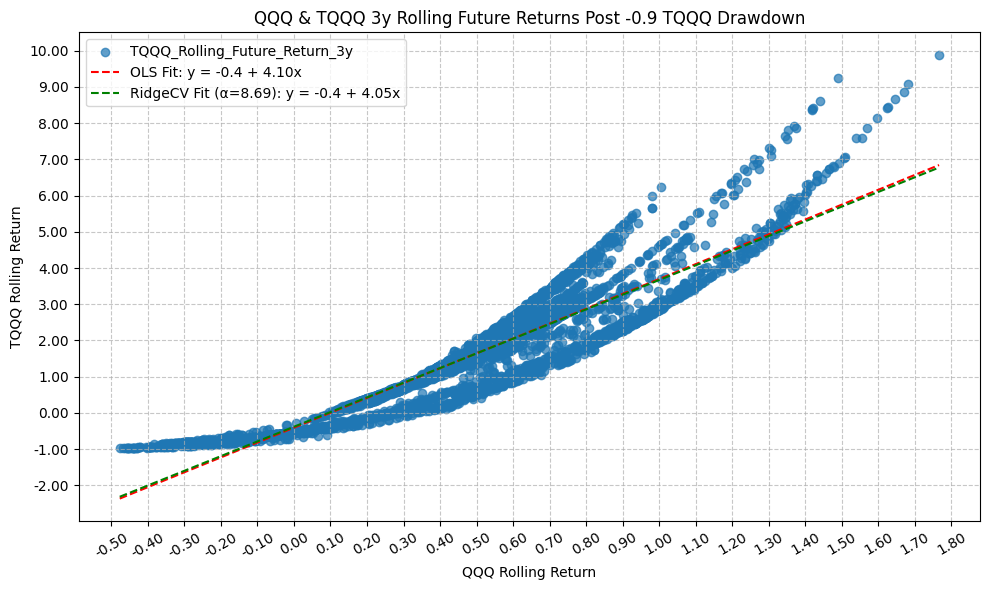

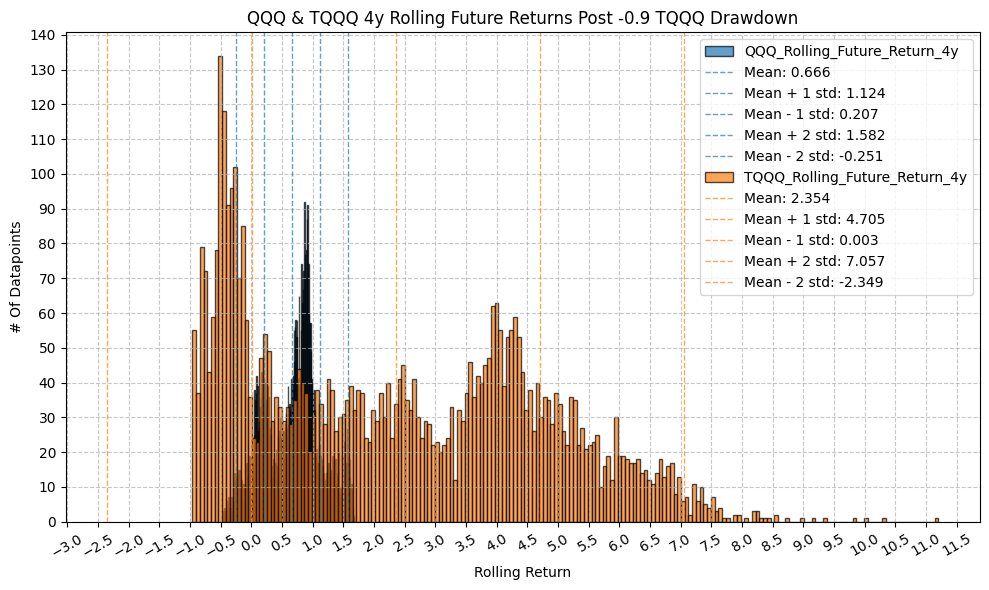

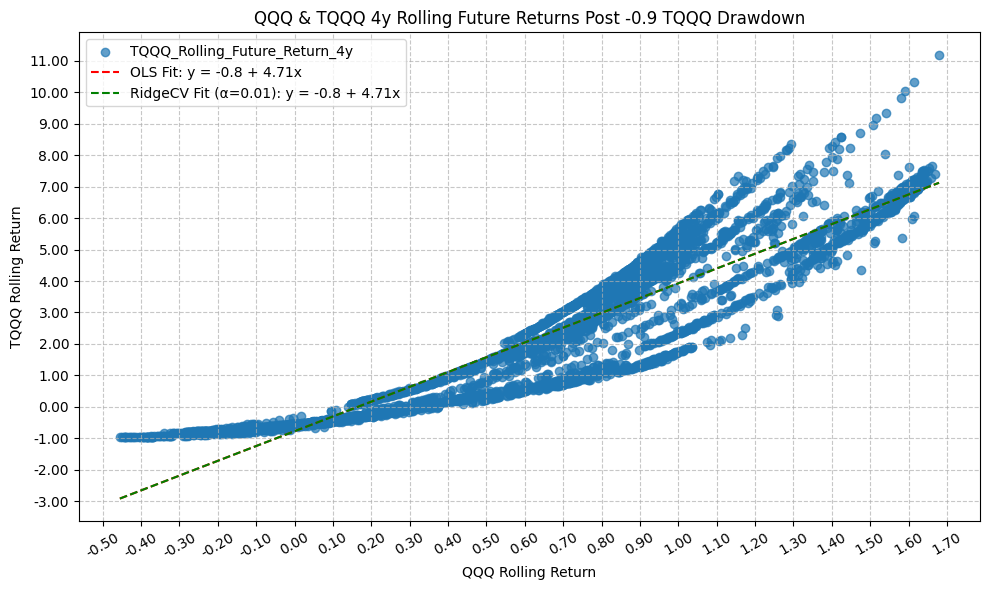

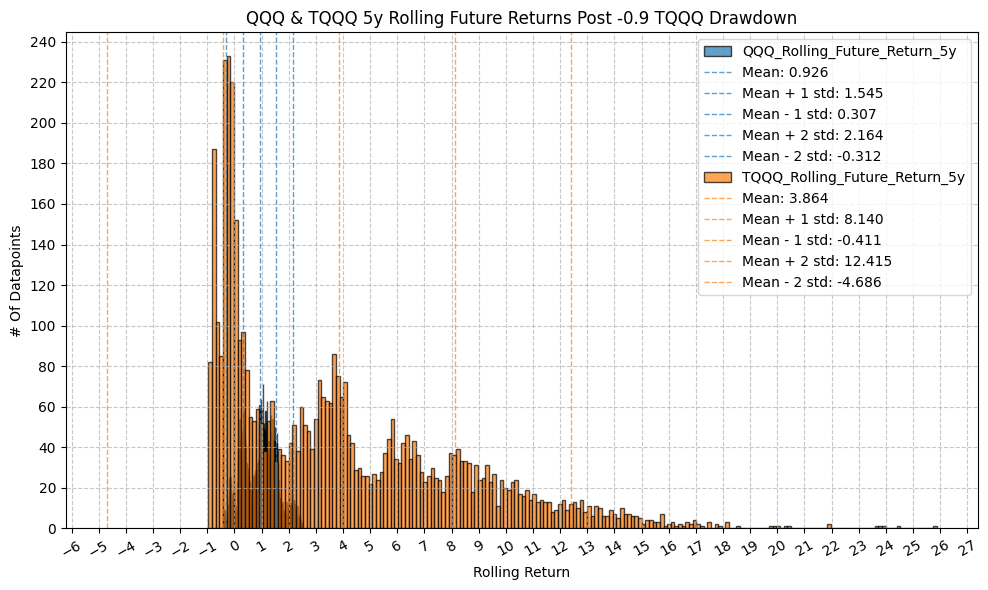

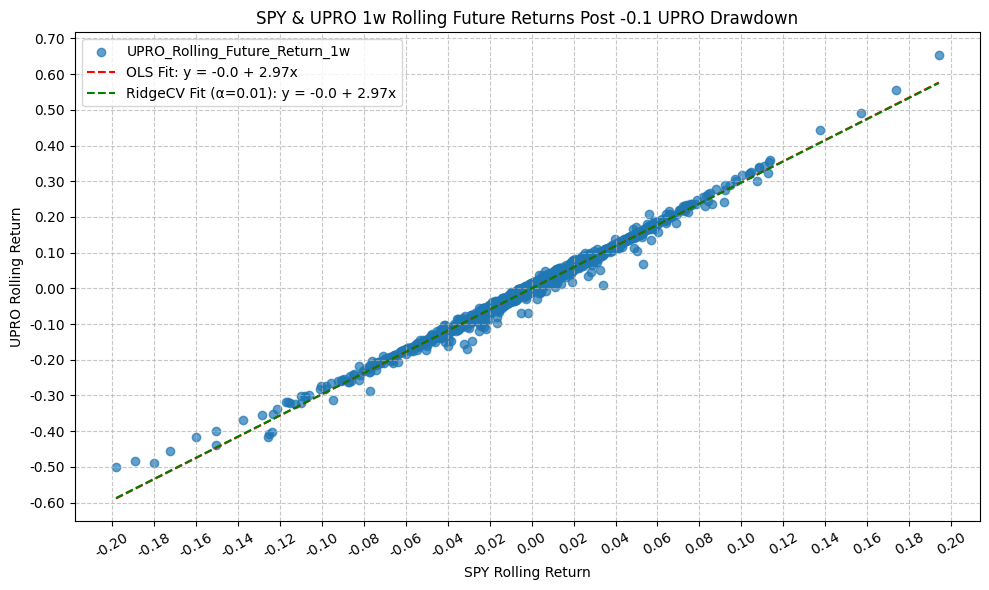

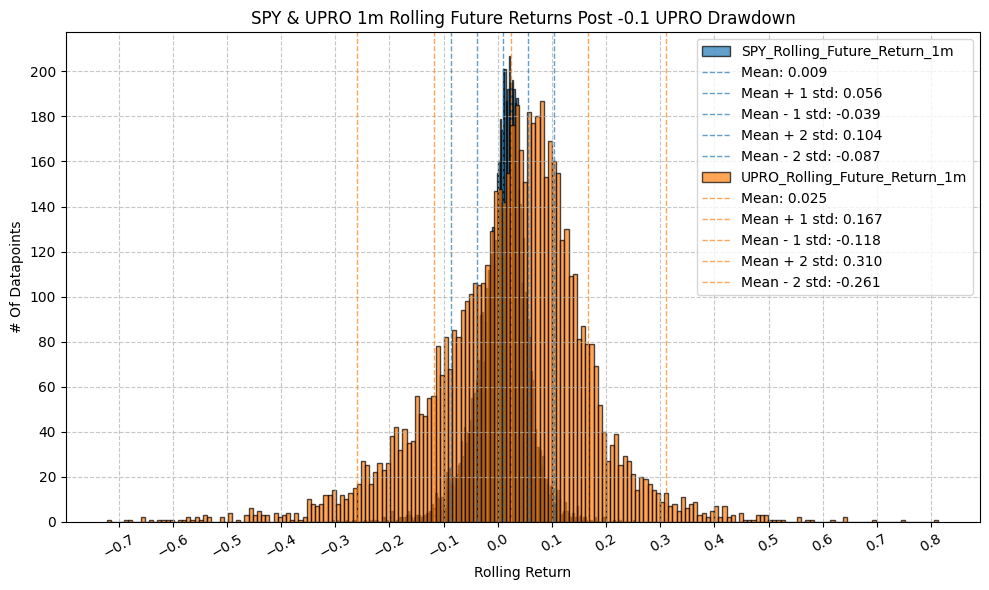

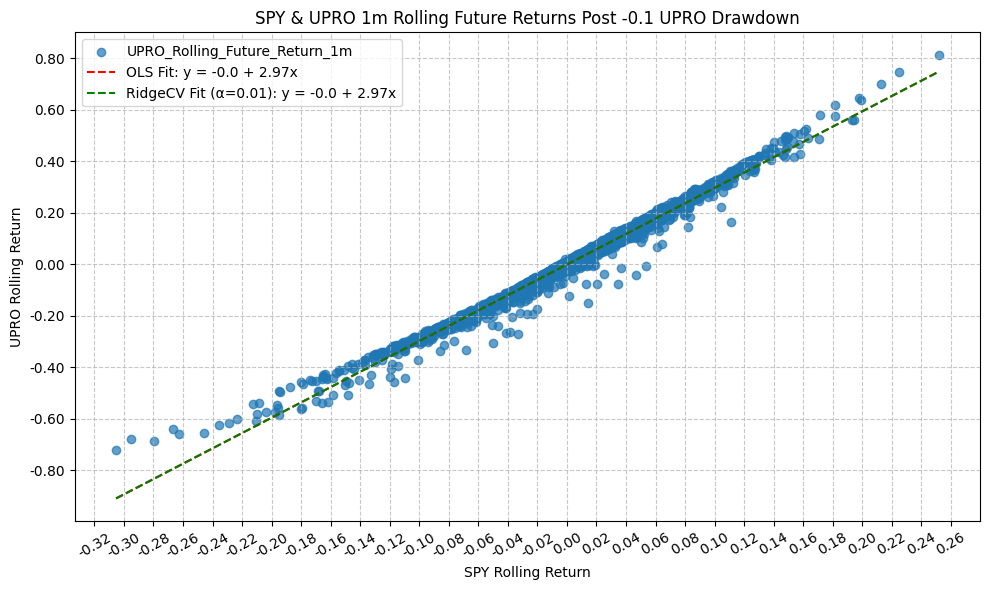

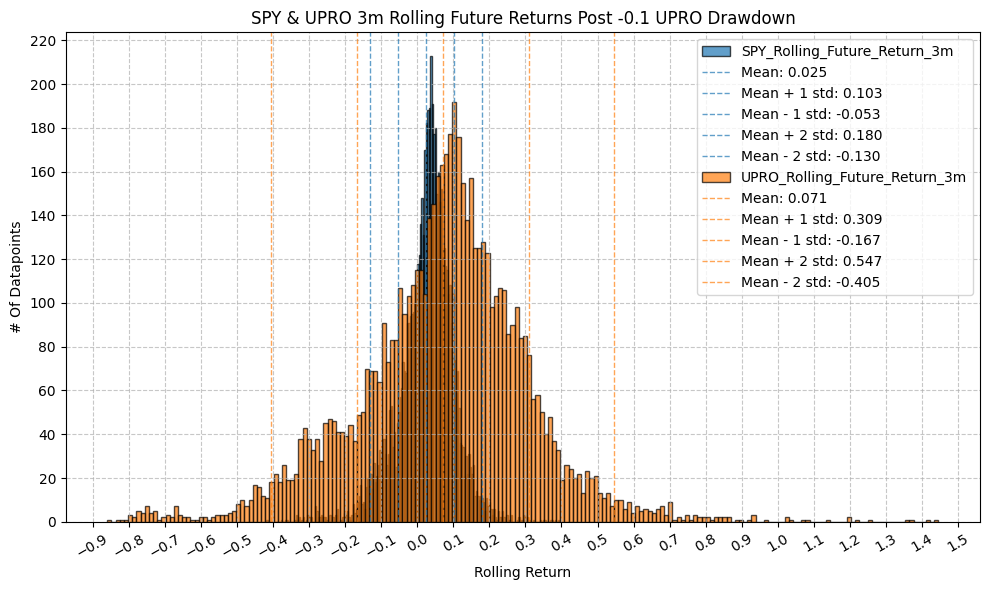

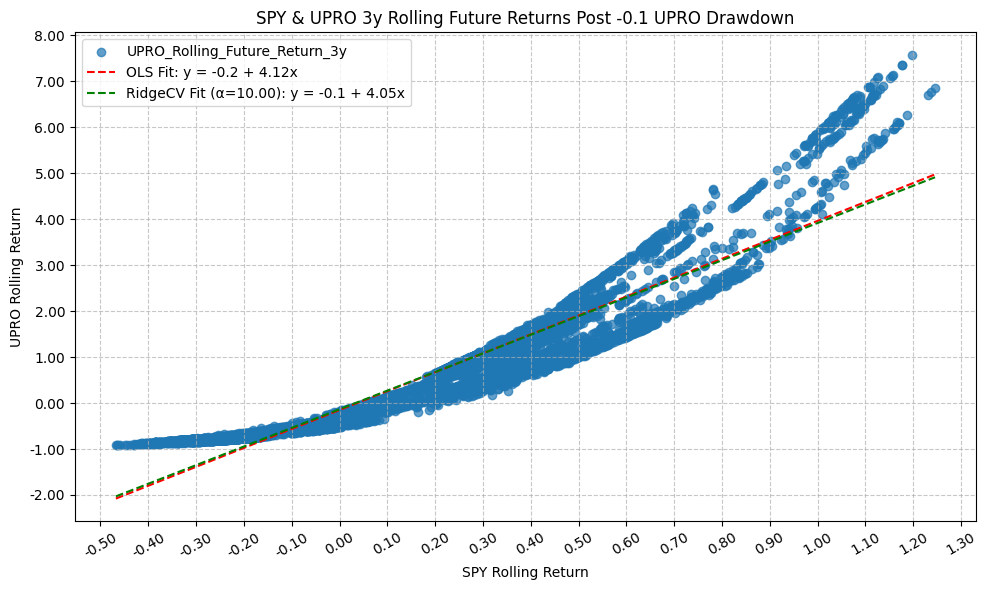

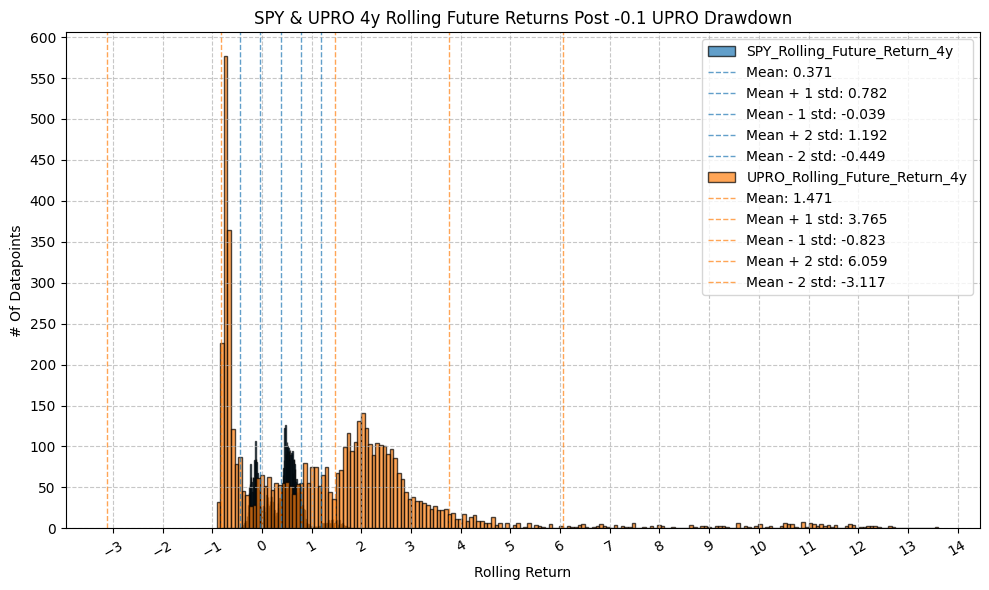

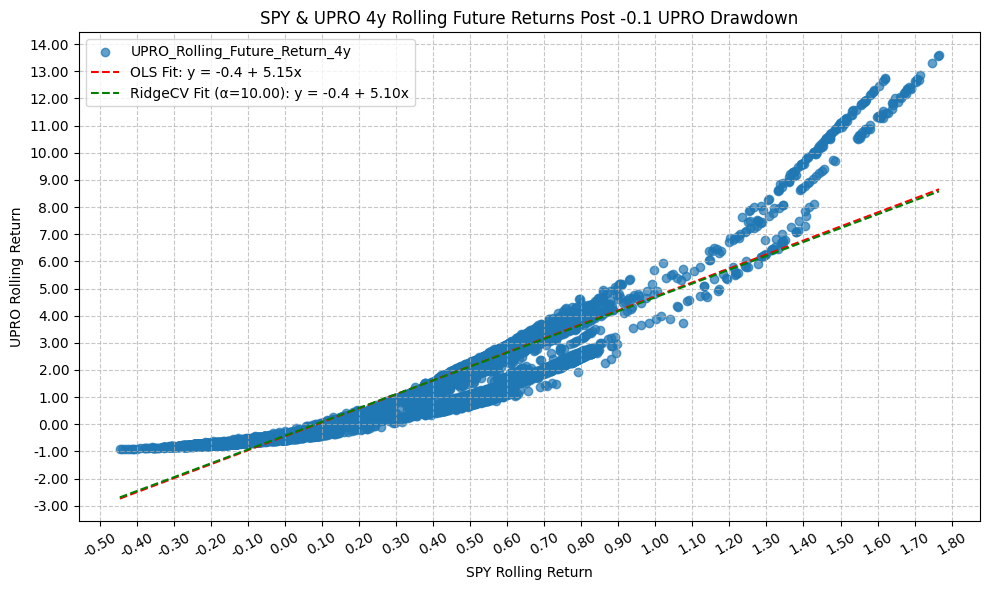

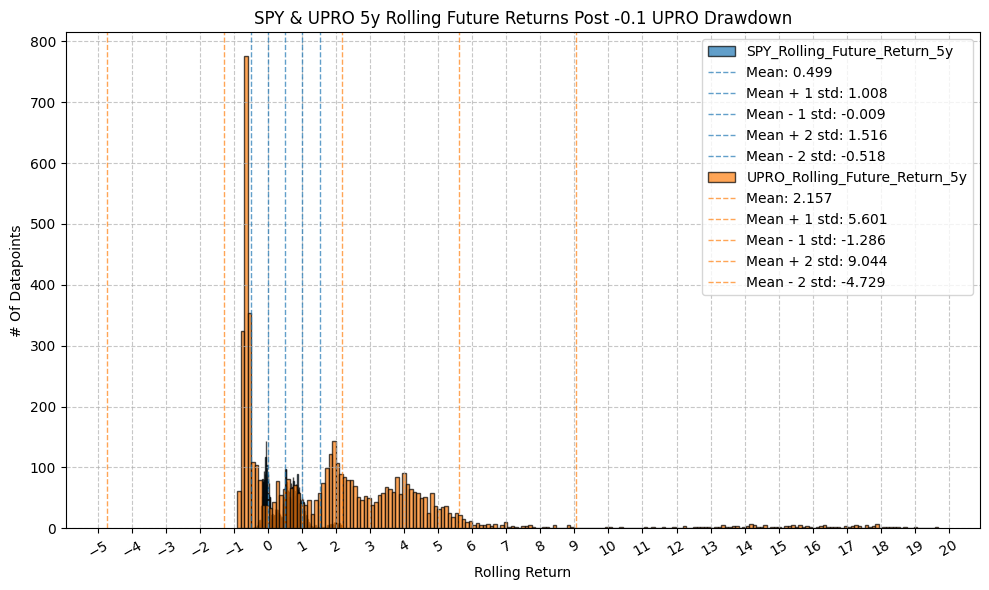

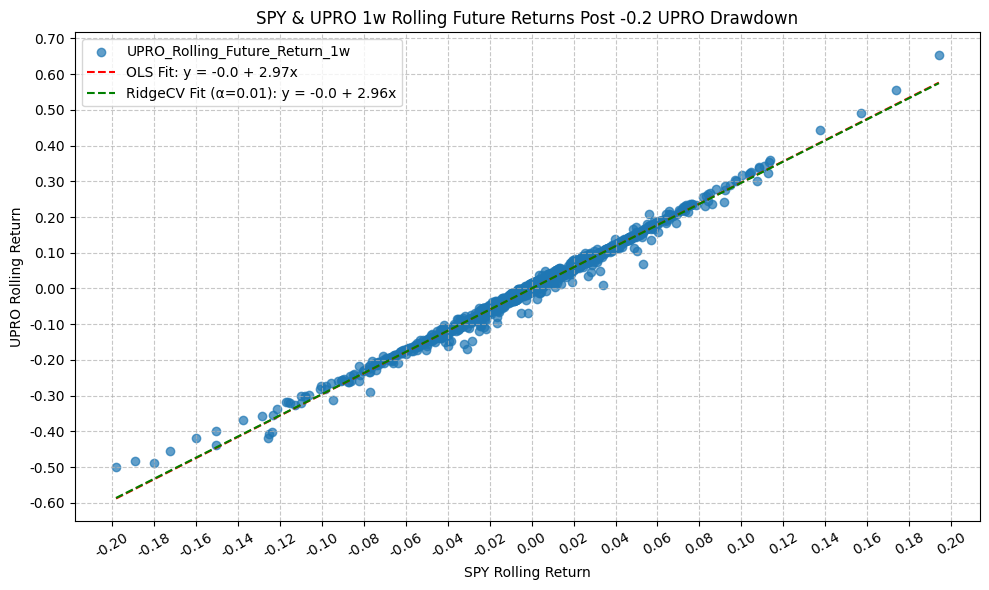

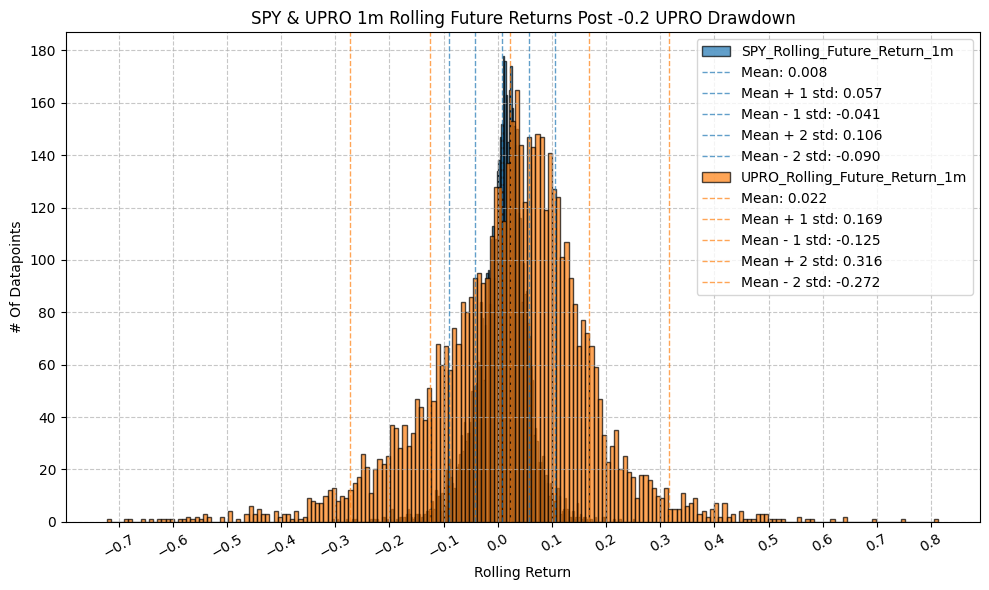

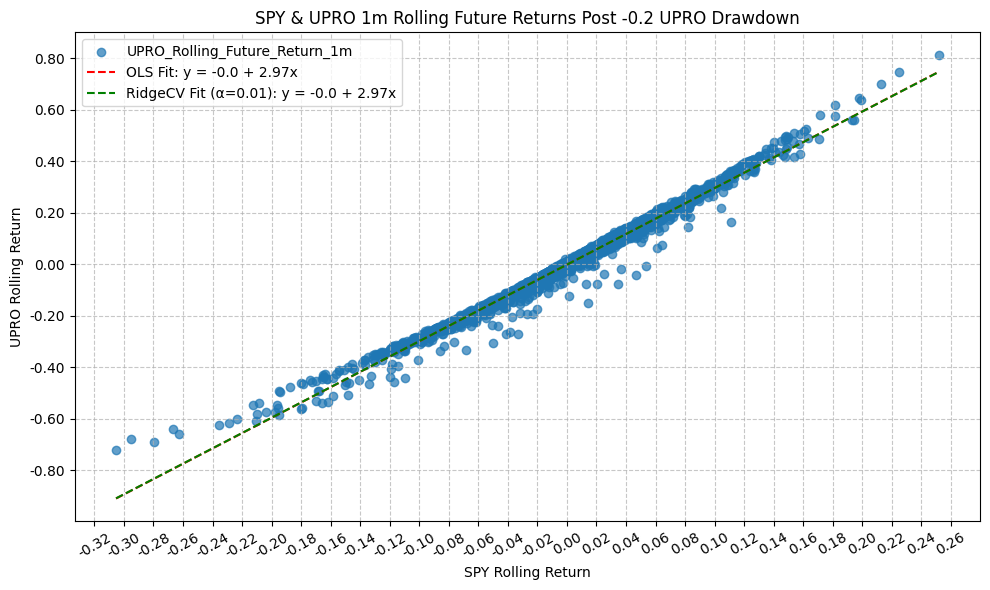

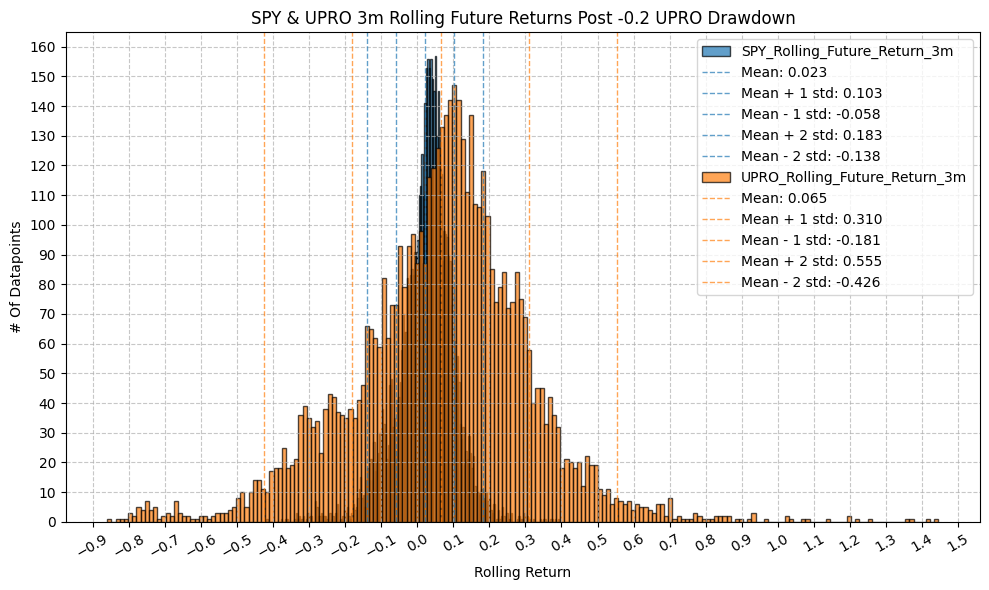

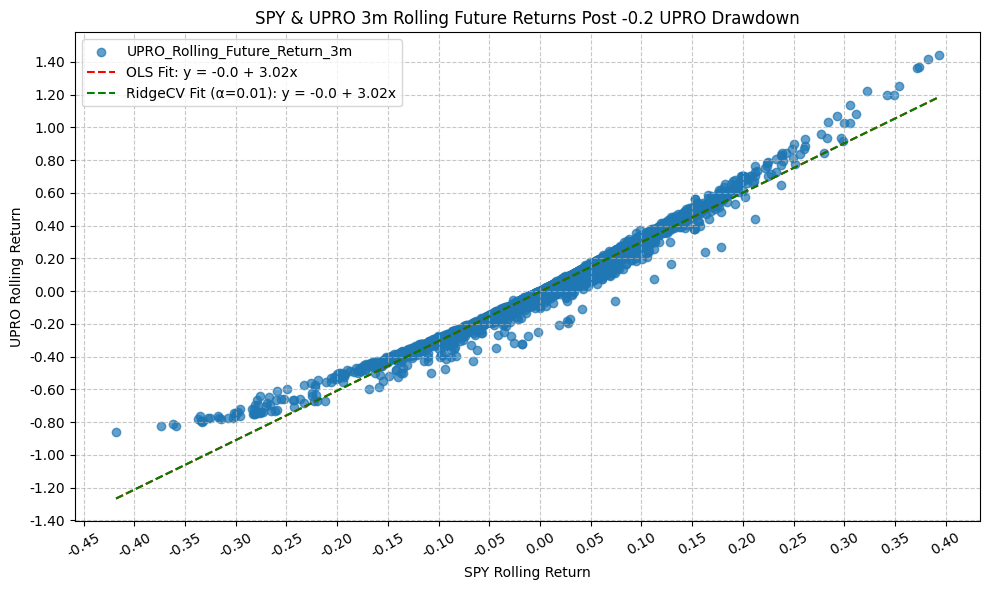

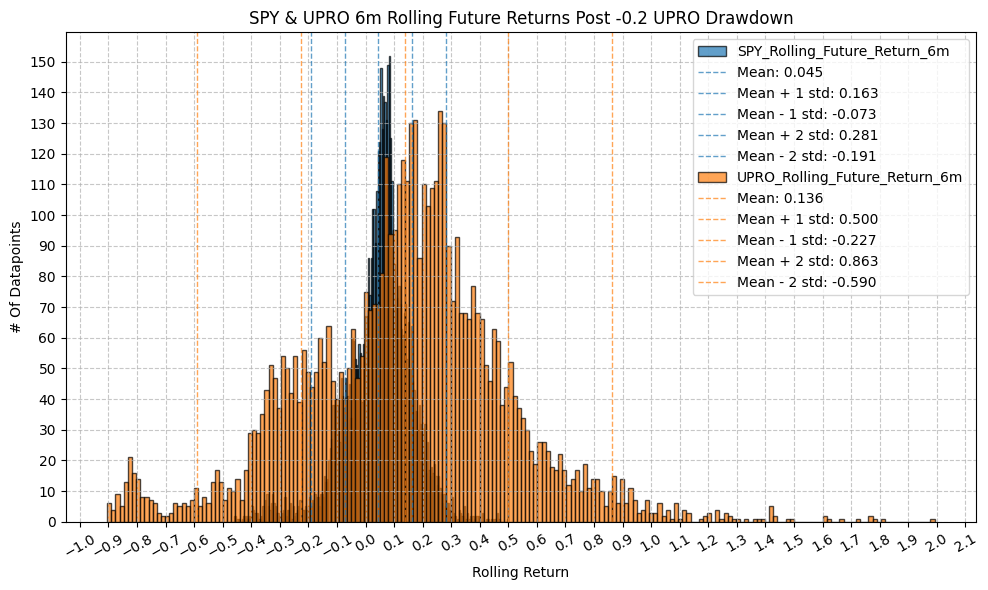

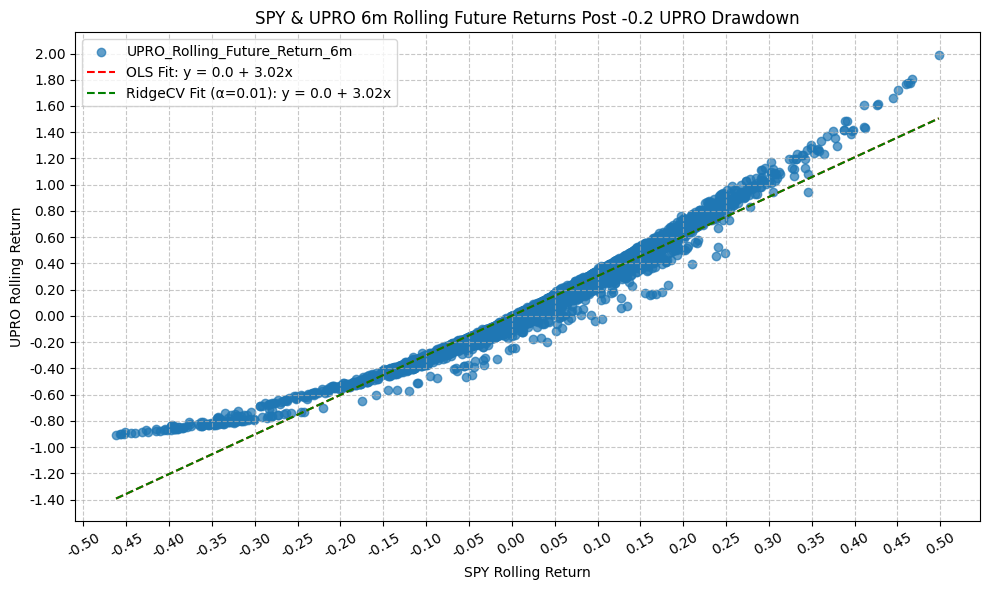

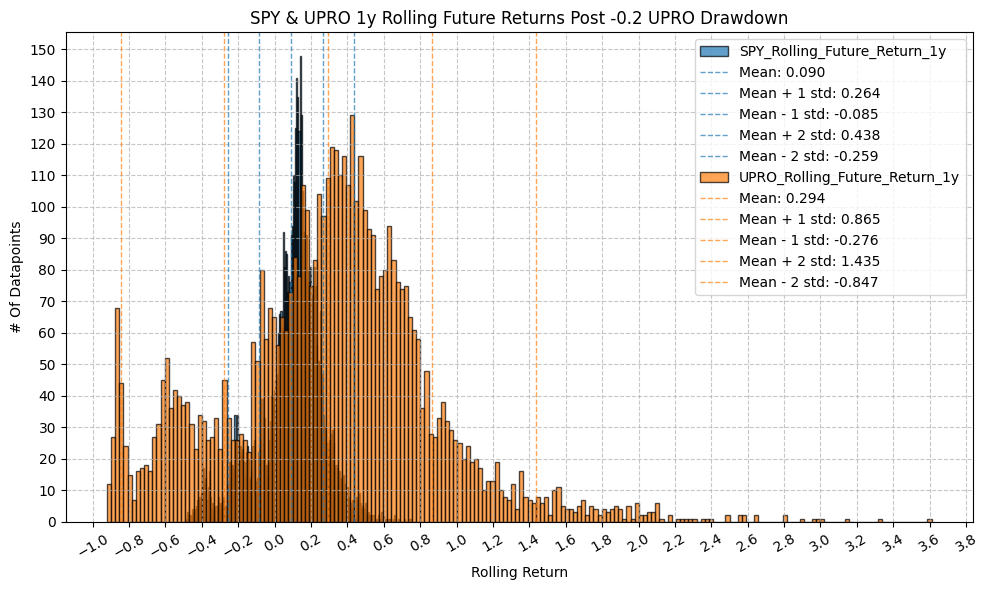

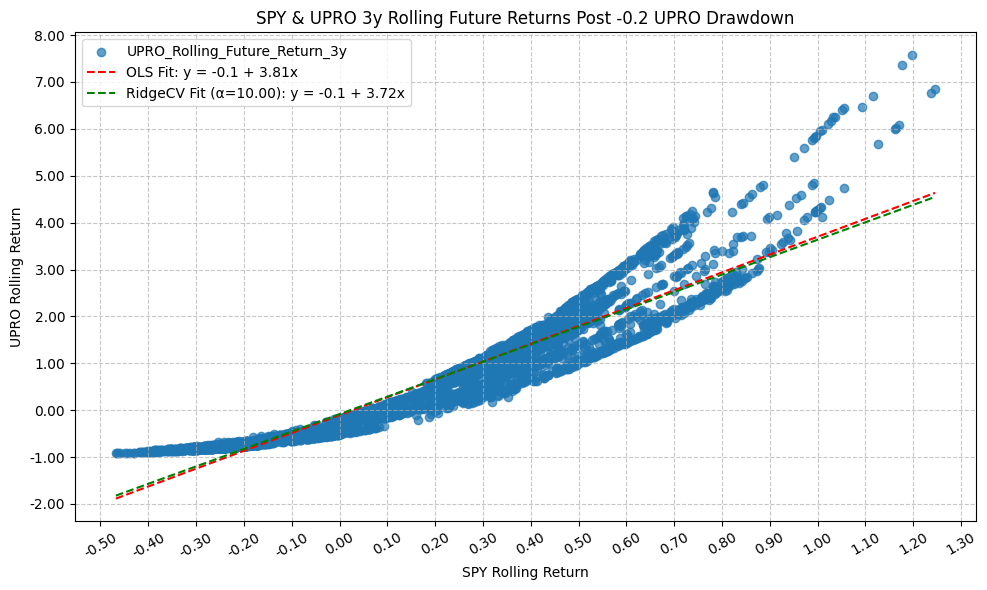

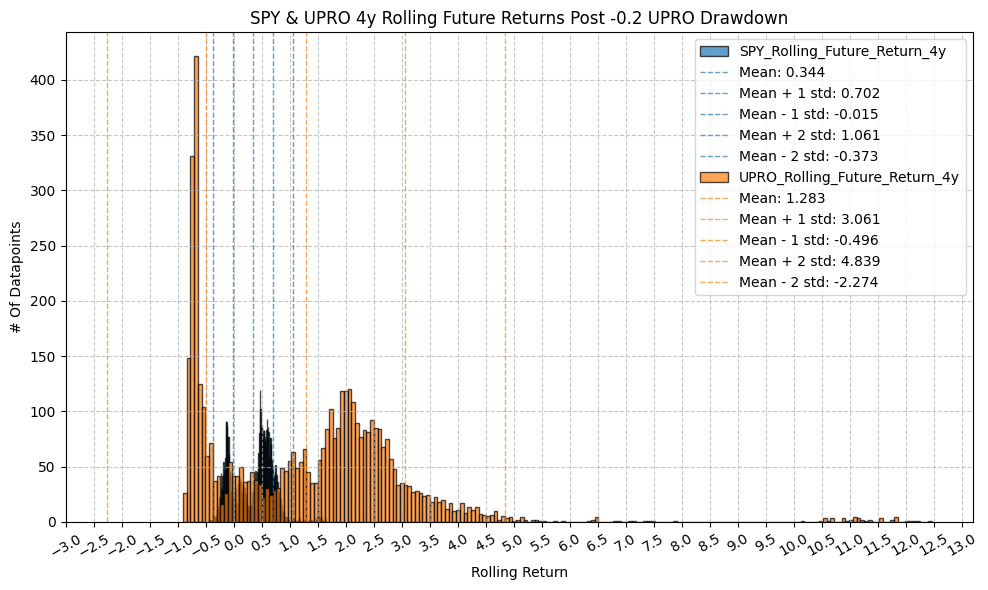

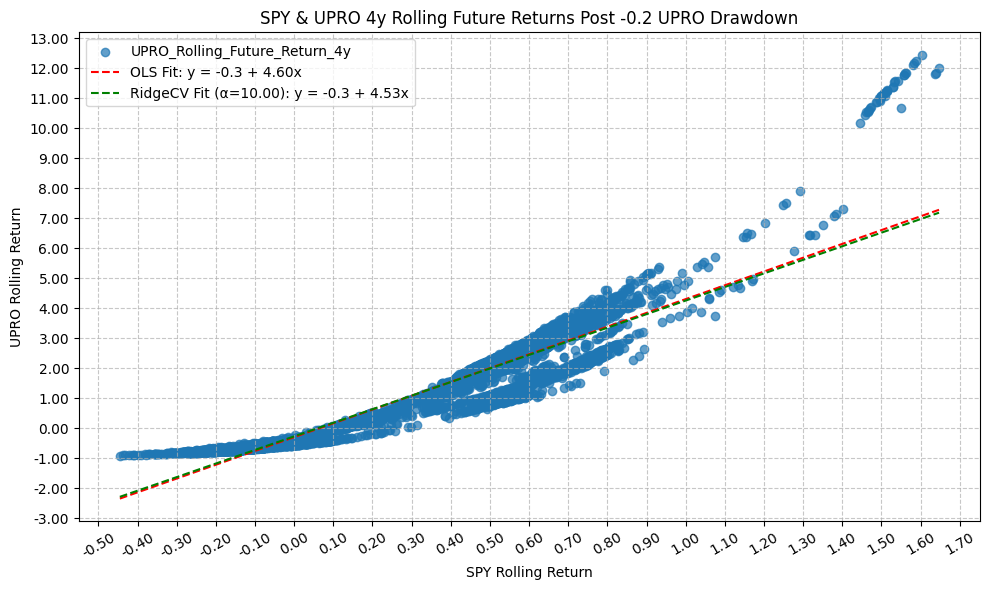

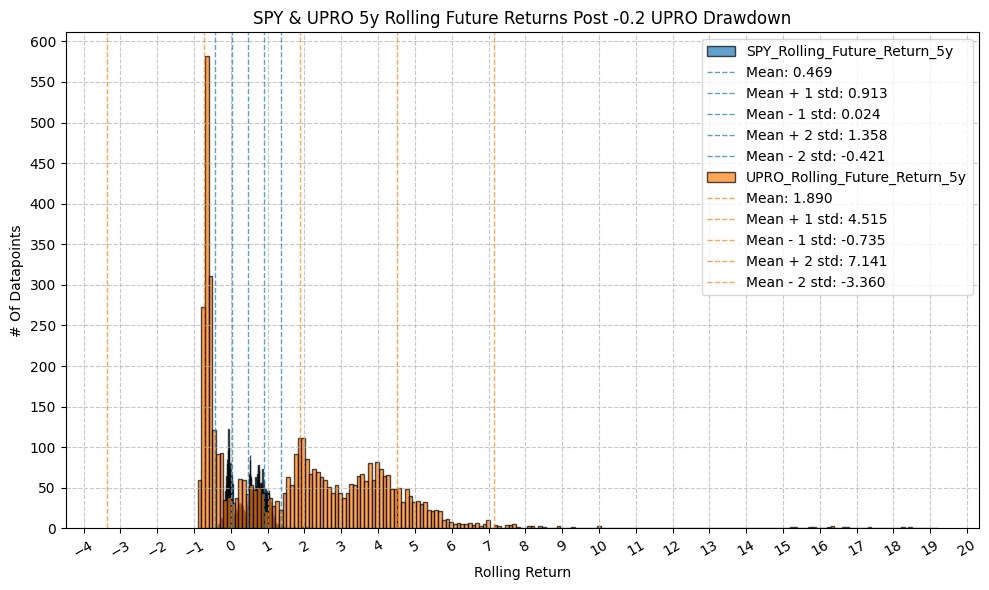

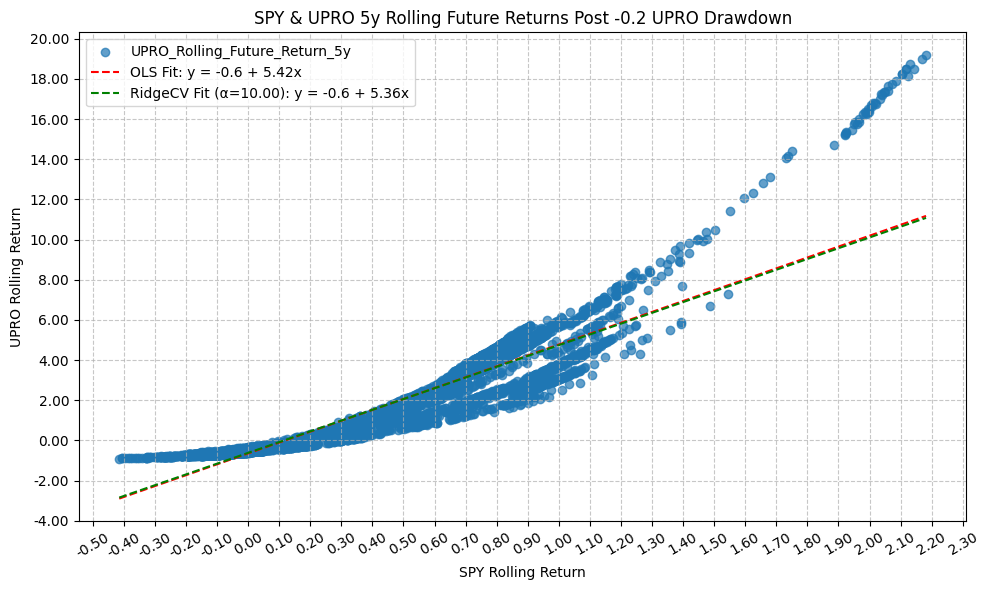

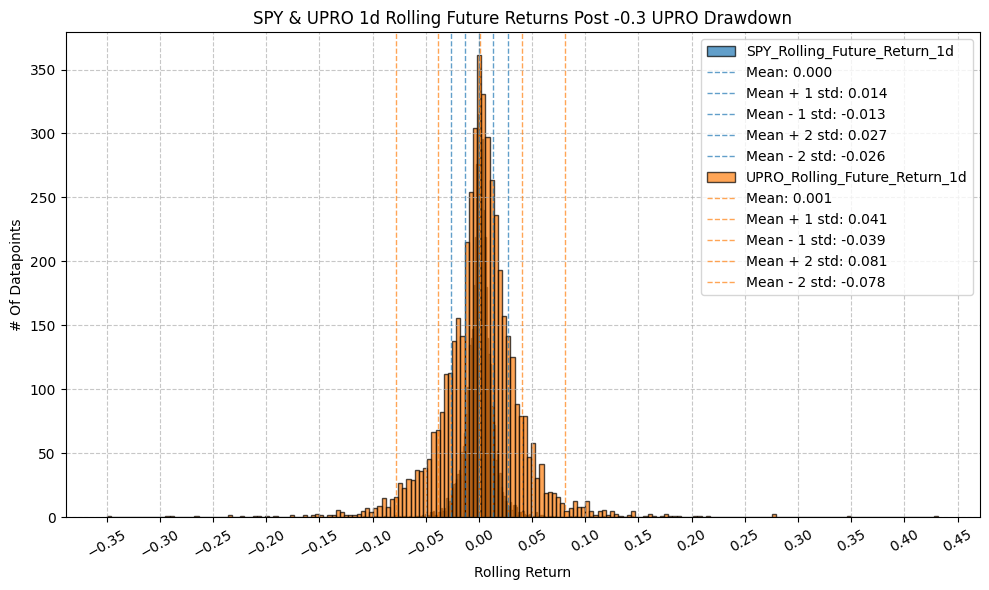

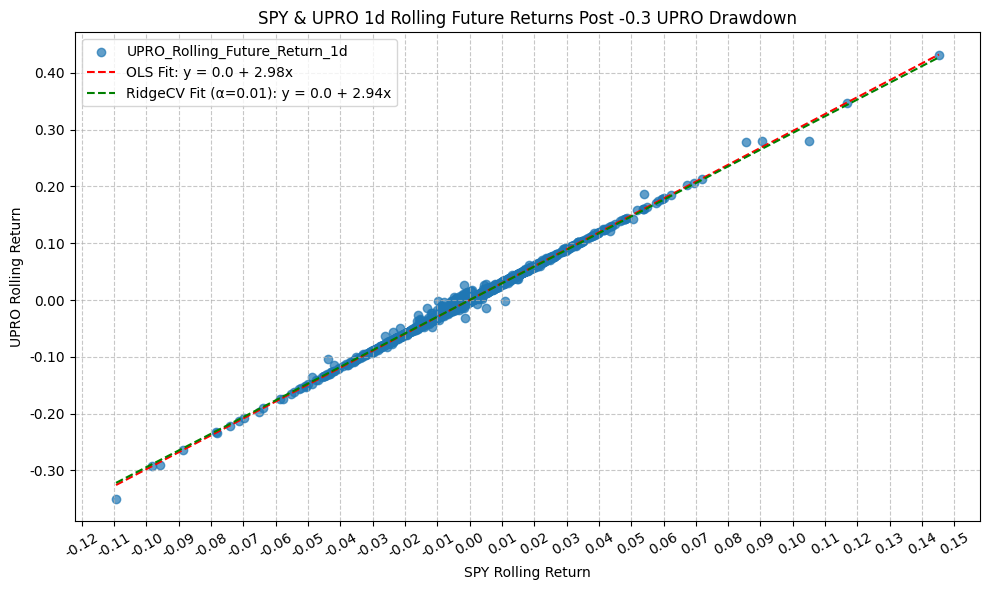

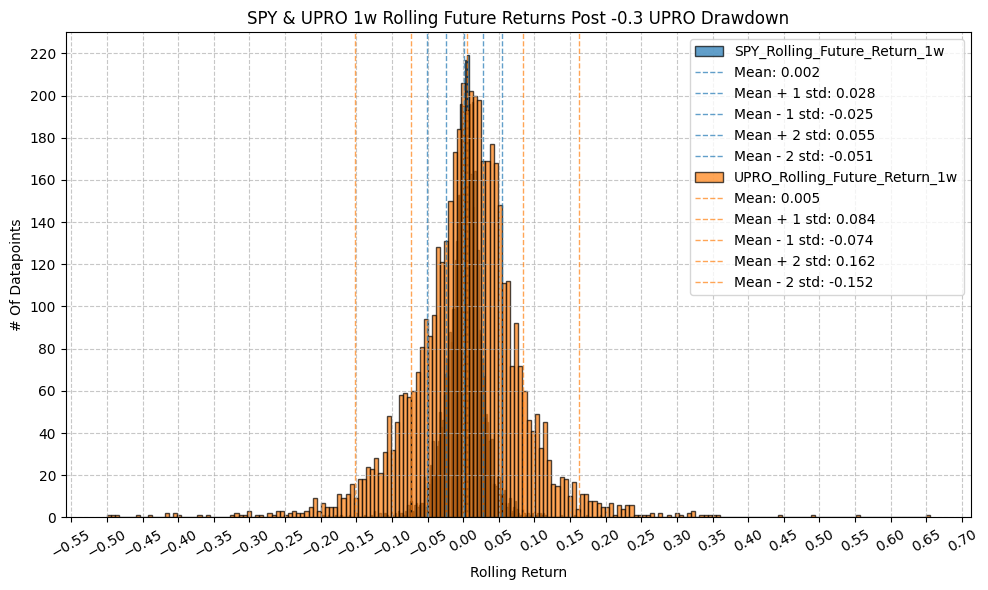

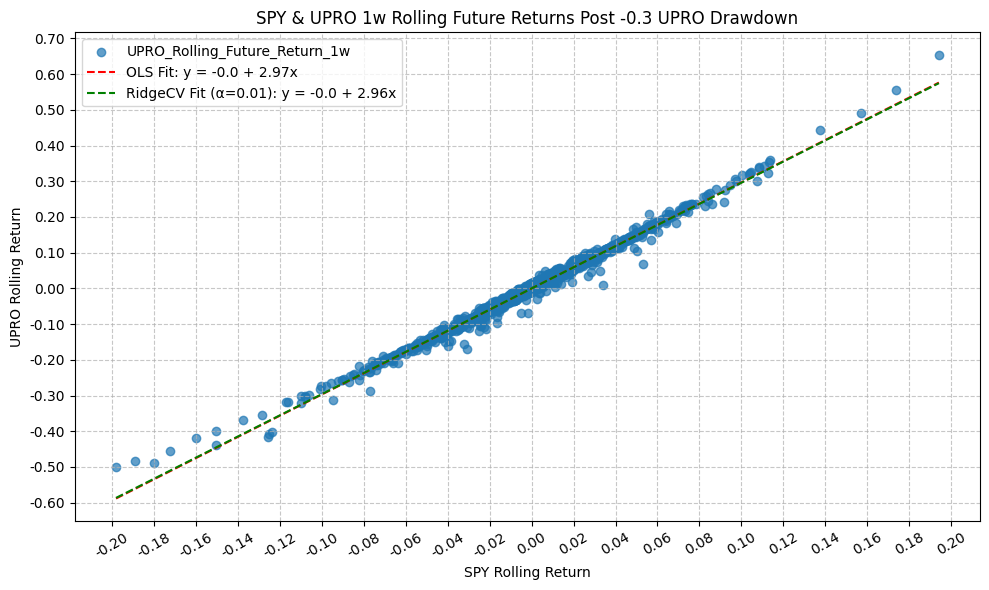

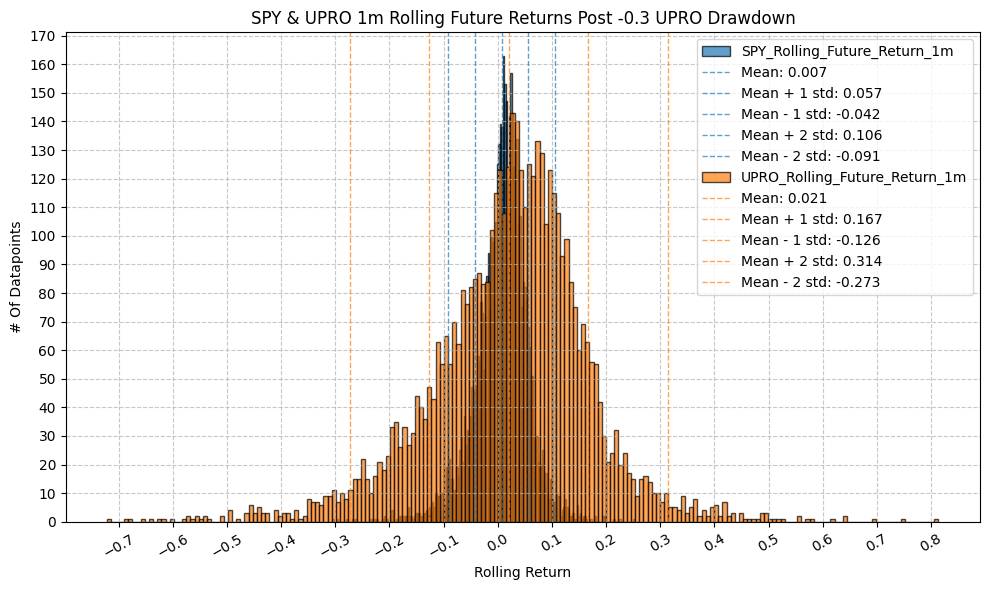

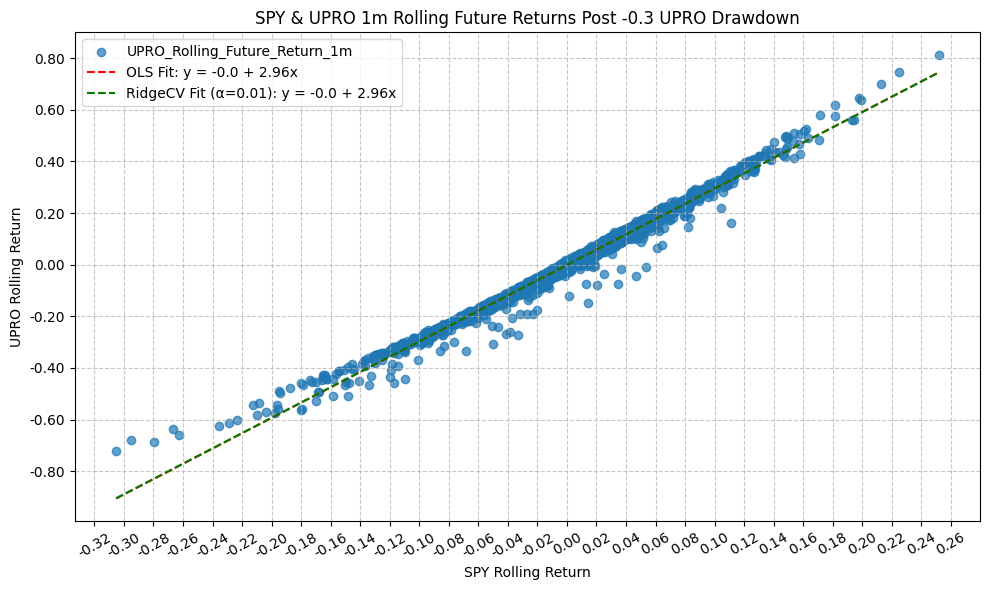

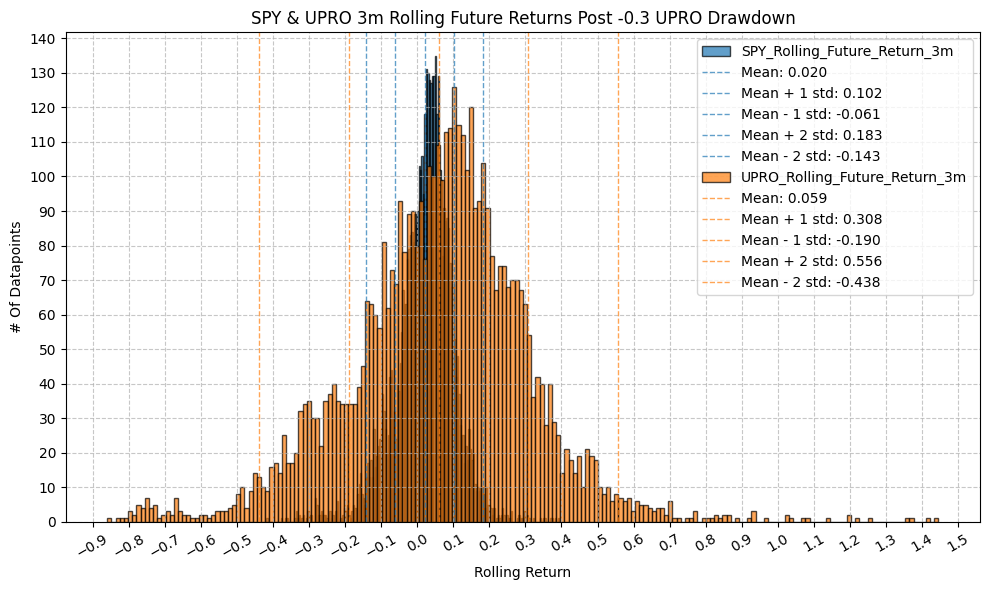

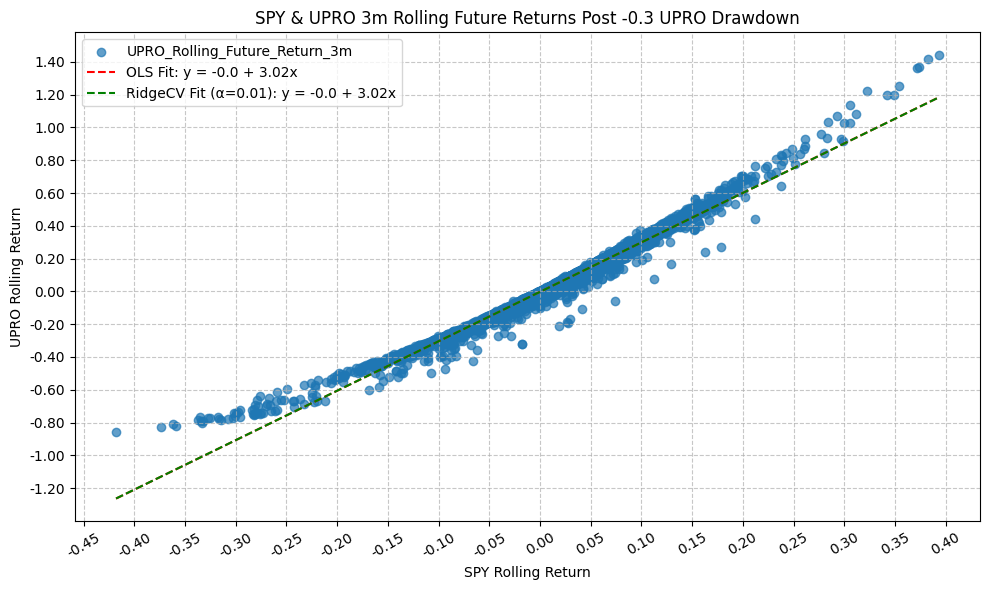

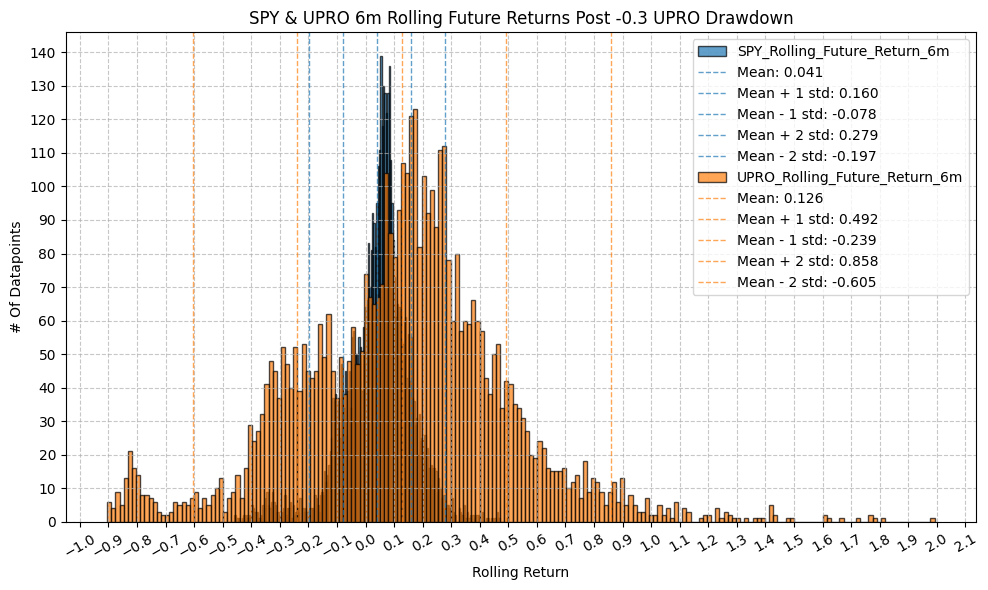

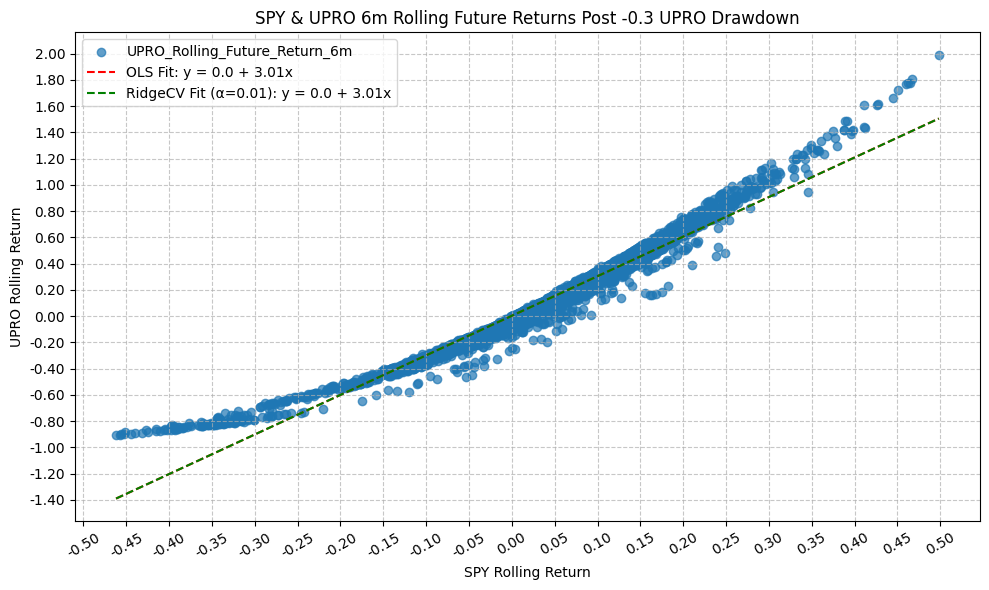

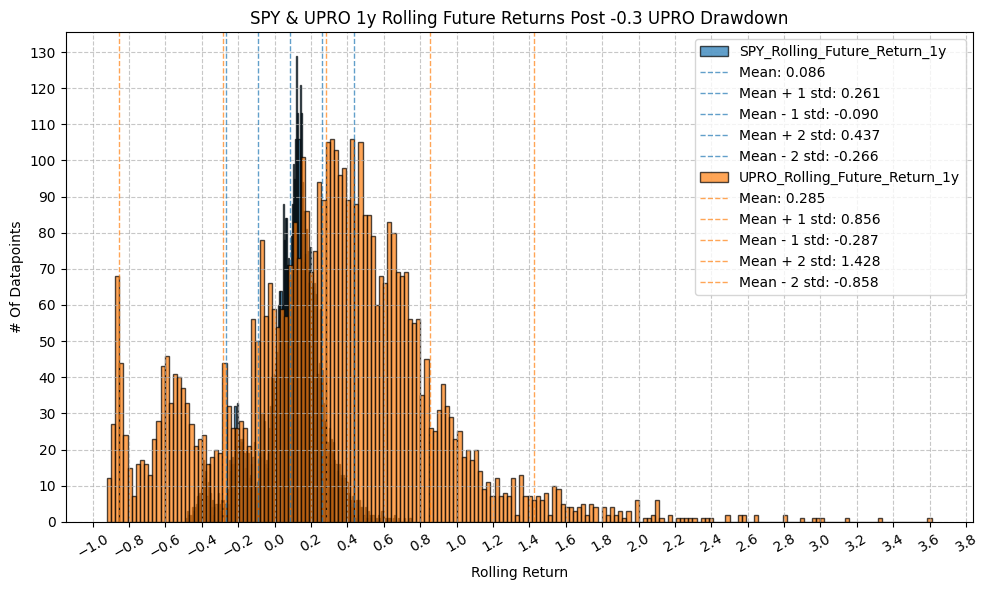

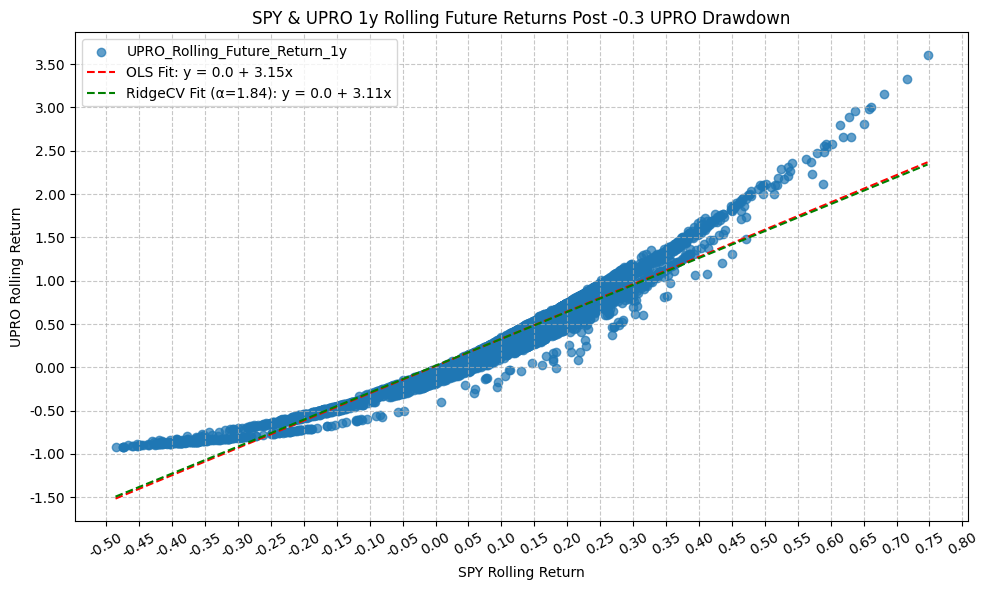

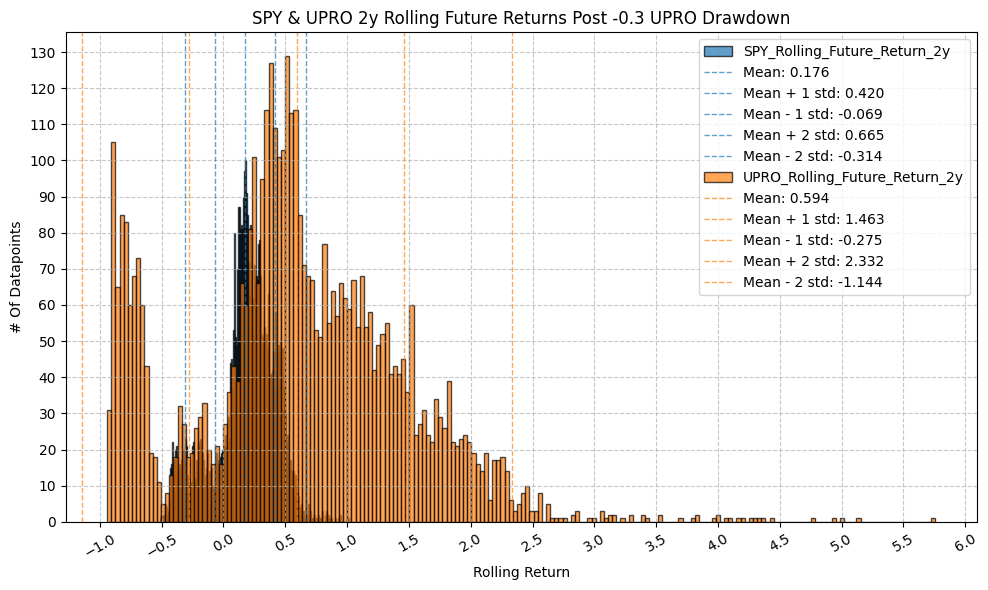

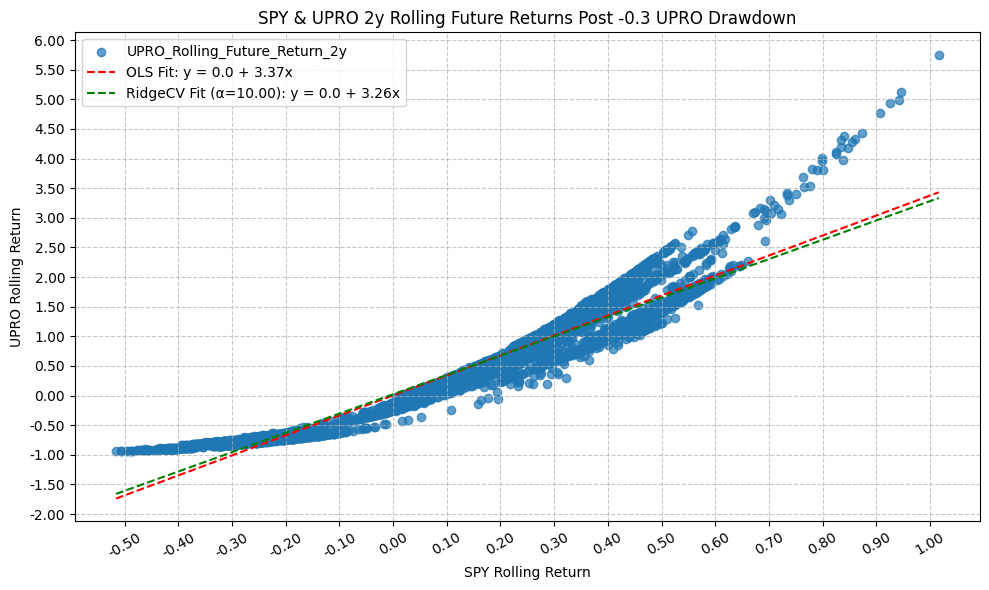

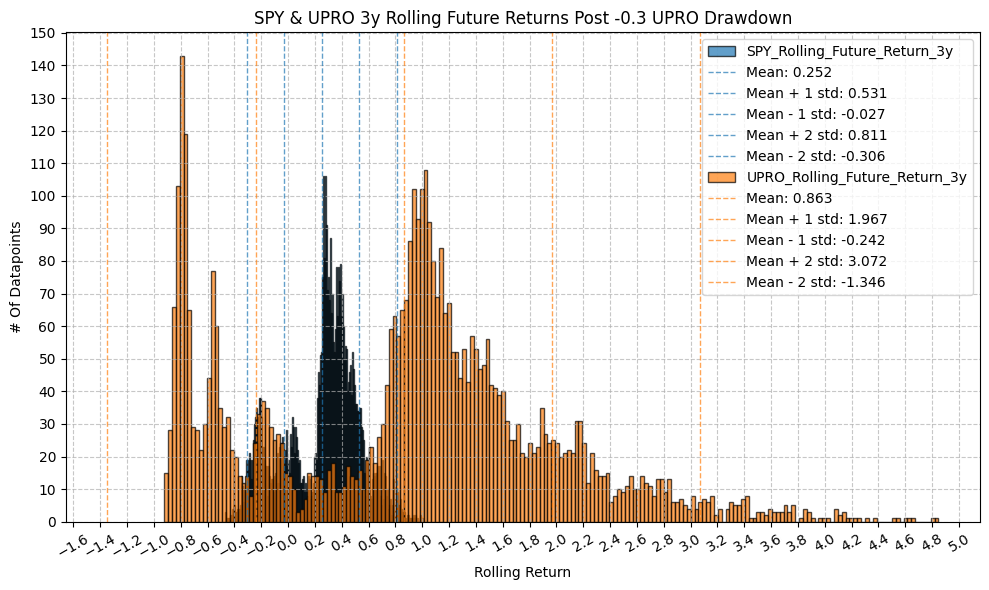

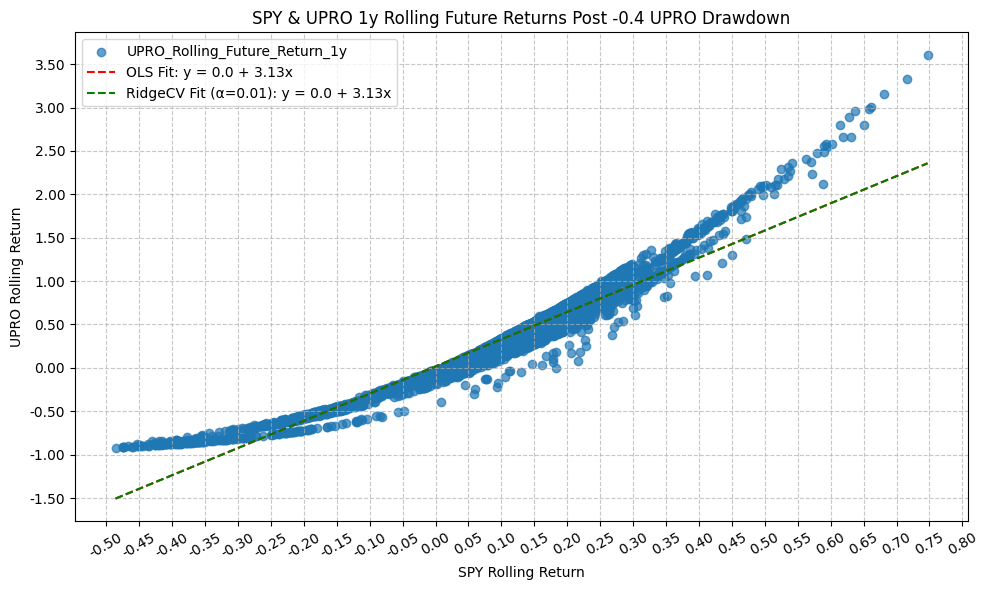

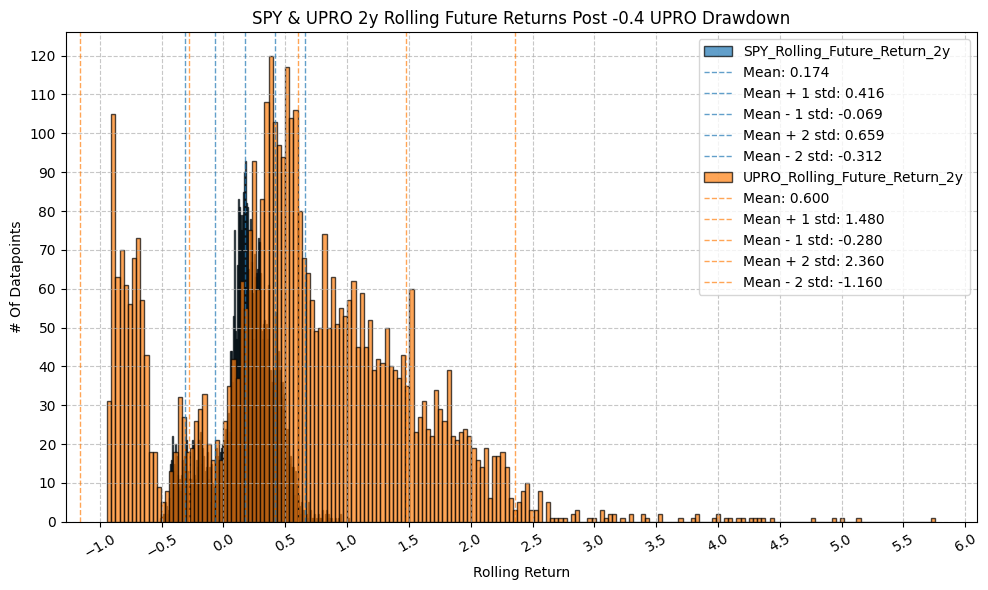

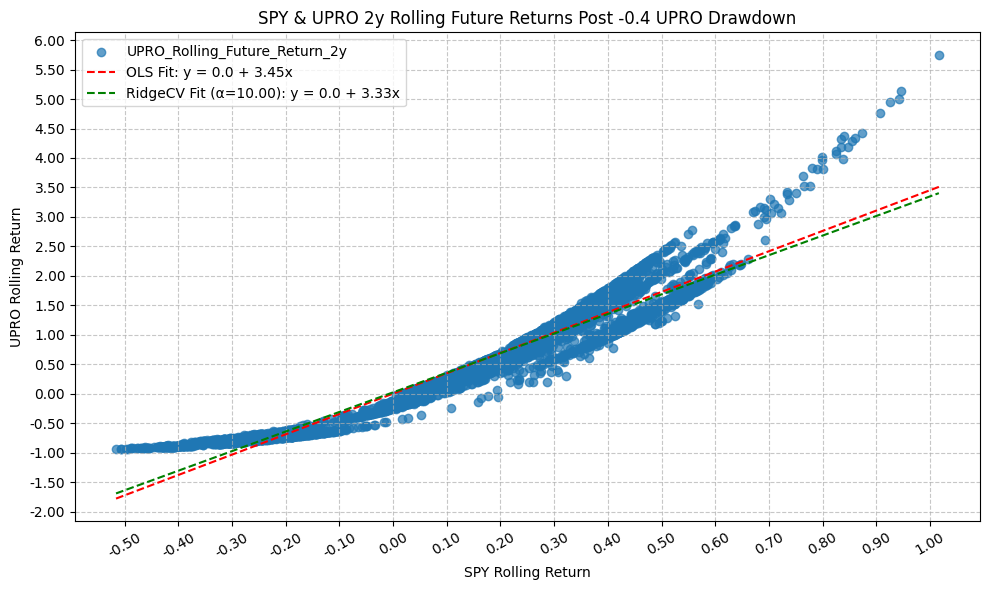

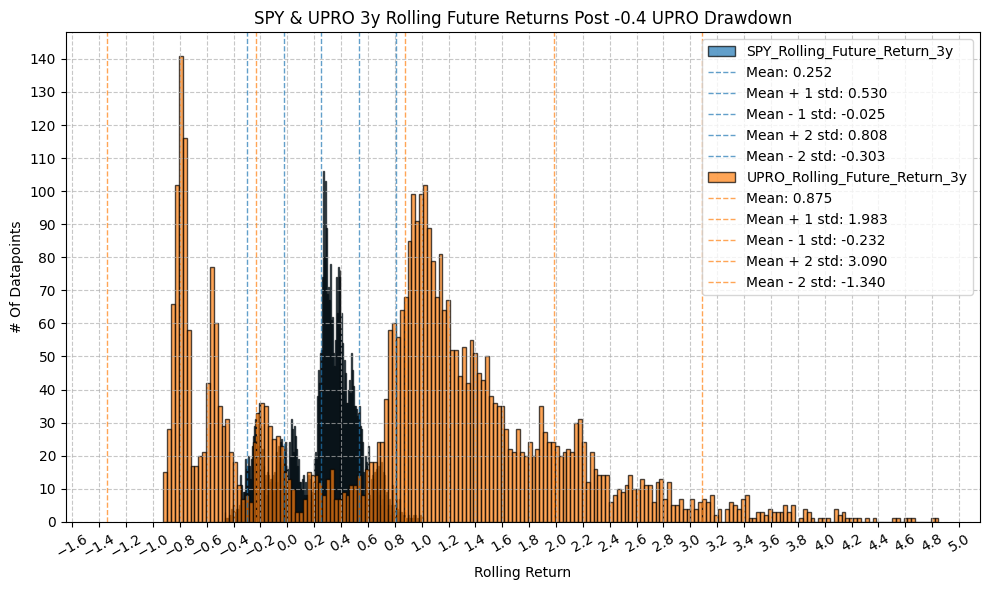

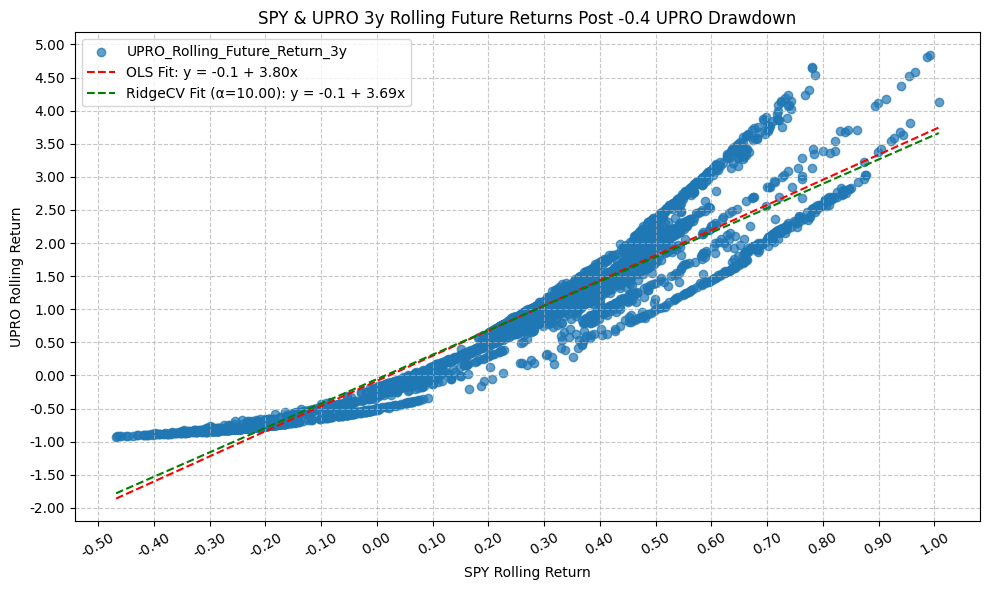

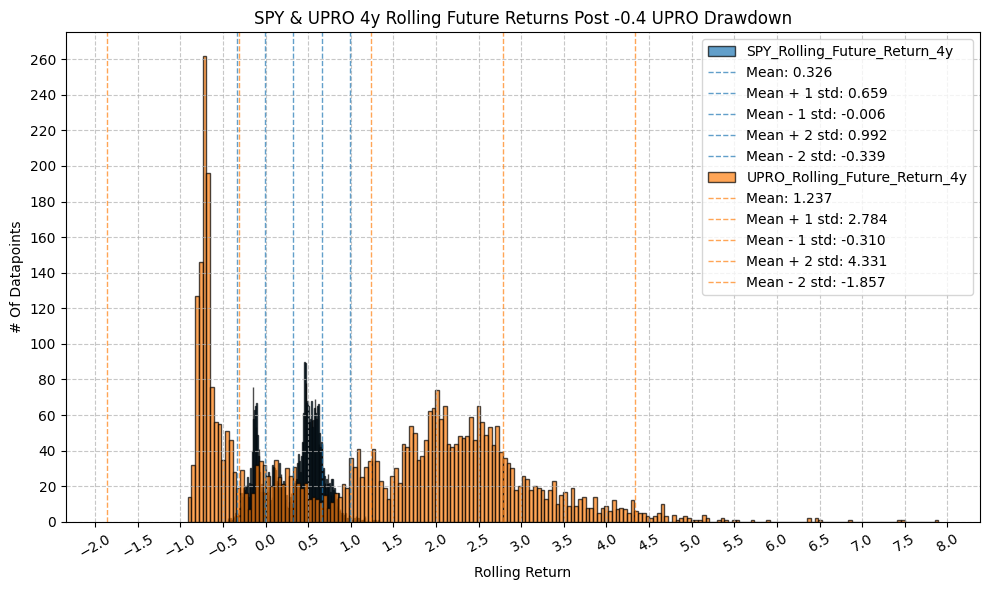

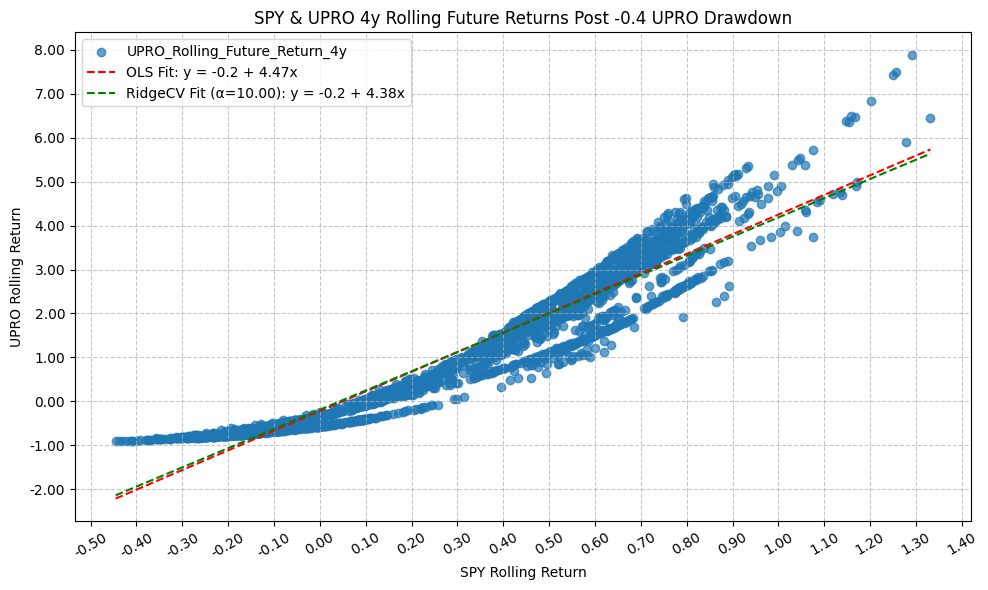

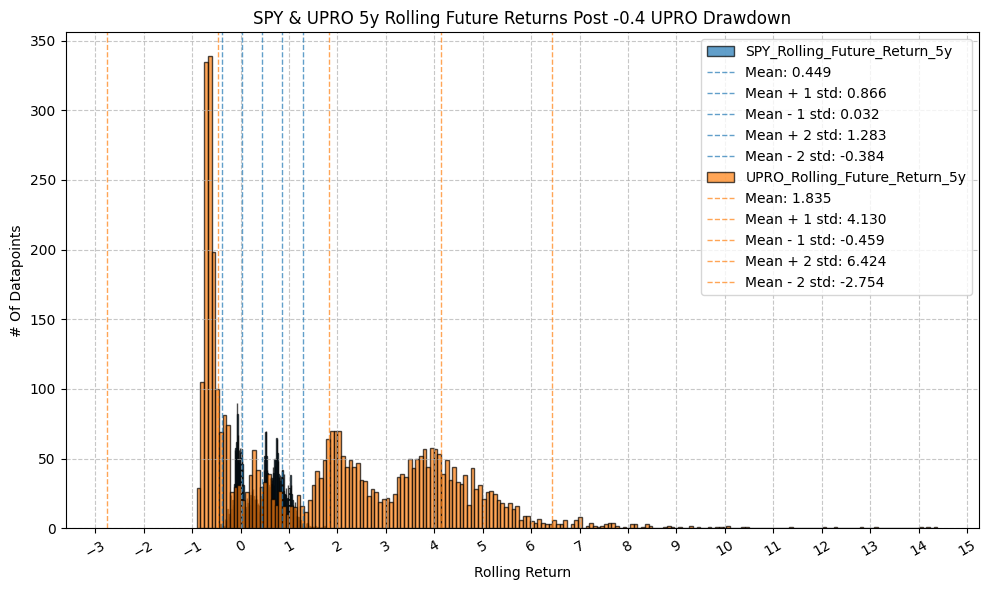

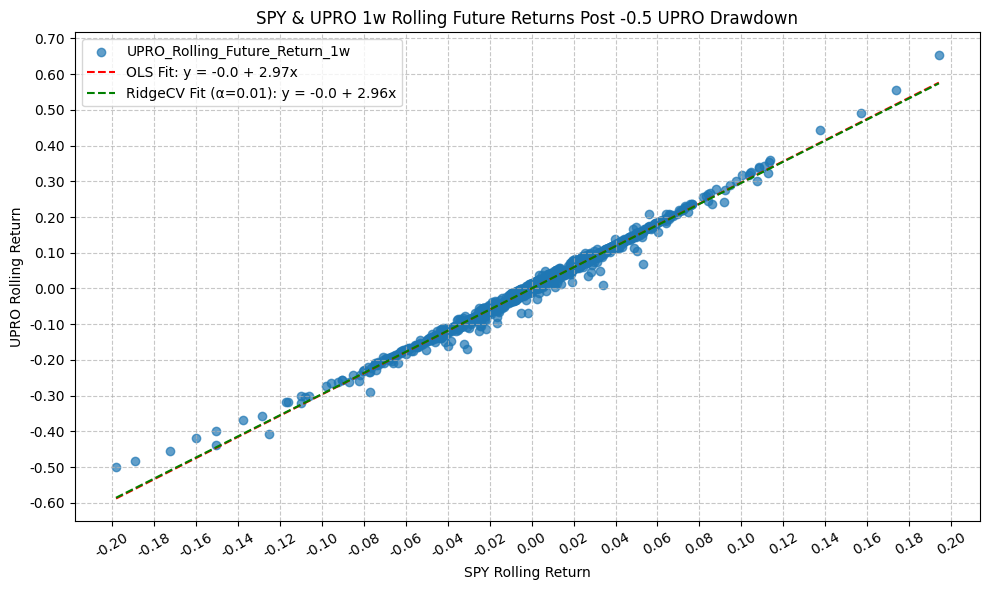

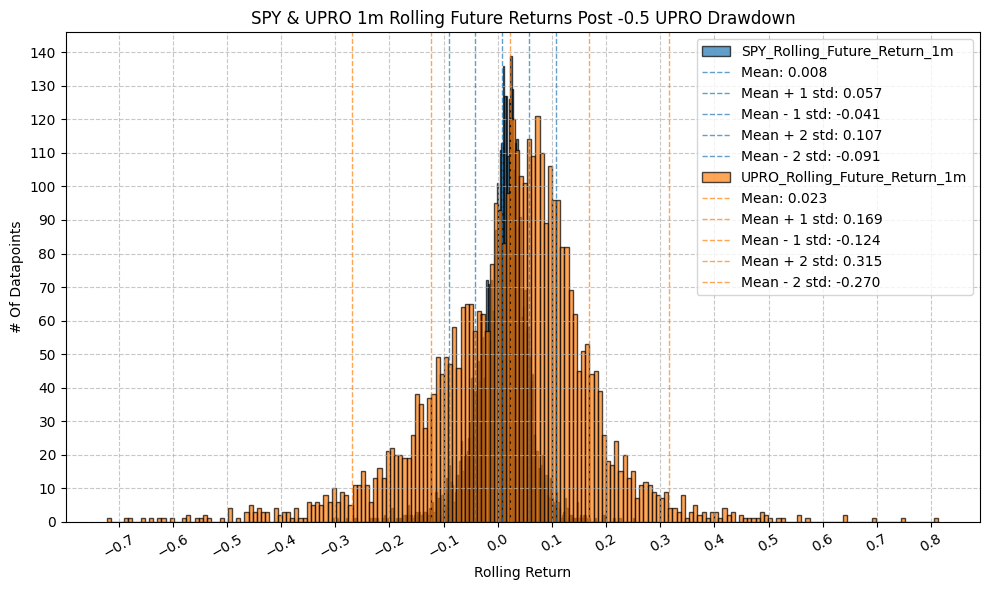

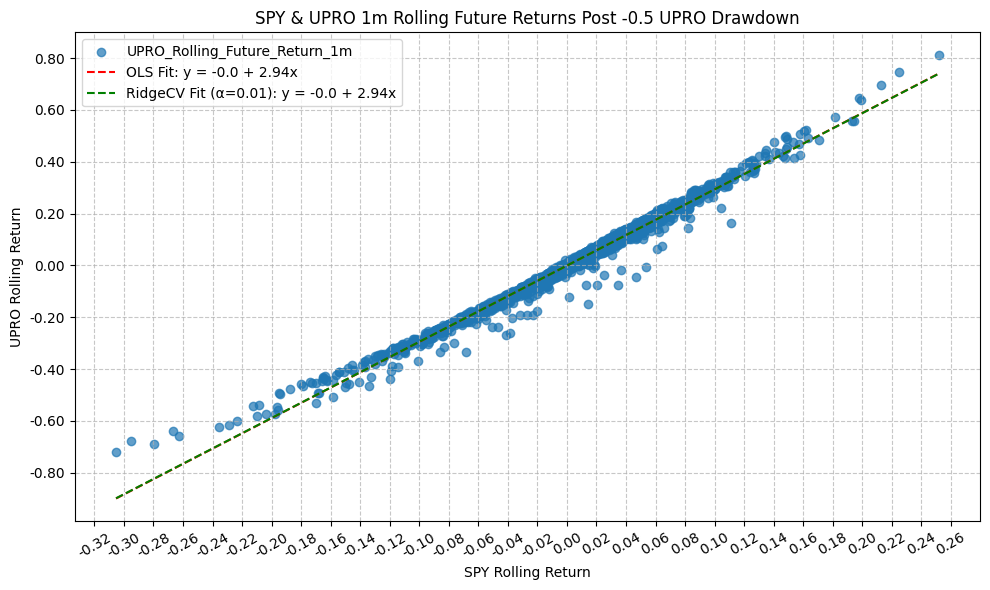

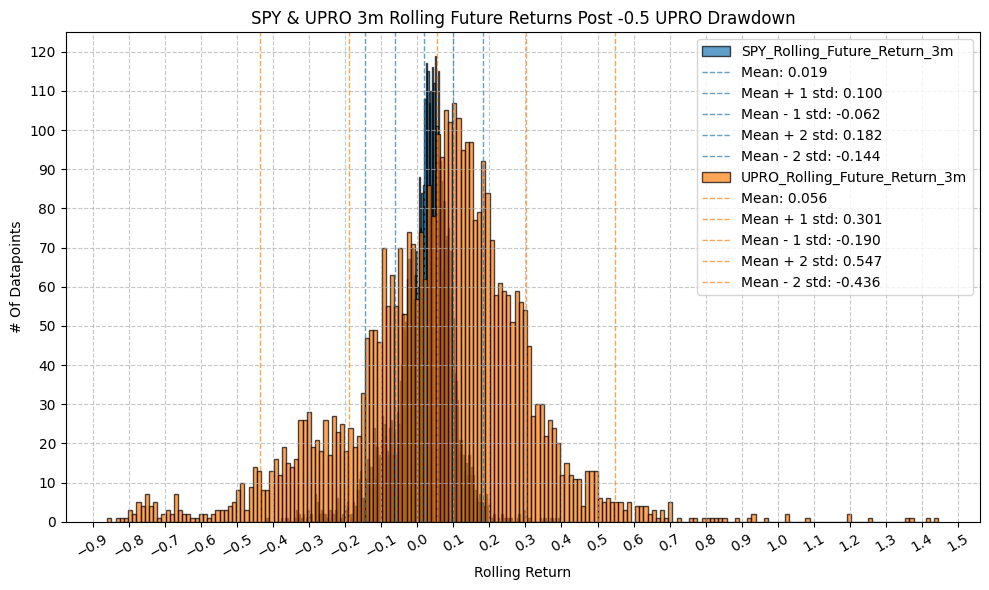

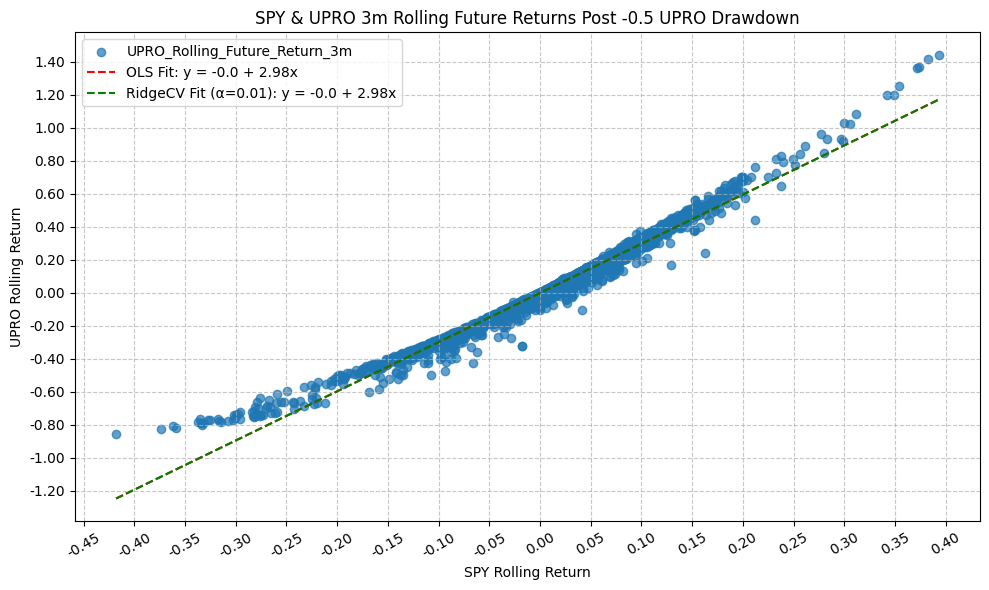

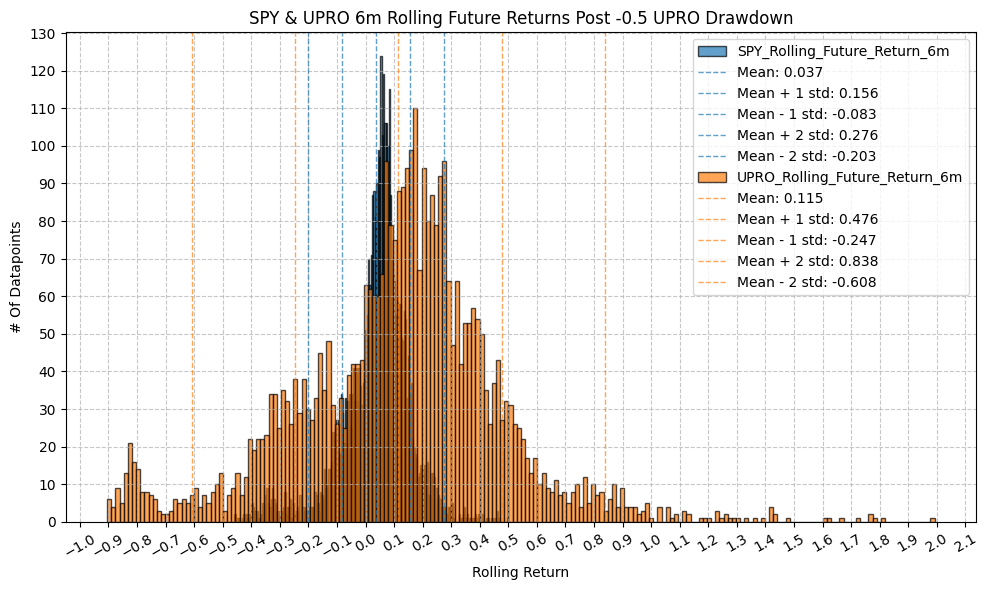

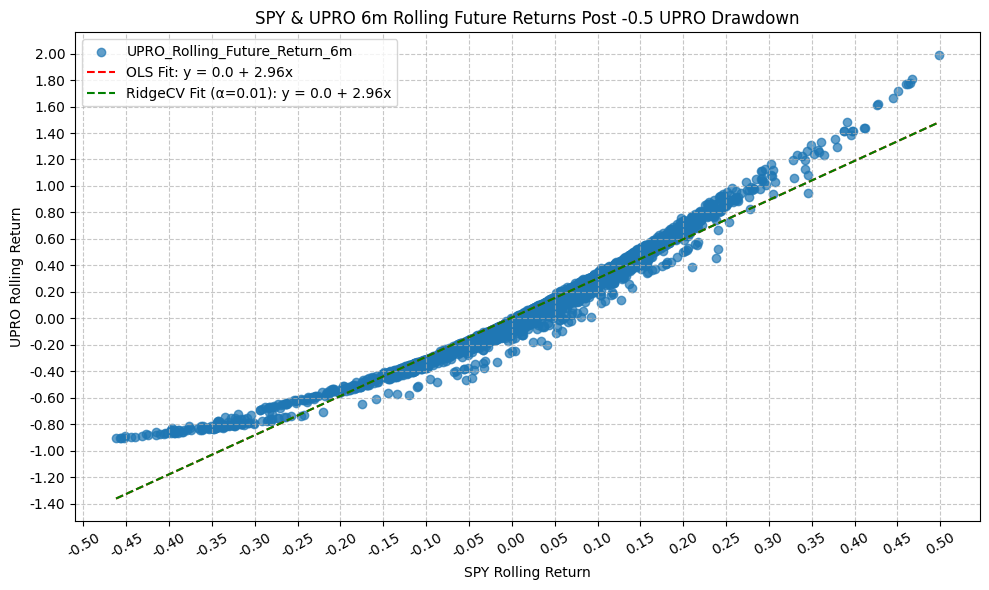

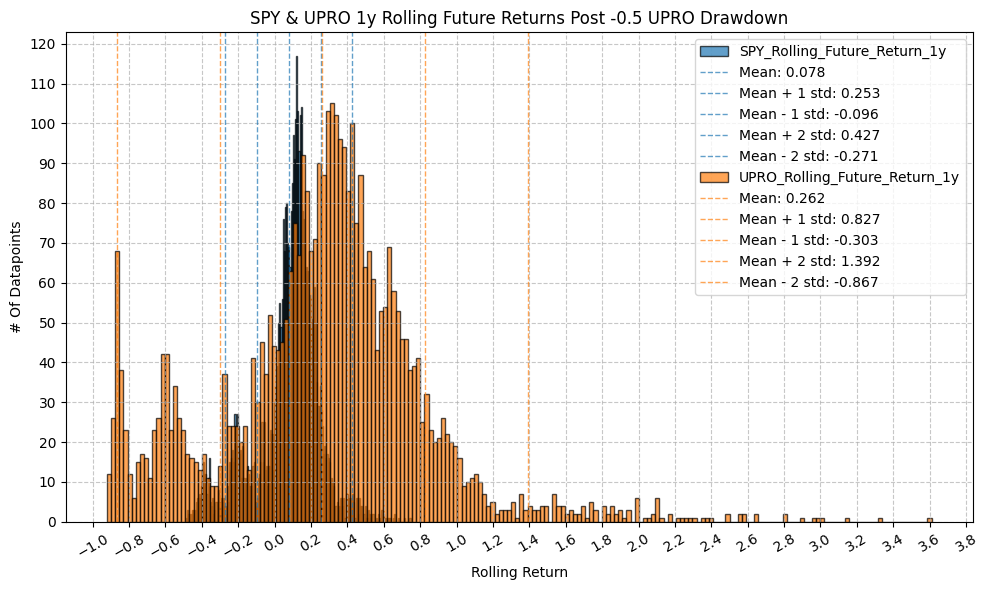

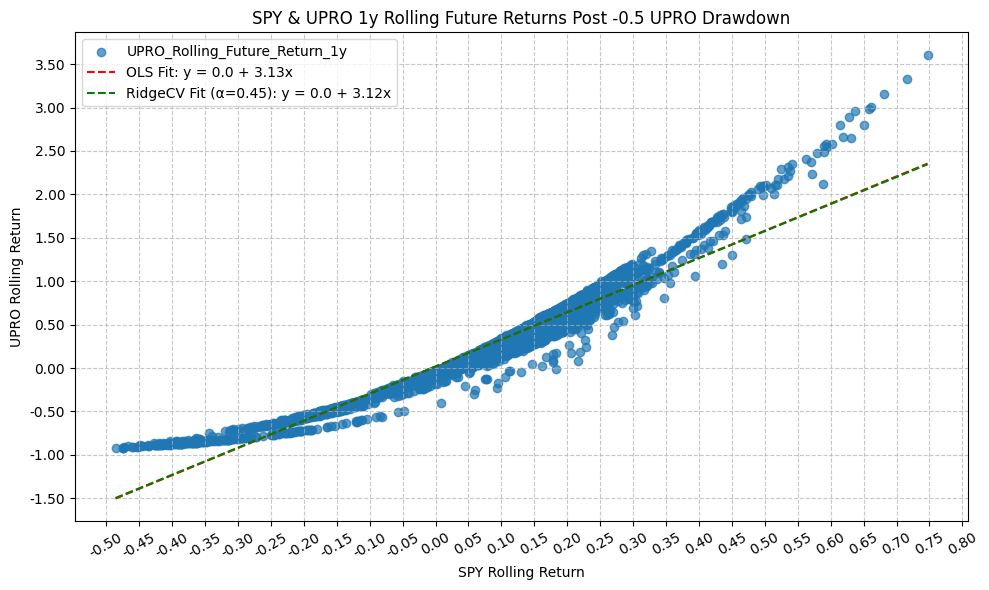

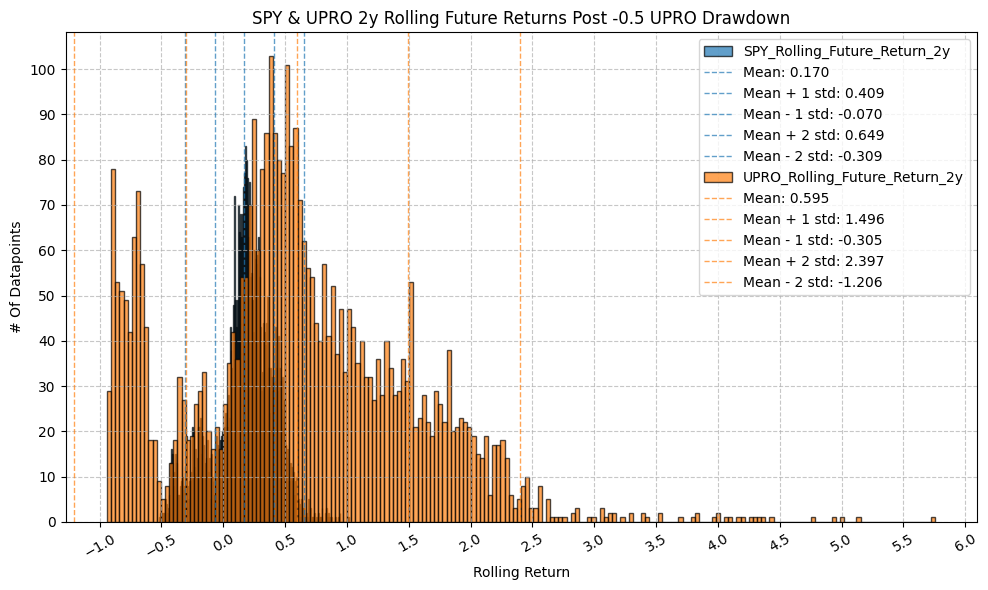

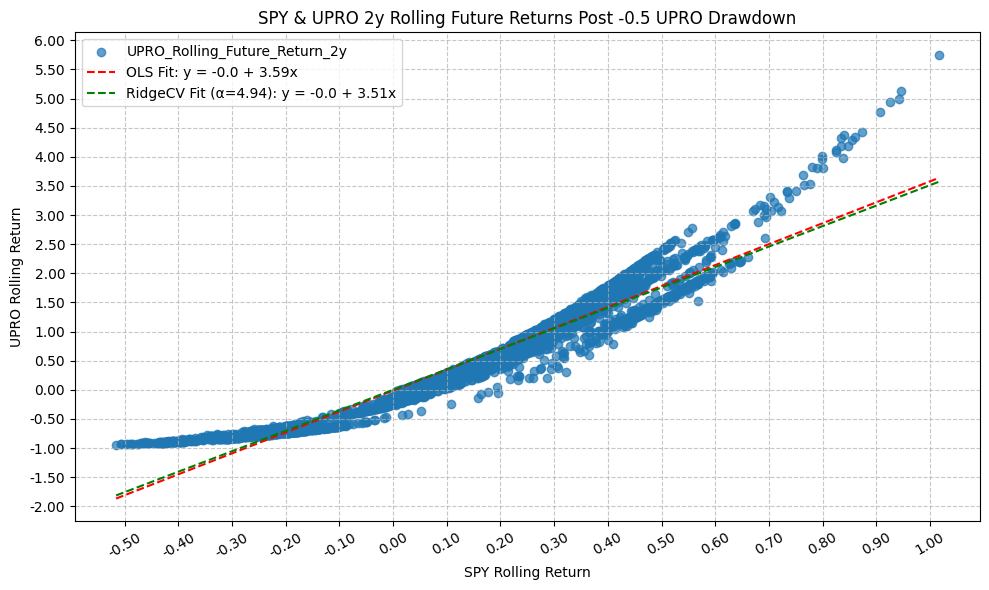

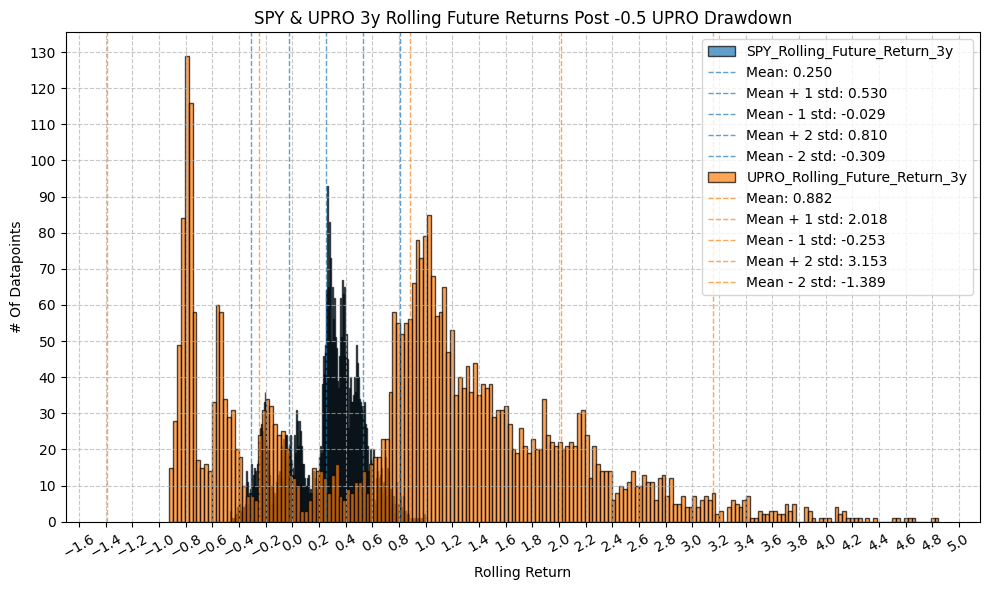

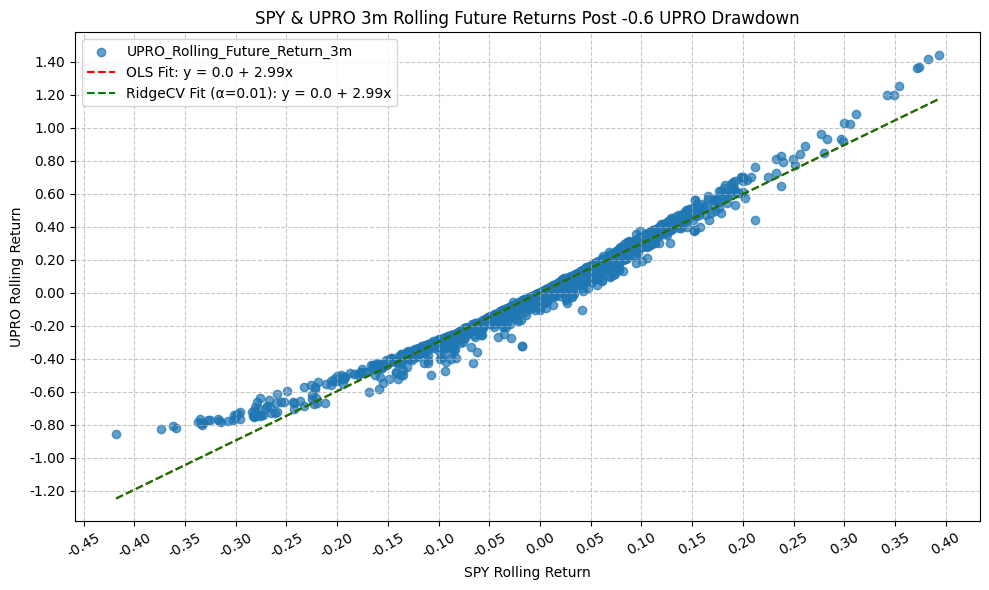

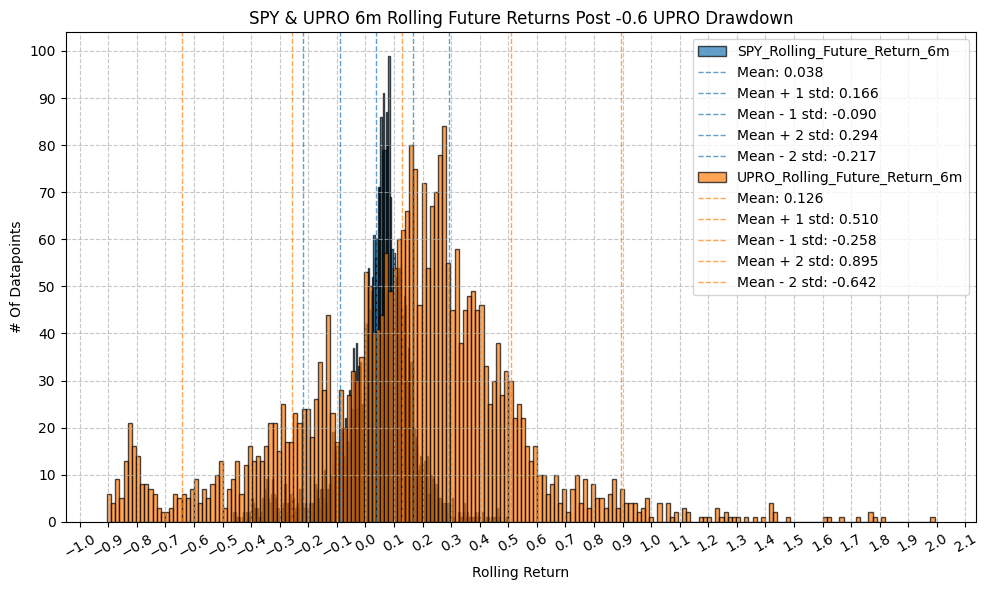

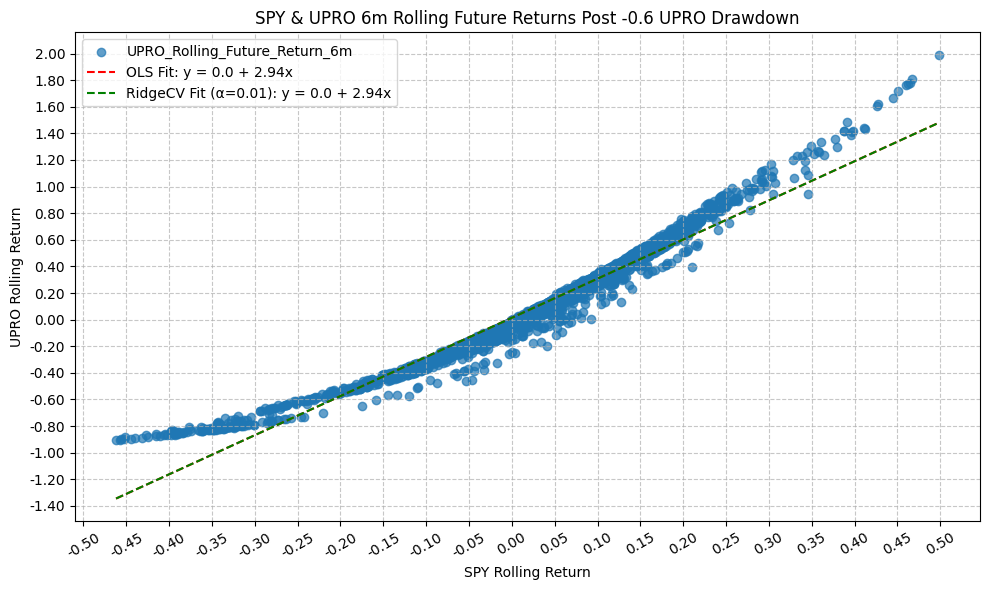

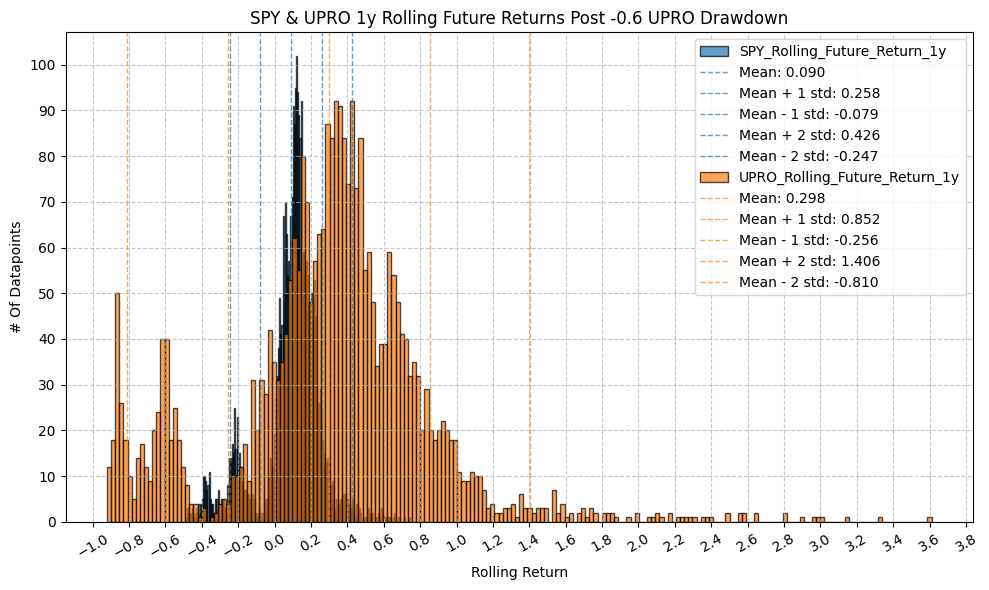

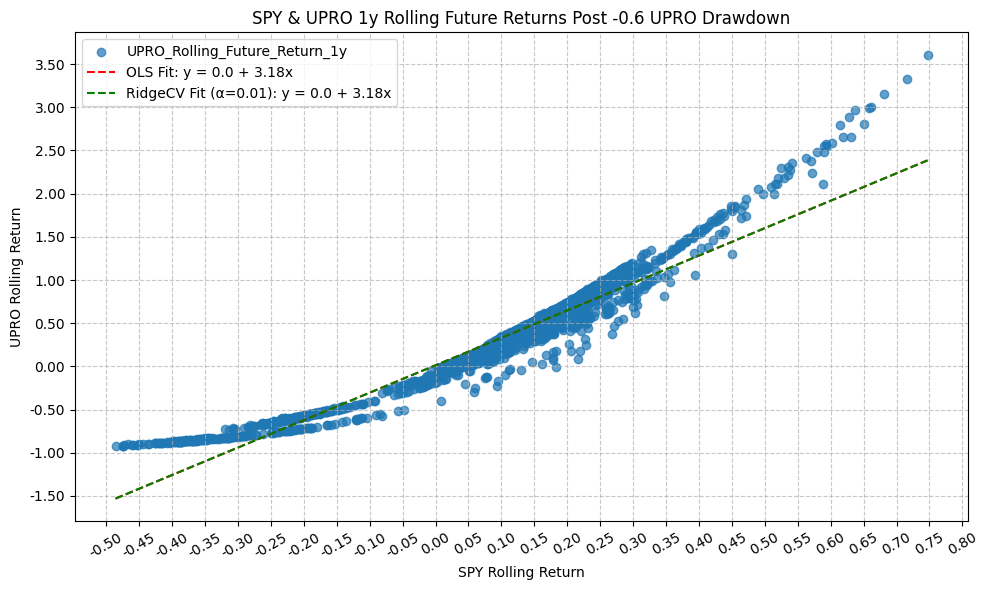

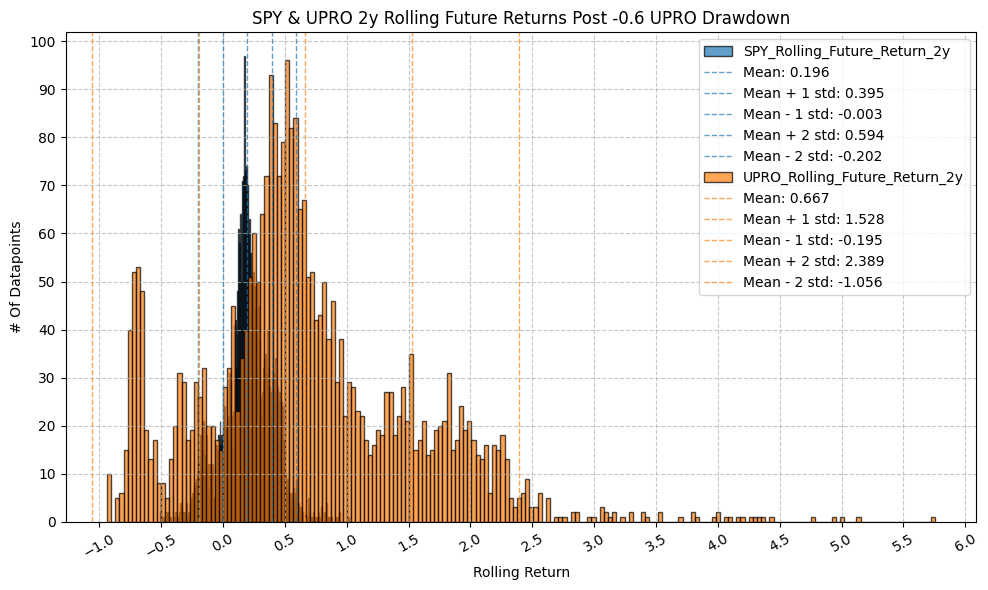

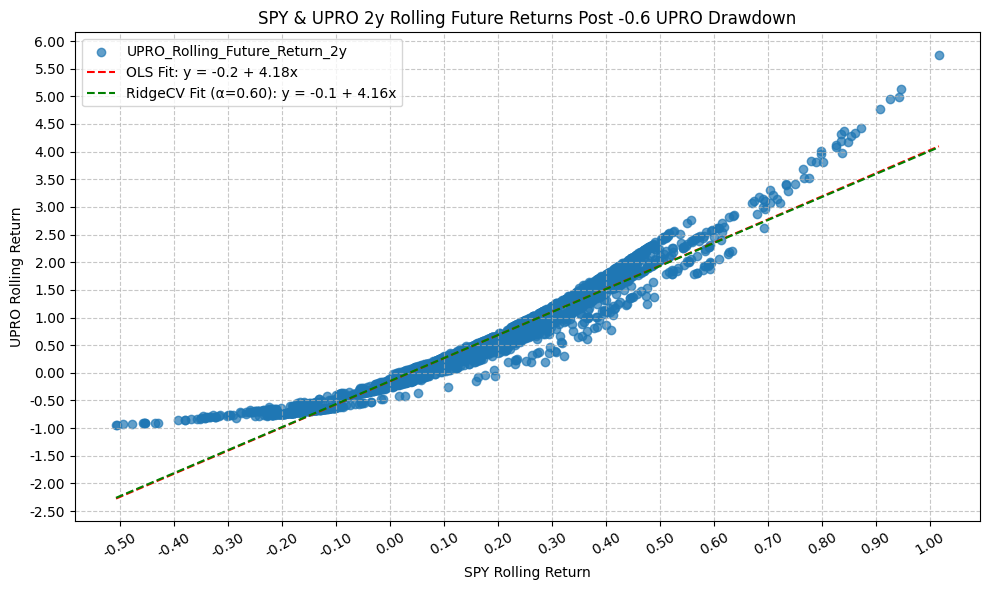

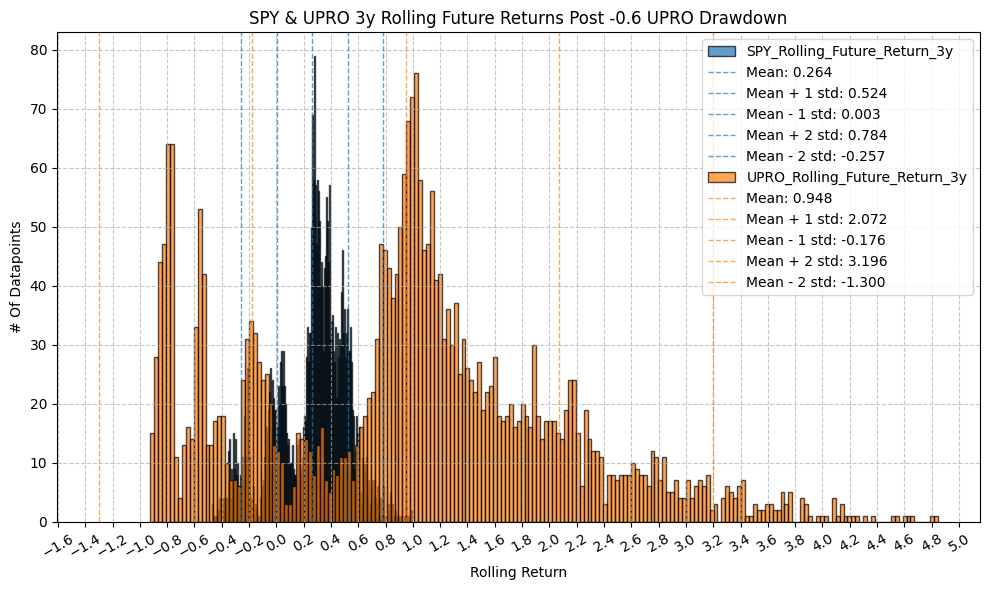

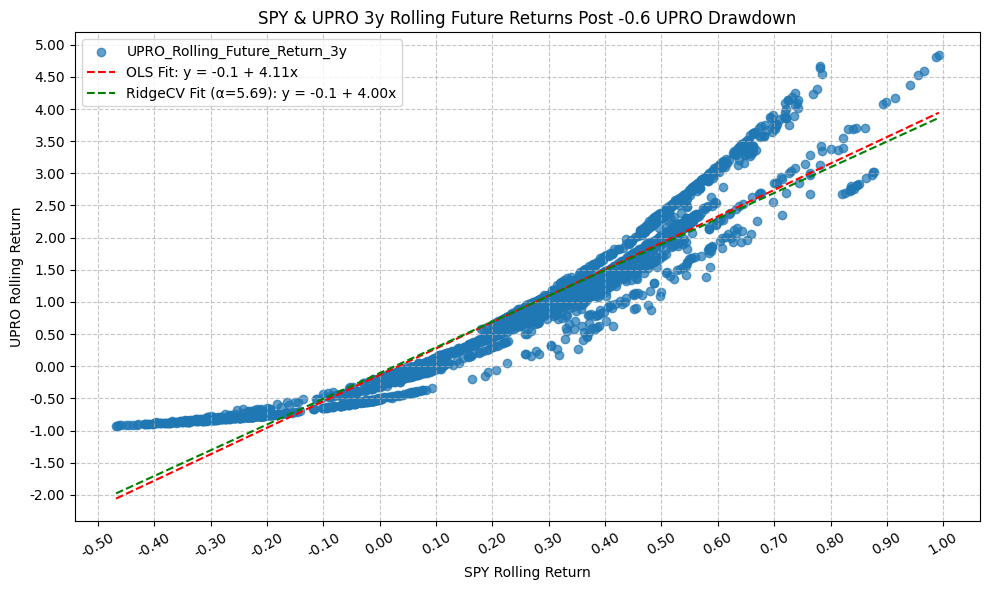

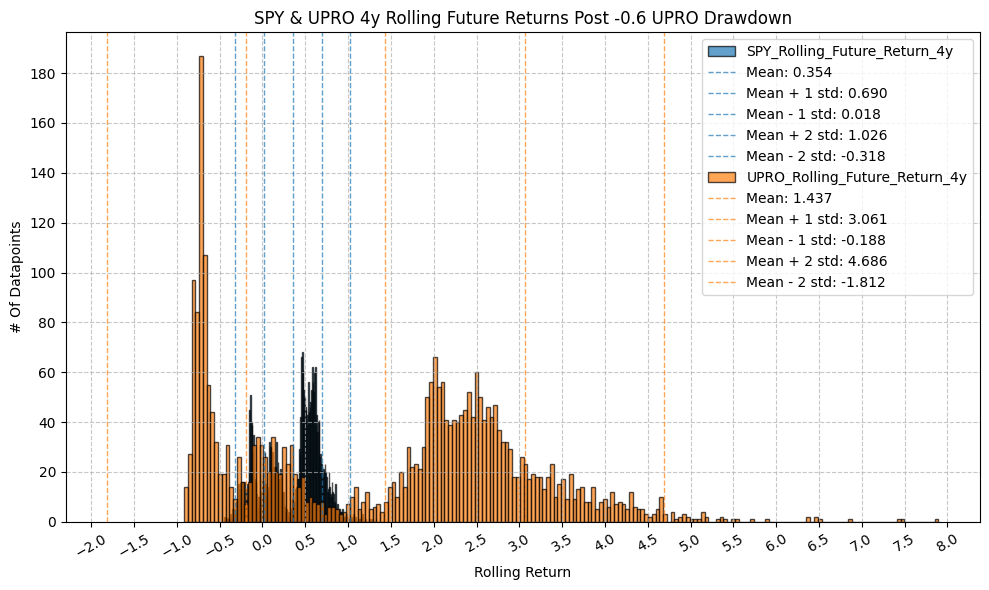

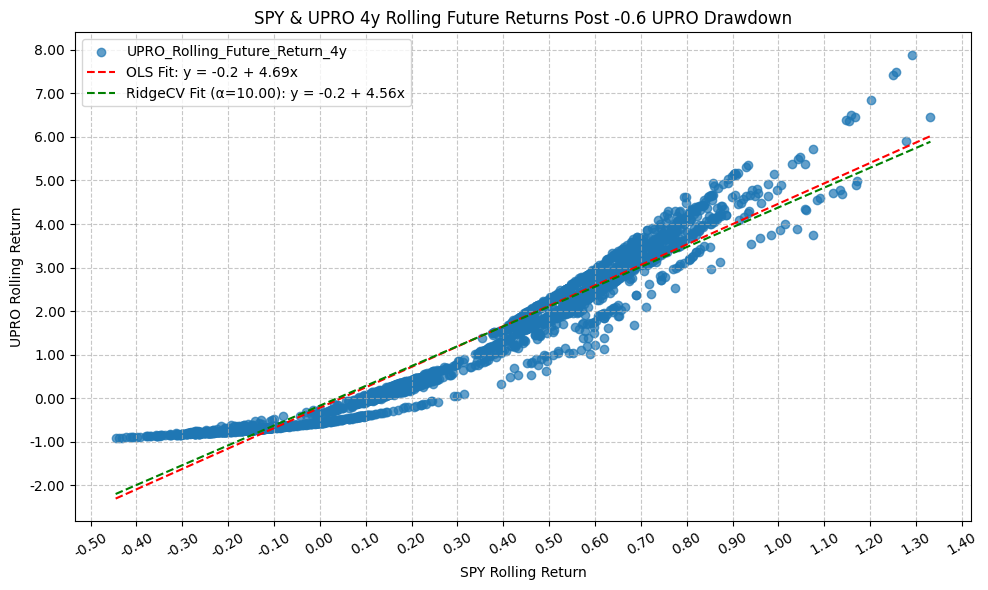

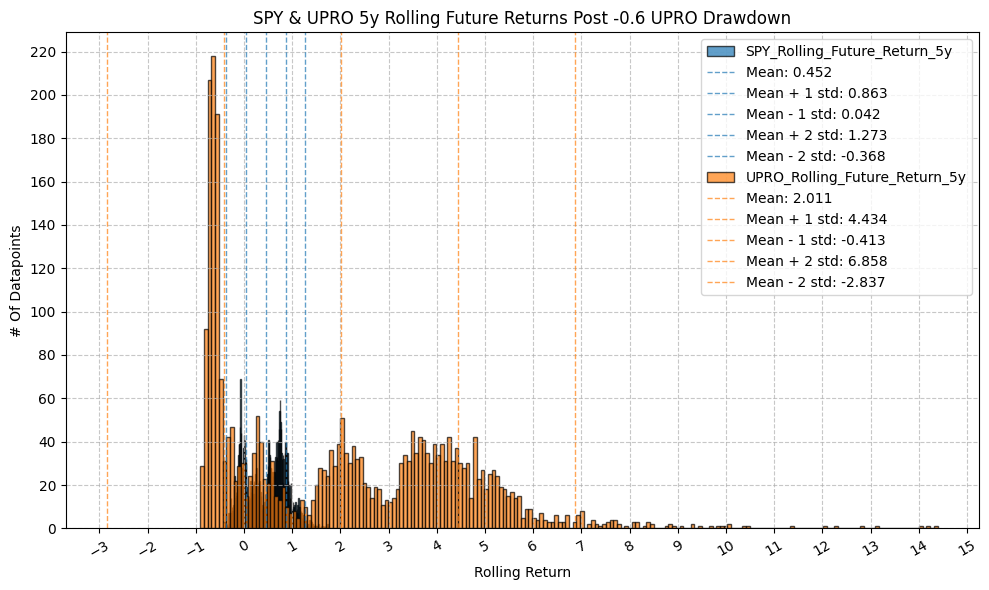

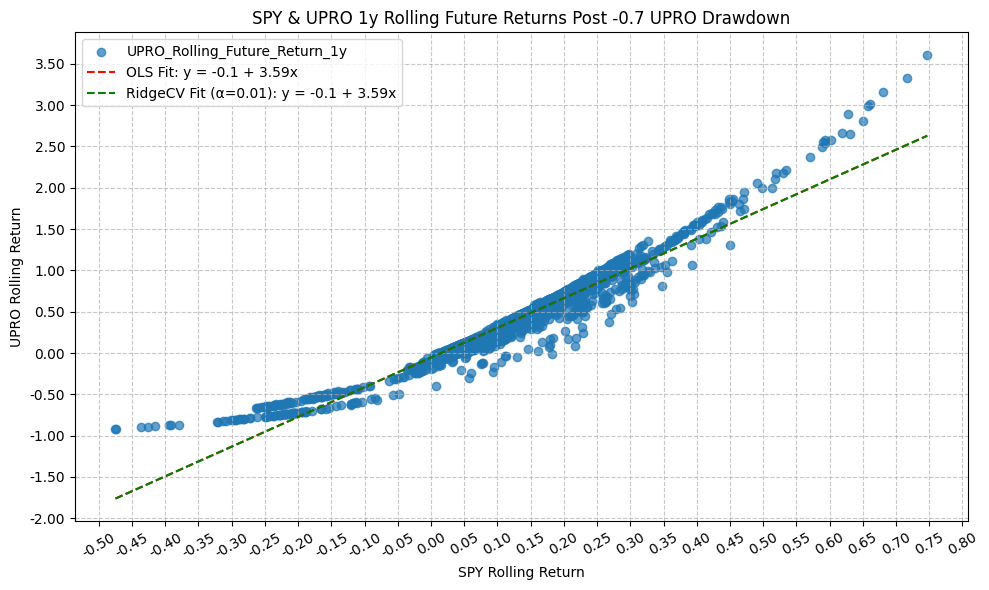

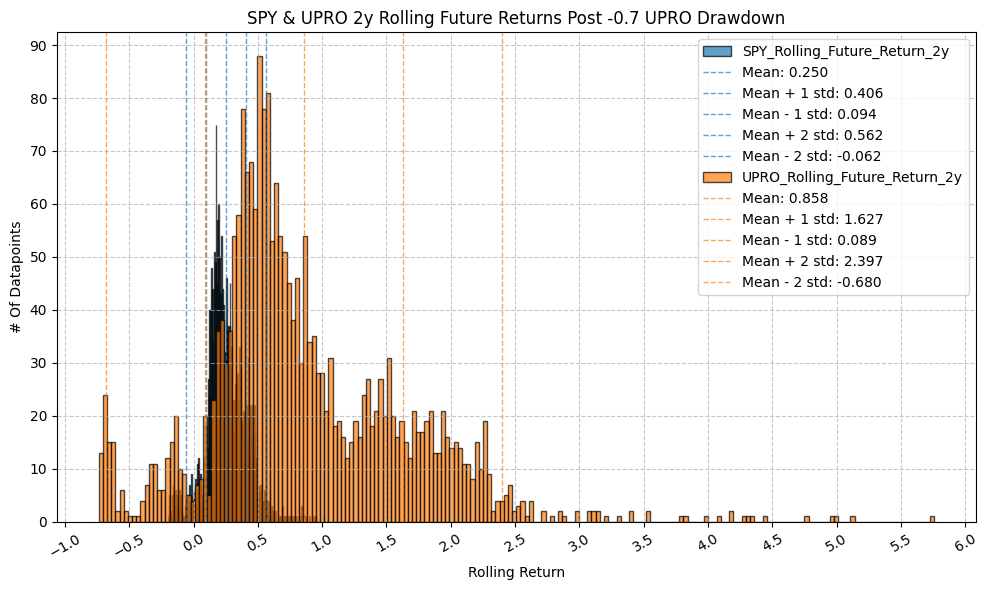

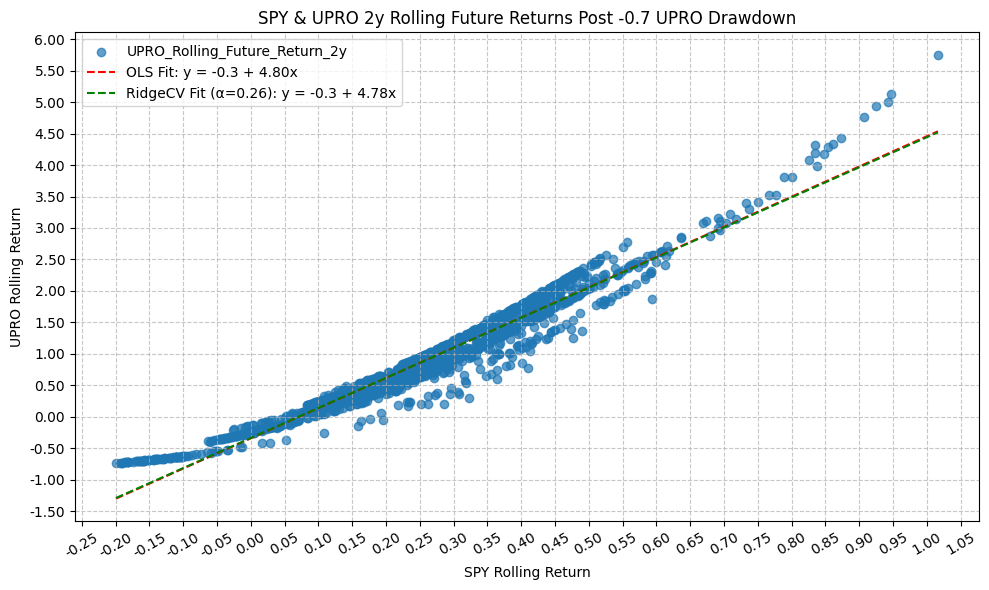

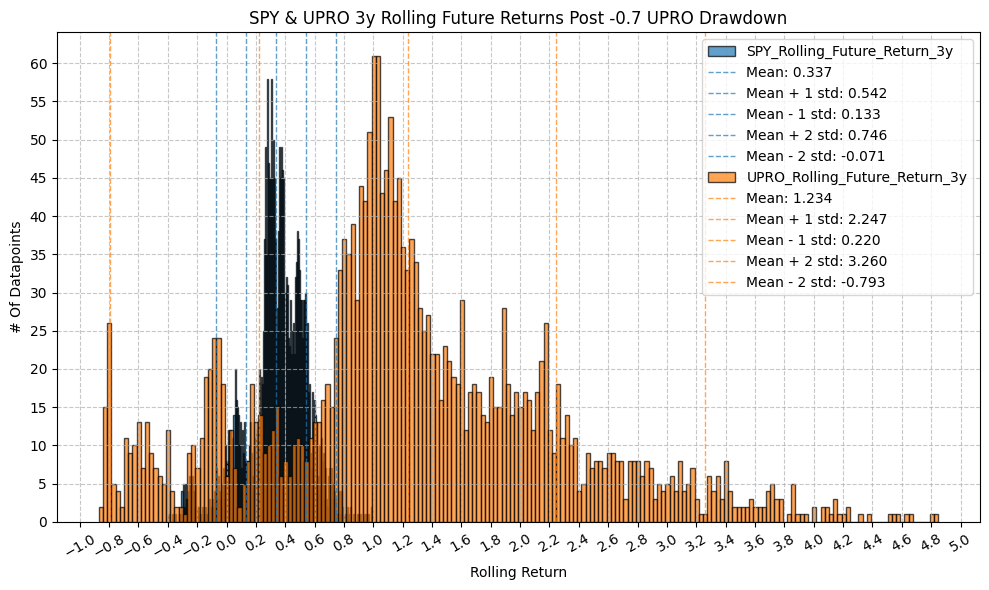

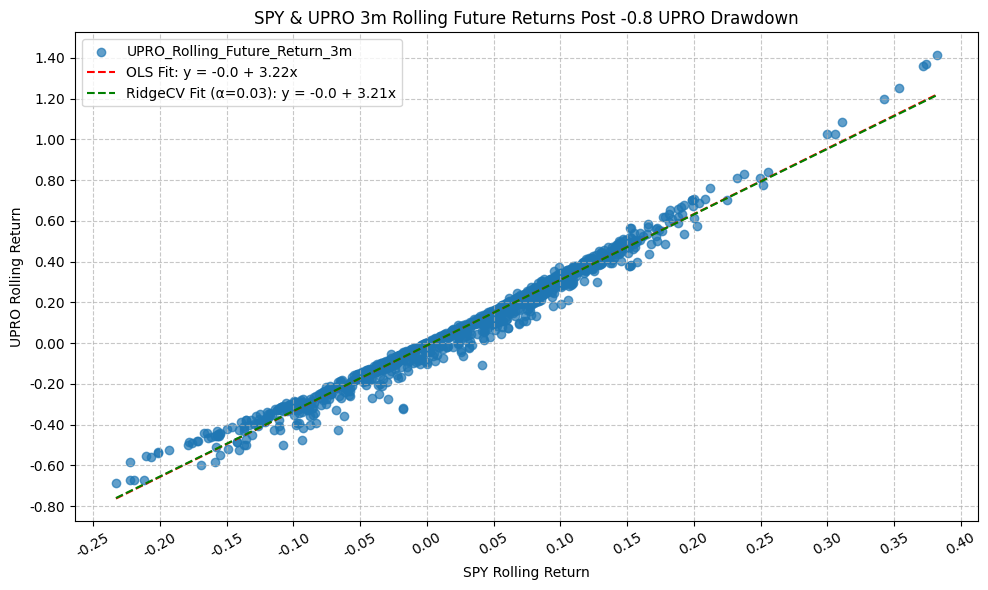

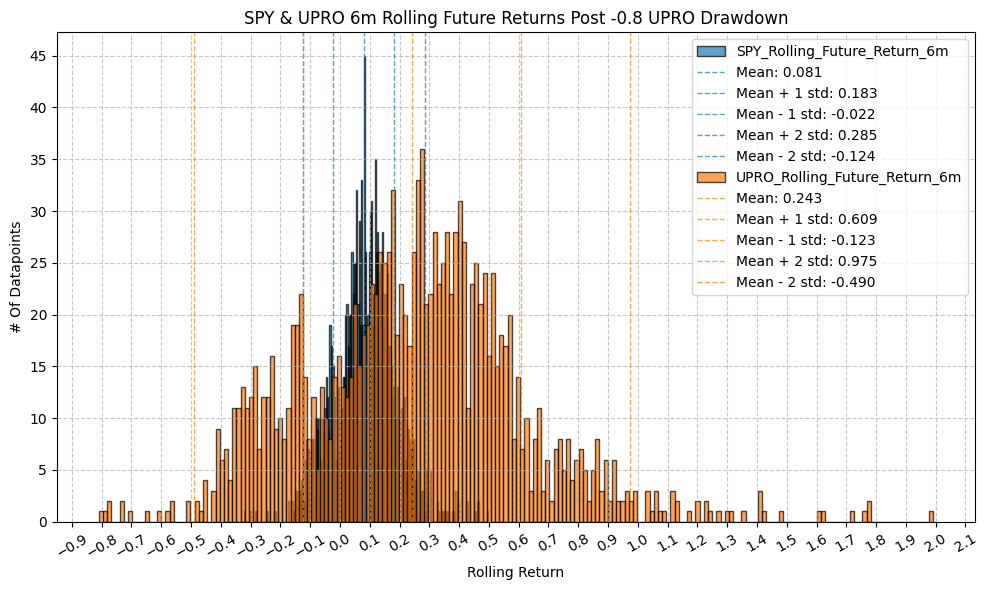

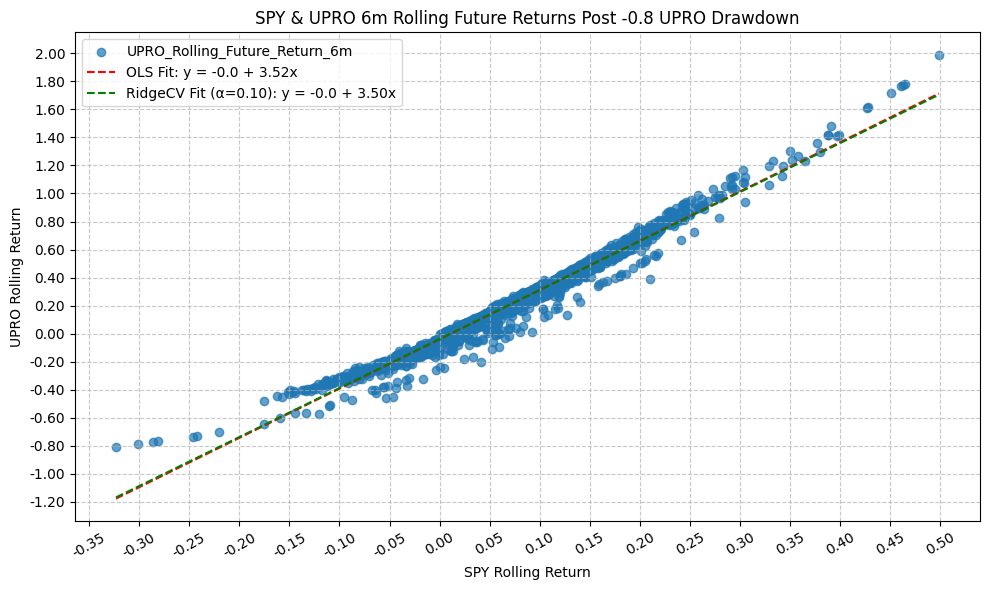

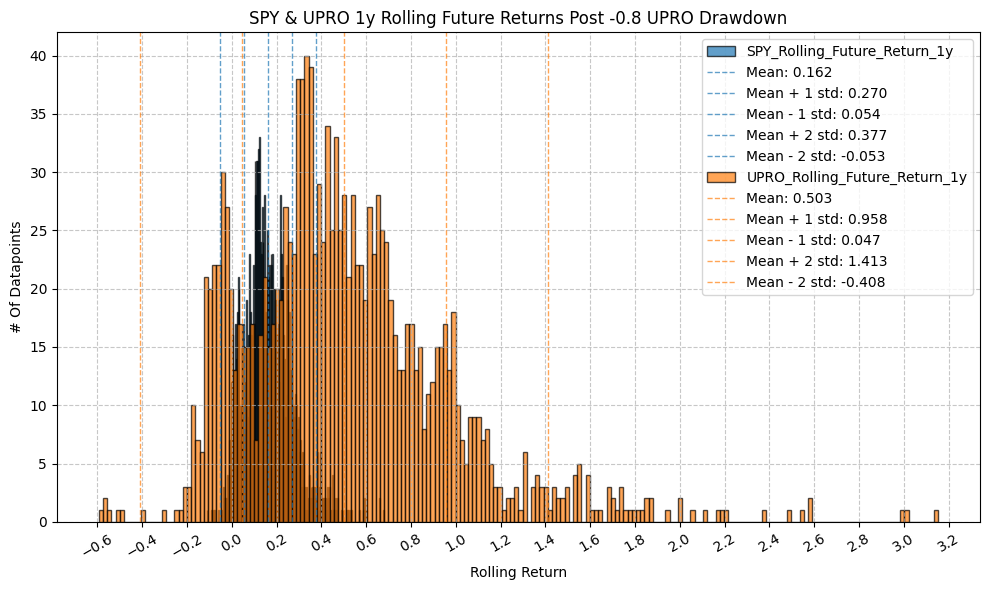

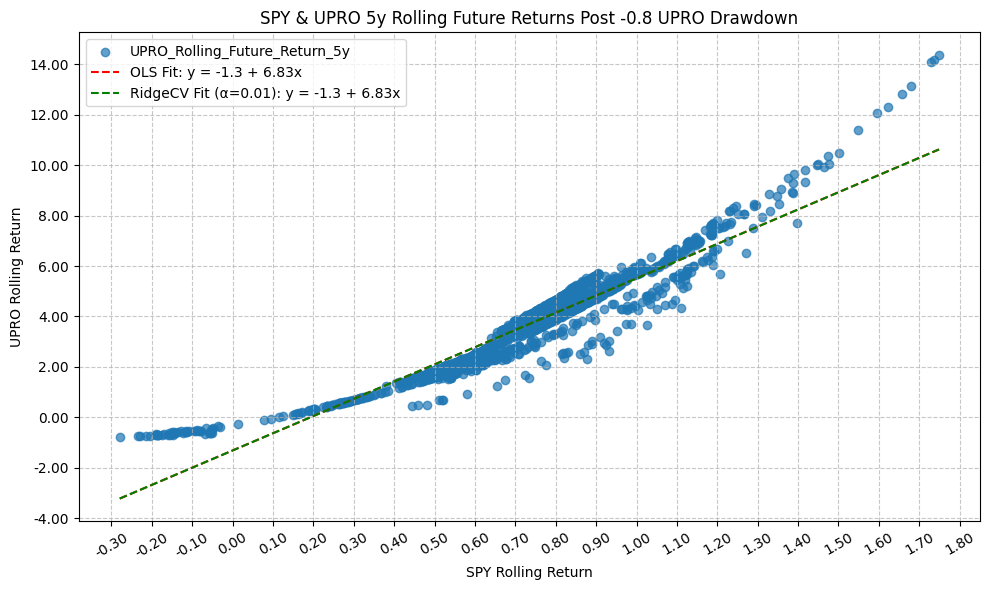

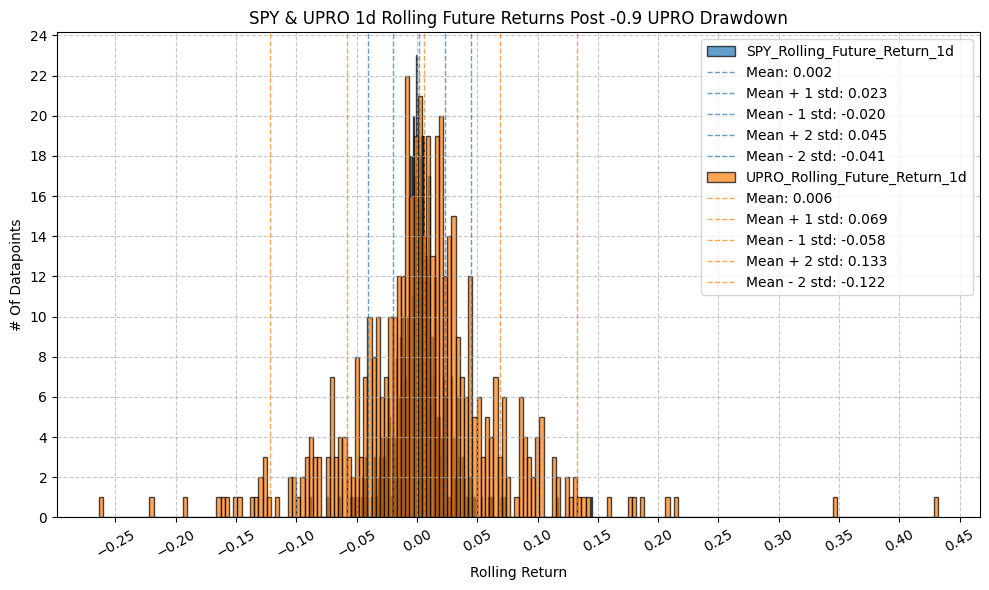

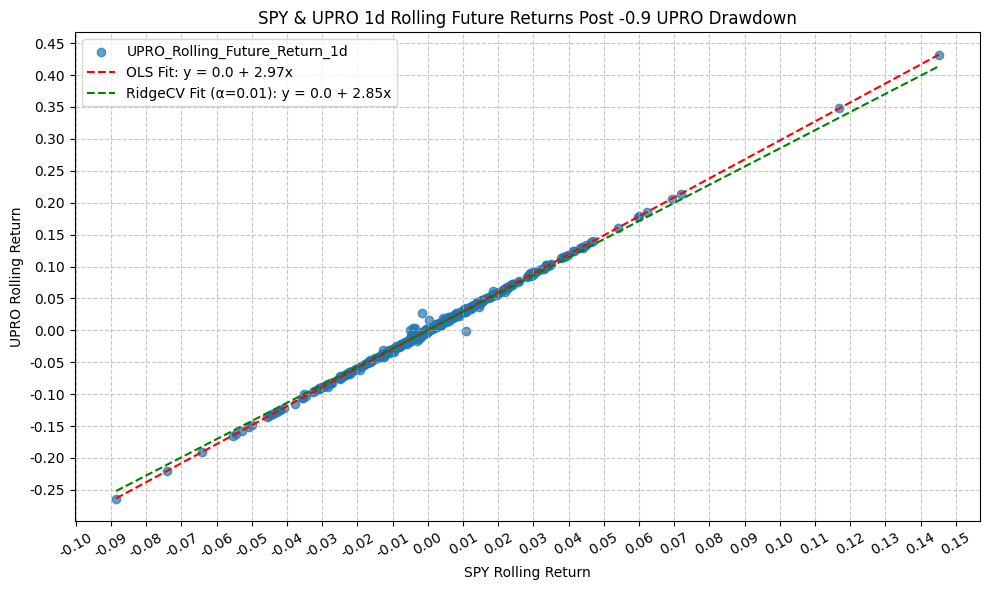

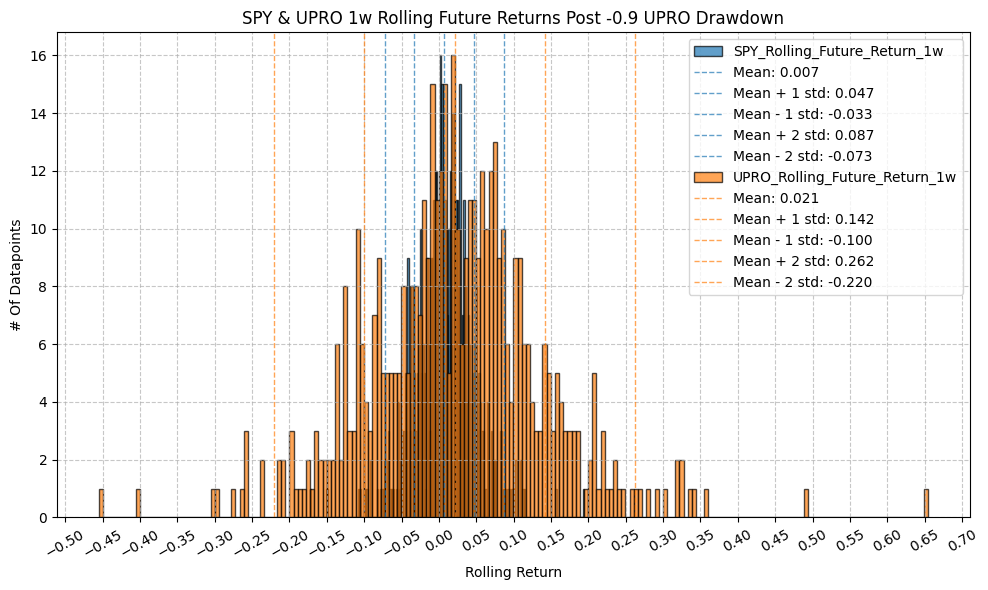

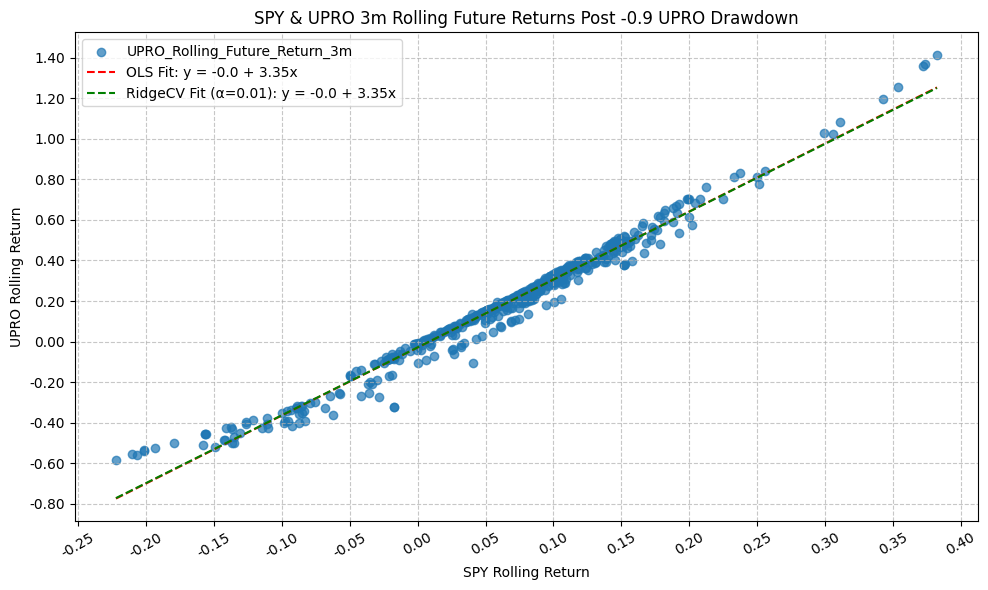

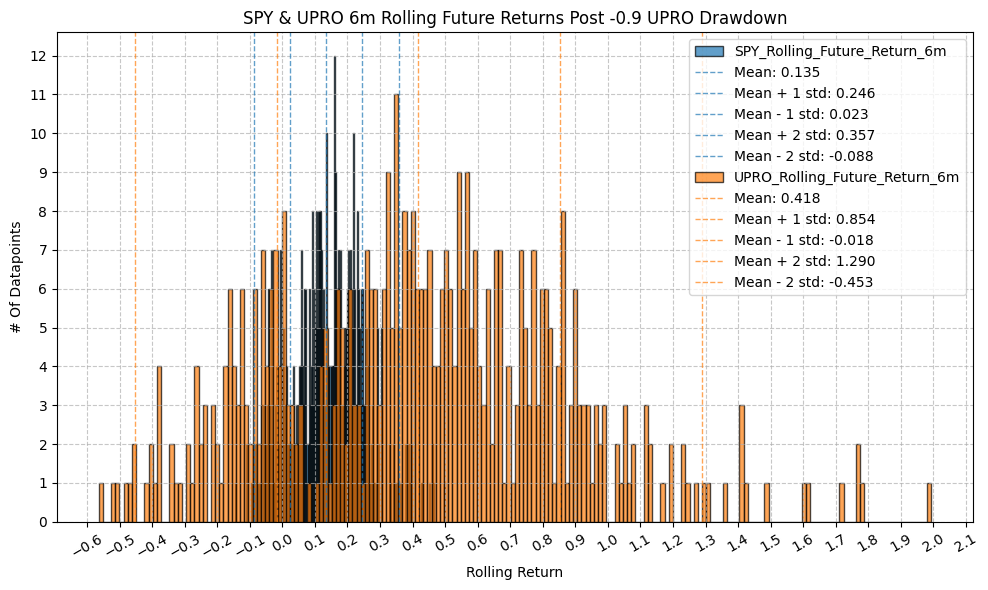

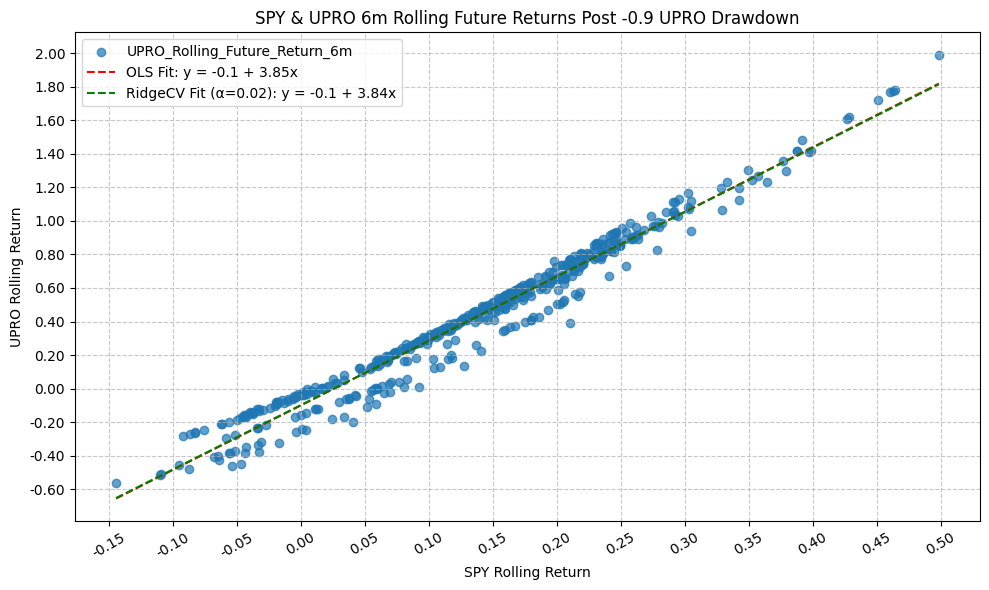

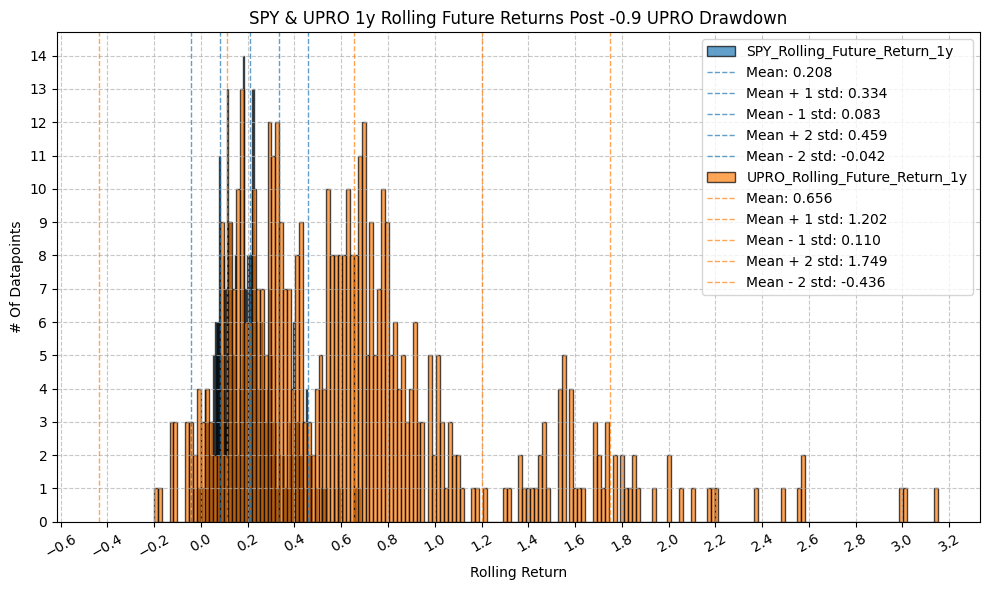

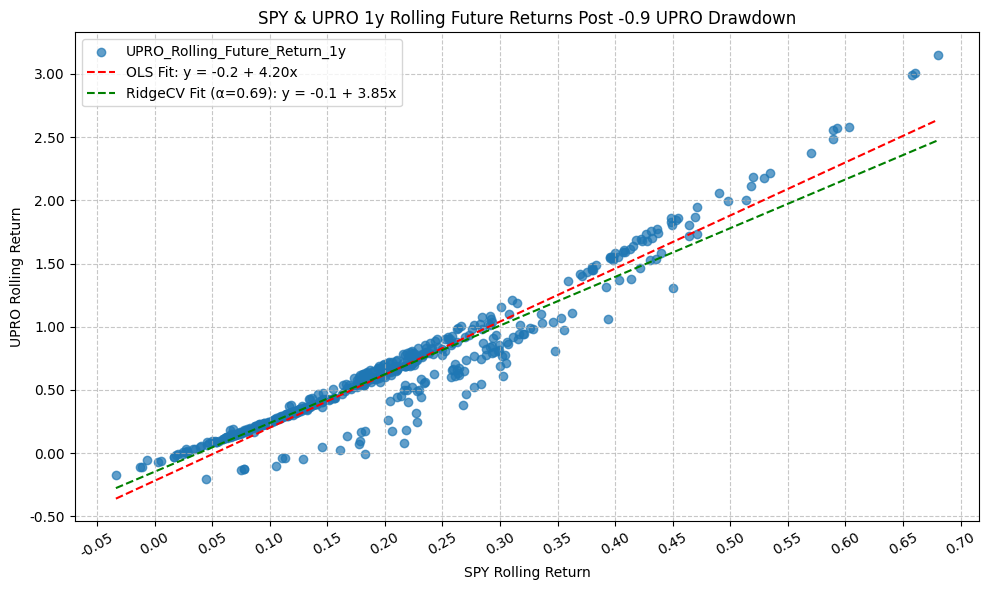

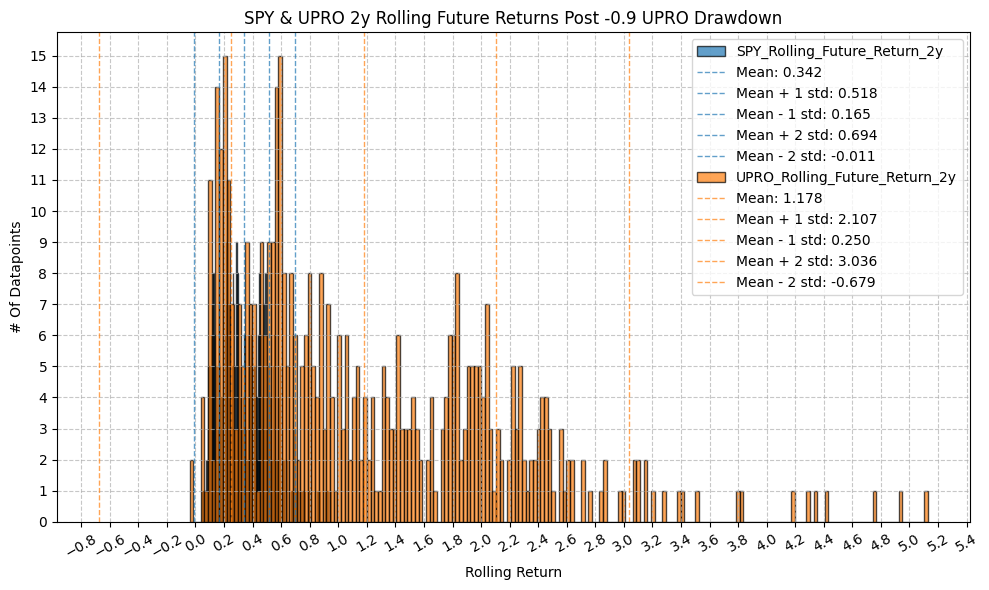

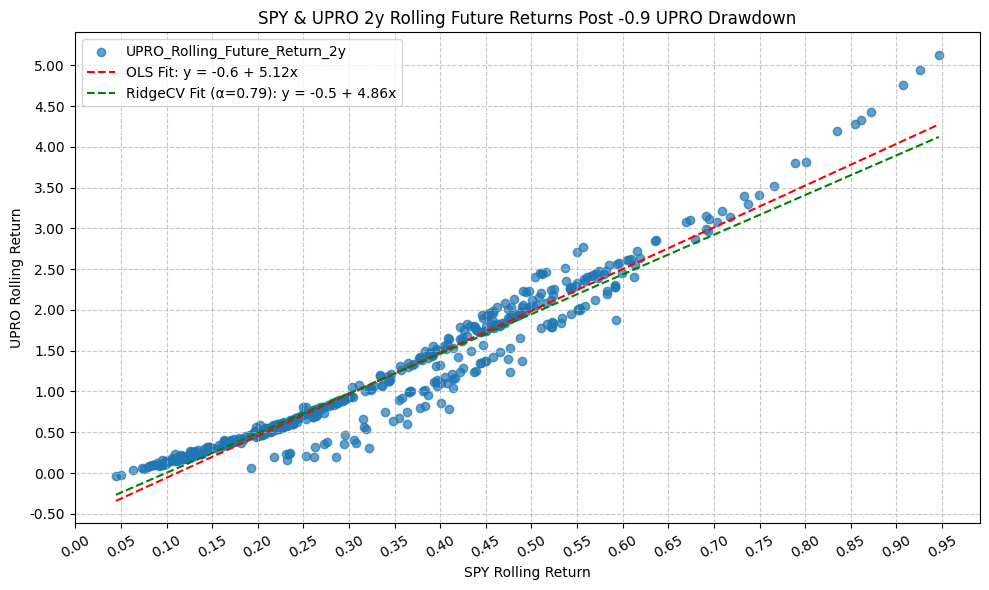

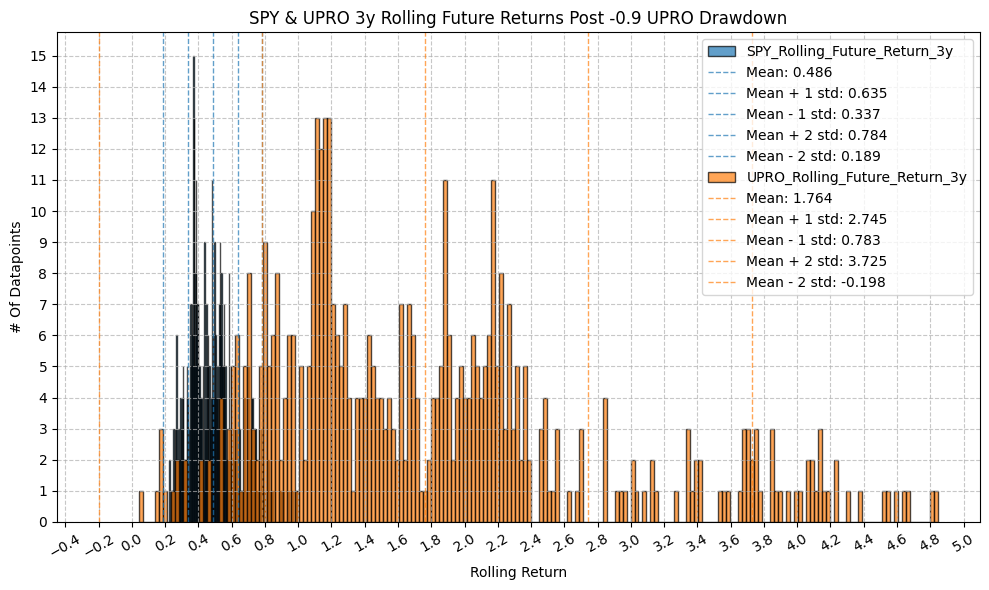

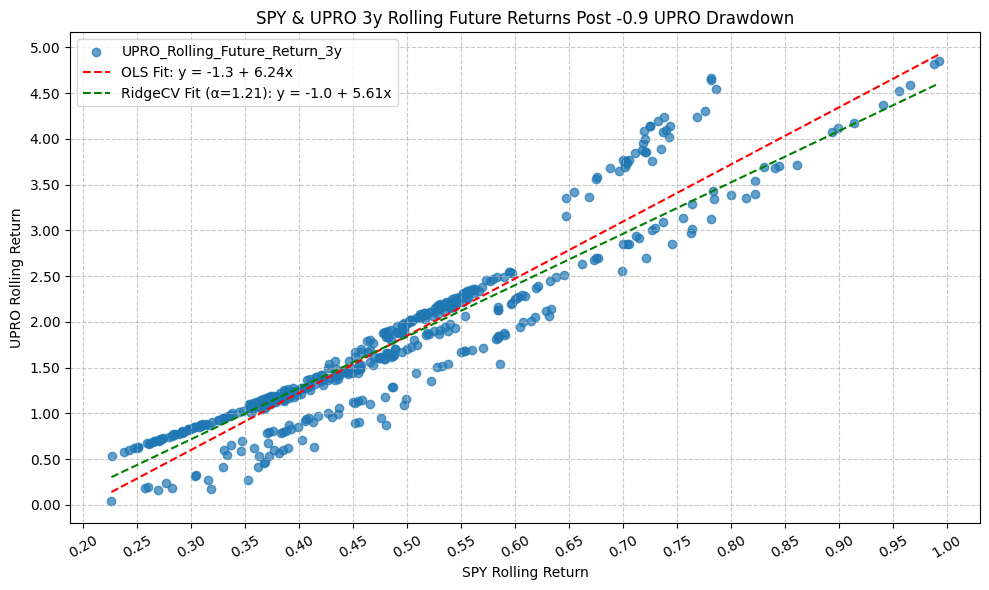

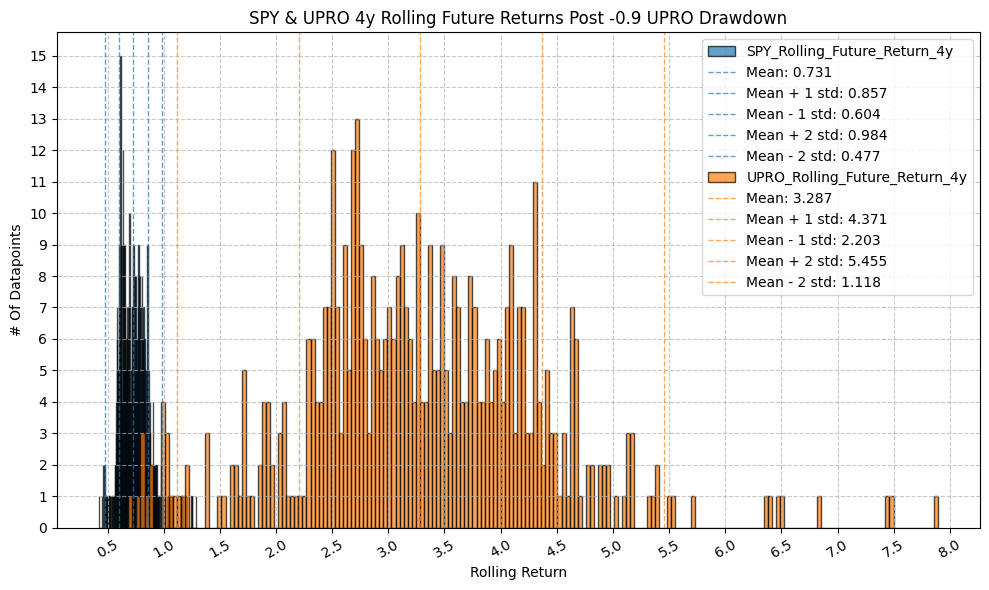

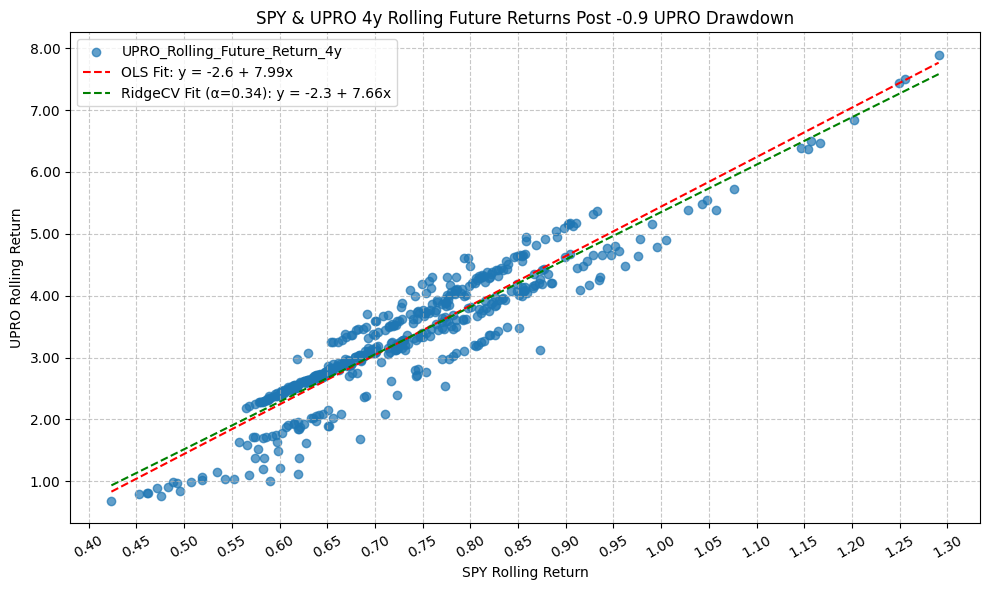

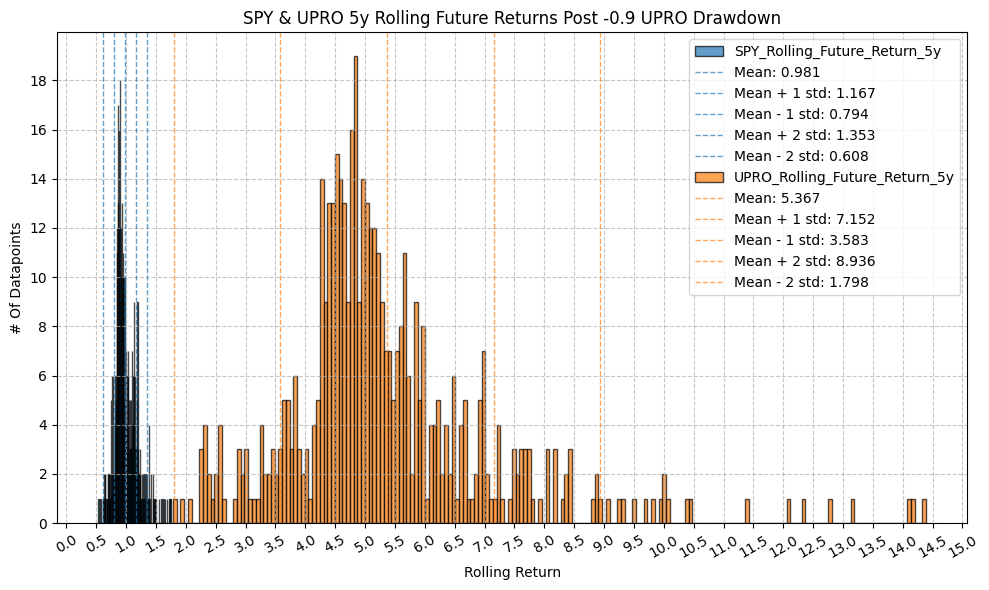

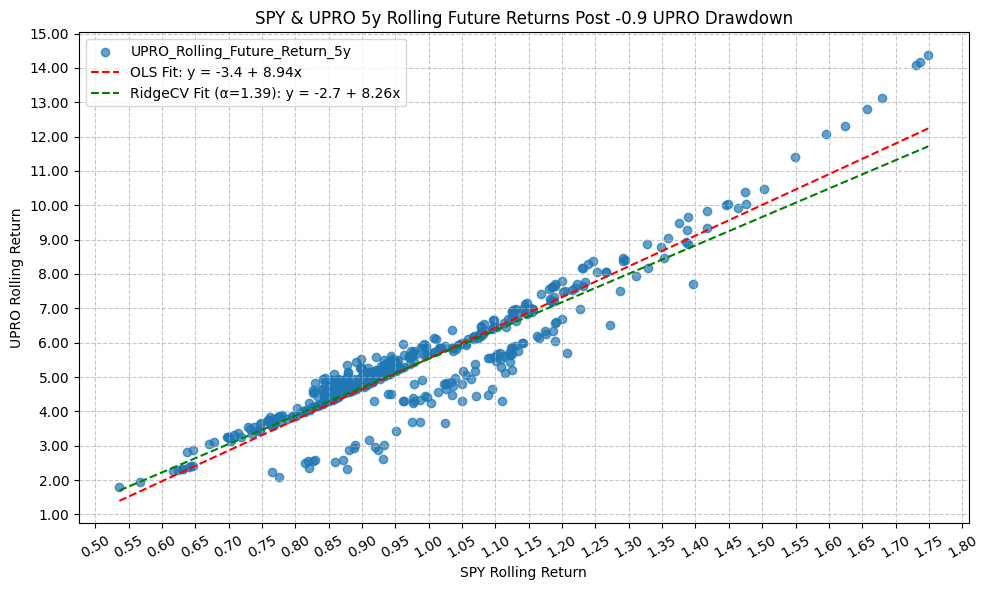

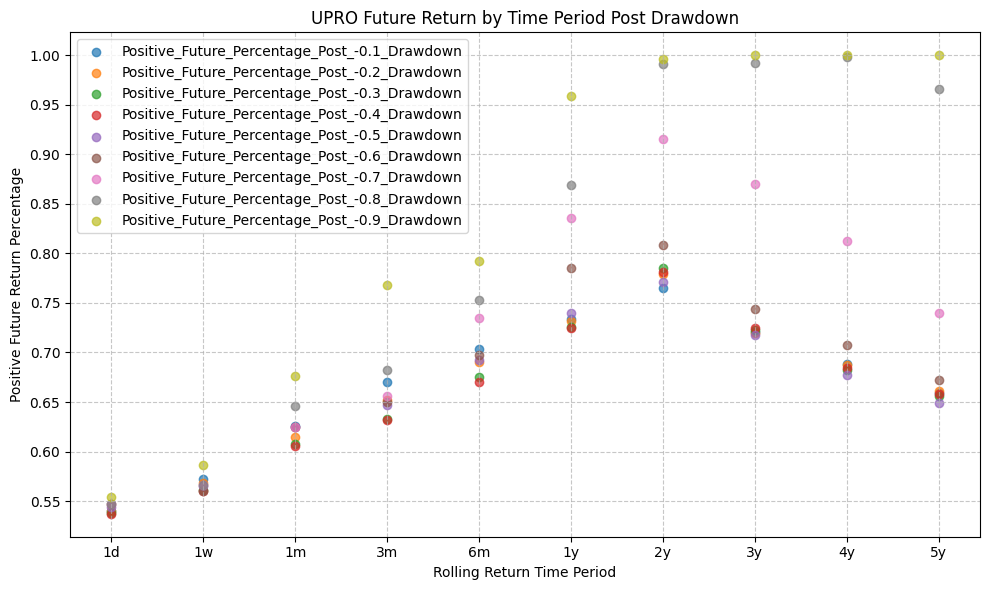

Rolling Returns Following Drawdowns (QQQ & TQQQ) #

We will identify the drawdown levels of TQQQ and then look at the subsequent rolling returns over various time horizons.

# Copy DataFrame

qqq_tqqq_extrap_future = qqq_tqqq_extrap.copy()

# Create a list of drawdown levels to analyze

drawdown_levels = [-0.10, -0.20, -0.30, -0.40, -0.50, -0.60, -0.70, -0.80, -0.90]

# Shift the rolling return columns by the number of days in the rolling window to get the returns following the drawdown

for etf in etfs:

for period_name, window in rolling_windows.items():

qqq_tqqq_extrap_future[f"{etf}_Rolling_Future_Return_{period_name}"] = qqq_tqqq_extrap_future[f"{etf}_Rolling_Return_{period_name}"].shift(-window)

Now, we can analyze the future rolling returns following specific drawdown levels:

# Create a dataframe to hold rolling returns stats

rolling_returns_drawdown_stats = pd.DataFrame()

for drawdown in drawdown_levels:

for period_name, window in rolling_windows.items():

try:

plot_histogram(

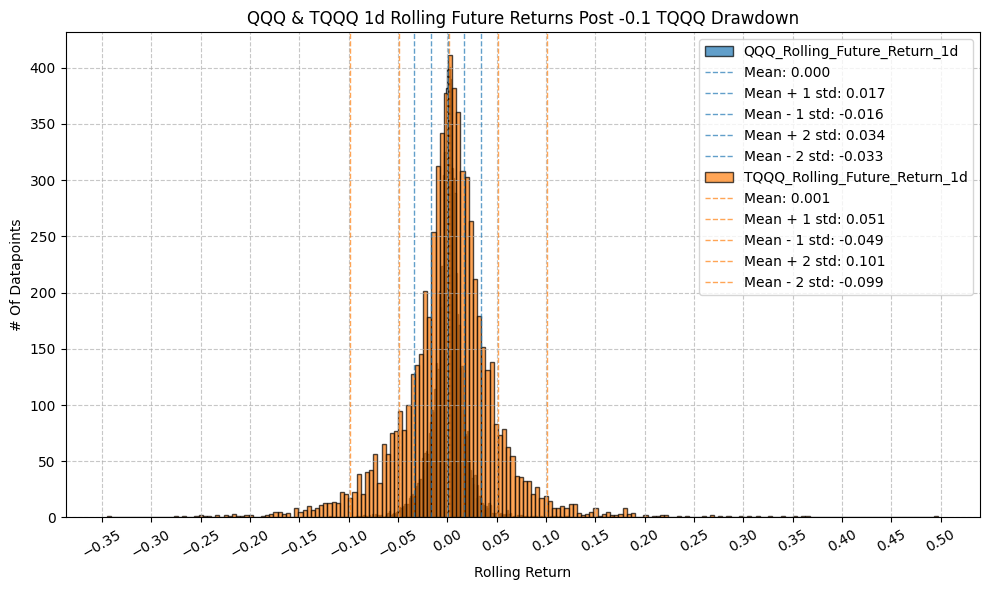

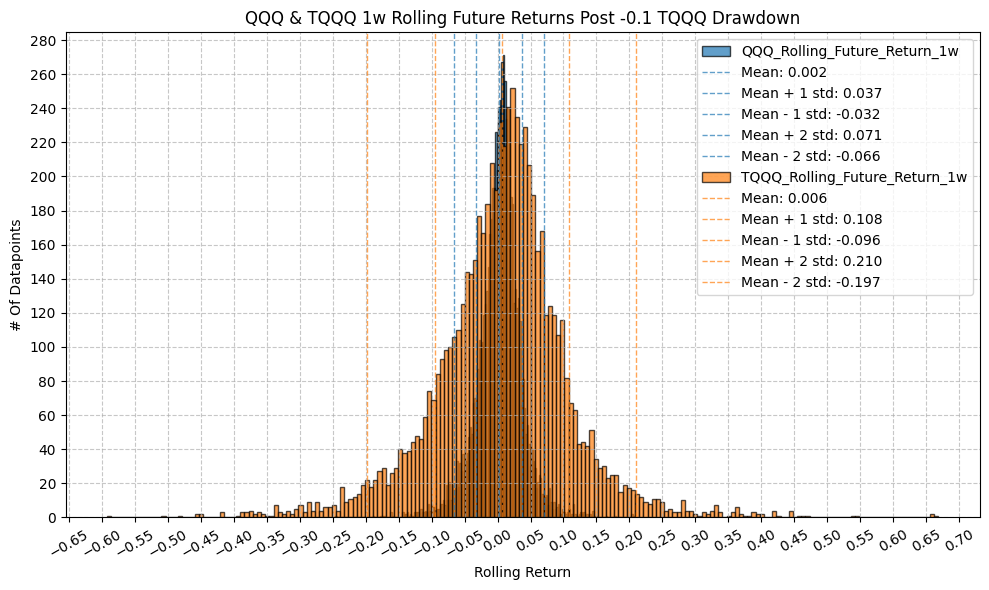

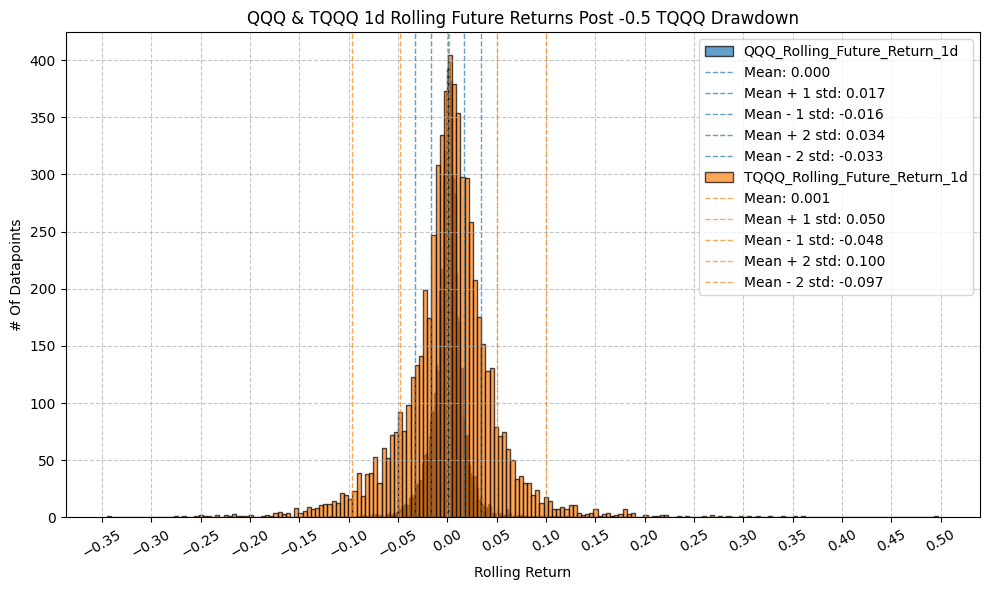

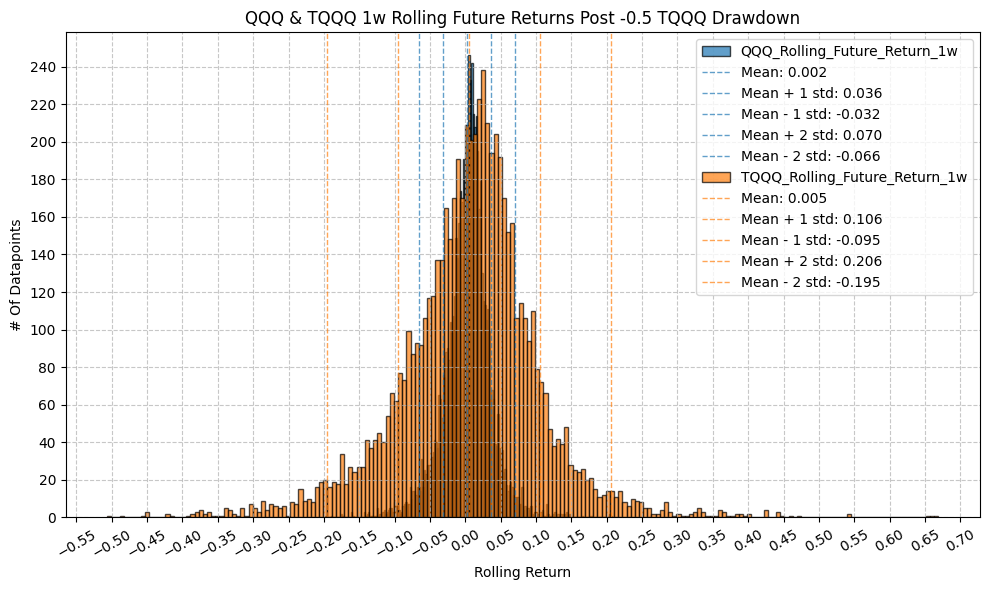

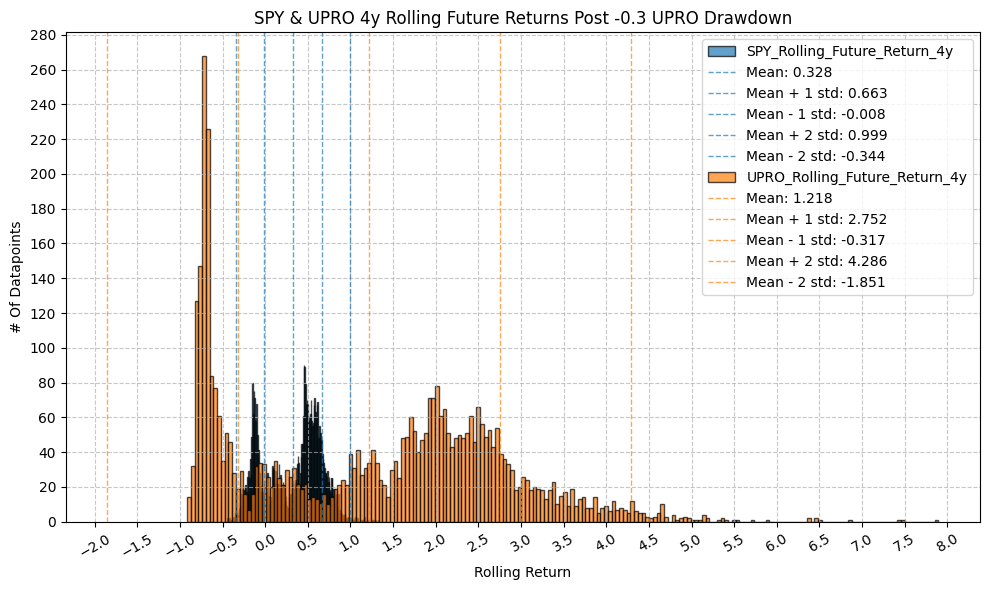

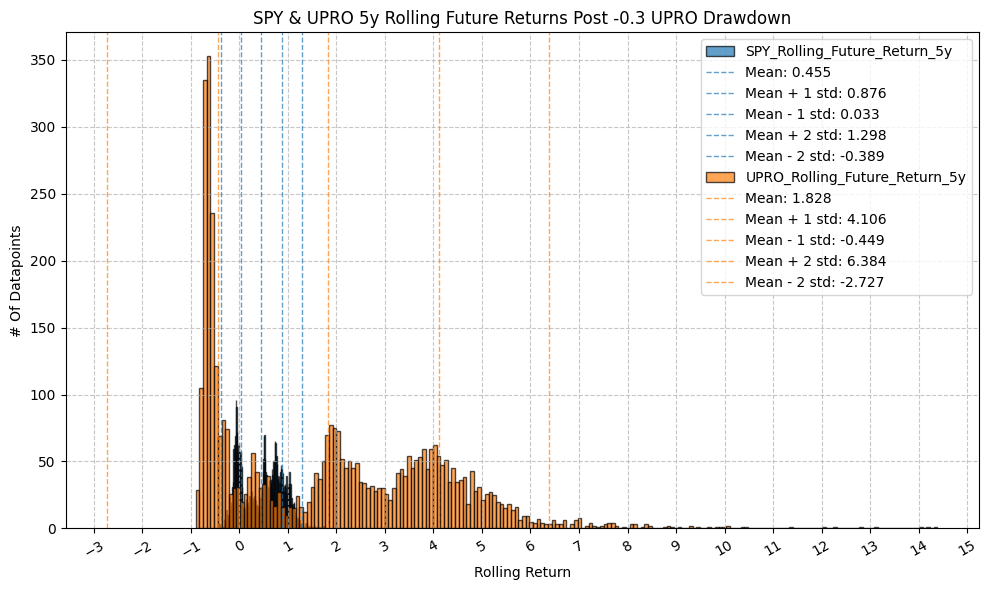

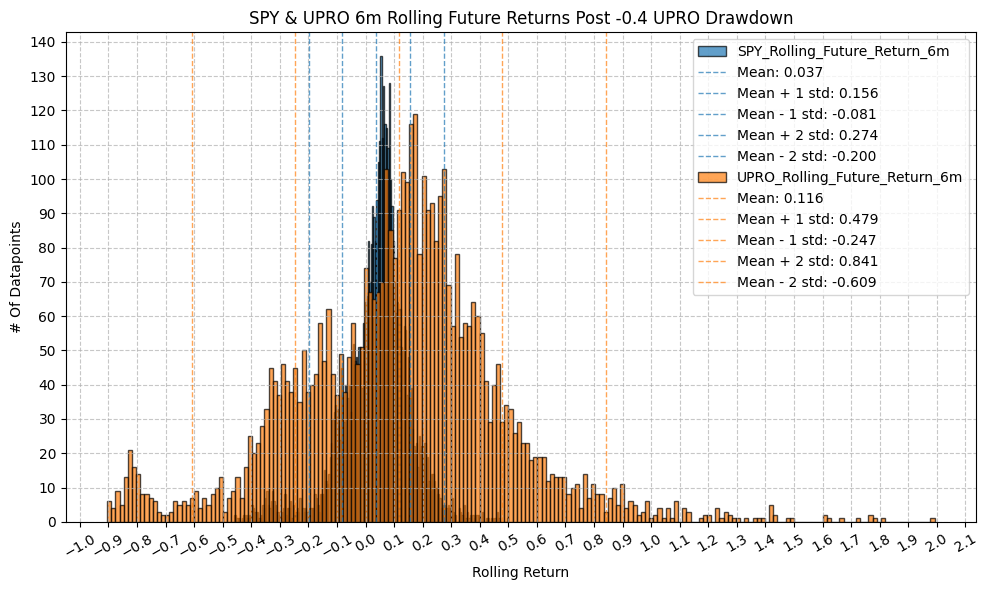

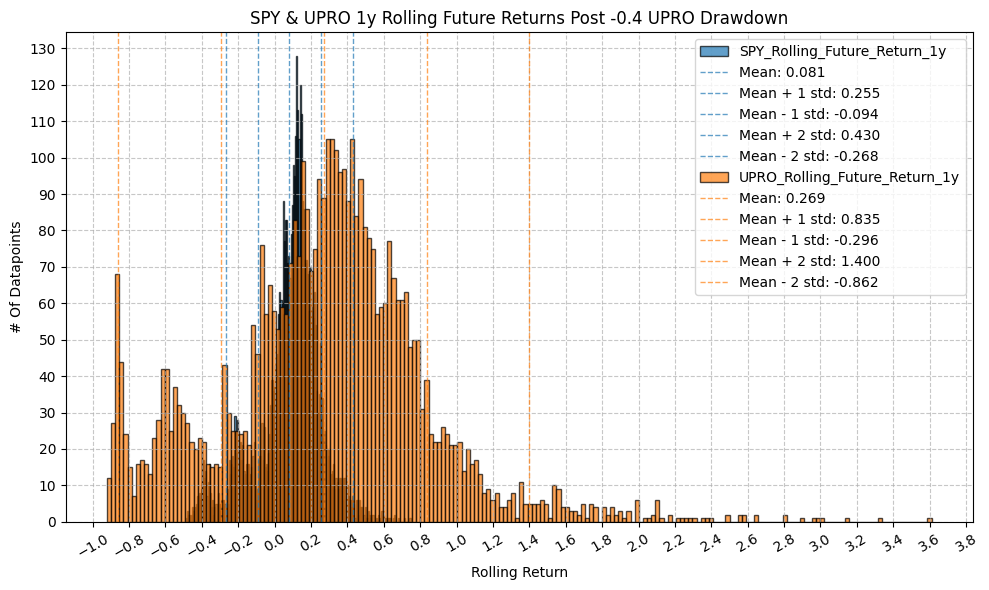

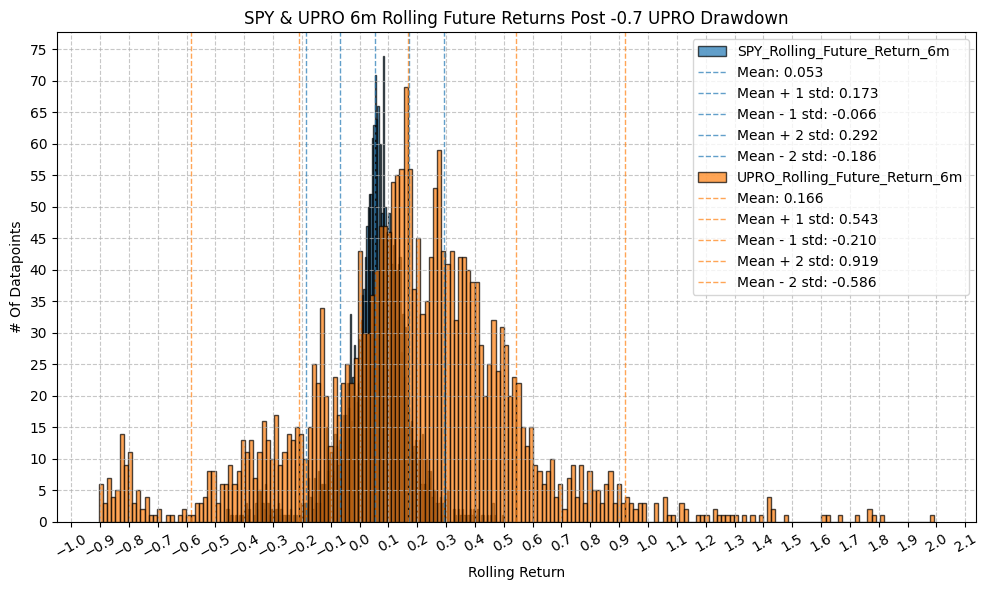

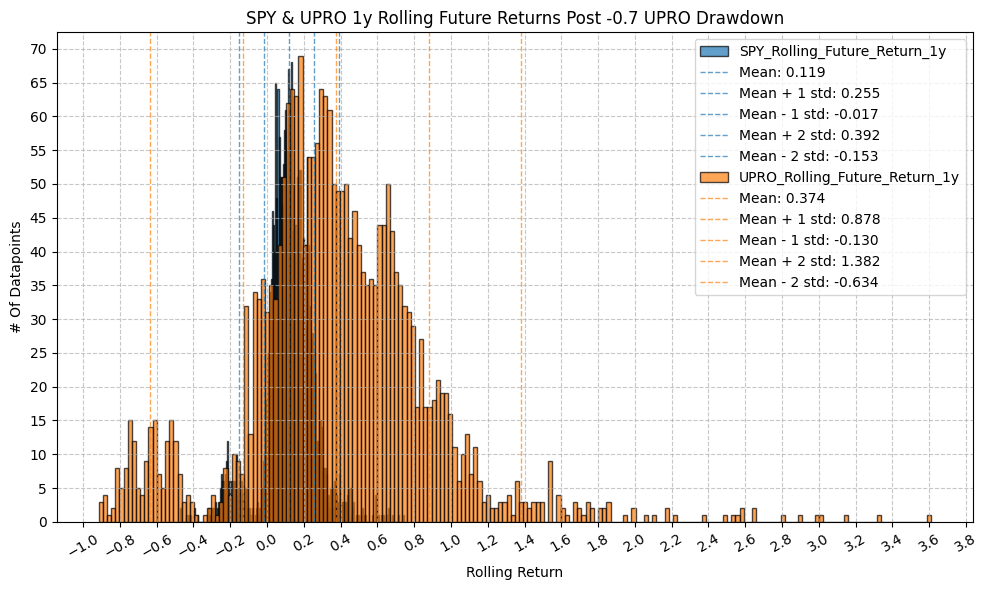

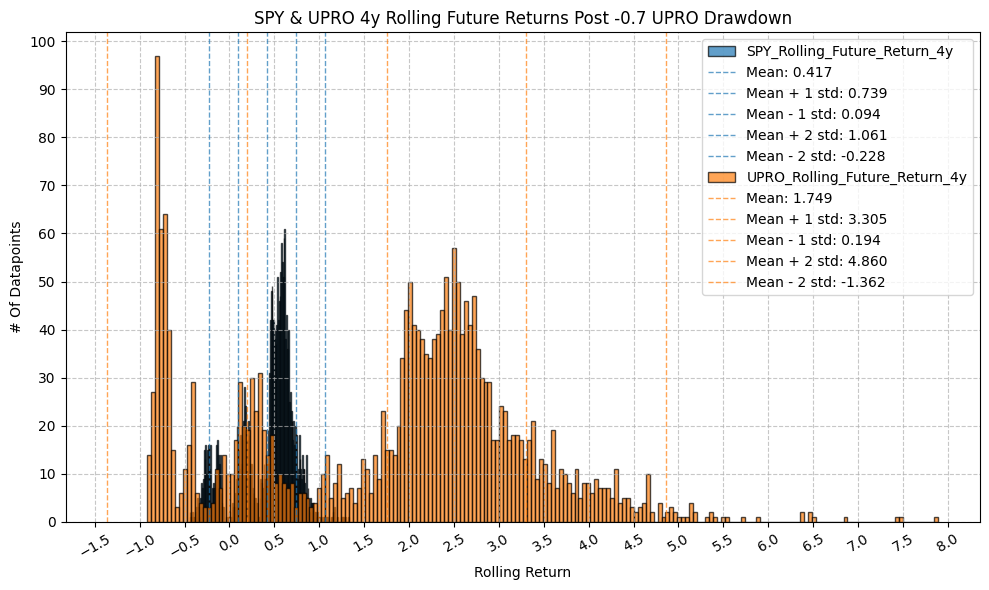

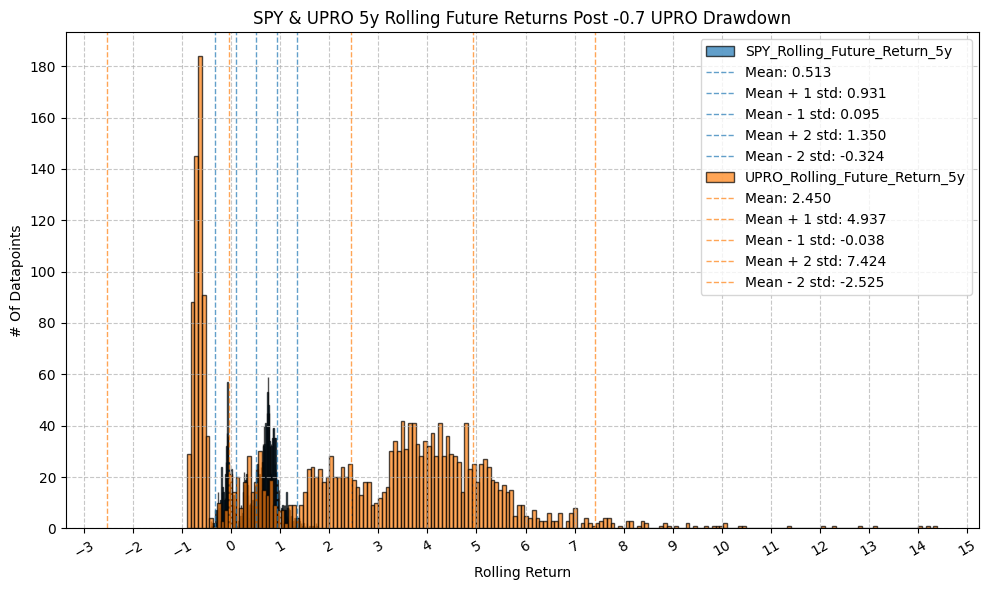

df=qqq_tqqq_extrap_future[qqq_tqqq_extrap_future["TQQQ_Drawdown"] <= drawdown],

plot_columns=[f"QQQ_Rolling_Future_Return_{period_name}", f"TQQQ_Rolling_Future_Return_{period_name}"],

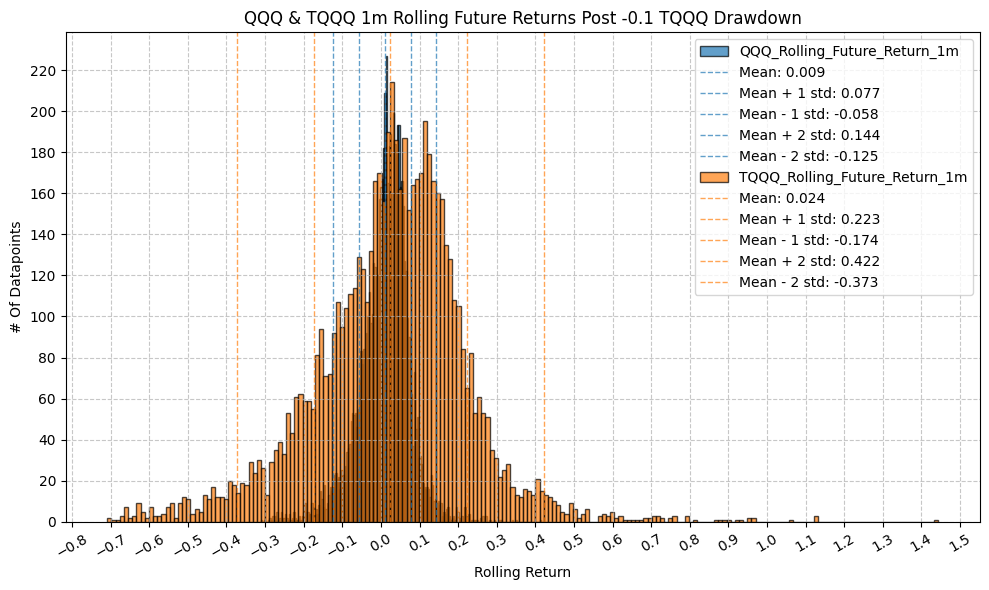

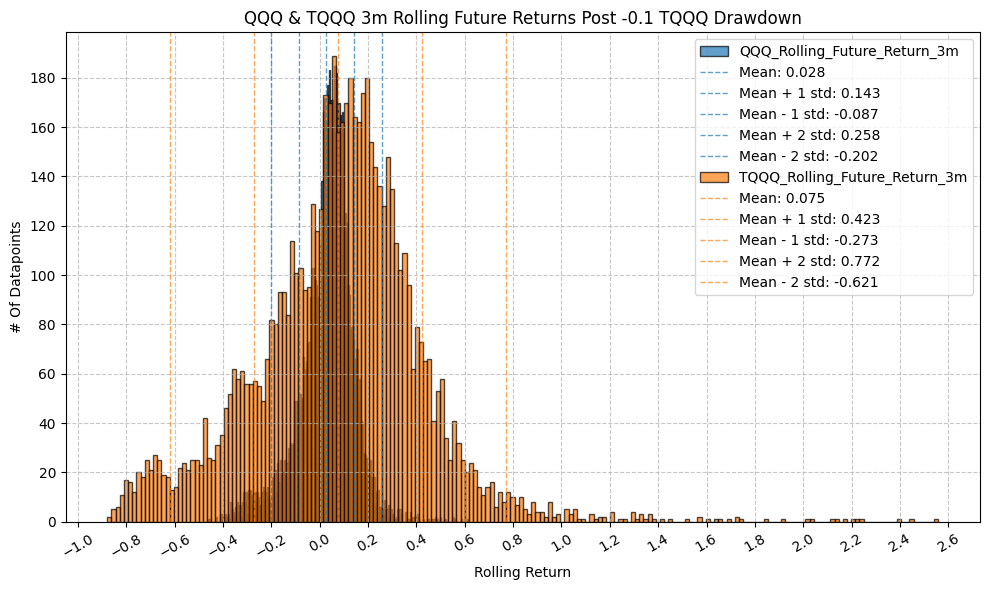

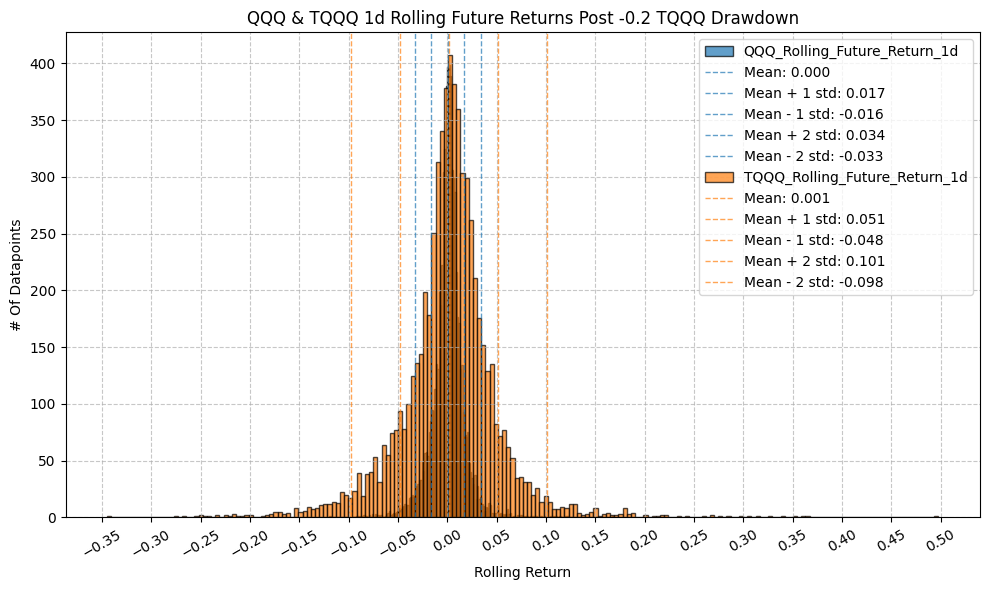

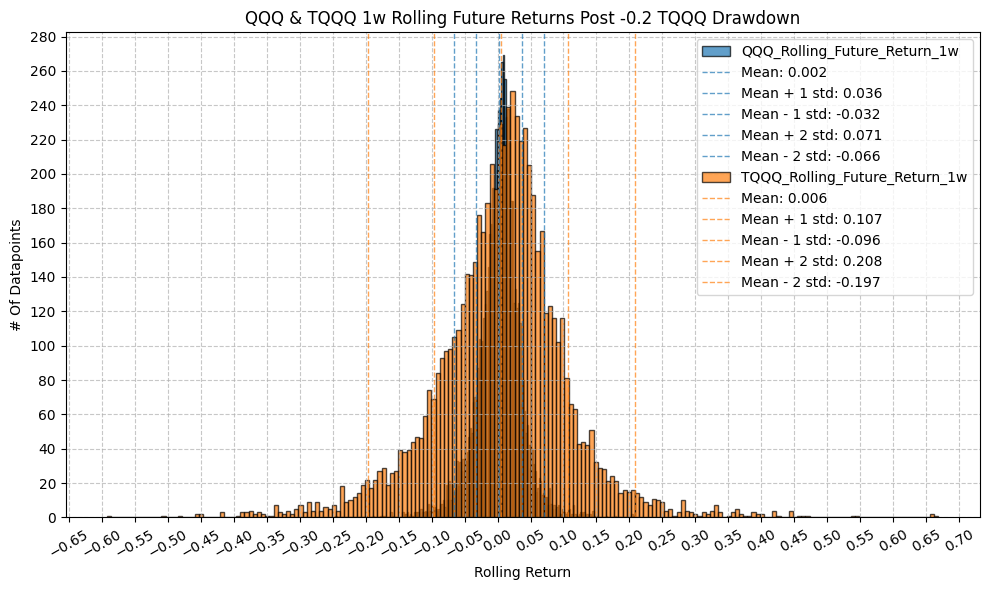

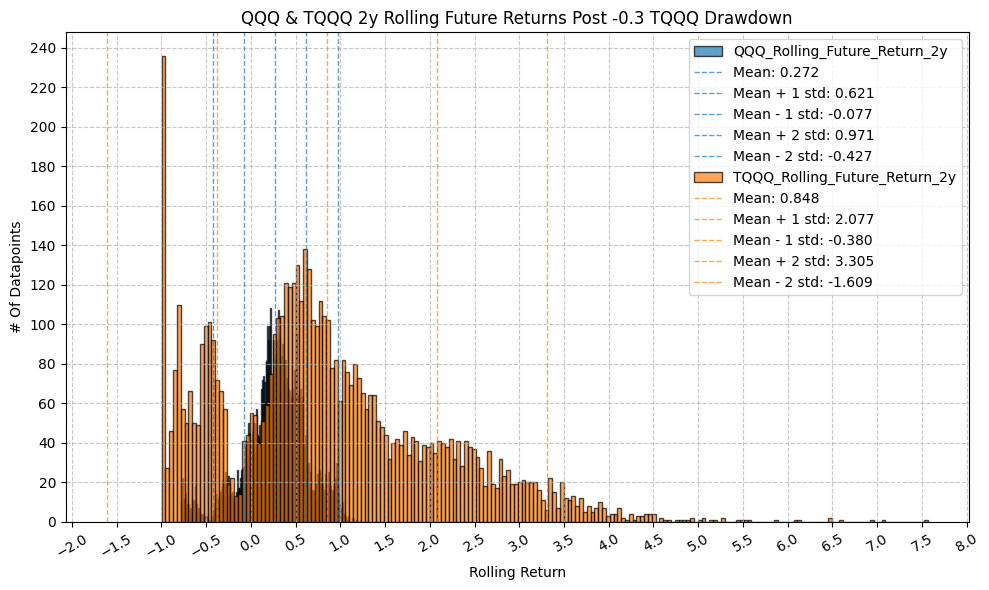

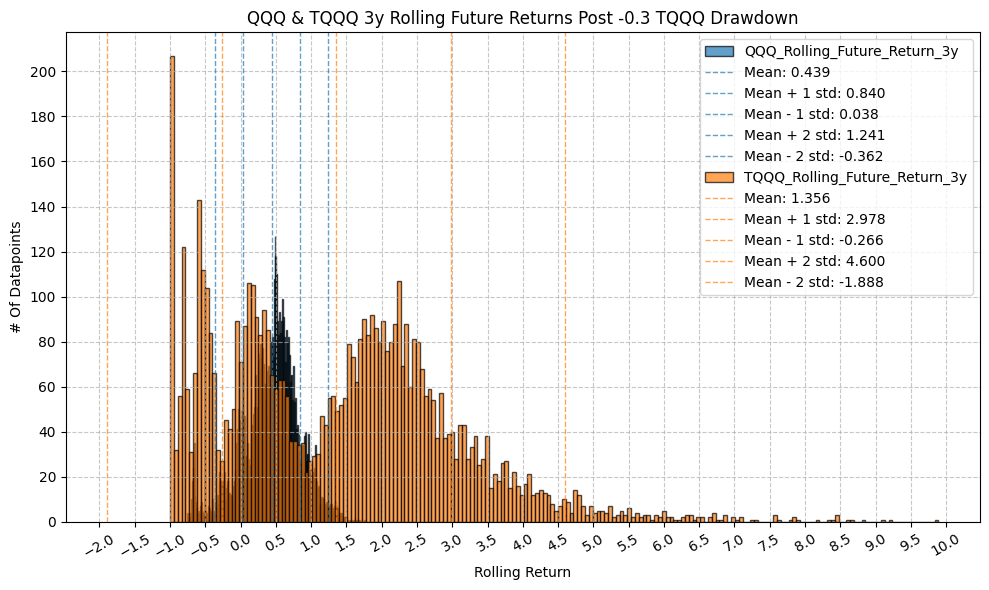

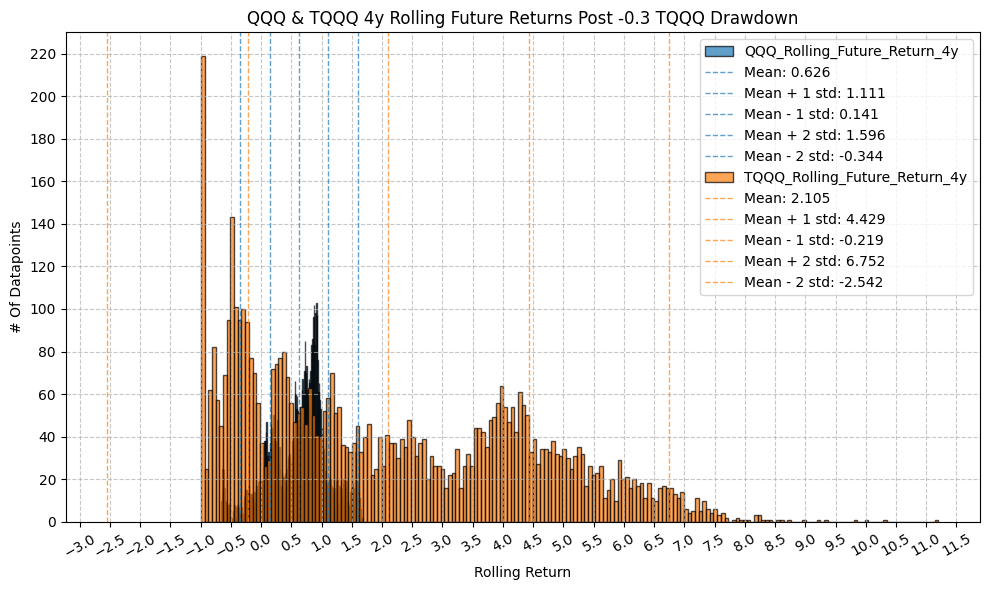

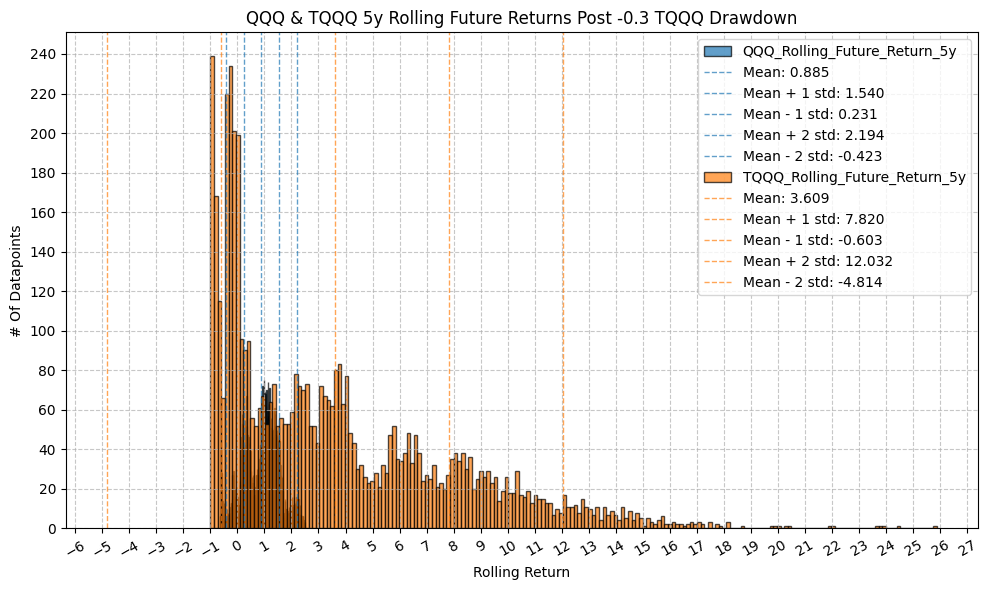

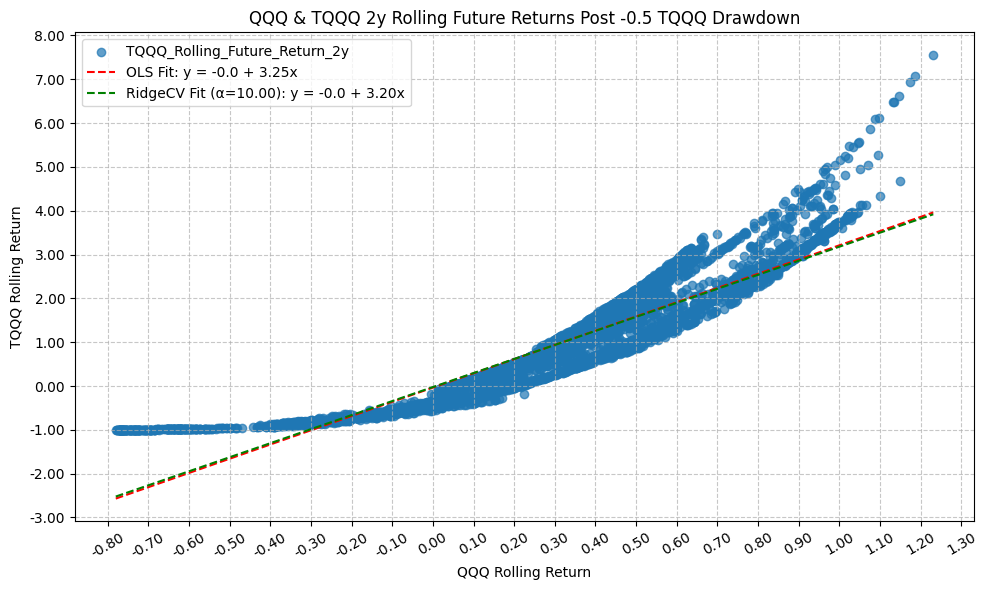

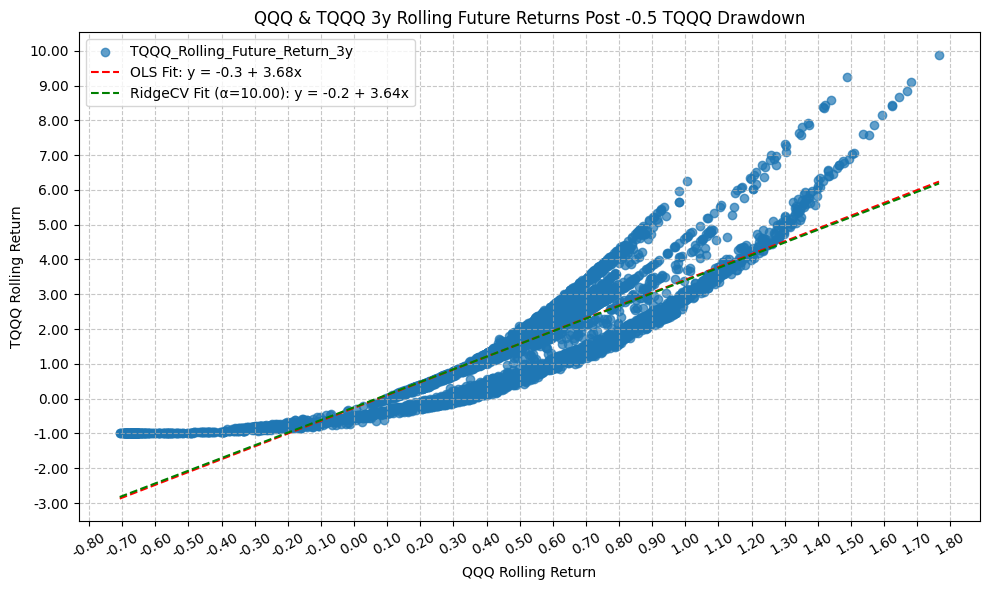

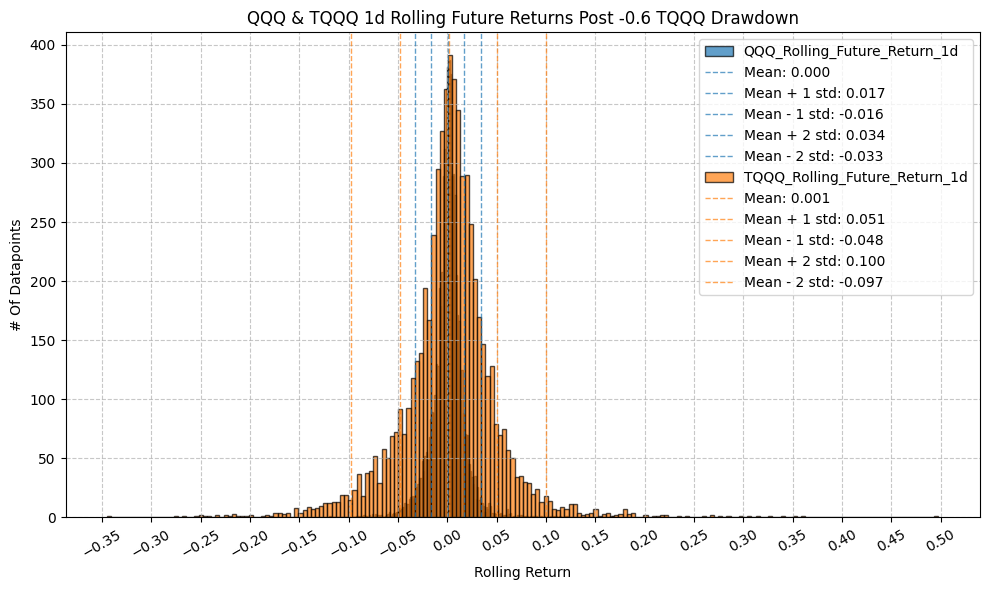

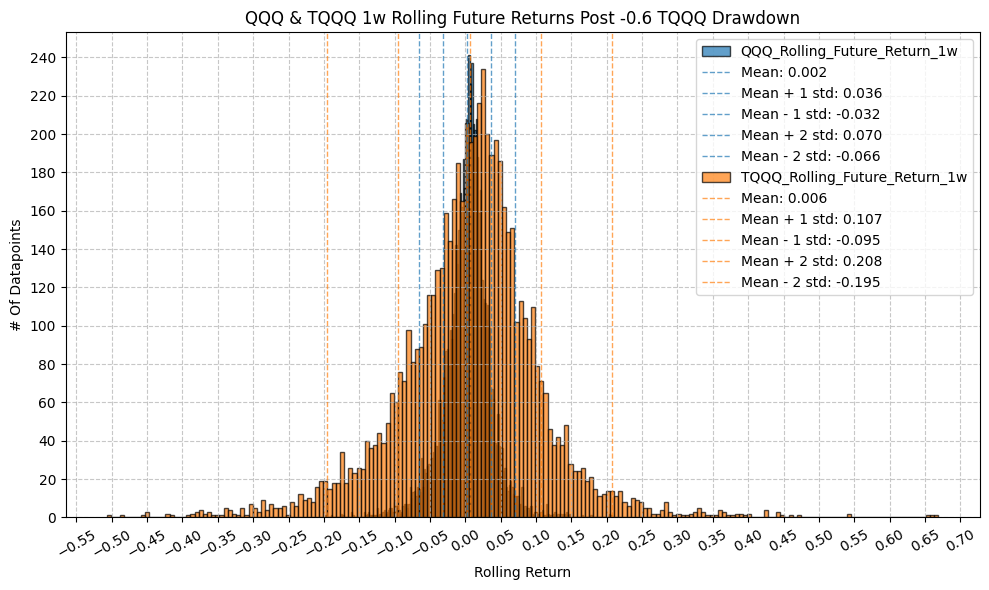

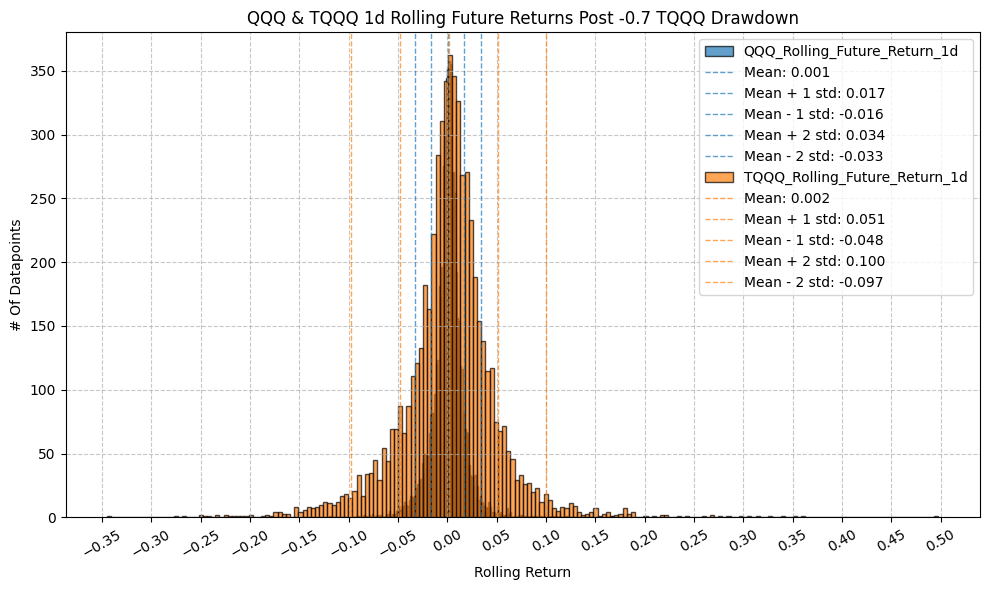

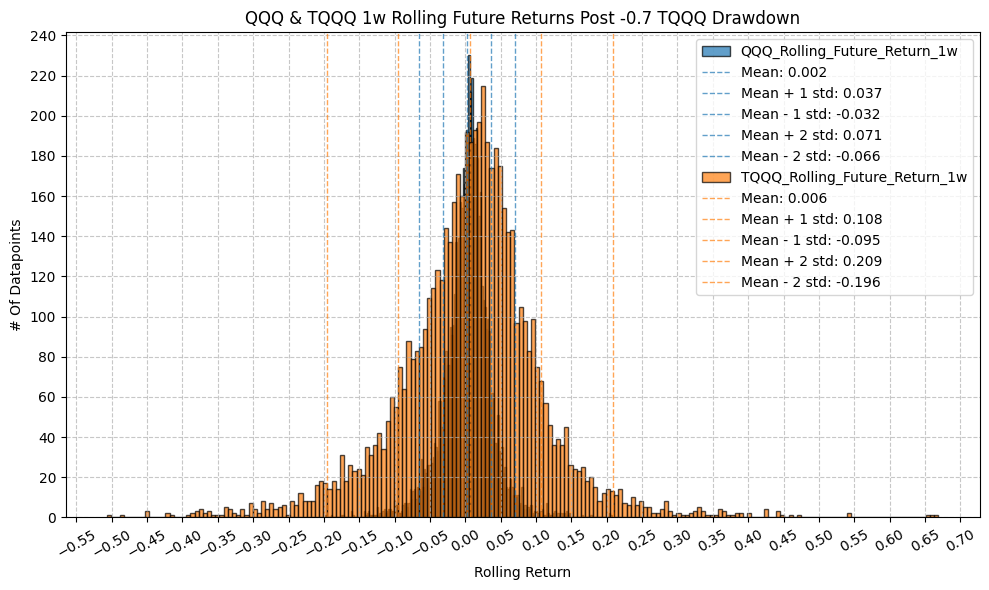

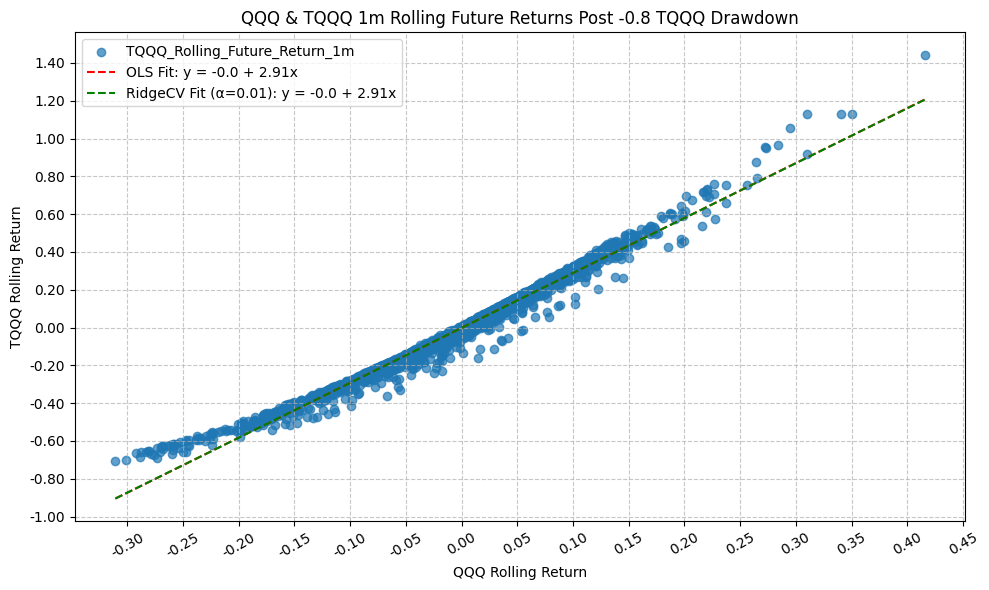

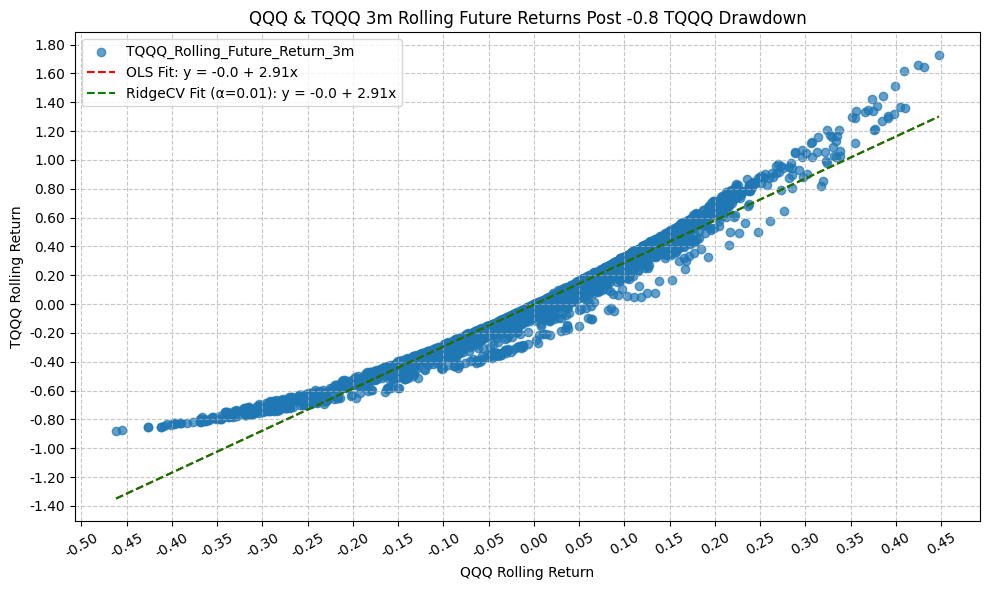

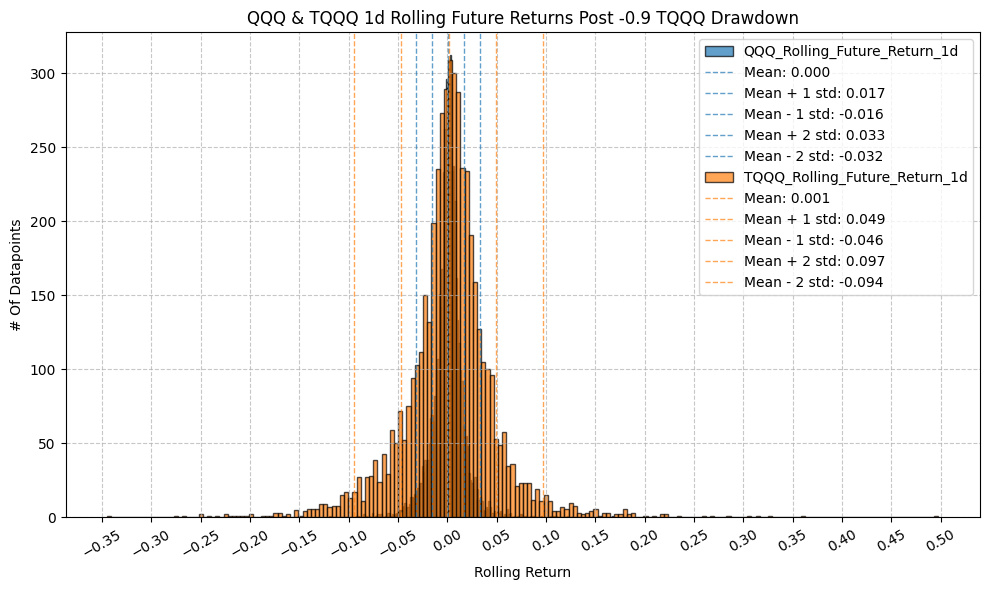

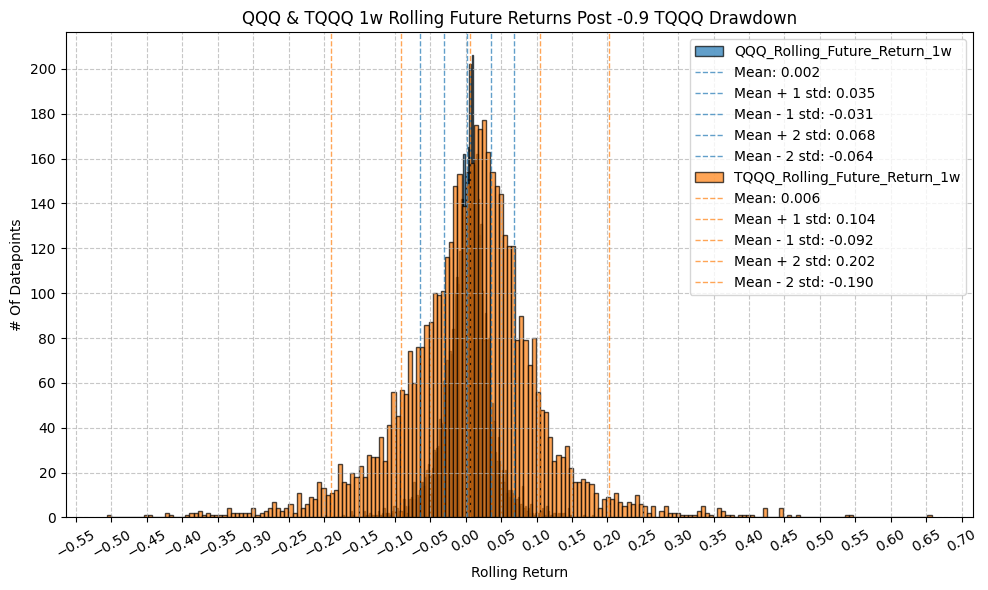

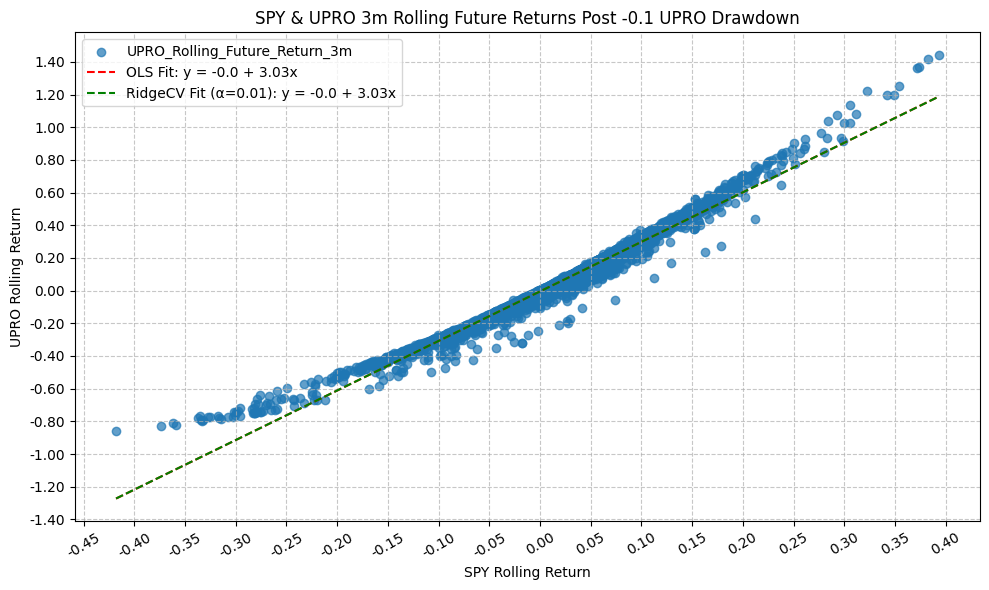

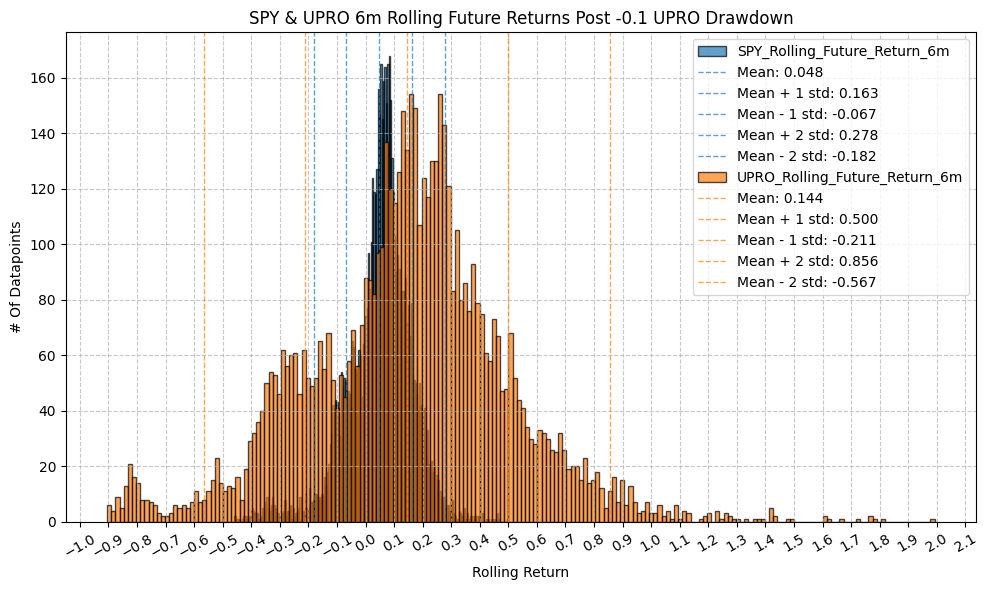

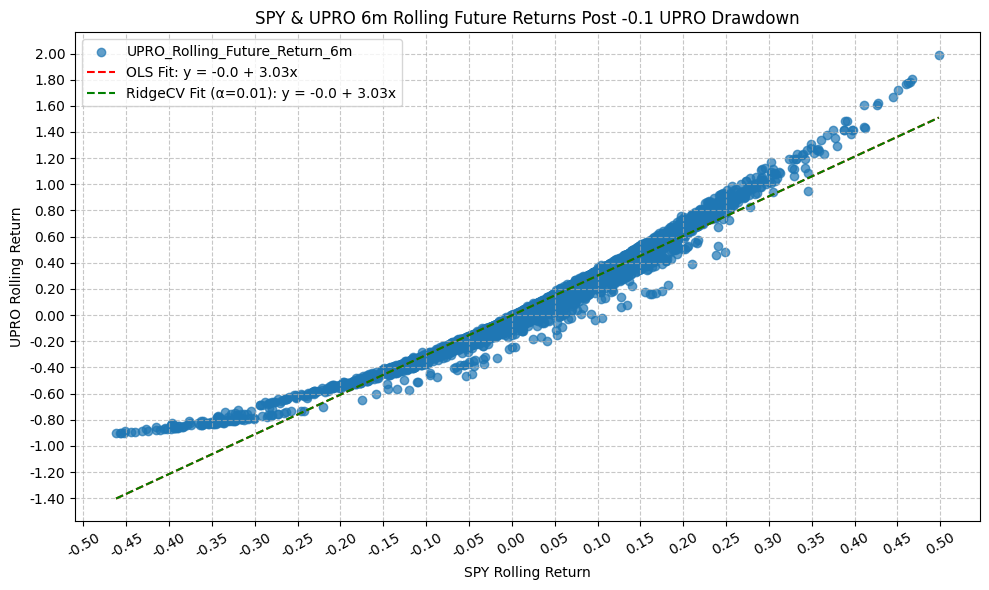

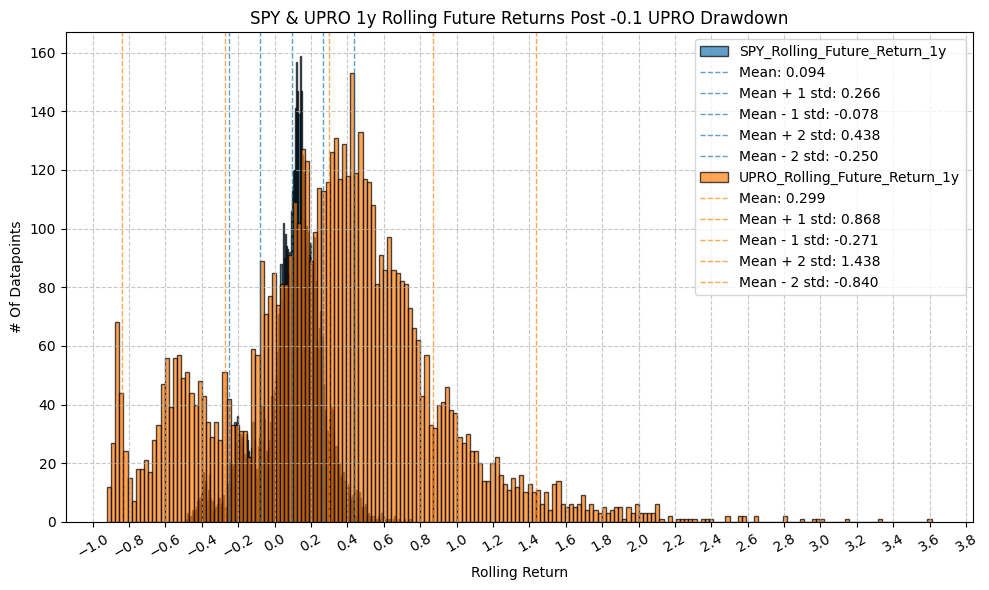

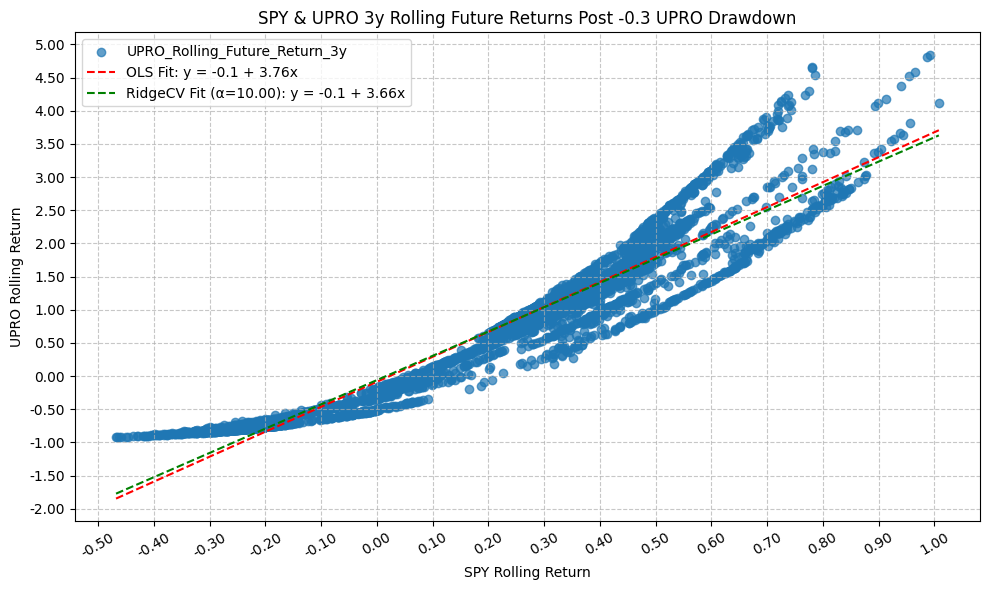

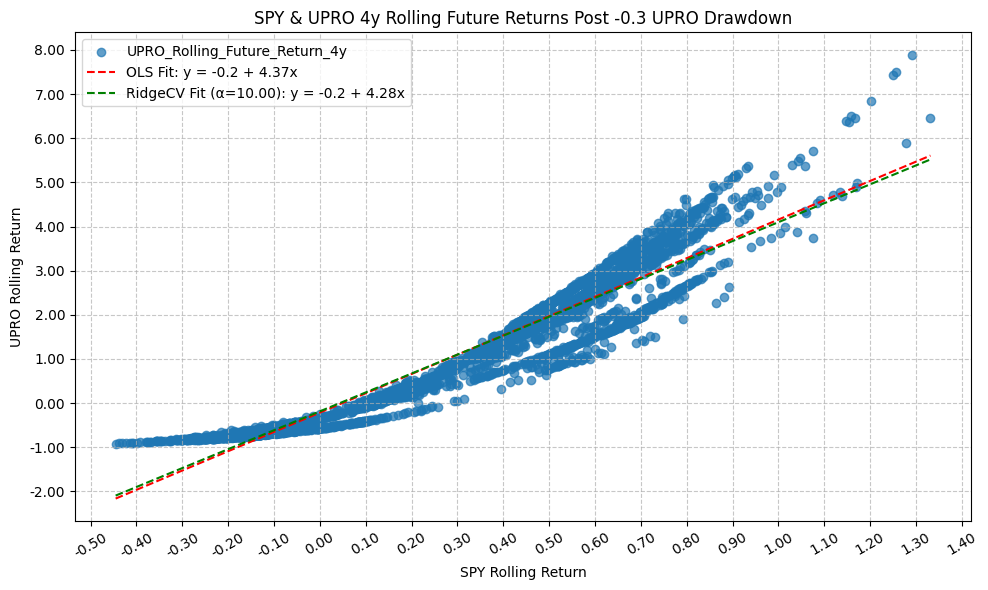

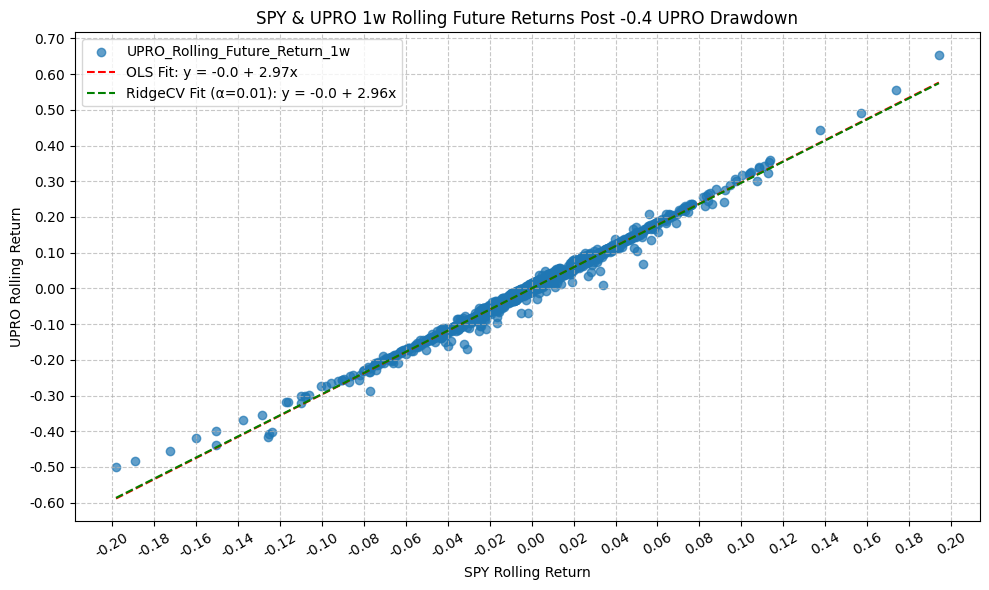

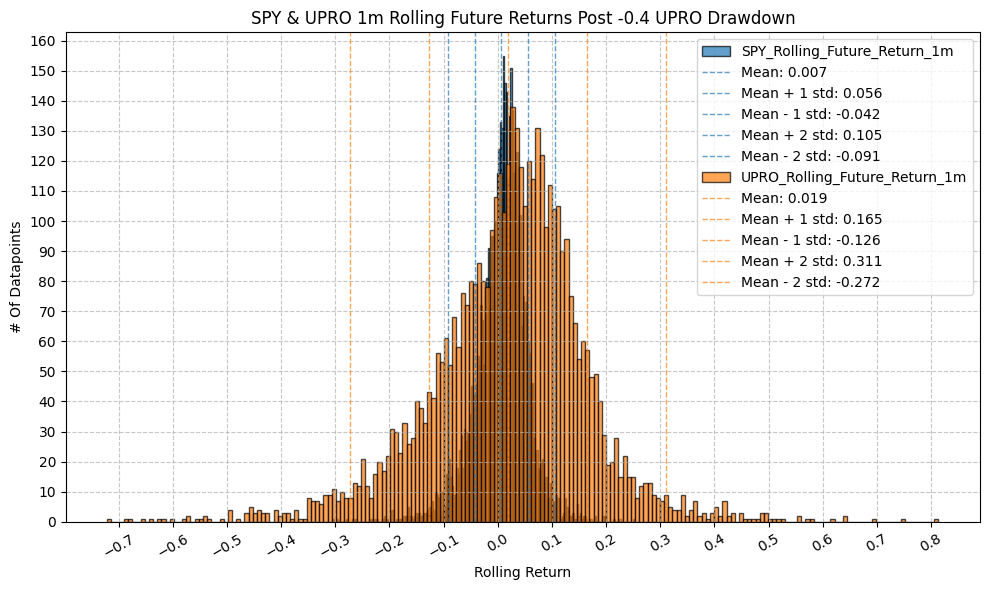

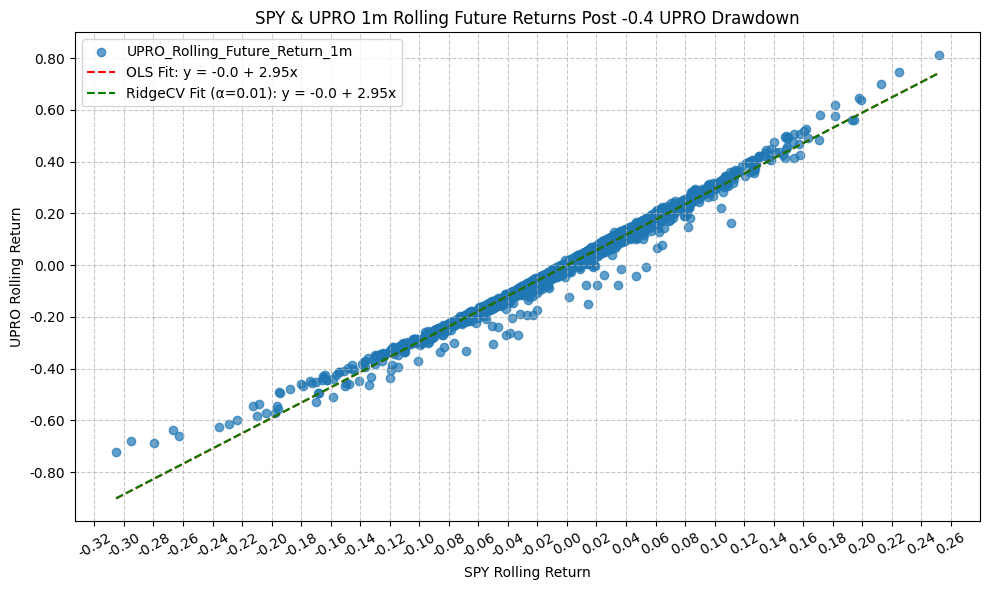

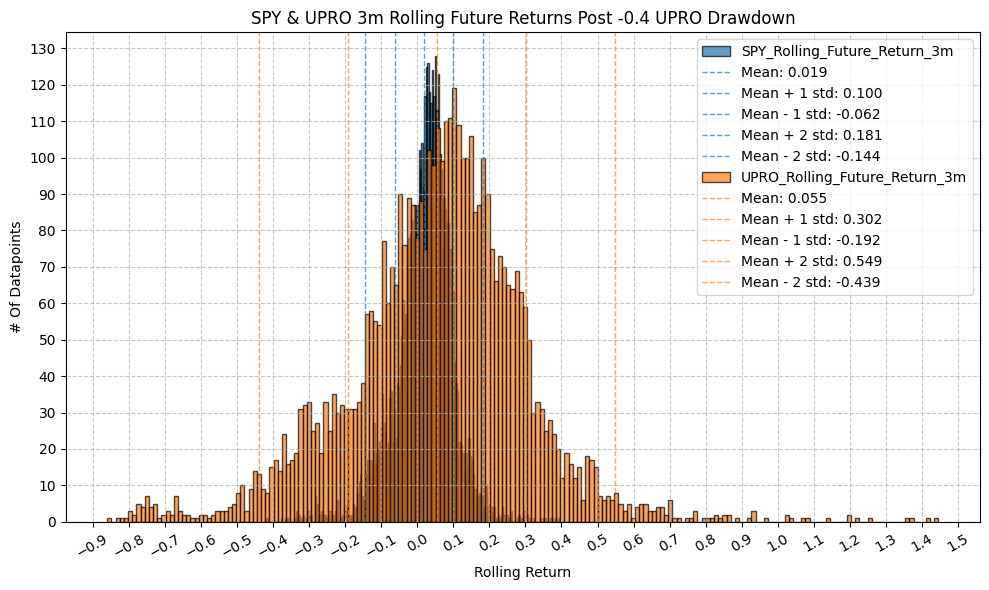

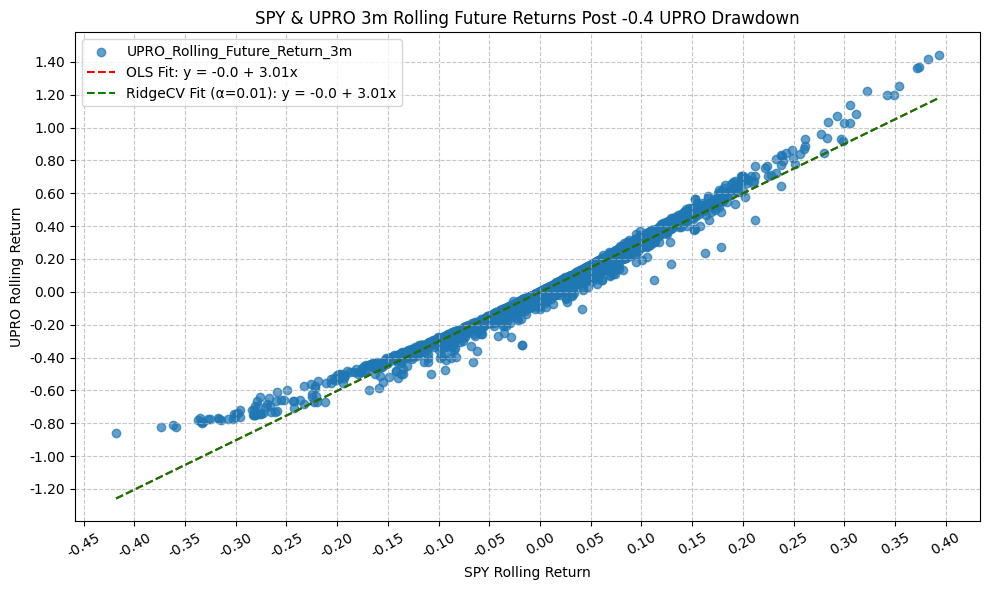

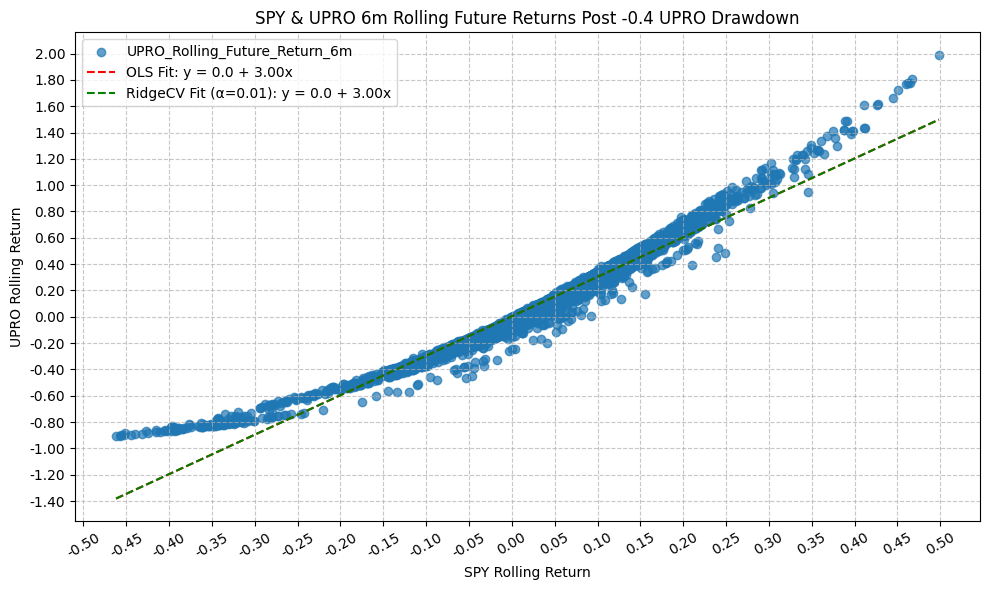

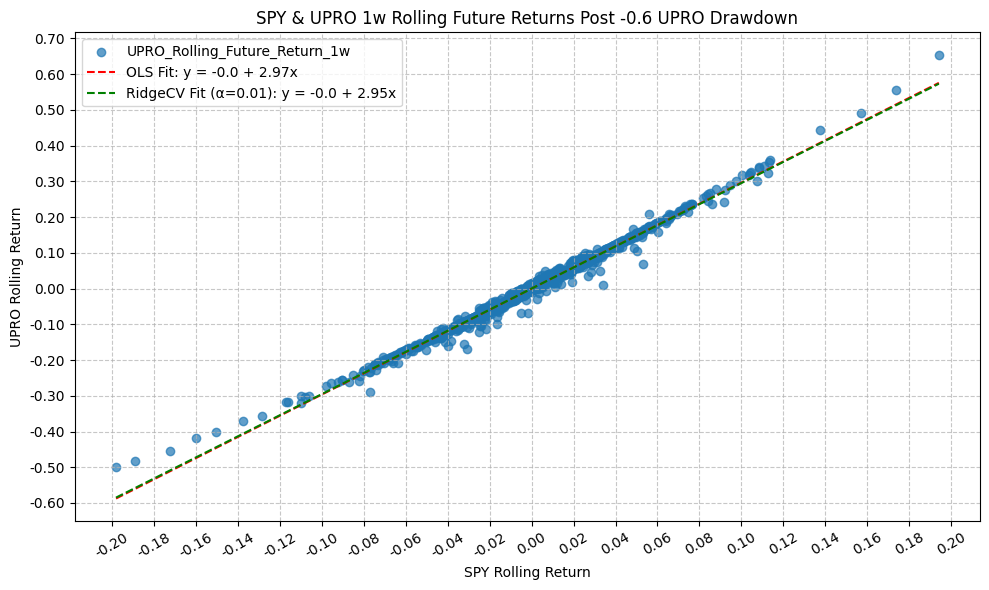

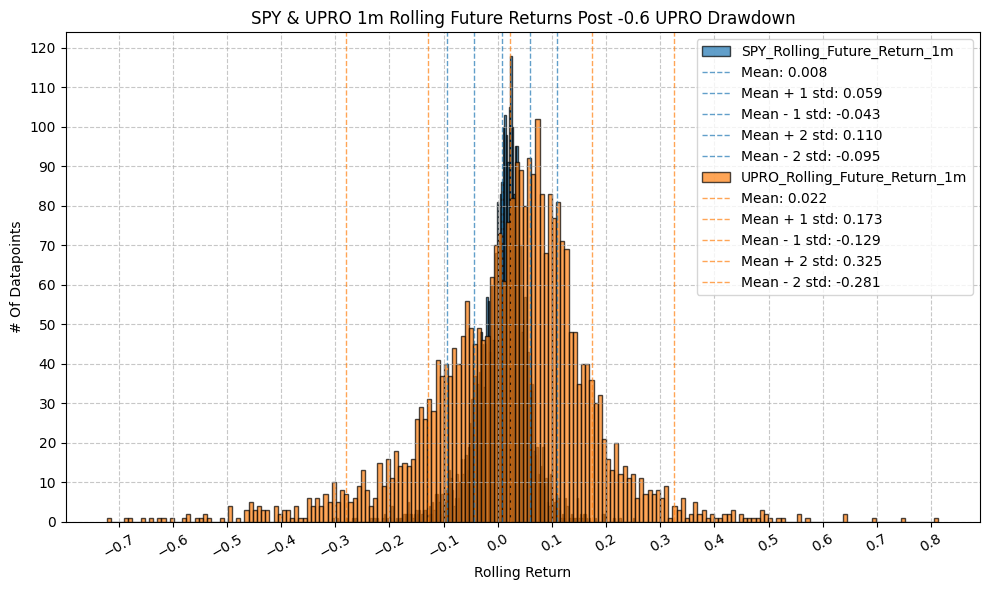

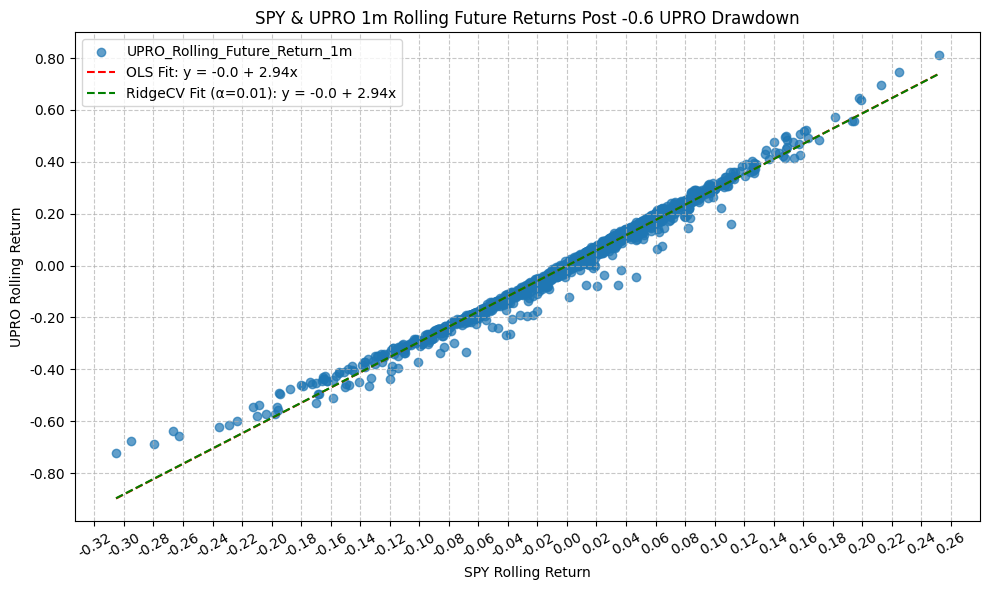

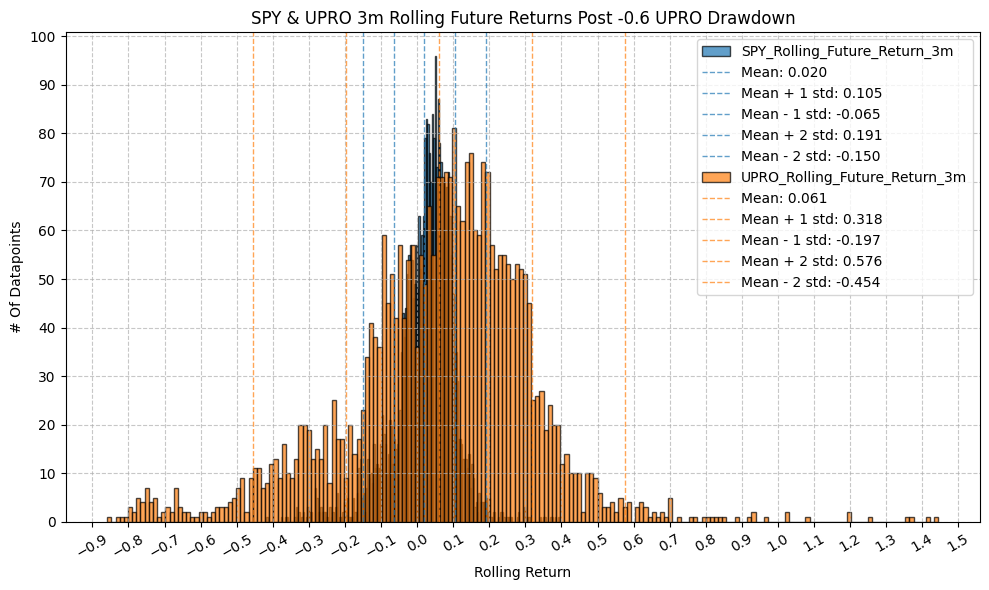

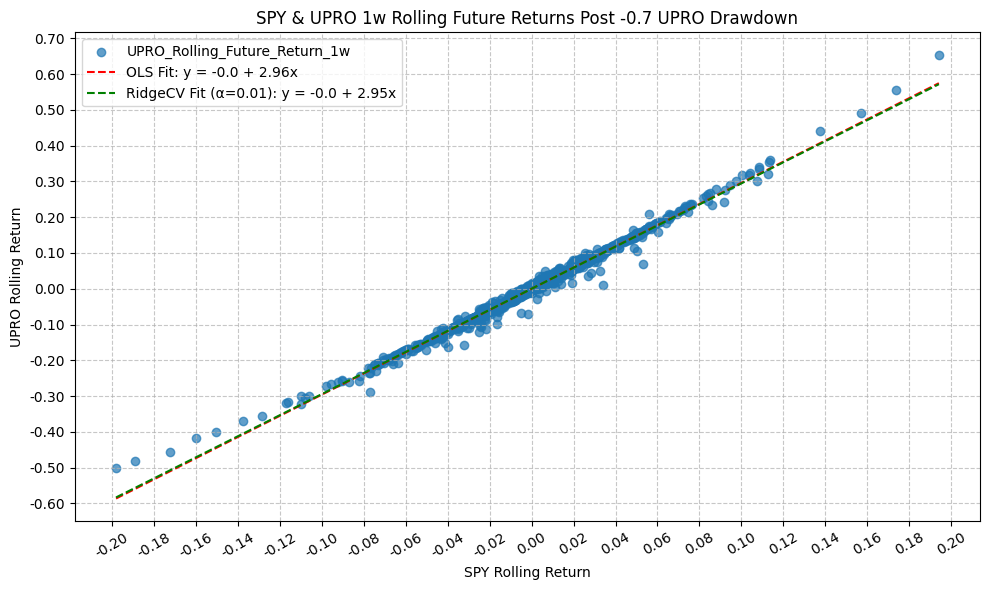

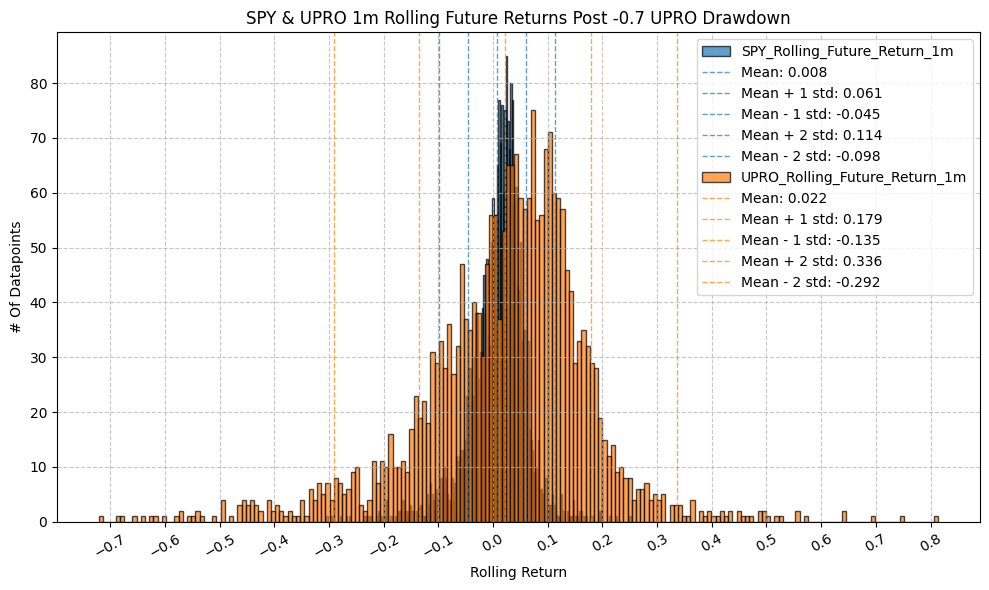

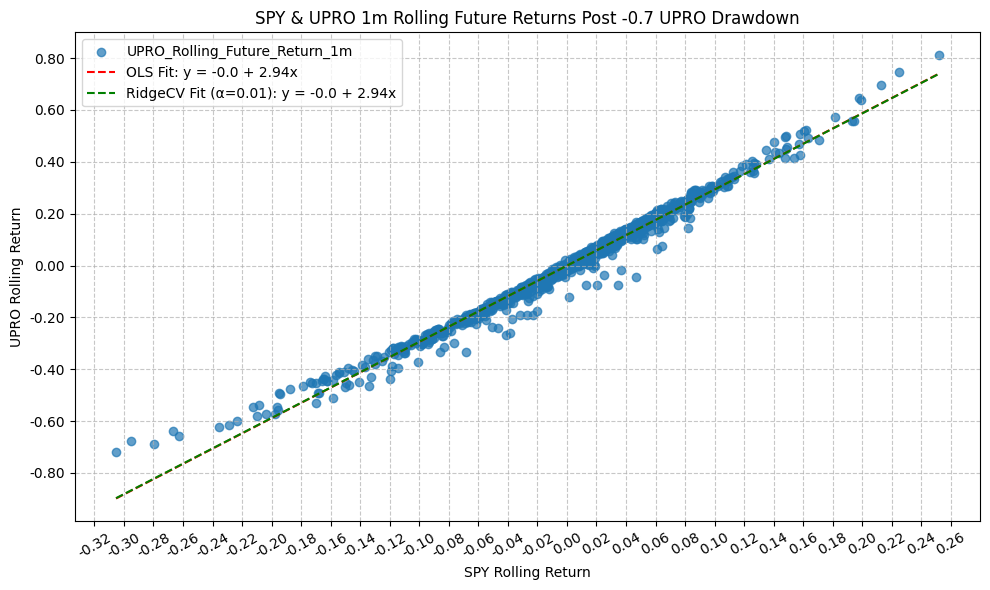

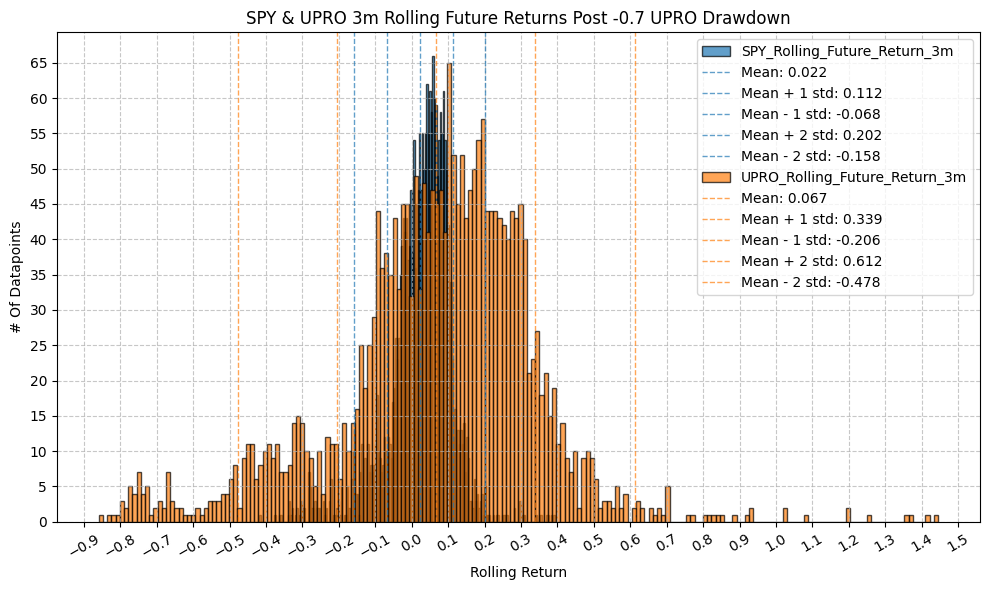

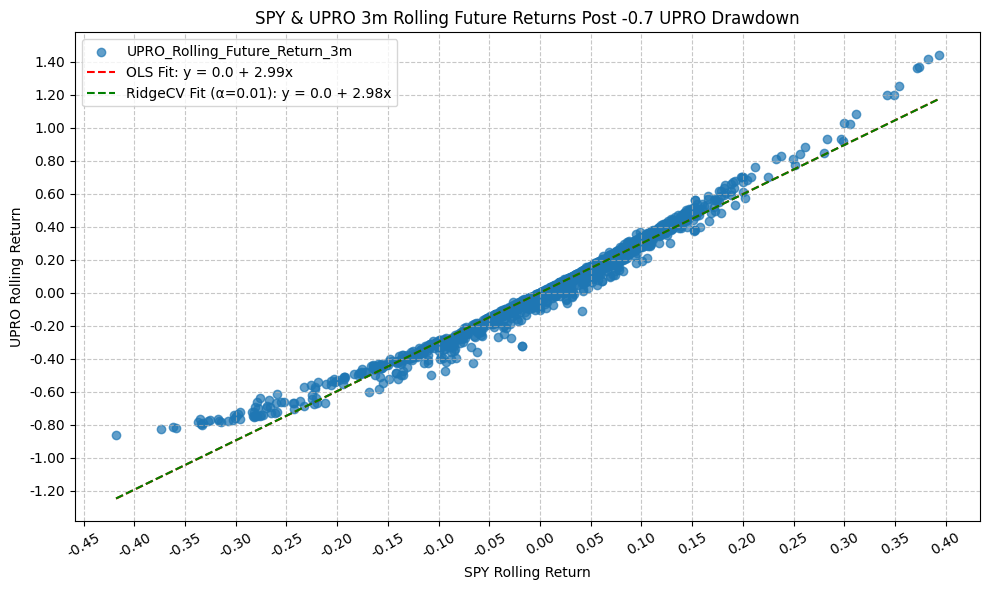

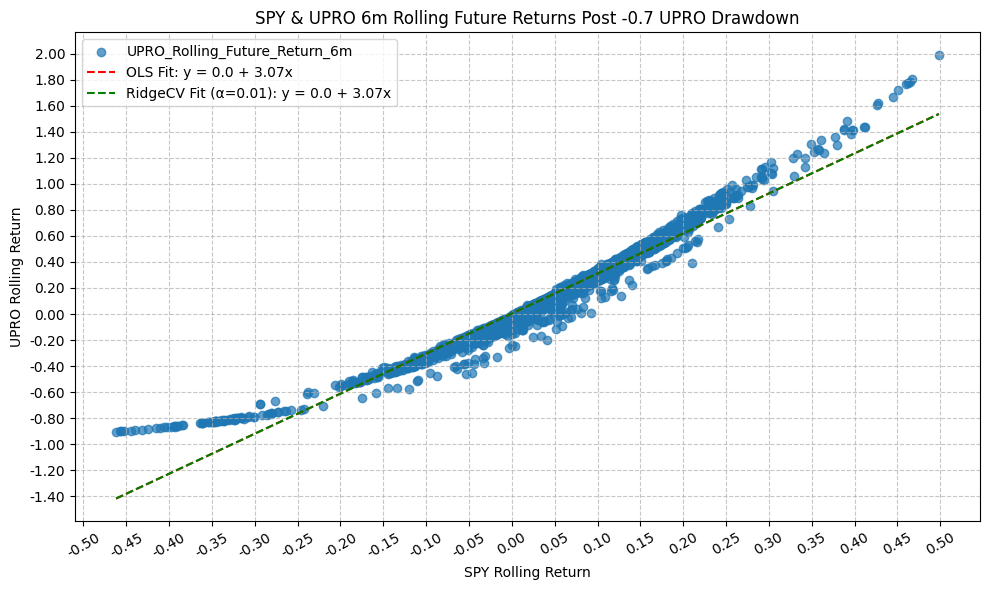

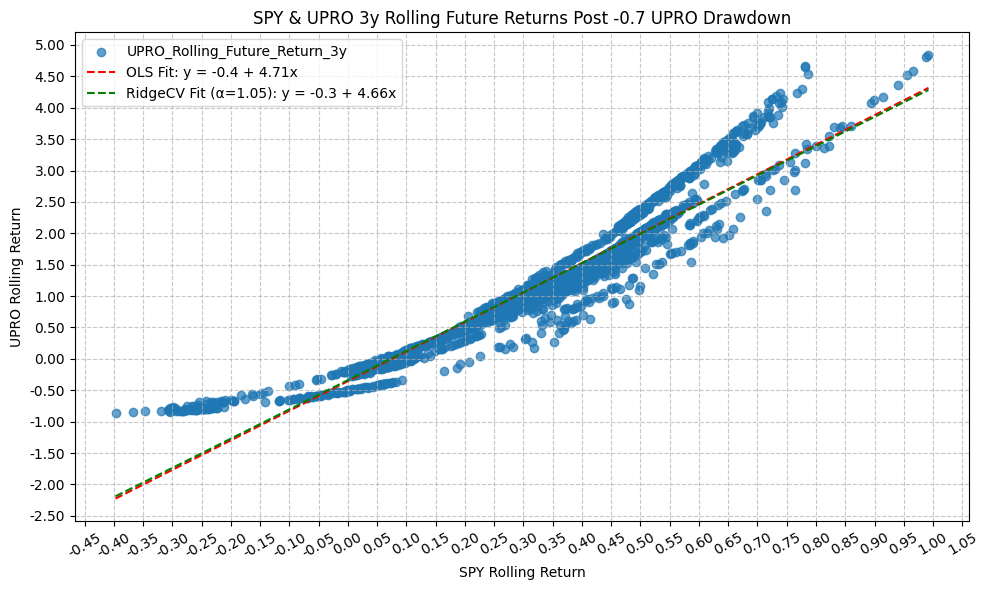

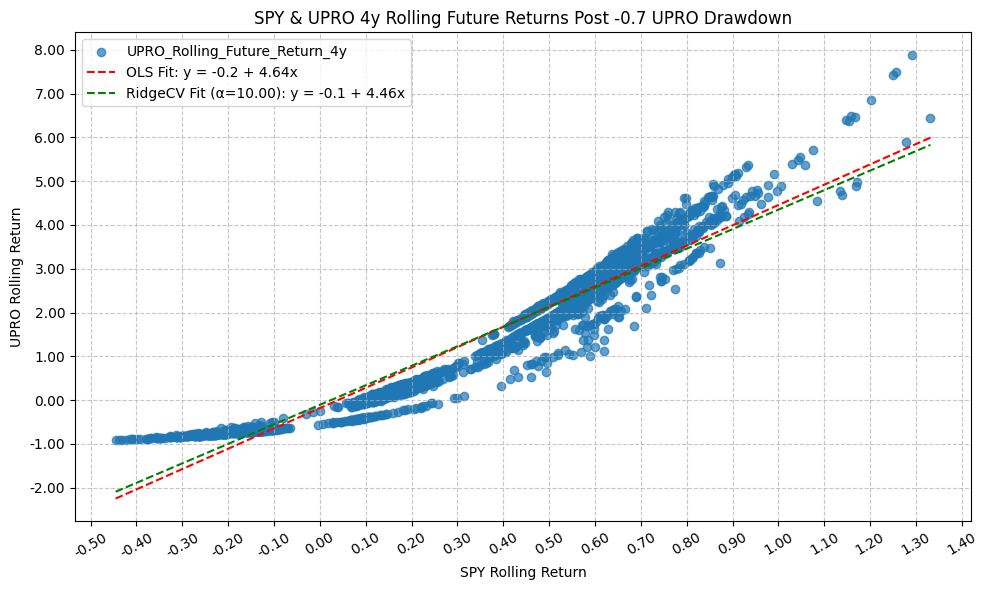

title=f"QQQ & TQQQ {period_name} Rolling Future Returns Post {drawdown} TQQQ Drawdown",

x_label="Rolling Return",

x_tick_spacing="Auto",

x_tick_rotation=30,

y_label="# Of Datapoints",

y_tick_spacing="Auto",

y_tick_rotation=0,

grid=True,

legend=True,

export_plot=False,

plot_file_name=None,

)

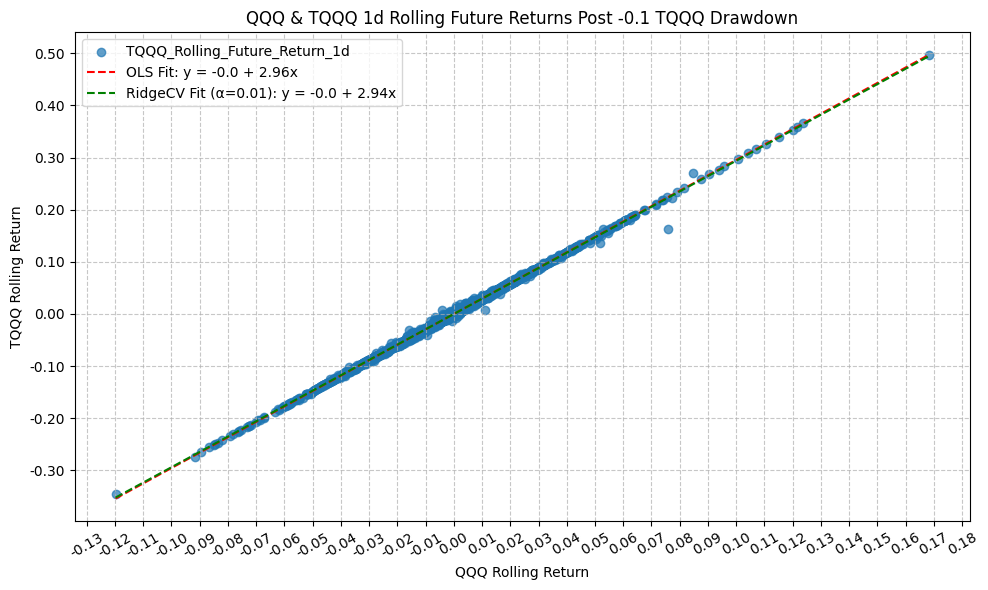

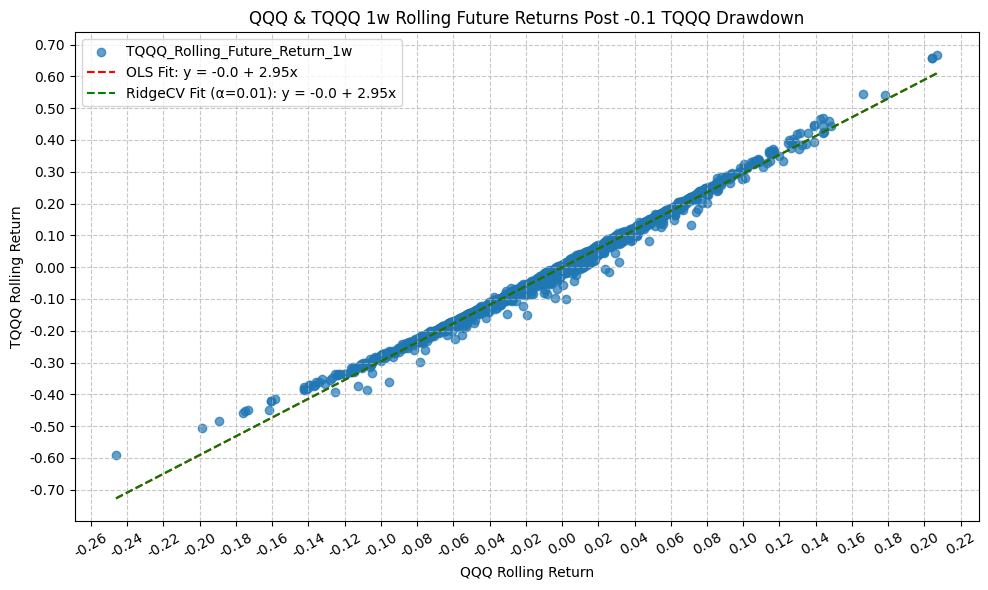

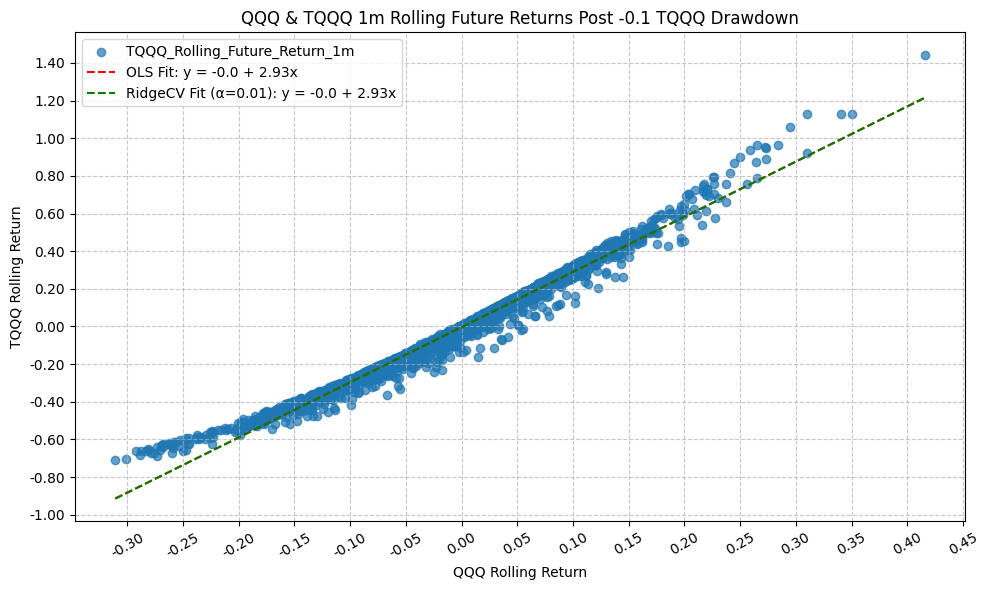

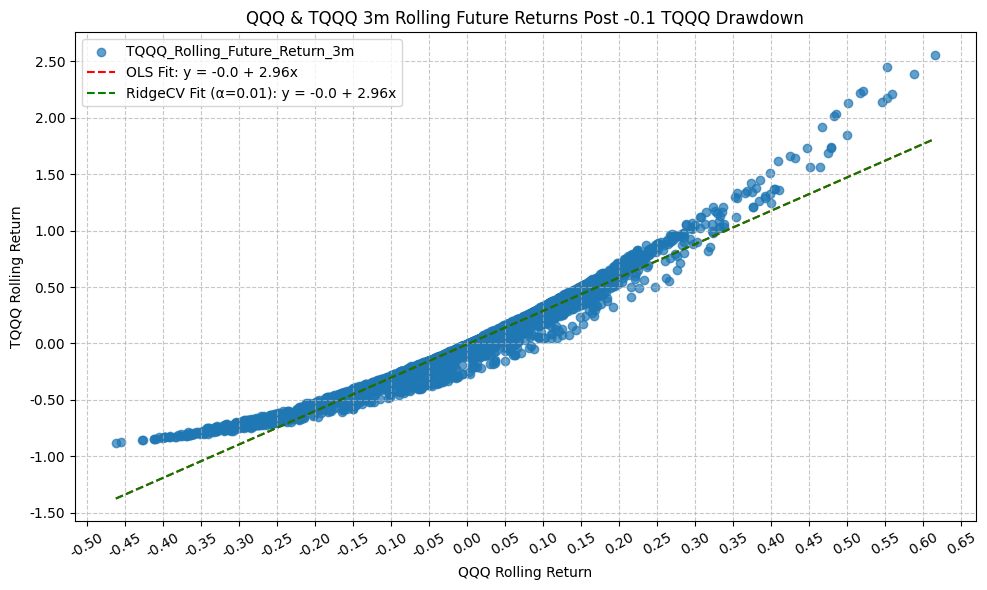

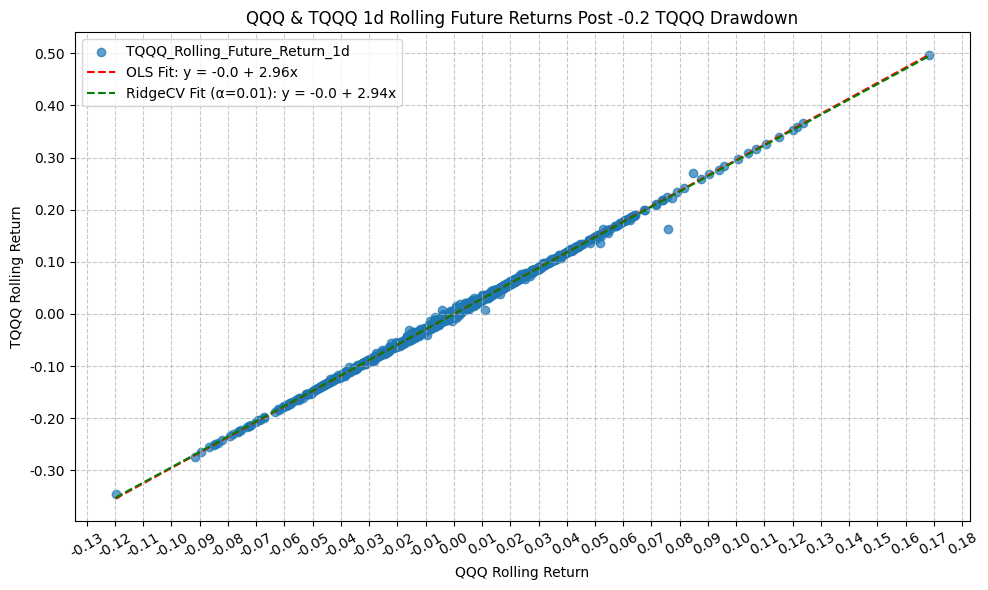

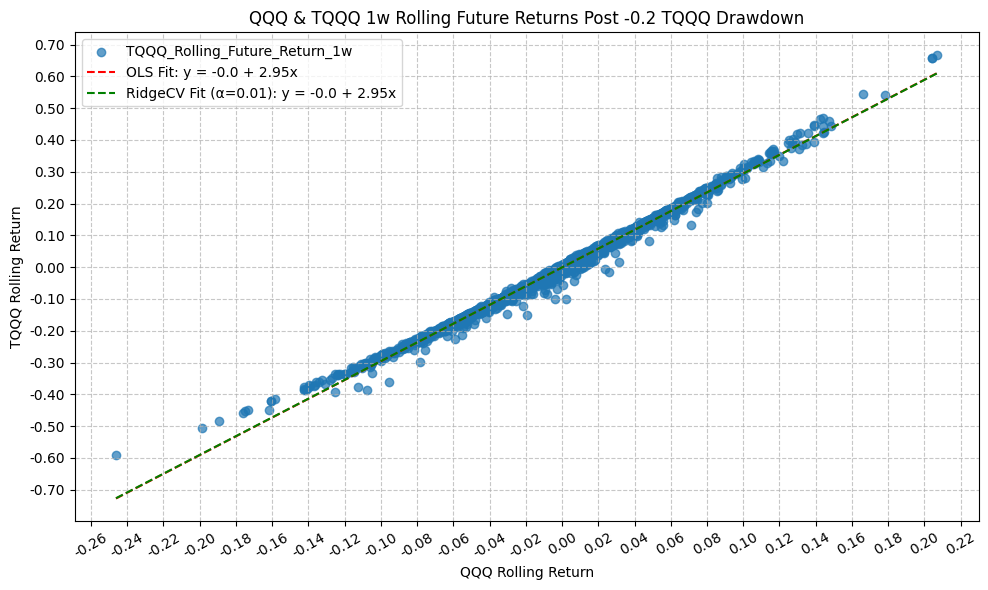

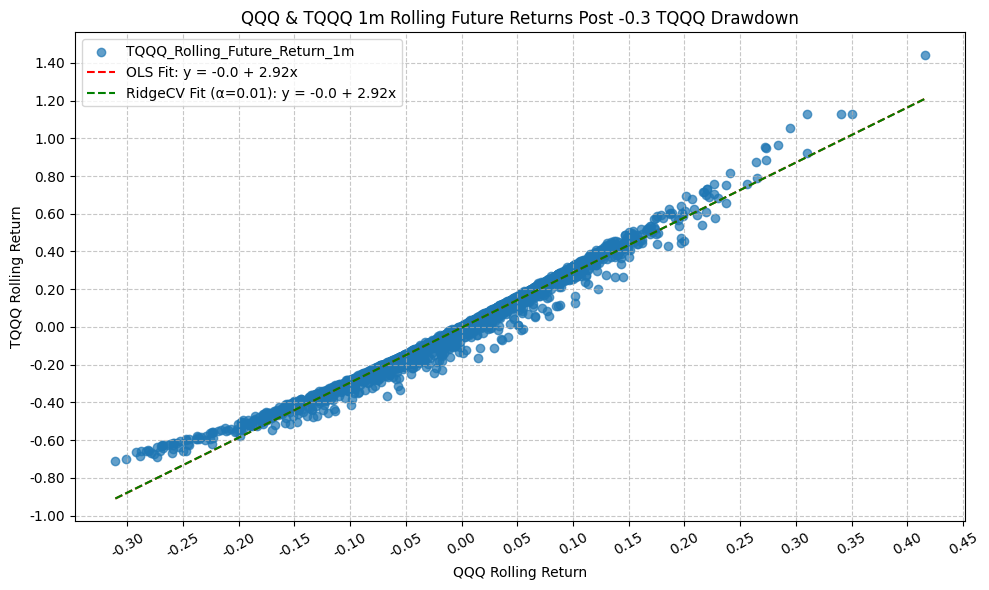

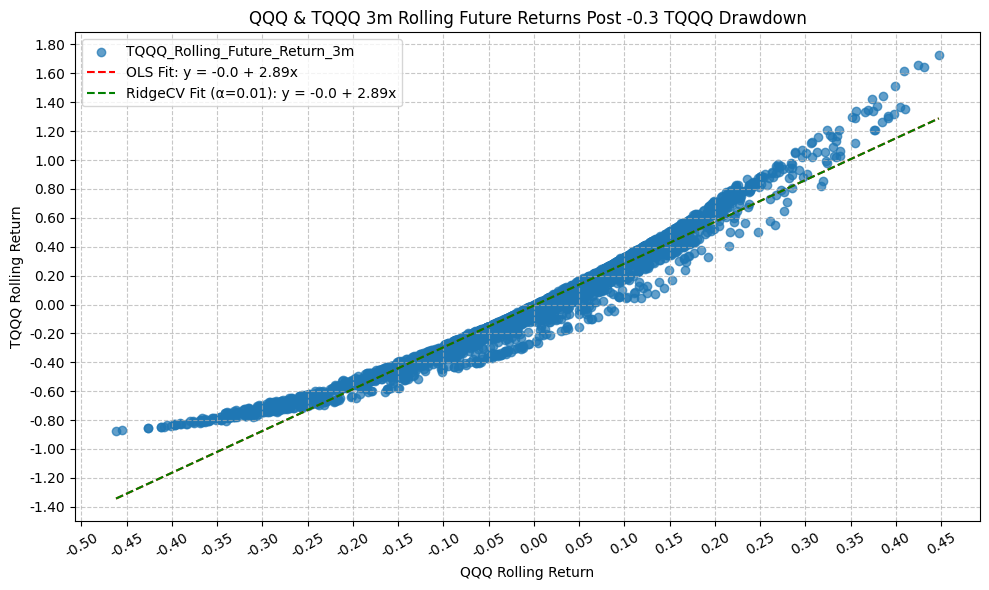

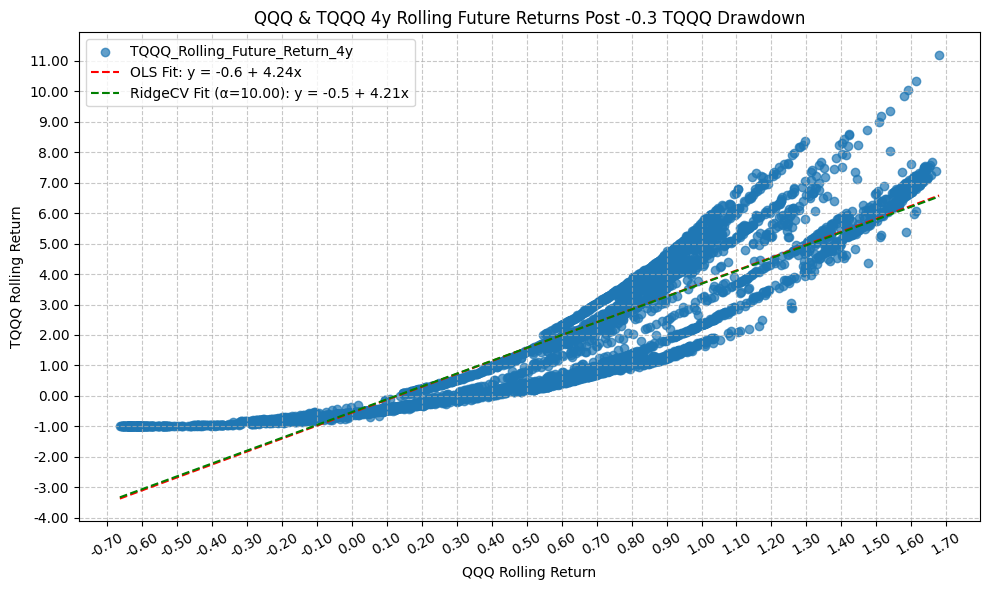

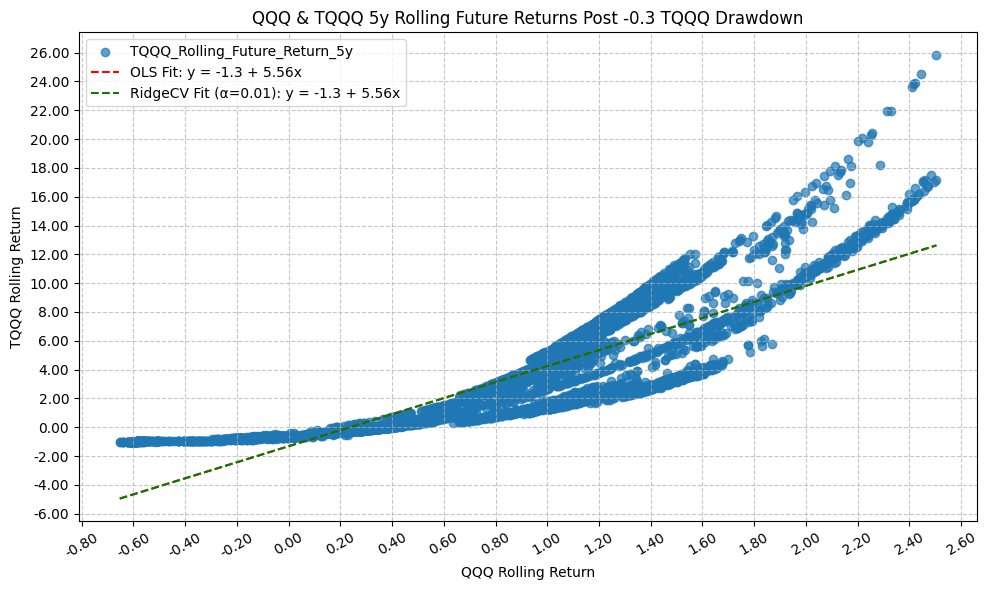

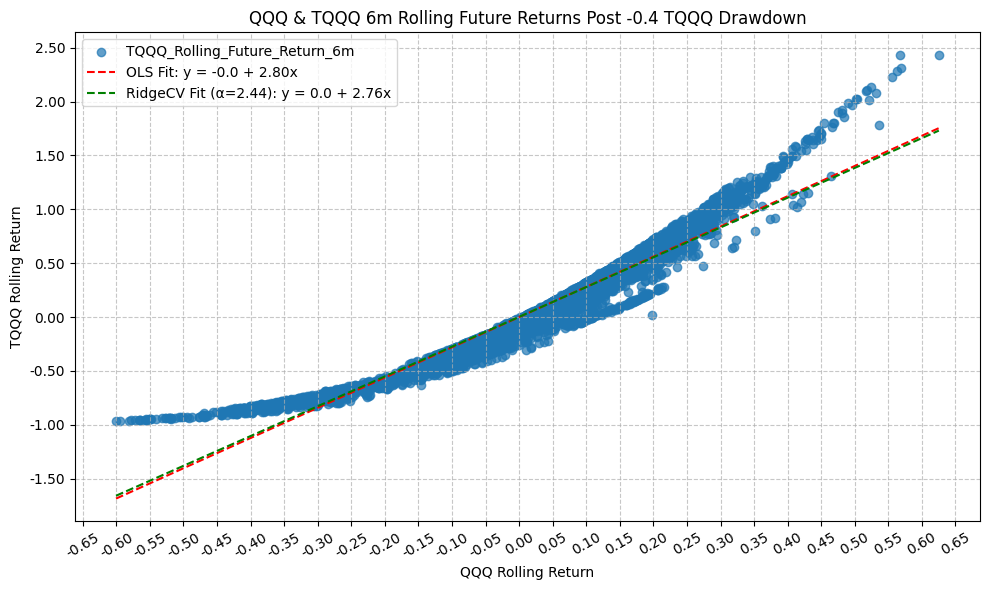

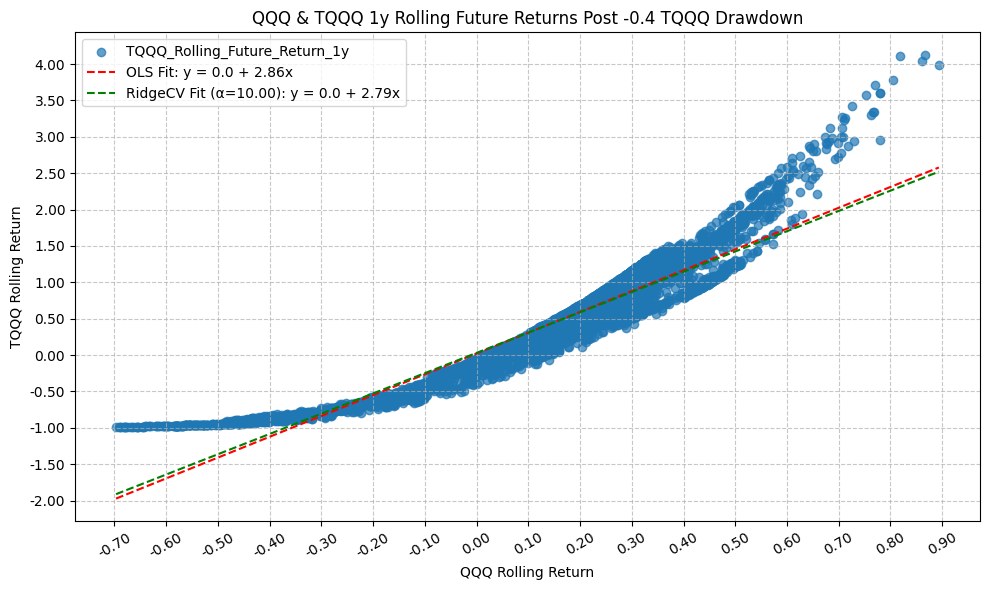

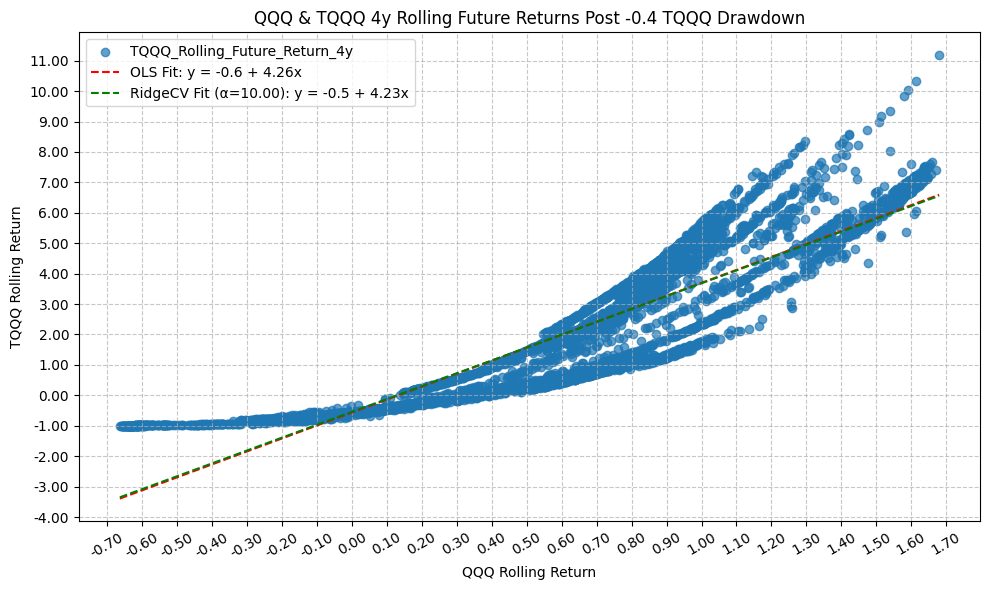

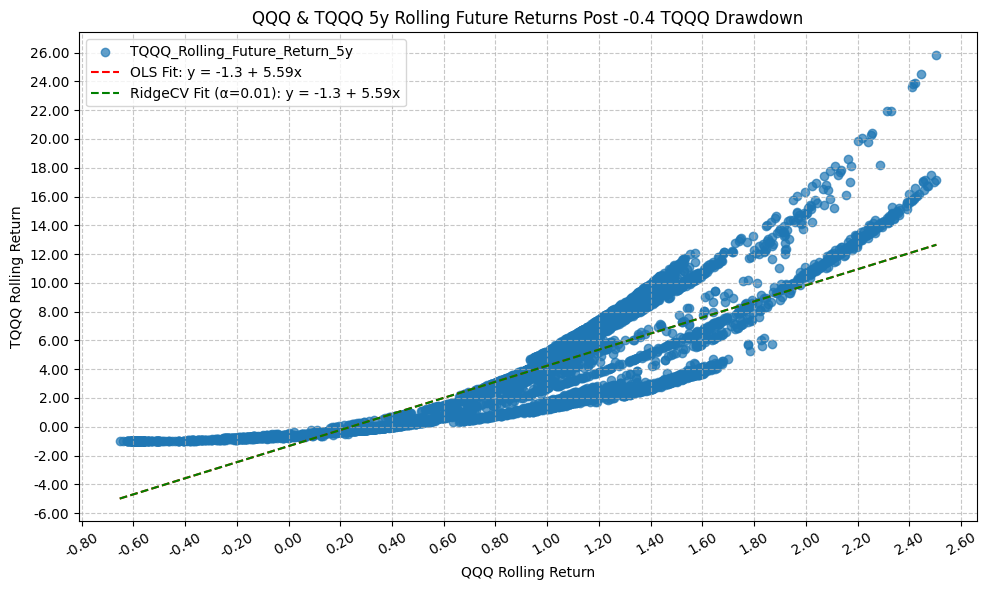

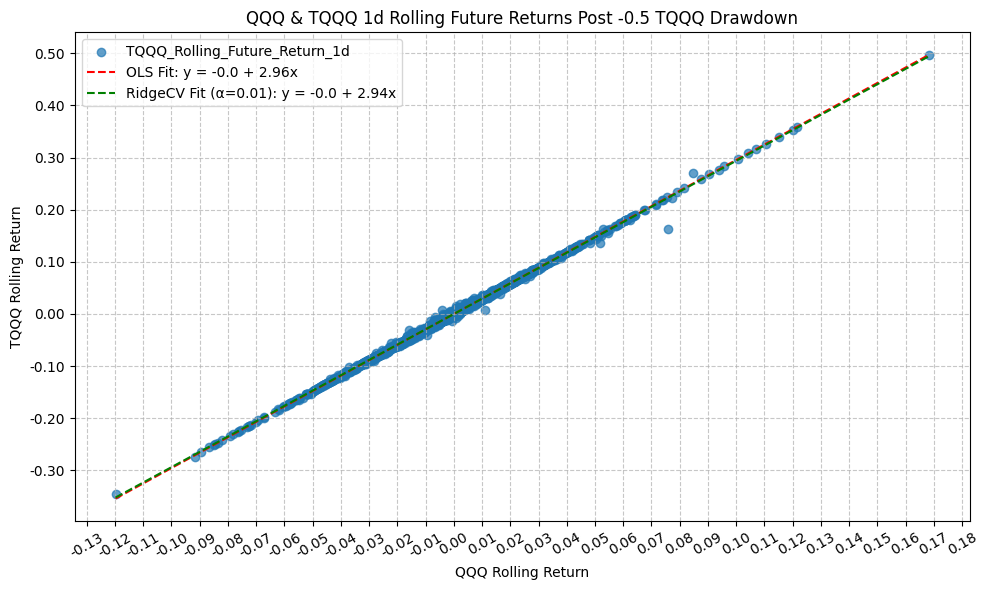

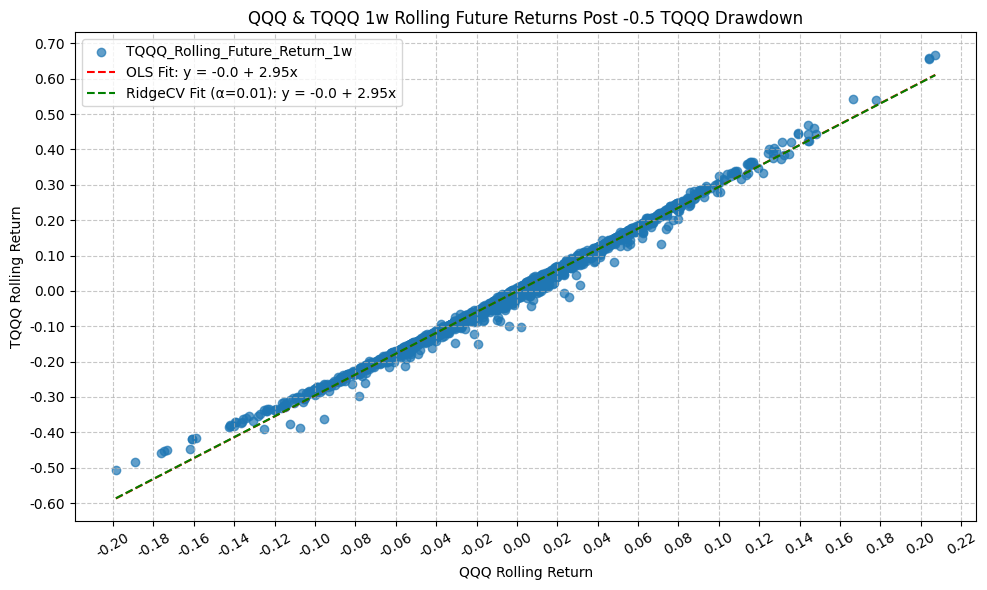

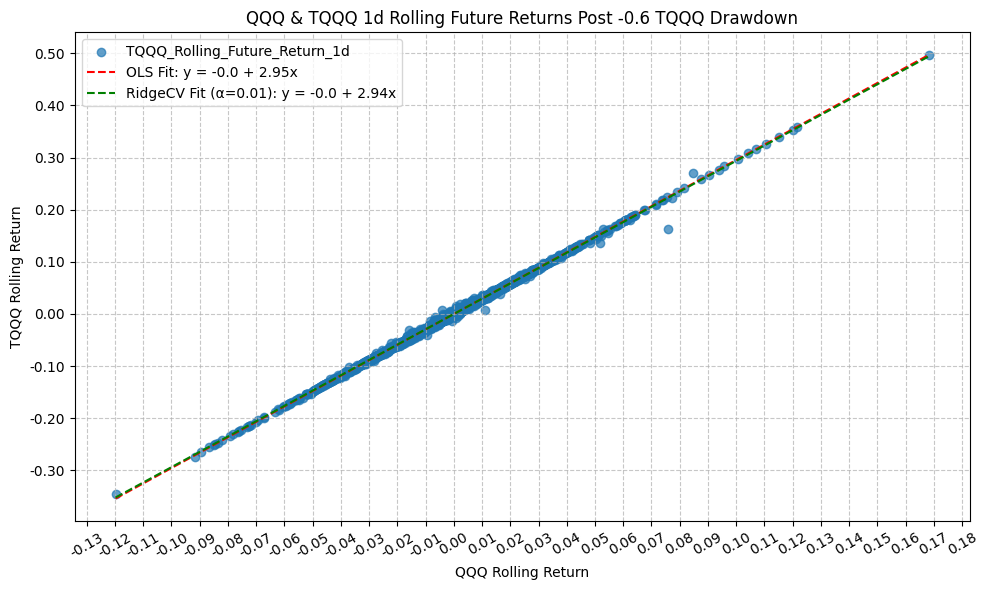

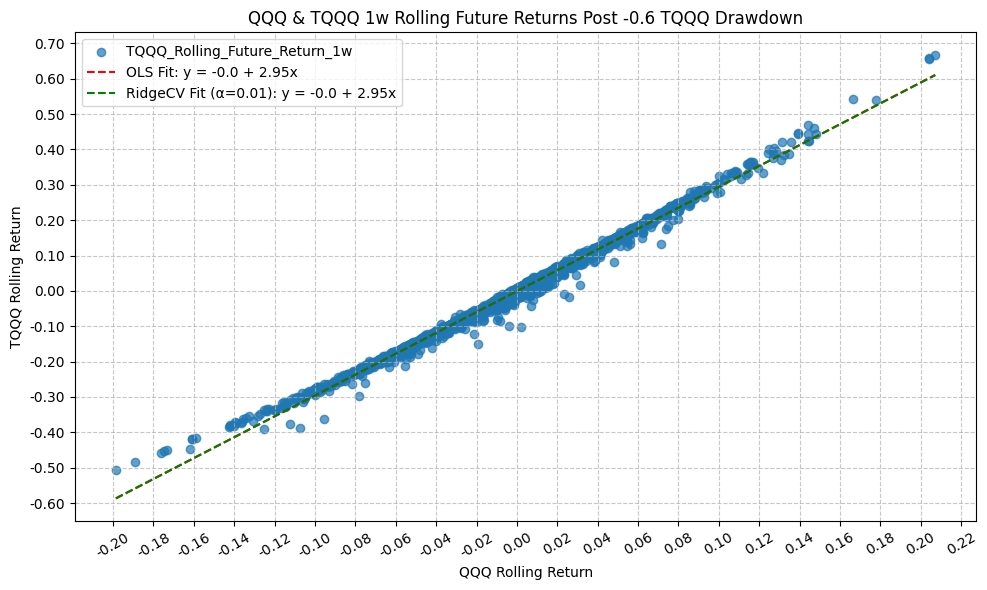

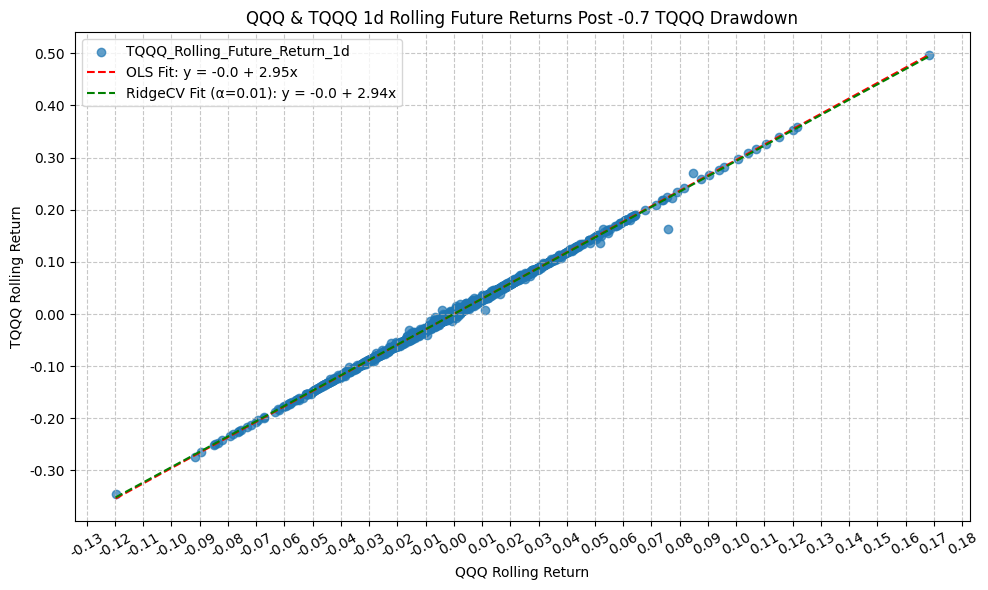

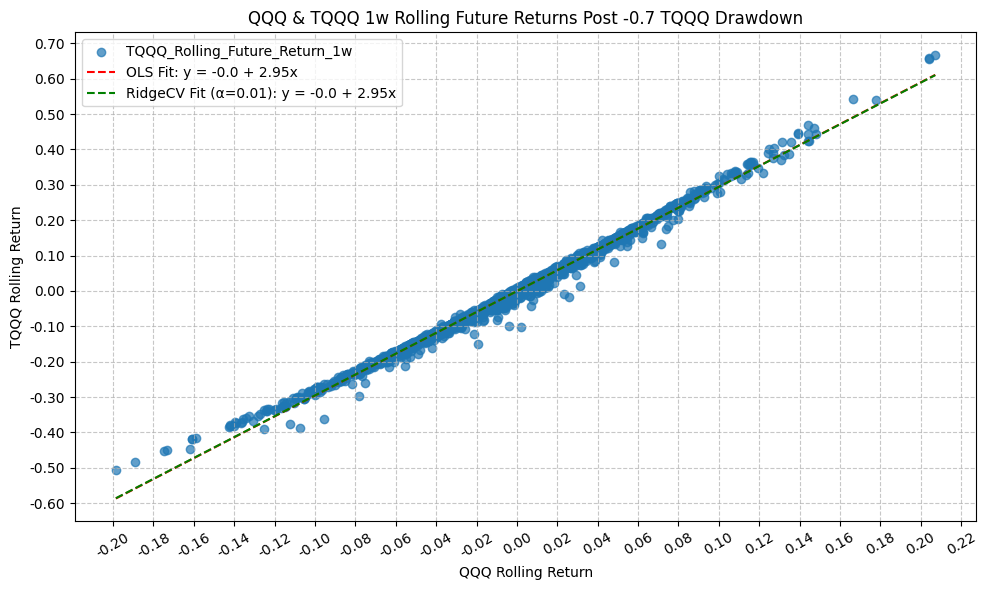

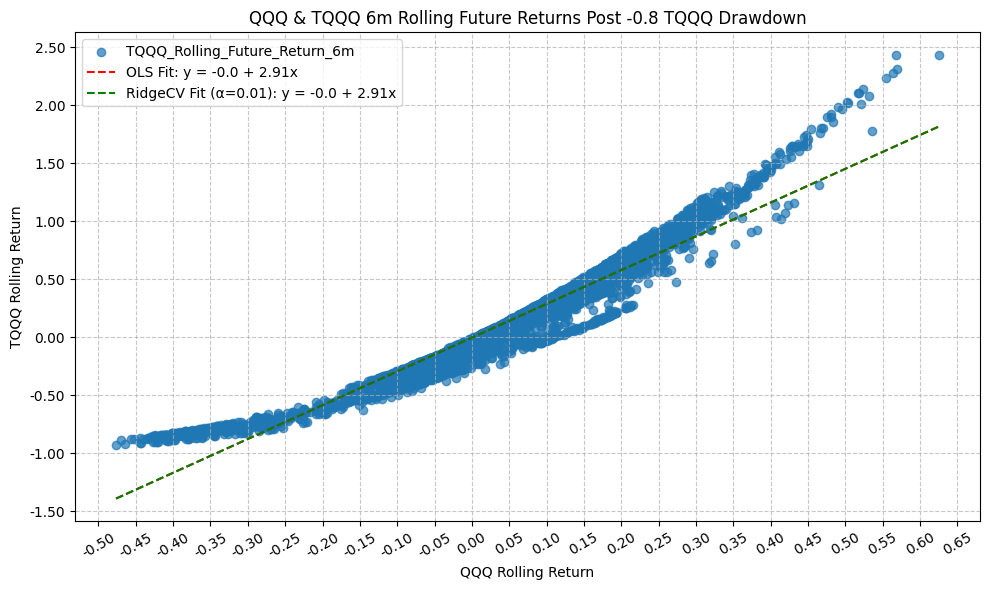

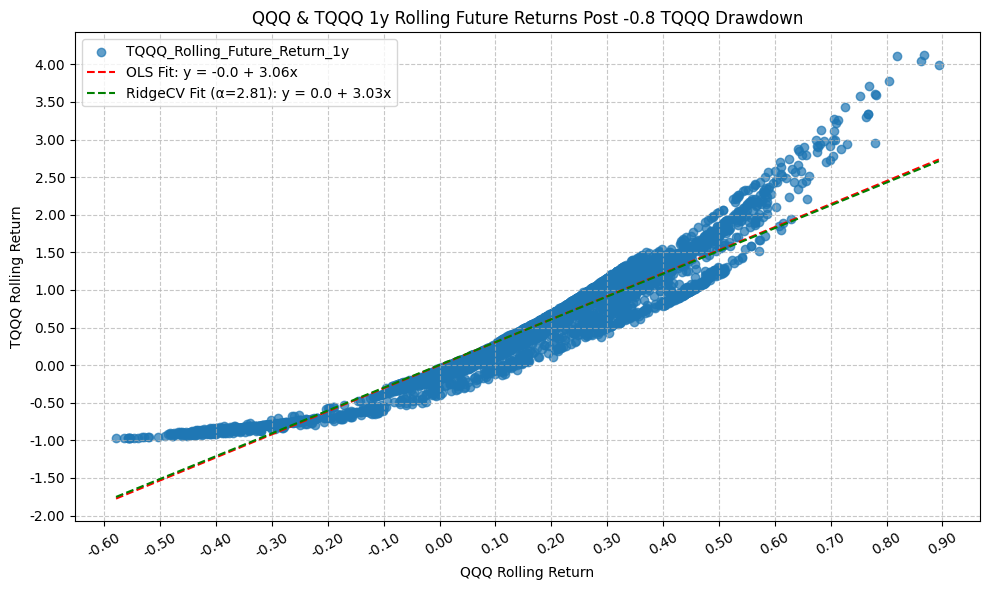

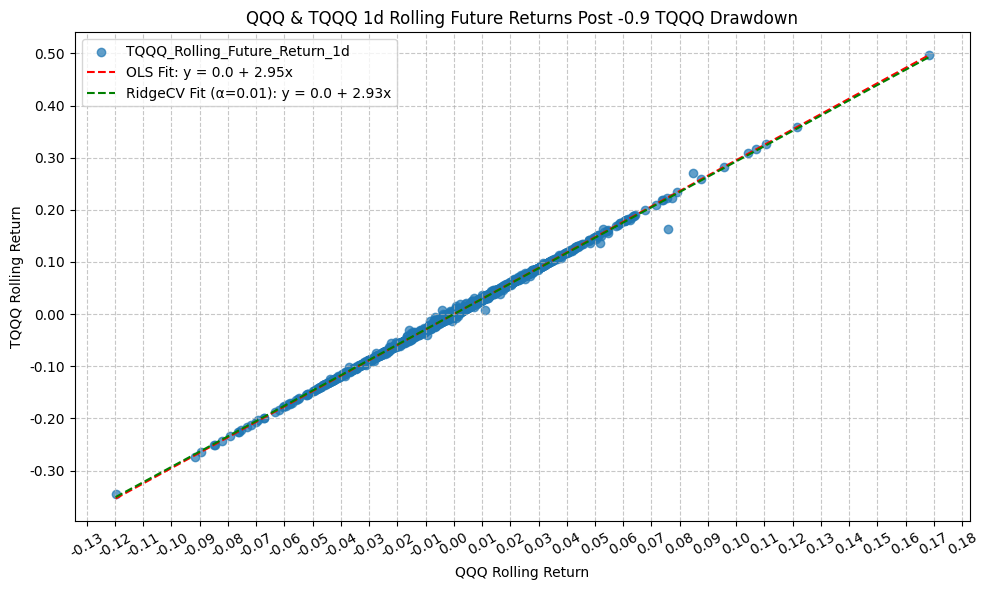

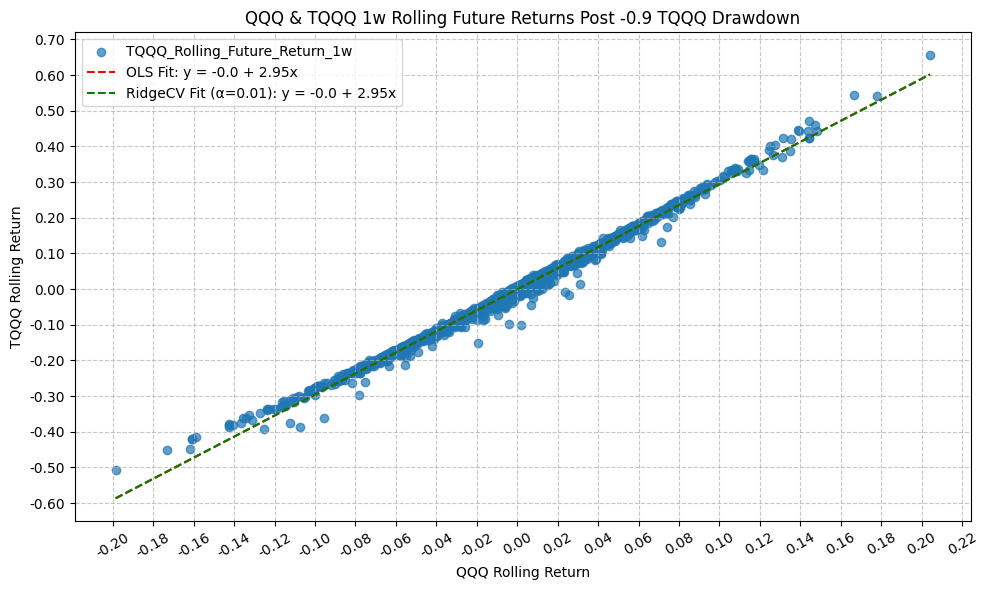

plot_scatter(

df=qqq_tqqq_extrap_future[qqq_tqqq_extrap_future["TQQQ_Drawdown"] <= drawdown],

x_plot_column=f"QQQ_Rolling_Future_Return_{period_name}",

y_plot_columns=[f"TQQQ_Rolling_Future_Return_{period_name}"],

title=f"QQQ & TQQQ {period_name} Rolling Future Returns Post {drawdown} TQQQ Drawdown",

x_label="QQQ Rolling Return",

x_format="Decimal",

x_format_decimal_places=2,

x_tick_spacing="Auto",

x_tick_start=None,

x_tick_rotation=30,

y_label="TQQQ Rolling Return",

y_format="Decimal",

y_format_decimal_places=2,

y_tick_spacing="Auto",

y_tick_rotation=0,

plot_OLS_regression_line=True,

OLS_column=f"TQQQ_Rolling_Future_Return_{period_name}",

plot_Ridge_regression_line=False,

Ridge_column=None,

plot_RidgeCV_regression_line=True,

RidgeCV_column=f"TQQQ_Rolling_Future_Return_{period_name}",

regression_constant=True,

grid=True,

legend=True,

export_plot=False,

plot_file_name=None,

)

# Run OLS regression with statsmodels

model = run_regression(

df=qqq_tqqq_extrap_future[qqq_tqqq_extrap_future["TQQQ_Drawdown"] <= drawdown],

x_plot_column=f"QQQ_Rolling_Future_Return_{period_name}",

y_plot_column=f"TQQQ_Rolling_Future_Return_{period_name}",

regression_model="OLS-statsmodels",

regression_constant=True,

)

print(model.summary())

# Filter by drawdown

drawdown_filter = qqq_tqqq_extrap_future[qqq_tqqq_extrap_future["TQQQ_Drawdown"] <= drawdown]

# Filter by period, drop rows with missing values

future_filter = drawdown_filter[[f"TQQQ_Rolling_Future_Return_{period_name}"]].dropna()

# Find length of future dataframe

future_length = len(future_filter)

# Find length of future dataframe where return is positive

positive_future_length = len(future_filter[future_filter[f"TQQQ_Rolling_Future_Return_{period_name}"] > 0])

# Calculate percentage of future returns that are positive

positive_future_percentage = (positive_future_length / future_length) if future_length > 0 else 0

# Add the regression results to the rolling returns stats dataframe

intercept = model.params.iloc[0]

# intercept_pvalue = model.pvalues.iloc[0] # p-value for Intercept

slope = model.params.iloc[1]

# slope_pvalue = model.pvalues.iloc[1] # p-value for Slope

r_squared = model.rsquared

rolling_returns_slope_int = pd.DataFrame({

"Drawdown": drawdown,

"Period": period_name,

"Intercept": [intercept],

# "Intercept_PValue": [intercept_pvalue],

"Slope": [slope],

# "Slope_PValue": [slope_pvalue],

"R_Squared": [r_squared],

"Positive_Future_Percentage": [positive_future_percentage],

})

rolling_returns_drawdown_stats = pd.concat([rolling_returns_drawdown_stats, rolling_returns_slope_int])

except:

print(f"Not enough data points for drawdown level {drawdown} and period {period_name} to run regression.")

OLS Regression Results

=========================================================================================

Dep. Variable: TQQQ_Rolling_Future_Return_1d R-squared: 0.999

Model: OLS Adj. R-squared: 0.999

Method: Least Squares F-statistic: 6.911e+06

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:32:36 Log-Likelihood: 33887.

No. Observations: 6713 AIC: -6.777e+04

Df Residuals: 6711 BIC: -6.776e+04

Df Model: 1

Covariance Type: nonrobust

================================================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------------------------

const -5.384e-05 1.9e-05 -2.837 0.005 -9.1e-05 -1.66e-05

QQQ_Rolling_Future_Return_1d 2.9553 0.001 2628.911 0.000 2.953 2.957

==============================================================================

Omnibus: 10002.255 Durbin-Watson: 2.566

Prob(Omnibus): 0.000 Jarque-Bera (JB): 41625835.132

Skew: -8.172 Prob(JB): 0.00

Kurtosis: 388.424 Cond. No. 59.3

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

=========================================================================================

Dep. Variable: TQQQ_Rolling_Future_Return_1w R-squared: 0.994

Model: OLS Adj. R-squared: 0.994

Method: Least Squares F-statistic: 1.107e+06

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:32:39 Log-Likelihood: 22953.

No. Observations: 6709 AIC: -4.590e+04

Df Residuals: 6707 BIC: -4.589e+04

Df Model: 1

Covariance Type: nonrobust

================================================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------------------------

const -0.0008 9.68e-05 -8.295 0.000 -0.001 -0.001

QQQ_Rolling_Future_Return_1w 2.9534 0.003 1052.034 0.000 2.948 2.959

==============================================================================

Omnibus: 2724.426 Durbin-Watson: 0.939

Prob(Omnibus): 0.000 Jarque-Bera (JB): 599408.005

Skew: -0.772 Prob(JB): 0.00

Kurtosis: 49.280 Cond. No. 29.1

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

=========================================================================================

Dep. Variable: TQQQ_Rolling_Future_Return_1m R-squared: 0.982

Model: OLS Adj. R-squared: 0.982

Method: Least Squares F-statistic: 3.756e+05

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:32:43 Log-Likelihood: 14814.

No. Observations: 6693 AIC: -2.962e+04

Df Residuals: 6691 BIC: -2.961e+04

Df Model: 1

Covariance Type: nonrobust

================================================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------------------------

const -0.0034 0.000 -10.258 0.000 -0.004 -0.003

QQQ_Rolling_Future_Return_1m 2.9366 0.005 612.886 0.000 2.927 2.946

==============================================================================

Omnibus: 1708.914 Durbin-Watson: 0.308

Prob(Omnibus): 0.000 Jarque-Bera (JB): 79259.198

Skew: 0.422 Prob(JB): 0.00

Kurtosis: 19.837 Cond. No. 14.8

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

=========================================================================================

Dep. Variable: TQQQ_Rolling_Future_Return_3m R-squared: 0.957

Model: OLS Adj. R-squared: 0.957

Method: Least Squares F-statistic: 1.486e+05

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:32:47 Log-Likelihood: 8047.1

No. Observations: 6651 AIC: -1.609e+04

Df Residuals: 6649 BIC: -1.608e+04

Df Model: 1

Covariance Type: nonrobust

================================================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------------------------

const -0.0076 0.001 -8.388 0.000 -0.009 -0.006

QQQ_Rolling_Future_Return_3m 2.9610 0.008 385.431 0.000 2.946 2.976

==============================================================================

Omnibus: 3434.679 Durbin-Watson: 0.113

Prob(Omnibus): 0.000 Jarque-Bera (JB): 87217.860

Skew: 1.941 Prob(JB): 0.00

Kurtosis: 20.310 Cond. No. 8.69

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

=========================================================================================

Dep. Variable: TQQQ_Rolling_Future_Return_6m R-squared: 0.921

Model: OLS Adj. R-squared: 0.921

Method: Least Squares F-statistic: 7.644e+04

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:32:50 Log-Likelihood: 3210.4

No. Observations: 6588 AIC: -6417.

Df Residuals: 6586 BIC: -6403.

Df Model: 1

Covariance Type: nonrobust

================================================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------------------------

const -0.0048 0.002 -2.481 0.013 -0.009 -0.001

QQQ_Rolling_Future_Return_6m 2.9627 0.011 276.474 0.000 2.942 2.984

==============================================================================

Omnibus: 4217.455 Durbin-Watson: 0.065

Prob(Omnibus): 0.000 Jarque-Bera (JB): 103404.384

Skew: 2.663 Prob(JB): 0.00

Kurtosis: 21.664 Cond. No. 5.87

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

=========================================================================================

Dep. Variable: TQQQ_Rolling_Future_Return_1y R-squared: 0.894

Model: OLS Adj. R-squared: 0.894

Method: Least Squares F-statistic: 5.421e+04

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:32:54 Log-Likelihood: -123.96

No. Observations: 6462 AIC: 251.9

Df Residuals: 6460 BIC: 265.5

Df Model: 1

Covariance Type: nonrobust

================================================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------------------------

const 0.0229 0.003 6.693 0.000 0.016 0.030

QQQ_Rolling_Future_Return_1y 2.8138 0.012 232.837 0.000 2.790 2.838

==============================================================================

Omnibus: 2629.651 Durbin-Watson: 0.052

Prob(Omnibus): 0.000 Jarque-Bera (JB): 28944.026

Skew: 1.637 Prob(JB): 0.00

Kurtosis: 12.837 Cond. No. 4.00

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

=========================================================================================

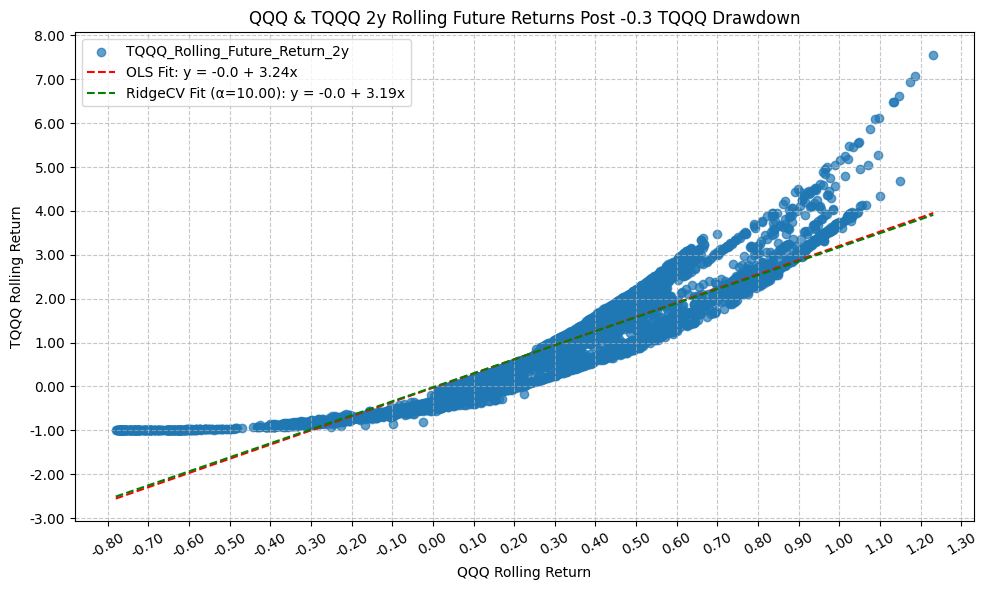

Dep. Variable: TQQQ_Rolling_Future_Return_2y R-squared: 0.847

Model: OLS Adj. R-squared: 0.847

Method: Least Squares F-statistic: 3.430e+04

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:32:57 Log-Likelihood: -4303.6

No. Observations: 6210 AIC: 8611.

Df Residuals: 6208 BIC: 8625.

Df Model: 1

Covariance Type: nonrobust

================================================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------------------------

const -0.0215 0.008 -2.822 0.005 -0.036 -0.007

QQQ_Rolling_Future_Return_2y 3.1933 0.017 185.210 0.000 3.159 3.227

==============================================================================

Omnibus: 1695.855 Durbin-Watson: 0.019

Prob(Omnibus): 0.000 Jarque-Bera (JB): 4735.104

Skew: 1.441 Prob(JB): 0.00

Kurtosis: 6.161 Cond. No. 3.03

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

=========================================================================================

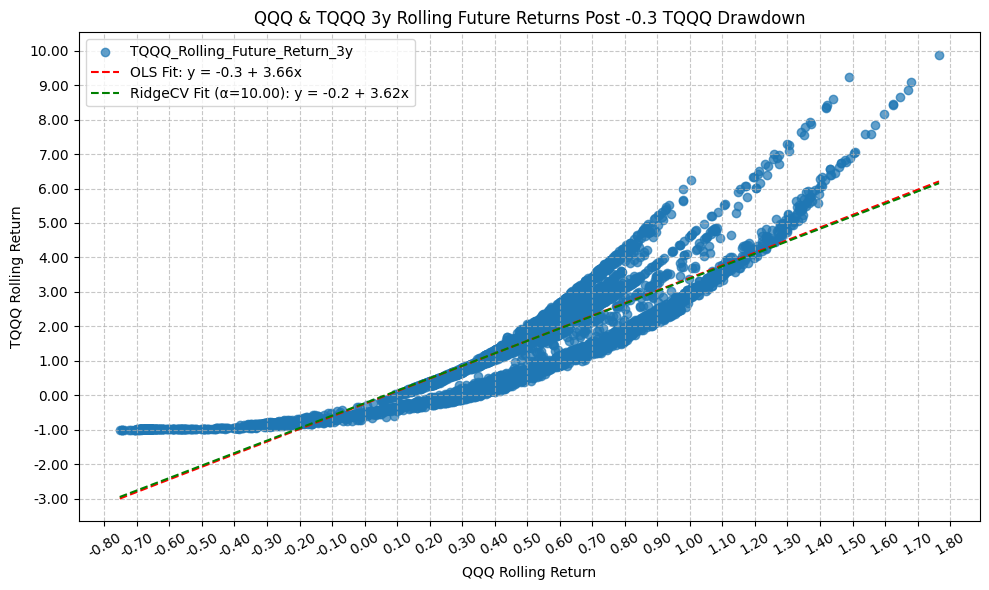

Dep. Variable: TQQQ_Rolling_Future_Return_3y R-squared: 0.814

Model: OLS Adj. R-squared: 0.814

Method: Least Squares F-statistic: 2.606e+04

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:33:01 Log-Likelihood: -6413.7

No. Observations: 5958 AIC: 1.283e+04

Df Residuals: 5956 BIC: 1.284e+04

Df Model: 1

Covariance Type: nonrobust

================================================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------------------------

const -0.1595 0.013 -12.233 0.000 -0.185 -0.134

QQQ_Rolling_Future_Return_3y 3.5008 0.022 161.442 0.000 3.458 3.543

==============================================================================

Omnibus: 890.338 Durbin-Watson: 0.015

Prob(Omnibus): 0.000 Jarque-Bera (JB): 1586.185

Skew: 0.965 Prob(JB): 0.00

Kurtosis: 4.632 Cond. No. 2.86

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

=========================================================================================

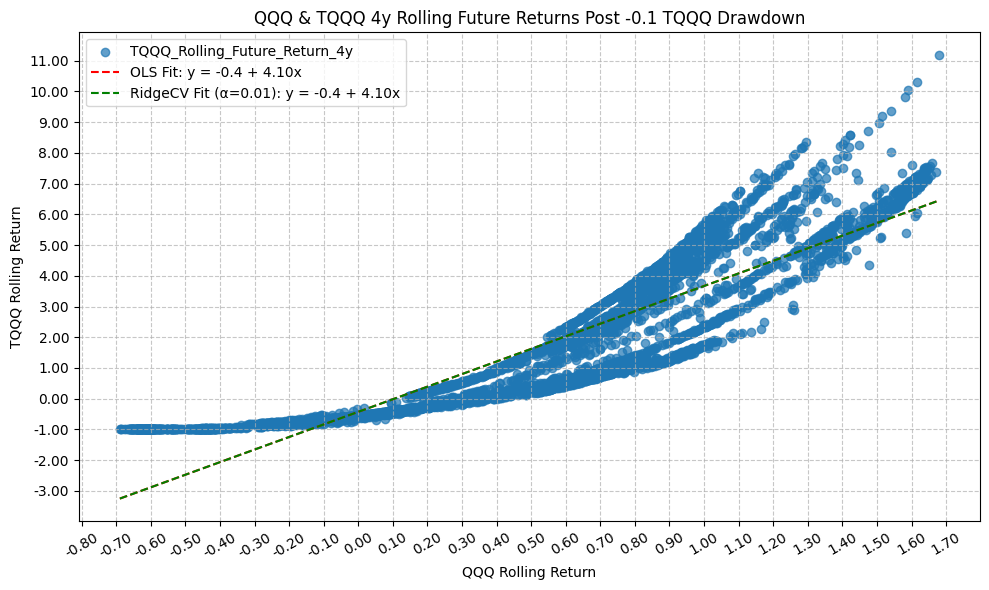

Dep. Variable: TQQQ_Rolling_Future_Return_4y R-squared: 0.779

Model: OLS Adj. R-squared: 0.779

Method: Least Squares F-statistic: 2.015e+04

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:33:06 Log-Likelihood: -8622.3

No. Observations: 5706 AIC: 1.725e+04

Df Residuals: 5704 BIC: 1.726e+04

Df Model: 1

Covariance Type: nonrobust

================================================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------------------------

const -0.4278 0.023 -18.865 0.000 -0.472 -0.383

QQQ_Rolling_Future_Return_4y 4.0704 0.029 141.956 0.000 4.014 4.127

==============================================================================

Omnibus: 148.305 Durbin-Watson: 0.010

Prob(Omnibus): 0.000 Jarque-Bera (JB): 90.147

Skew: 0.162 Prob(JB): 2.66e-20

Kurtosis: 2.476 Cond. No. 2.86

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

=========================================================================================

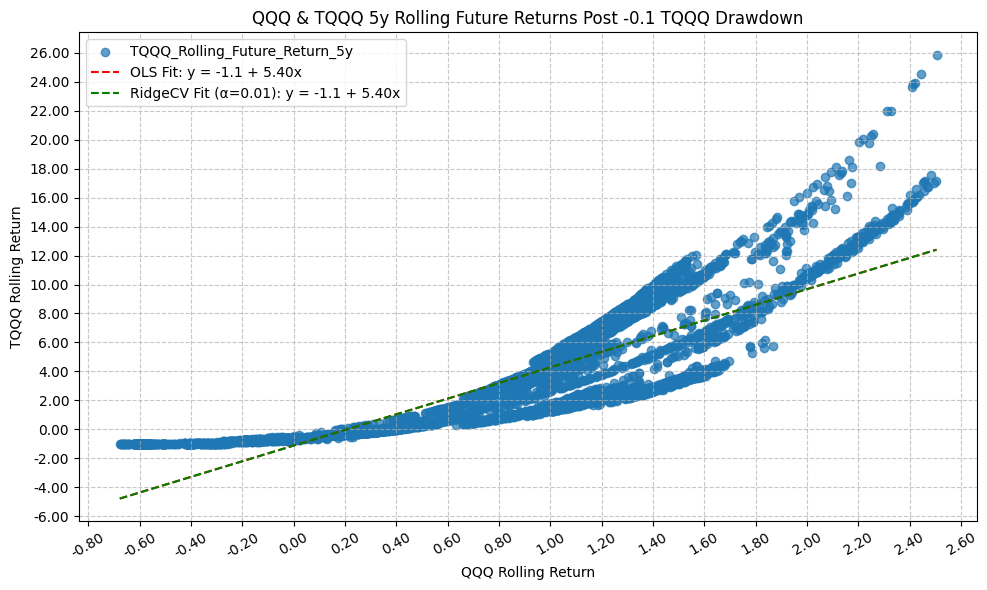

Dep. Variable: TQQQ_Rolling_Future_Return_5y R-squared: 0.741

Model: OLS Adj. R-squared: 0.741

Method: Least Squares F-statistic: 1.558e+04

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:33:11 Log-Likelihood: -11885.

No. Observations: 5454 AIC: 2.377e+04

Df Residuals: 5452 BIC: 2.379e+04

Df Model: 1

Covariance Type: nonrobust

================================================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------------------------

const -1.1362 0.047 -24.162 0.000 -1.228 -1.044

QQQ_Rolling_Future_Return_5y 5.3839 0.043 124.822 0.000 5.299 5.469

==============================================================================

Omnibus: 283.895 Durbin-Watson: 0.009

Prob(Omnibus): 0.000 Jarque-Bera (JB): 407.097

Skew: 0.473 Prob(JB): 3.98e-89

Kurtosis: 3.946 Cond. No. 2.92

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

=========================================================================================

Dep. Variable: TQQQ_Rolling_Future_Return_1d R-squared: 0.999

Model: OLS Adj. R-squared: 0.999

Method: Least Squares F-statistic: 6.673e+06

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:33:15 Log-Likelihood: 33428.

No. Observations: 6630 AIC: -6.685e+04

Df Residuals: 6628 BIC: -6.684e+04

Df Model: 1

Covariance Type: nonrobust

================================================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------------------------

const -5.435e-05 1.92e-05 -2.829 0.005 -9.2e-05 -1.67e-05

QQQ_Rolling_Future_Return_1d 2.9552 0.001 2583.241 0.000 2.953 2.957

==============================================================================

Omnibus: 9847.883 Durbin-Watson: 2.566

Prob(Omnibus): 0.000 Jarque-Bera (JB): 40121425.142

Skew: -8.123 Prob(JB): 0.00

Kurtosis: 383.752 Cond. No. 59.6

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

=========================================================================================

Dep. Variable: TQQQ_Rolling_Future_Return_1w R-squared: 0.994

Model: OLS Adj. R-squared: 0.994

Method: Least Squares F-statistic: 1.085e+06

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:33:19 Log-Likelihood: 22679.

No. Observations: 6627 AIC: -4.535e+04

Df Residuals: 6625 BIC: -4.534e+04

Df Model: 1

Covariance Type: nonrobust

================================================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------------------------

const -0.0008 9.73e-05 -8.044 0.000 -0.001 -0.001

QQQ_Rolling_Future_Return_1w 2.9524 0.003 1041.850 0.000 2.947 2.958

==============================================================================

Omnibus: 2728.411 Durbin-Watson: 0.932

Prob(Omnibus): 0.000 Jarque-Bera (JB): 607972.381

Skew: -0.798 Prob(JB): 0.00

Kurtosis: 49.896 Cond. No. 29.2

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

=========================================================================================

Dep. Variable: TQQQ_Rolling_Future_Return_1m R-squared: 0.983

Model: OLS Adj. R-squared: 0.983

Method: Least Squares F-statistic: 3.754e+05

Date: Wed, 17 Jun 2026 Prob (F-statistic): 0.00

Time: 14:33:22 Log-Likelihood: 14767.

No. Observations: 6616 AIC: -2.953e+04

Df Residuals: 6614 BIC: -2.952e+04

Df Model: 1

Covariance Type: nonrobust

================================================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------------------------

const -0.0034 0.000 -10.499 0.000 -0.004 -0.003

QQQ_Rolling_Future_Return_1m 2.9290 0.005 612.735 0.000 2.920 2.938

==============================================================================

Omnibus: 1557.724 Durbin-Watson: 0.313

Prob(Omnibus): 0.000 Jarque-Bera (JB): 79422.712

Skew: 0.204 Prob(JB): 0.00

Kurtosis: 19.969 Cond. No. 15.0

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

=========================================================================================