Performance Of Various Asset Classes During Fed Policy Cycles

Table of Contents

Introduction #

In this post, we will look into the Fed Funds cycles and evaluate asset class performance during tightening and easing of monetary policy. We’ll pull data for stocks, bonds (IG and HY), and gold, and analyze their returns during different phases of the Fed Funds cycle. We’ll also establish a simple strategy and allocate capital to a specific asset based on the current phase of the cycle, and evaluate the performance of this strategy over time.

Python Imports #

# Standard Library

import datetime

import os

import sys

import warnings

from datetime import datetime

from pathlib import Path

# Data Handling

import numpy as np

import pandas as pd

# Data Sources

import pandas_datareader.data as web

# Statistical Analysis

import statsmodels.api as sm

# Suppress warnings

warnings.filterwarnings("ignore")

# Add the source subdirectory to the system path to allow import config from settings.py

current_directory = Path(os.getcwd())

website_base_directory = current_directory.parent.parent.parent

src_directory = website_base_directory / "src"

sys.path.append(str(src_directory)) if str(src_directory) not in sys.path else None

# Import settings.py

from settings import config

# Add configured directories from config to path

SOURCE_DIR = config("SOURCE_DIR")

sys.path.append(str(Path(SOURCE_DIR))) if str(Path(SOURCE_DIR)) not in sys.path else None

# Add other configured directories

BASE_DIR = config("BASE_DIR")

CONTENT_DIR = config("CONTENT_DIR")

POSTS_DIR = config("POSTS_DIR")

PAGES_DIR = config("PAGES_DIR")

PUBLIC_DIR = config("PUBLIC_DIR")

SOURCE_DIR = config("SOURCE_DIR")

DATA_DIR = config("DATA_DIR")

DATA_MANUAL_DIR = config("DATA_MANUAL_DIR")

Python Functions #

Here are the functions needed for this project:

- bb_clean_data: Takes an Excel export from Bloomberg, removes the miscellaneous headings/rows, and returns a DataFrame.

- calc_fed_cycle_asset_performance: Calculates metrics for an asset based on a specified Fed tightening/easing cycle.

- load_data: Load data from a CSV, Excel, or Pickle file into a pandas DataFrame.

- pandas_set_decimal_places: Set the number of decimal places displayed for floating-point numbers in pandas.

- plot_bar_returns_ffr_change: Plot the bar chart of the cumulative or annualized returns for the asset class along with the change in the Fed Funds Rate.

- plot_scatter_regression_ffr_vs_returns: Plot the scatter plot and regression of the annualized return for the asset class along with the annualized change in the Fed Funds Rate.

- plot_time_series: Plot the time series data from a DataFrame for a specified date range and columns.

- summary_stats: Generate summary statistics for a series of returns.

from bb_clean_data import bb_clean_data

from calc_fed_cycle_asset_performance import calc_fed_cycle_asset_performance

from load_data import load_data

from pandas_set_decimal_places import pandas_set_decimal_places

from plot_bar_returns_ffr_change import plot_bar_returns_ffr_change

from plot_scatter_regression_ffr_vs_returns import plot_scatter_regression_ffr_vs_returns

from plot_time_series import plot_time_series

from summary_stats import summary_stats

Data Overview #

Acquire & Plot Fed Funds Data #

First, let’s get the data for the Fed Funds target rate (FFR). This data is found in 3 different datasets from FRED.

# Set decimal places

pandas_set_decimal_places(4)

# Pull Federal Funds Target Rate (DISCONTINUED) (DFEDTAR)

fedfunds_target_old = web.DataReader("DFEDTAR", "fred", start="1900-01-01", end=datetime.today())

# Pull Federal Funds Target Range - Upper Limit (DFEDTARU)

fedfunds_target_new_upper = web.DataReader("DFEDTARU", "fred", start="1900-01-01", end=datetime.today())

# Pull Federal Funds Target Range - Lower Limit (DFEDTARL)

fedfunds_target_new_lower = web.DataReader("DFEDTARL", "fred", start="1900-01-01", end=datetime.today())

# Merge the datasets together

fedfunds_combined = pd.concat([fedfunds_target_old, fedfunds_target_new_upper, fedfunds_target_new_lower], axis=1)

# Divide all values by 100 to get decimal rates

for col in fedfunds_combined.columns:

fedfunds_combined[col] = fedfunds_combined[col] / 100

# Resample to month-end (as if we know the rate at the end of the month)

fedfunds_monthly = fedfunds_combined.resample("ME").last()

display(fedfunds_monthly)

| DFEDTAR | DFEDTARU | DFEDTARL | |

|---|---|---|---|

| DATE | |||

| 1982-09-30 | 0.1025 | NaN | NaN |

| 1982-10-31 | 0.0950 | NaN | NaN |

| 1982-11-30 | 0.0900 | NaN | NaN |

| 1982-12-31 | 0.0850 | NaN | NaN |

| 1983-01-31 | 0.0850 | NaN | NaN |

| ... | ... | ... | ... |

| 2025-11-30 | NaN | 0.0400 | 0.0375 |

| 2025-12-31 | NaN | 0.0375 | 0.0350 |

| 2026-01-31 | NaN | 0.0375 | 0.0350 |

| 2026-02-28 | NaN | 0.0375 | 0.0350 |

| 2026-03-31 | NaN | 0.0375 | 0.0350 |

523 rows × 3 columns

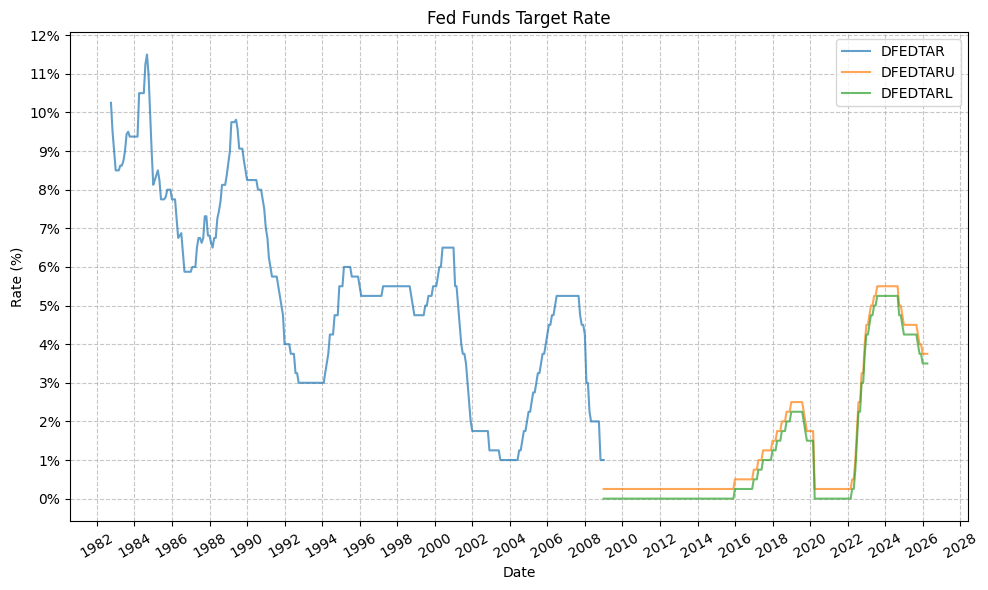

We can then generate several useful plots. First, the Fed Funds target rate:

plot_time_series(

df=fedfunds_monthly,

plot_start_date=None,

plot_end_date=None,

plot_columns=["DFEDTAR", "DFEDTARU", "DFEDTARL"],

title="Fed Funds Target Rate",

x_label="Date",

x_format="Year",

x_tick_spacing=2,

x_tick_rotation=30,

y_label="Rate (%)",

y_format="Percentage",

y_format_decimal_places=0,

y_tick_spacing=0.01,

y_tick_rotation=0,

grid=True,

legend=True,

export_plot=False,

plot_file_name=None,

)

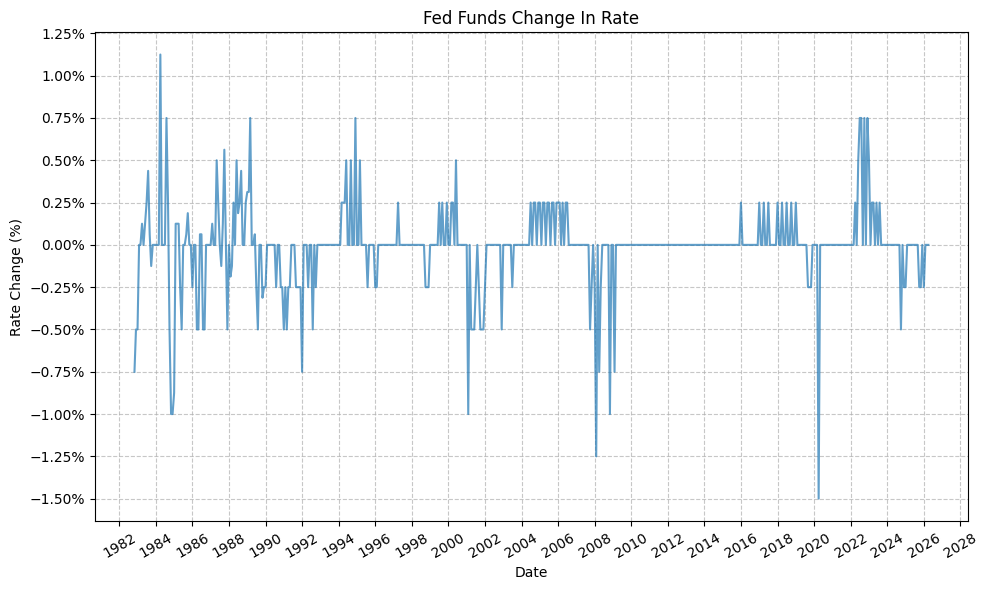

# First drop the lower column and merge

fedfunds_monthly["fed_funds"] = fedfunds_monthly["DFEDTAR"].combine_first(fedfunds_monthly["DFEDTARU"])

fedfunds_monthly = fedfunds_monthly.drop(columns=["DFEDTARL", "DFEDTARU", "DFEDTAR"])

# Compute change in rate from either column

fedfunds_monthly["fed_funds_change"] = fedfunds_monthly["fed_funds"].diff()

display(fedfunds_monthly)

| fed_funds | fed_funds_change | |

|---|---|---|

| DATE | ||

| 1982-09-30 | 0.1025 | NaN |

| 1982-10-31 | 0.0950 | -0.0075 |

| 1982-11-30 | 0.0900 | -0.0050 |

| 1982-12-31 | 0.0850 | -0.0050 |

| 1983-01-31 | 0.0850 | 0.0000 |

| ... | ... | ... |

| 2025-11-30 | 0.0400 | 0.0000 |

| 2025-12-31 | 0.0375 | -0.0025 |

| 2026-01-31 | 0.0375 | 0.0000 |

| 2026-02-28 | 0.0375 | 0.0000 |

| 2026-03-31 | 0.0375 | 0.0000 |

523 rows × 2 columns

And then the change in FFR from month-to-month:

plot_time_series(

df=fedfunds_monthly,

plot_start_date=None,

plot_end_date=None,

plot_columns=["fed_funds_change"],

title="Fed Funds Change In Rate",

x_label="Date",

x_format="Year",

x_tick_spacing=2,

x_tick_rotation=30,

y_label="Rate Change (%)",

y_format="Percentage",

y_format_decimal_places=2,

y_tick_spacing=0.0025,

y_tick_rotation=0,

grid=True,

legend=False,

export_plot=False,

plot_file_name=None,

)

This plot, in particular, makes it easy to show the monthly increase and decrease in the FFR, as well as the magnitude of the change (i.e. slow, drawn-out increases or decreases or abrupt large increases or decreases).

Define Fed Policy Cycles #

Next, we will define the Fed policy tightening and easing cycles:

# Set timeframe

start_date = "1989-12-15"

end_date = "2026-01-31"

# Copy DataFrame to avoid modifying original

fedfunds_cycles = fedfunds_monthly.copy()

fedfunds_cycles = fedfunds_cycles.loc[start_date:end_date]

# Reset index

fedfunds_cycles = fedfunds_cycles.reset_index()

# Drop the "fed_funds_change" column as we will use it to determine the cycle type later, but we don't need it in the final dataframe

fedfunds_cycles = fedfunds_cycles.drop(columns=["fed_funds_change"])

# Rename the date column to "Start Date", and the "fed_funds" column to "Fed Funds Start"

fedfunds_cycles = fedfunds_cycles.rename(columns={"DATE": "start_date", "fed_funds": "fed_funds_start"})

# Copy the "Start Date" column to a new column called "End Date" and shift it up by one row

fedfunds_cycles["end_date"] = fedfunds_cycles["start_date"].shift(-1)

# Copy the "Fed Funds Start" column to a new column called "Fed Funds End" and shift it up by one row

fedfunds_cycles["fed_funds_end"] = fedfunds_cycles["fed_funds_start"].shift(-1)

# Calculate the change in Fed Funds rate for each cycle

fedfunds_cycles["fed_funds_change"] = fedfunds_cycles["fed_funds_end"] - fedfunds_cycles["fed_funds_start"]

# Based on "Fed Funds Change" column, determine if the rate is increasing, decreasing, or unchanged

fedfunds_cycles["cycle"] = fedfunds_cycles["fed_funds_change"].apply(

lambda x: "Tightening" if x > 0 else ("Easing" if x < 0 else "Neutral"))

display(fedfunds_cycles)

| start_date | fed_funds_start | end_date | fed_funds_end | fed_funds_change | cycle | |

|---|---|---|---|---|---|---|

| 0 | 1989-12-31 | 0.0825 | 1990-01-31 | 0.0825 | 0.0000 | Neutral |

| 1 | 1990-01-31 | 0.0825 | 1990-02-28 | 0.0825 | 0.0000 | Neutral |

| 2 | 1990-02-28 | 0.0825 | 1990-03-31 | 0.0825 | 0.0000 | Neutral |

| 3 | 1990-03-31 | 0.0825 | 1990-04-30 | 0.0825 | 0.0000 | Neutral |

| 4 | 1990-04-30 | 0.0825 | 1990-05-31 | 0.0825 | 0.0000 | Neutral |

| ... | ... | ... | ... | ... | ... | ... |

| 429 | 2025-09-30 | 0.0425 | 2025-10-31 | 0.0400 | -0.0025 | Easing |

| 430 | 2025-10-31 | 0.0400 | 2025-11-30 | 0.0400 | 0.0000 | Neutral |

| 431 | 2025-11-30 | 0.0400 | 2025-12-31 | 0.0375 | -0.0025 | Easing |

| 432 | 2025-12-31 | 0.0375 | 2026-01-31 | 0.0375 | 0.0000 | Neutral |

| 433 | 2026-01-31 | 0.0375 | NaT | NaN | NaN | Neutral |

434 rows × 6 columns

Grouping the consecutive months of tightening and easing together, we can create a DataFrame that gives us the cumulative change in the FFR for each cycle, as well as the start and end dates for each cycle. This will be useful for evaluating asset class performance during these cycles.

fedfunds_grouped_cycles = fedfunds_cycles.copy()

# Create a group key that increments whenever the Cycle value changes

fedfunds_grouped_cycles['group'] = (fedfunds_grouped_cycles['cycle'] != fedfunds_grouped_cycles['cycle'].shift(1)).cumsum()

# Group by both the group key and Cycle label

cycle_ranges = (

fedfunds_grouped_cycles.groupby(['group', 'cycle'], sort=False)

.agg(

start_date=('start_date', 'first'),

end_date=('end_date', 'last'),

fed_funds_start=('fed_funds_start', 'first'),

fed_funds_end=('fed_funds_end', 'last')

)

.reset_index(drop=False)

.drop(columns='group')

)

display(cycle_ranges)

| cycle | start_date | end_date | fed_funds_start | fed_funds_end | |

|---|---|---|---|---|---|

| 0 | Neutral | 1989-12-31 | 1990-06-30 | 0.0825 | 0.0825 |

| 1 | Easing | 1990-06-30 | 1990-07-31 | 0.0825 | 0.0800 |

| 2 | Neutral | 1990-07-31 | 1990-09-30 | 0.0800 | 0.0800 |

| 3 | Easing | 1990-09-30 | 1991-04-30 | 0.0800 | 0.0575 |

| 4 | Neutral | 1991-04-30 | 1991-07-31 | 0.0575 | 0.0575 |

| ... | ... | ... | ... | ... | ... |

| 116 | Neutral | 2024-12-31 | 2025-08-31 | 0.0450 | 0.0450 |

| 117 | Easing | 2025-08-31 | 2025-10-31 | 0.0450 | 0.0400 |

| 118 | Neutral | 2025-10-31 | 2025-11-30 | 0.0400 | 0.0400 |

| 119 | Easing | 2025-11-30 | 2025-12-31 | 0.0400 | 0.0375 |

| 120 | Neutral | 2025-12-31 | 2026-01-31 | 0.0375 | 0.0375 |

121 rows × 5 columns

Furthermore, we will make the assumption that any “Neutral” months (i.e. months where the FFR did not change) are part of the preceding cycle – to a point. For example, if we have a tightening month followed by a neutral month, we will consider the neutral month to be part of the tightening cycle. This is a simplifying assumption, but it allows us to categorize all months into either tightening or easing cycles without having to create a separate category for neutral months. From a practical standpoint, this also makes it easier to evaluate asset class performance during these cycles, as we can simply look at the performance during the tightening and easing cycles without having to worry about the neutral months. We will foward fill no more than 6 months of neutral months, however, as it would be unreasonable to assume that a month of neutral policy is part of the preceding cycle if it has been 6 months since the last change in policy.

fedfunds_grouped_cycles = fedfunds_cycles.copy()

# Forward fill cycle labels preceding "Neutral" cycles

fedfunds_grouped_cycles['cycle_filled'] = fedfunds_grouped_cycles['cycle'].replace('Neutral', pd.NA).ffill(limit=6)

# Replaced any remaining <NA> values with "Modified Tightening"

fedfunds_grouped_cycles['cycle_filled'] = fedfunds_grouped_cycles['cycle_filled'].fillna('Modified Tightening')

# Create a group key that increments whenever the Cycle value changes

fedfunds_grouped_cycles['group'] = (fedfunds_grouped_cycles['cycle_filled'] != fedfunds_grouped_cycles['cycle_filled'].shift(1)).cumsum()

# Group by both the group key and Cycle label

cycle_ranges = (

fedfunds_grouped_cycles.groupby(['group', 'cycle_filled'], sort=False)

.agg(

start_date=('start_date', 'first'),

end_date=('end_date', 'last'),

fed_funds_start=('fed_funds_start', 'first'),

fed_funds_end=('fed_funds_end', 'last')

)

.reset_index(drop=False)

.drop(columns='group')

)

# Calc change in Fed Funds rate for each cycle

cycle_ranges["fed_funds_change"] = cycle_ranges["fed_funds_end"] - cycle_ranges["fed_funds_start"]

# Add cycle labels

cycle_labels = [f"Cycle {i+1}" for i in range(len(cycle_ranges))]

# Combine labels with cycle_ranges

cycle_ranges['cycle_label'] = cycle_labels

display(cycle_ranges)

| cycle_filled | start_date | end_date | fed_funds_start | fed_funds_end | fed_funds_change | cycle_label | |

|---|---|---|---|---|---|---|---|

| 0 | Modified Tightening | 1989-12-31 | 1990-06-30 | 0.0825 | 0.0825 | 0.0000 | Cycle 1 |

| 1 | Easing | 1990-06-30 | 1993-03-31 | 0.0825 | 0.0300 | -0.0525 | Cycle 2 |

| 2 | Modified Tightening | 1993-03-31 | 1994-01-31 | 0.0300 | 0.0300 | 0.0000 | Cycle 3 |

| 3 | Tightening | 1994-01-31 | 1995-06-30 | 0.0300 | 0.0600 | 0.0300 | Cycle 4 |

| 4 | Easing | 1995-06-30 | 1996-07-31 | 0.0600 | 0.0525 | -0.0075 | Cycle 5 |

| 5 | Modified Tightening | 1996-07-31 | 1997-02-28 | 0.0525 | 0.0525 | 0.0000 | Cycle 6 |

| 6 | Tightening | 1997-02-28 | 1997-09-30 | 0.0525 | 0.0550 | 0.0025 | Cycle 7 |

| 7 | Modified Tightening | 1997-09-30 | 1998-08-31 | 0.0550 | 0.0550 | 0.0000 | Cycle 8 |

| 8 | Easing | 1998-08-31 | 1999-05-31 | 0.0550 | 0.0475 | -0.0075 | Cycle 9 |

| 9 | Tightening | 1999-05-31 | 2000-11-30 | 0.0475 | 0.0650 | 0.0175 | Cycle 10 |

| 10 | Modified Tightening | 2000-11-30 | 2000-12-31 | 0.0650 | 0.0650 | 0.0000 | Cycle 11 |

| 11 | Easing | 2000-12-31 | 2002-06-30 | 0.0650 | 0.0175 | -0.0475 | Cycle 12 |

| 12 | Modified Tightening | 2002-06-30 | 2002-10-31 | 0.0175 | 0.0175 | 0.0000 | Cycle 13 |

| 13 | Easing | 2002-10-31 | 2003-12-31 | 0.0175 | 0.0100 | -0.0075 | Cycle 14 |

| 14 | Modified Tightening | 2003-12-31 | 2004-05-31 | 0.0100 | 0.0100 | 0.0000 | Cycle 15 |

| 15 | Tightening | 2004-05-31 | 2006-12-31 | 0.0100 | 0.0525 | 0.0425 | Cycle 16 |

| 16 | Modified Tightening | 2006-12-31 | 2007-08-31 | 0.0525 | 0.0525 | 0.0000 | Cycle 17 |

| 17 | Easing | 2007-08-31 | 2009-07-31 | 0.0525 | 0.0025 | -0.0500 | Cycle 18 |

| 18 | Modified Tightening | 2009-07-31 | 2015-11-30 | 0.0025 | 0.0025 | 0.0000 | Cycle 19 |

| 19 | Tightening | 2015-11-30 | 2016-06-30 | 0.0025 | 0.0050 | 0.0025 | Cycle 20 |

| 20 | Modified Tightening | 2016-06-30 | 2016-11-30 | 0.0050 | 0.0050 | 0.0000 | Cycle 21 |

| 21 | Tightening | 2016-11-30 | 2019-06-30 | 0.0050 | 0.0250 | 0.0200 | Cycle 22 |

| 22 | Modified Tightening | 2019-06-30 | 2019-07-31 | 0.0250 | 0.0250 | 0.0000 | Cycle 23 |

| 23 | Easing | 2019-07-31 | 2020-09-30 | 0.0250 | 0.0025 | -0.0225 | Cycle 24 |

| 24 | Modified Tightening | 2020-09-30 | 2022-02-28 | 0.0025 | 0.0025 | 0.0000 | Cycle 25 |

| 25 | Tightening | 2022-02-28 | 2024-01-31 | 0.0025 | 0.0550 | 0.0525 | Cycle 26 |

| 26 | Modified Tightening | 2024-01-31 | 2024-08-31 | 0.0550 | 0.0550 | 0.0000 | Cycle 27 |

| 27 | Easing | 2024-08-31 | 2025-06-30 | 0.0550 | 0.0450 | -0.0100 | Cycle 28 |

| 28 | Modified Tightening | 2025-06-30 | 2025-08-31 | 0.0450 | 0.0450 | 0.0000 | Cycle 29 |

| 29 | Easing | 2025-08-31 | 2026-01-31 | 0.0450 | 0.0375 | -0.0075 | Cycle 30 |

Asset Class Performance By Fed Policy Cycle #

Moving on, we will now look at the performance of four (4) different asset classes during each Fed cycle. We’ll use the following Bloomberg indices:

- SPXT_S&P 500 Total Return Index (Stocks)

- SPBDU10T_S&P US Treasury Bond 7-10 Year Total Return Index (Bonds)

- LF98TRUU_Bloomberg US Corporate High Yield Total Return Index Value Unhedged USD (High Yield Bonds)

- XAU_Gold USD Spot (Gold)

Stocks #

First, we will clean and load the data for the S&P 500 Total Return Index (SPXT):

pandas_set_decimal_places(2)

bb_clean_data(

base_directory=DATA_DIR,

fund_ticker_name="SPXT_S&P 500 Total Return Index",

source="Bloomberg",

asset_class="Indices",

excel_export=True,

pickle_export=True,

output_confirmation=False,

)

spxt = load_data(

base_directory=DATA_DIR,

ticker="SPXT_S&P 500 Total Return Index_Clean",

source="Bloomberg",

asset_class="Indices",

timeframe="Daily",

file_format="pickle",

)

# Filter SPXT to date range

spxt = spxt[(spxt.index >= pd.to_datetime(start_date)) & (spxt.index <= pd.to_datetime(end_date))]

# Drop everything except the "close" column

spxt = spxt[["Close"]]

# Resample to monthly frequency

spxt_monthly = spxt.resample("M").last()

spxt_monthly["Monthly_Return"] = spxt_monthly["Close"].pct_change()

spxt_monthly = spxt_monthly.dropna()

display(spxt_monthly)

| Close | Monthly_Return | |

|---|---|---|

| Date | ||

| 1990-01-31 | 353.94 | -0.07 |

| 1990-02-28 | 358.50 | 0.01 |

| 1990-03-31 | 368 | 0.03 |

| 1990-04-30 | 358.81 | -0.02 |

| 1990-05-31 | 393.80 | 0.10 |

| ... | ... | ... |

| 2025-09-30 | 14826.80 | 0.04 |

| 2025-10-31 | 15173.95 | 0.02 |

| 2025-11-30 | 15211.14 | 0.00 |

| 2025-12-31 | 15220.45 | 0.00 |

| 2026-01-31 | 15441.15 | 0.01 |

433 rows × 2 columns

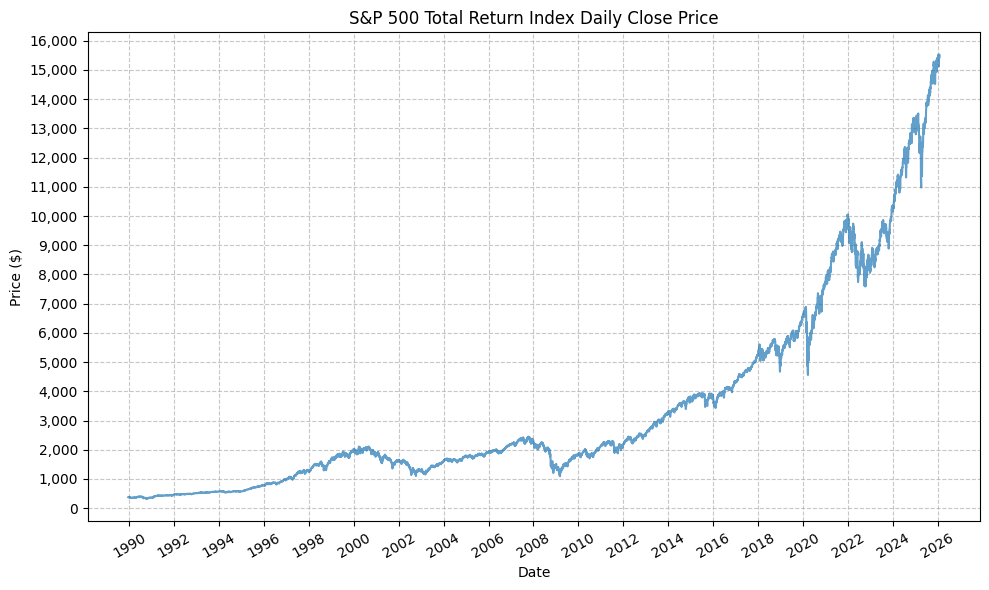

Next, we can plot the price history before calculating the cycle performance:

plot_time_series(

df=spxt,

plot_start_date=None,

plot_end_date=None,

plot_columns=["Close"],

title="S&P 500 Total Return Index Daily Close Price",

x_label="Date",

x_format="Year",

x_tick_spacing=2,

x_tick_rotation=30,

y_label="Price ($)",

y_format="Decimal",

y_format_decimal_places=0,

y_tick_spacing=1000,

y_tick_rotation=0,

grid=True,

legend=False,

export_plot=False,

plot_file_name=None,

)

Next, we will calculate the performance for SPY based on the pre-defined Fed cycles:

spxt_cycles = calc_fed_cycle_asset_performance(

start_date=cycle_ranges["start_date"],

end_date=cycle_ranges["end_date"],

label=cycle_ranges["cycle_label"],

fed_funds_change=cycle_ranges["fed_funds_change"],

monthly_returns=spxt_monthly,

)

display(spxt_cycles)

| Cycle | Start | End | Months | CumulativeReturn | CumulativeReturnPct | AverageMonthlyReturn | AverageMonthlyReturnPct | AnnualizedReturn | AnnualizedReturnPct | Volatility | FedFundsChange | FedFundsChange_bps | FFR_AnnualizedChange | FFR_AnnualizedChange_bps | Label | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | Cycle 1 | 1989-12-31 | 1990-06-30 | 6 | 0.03 | 3.09 | 0.01 | 0.63 | 0.06 | 6.28 | 0.19 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 1, 1989-12-31 to 1990-06-30 |

| 1 | Cycle 2 | 1990-06-30 | 1993-03-31 | 34 | 0.37 | 36.80 | 0.01 | 1.00 | 0.12 | 11.69 | 0.13 | -0.05 | -525.00 | -0.02 | -185.29 | Cycle 2, 1990-06-30 to 1993-03-31 |

| 2 | Cycle 3 | 1993-03-31 | 1994-01-31 | 11 | 0.11 | 11.36 | 0.01 | 1.00 | 0.12 | 12.45 | 0.07 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 3, 1993-03-31 to 1994-01-31 |

| 3 | Cycle 4 | 1994-01-31 | 1995-06-30 | 18 | 0.22 | 21.80 | 0.01 | 1.14 | 0.14 | 14.05 | 0.10 | 0.03 | 300.00 | 0.02 | 200.00 | Cycle 4, 1994-01-31 to 1995-06-30 |

| 4 | Cycle 5 | 1995-06-30 | 1996-07-31 | 14 | 0.23 | 23.23 | 0.02 | 1.53 | 0.20 | 19.61 | 0.08 | -0.01 | -75.00 | -0.01 | -64.29 | Cycle 5, 1995-06-30 to 1996-07-31 |

| 5 | Cycle 6 | 1996-07-31 | 1997-02-28 | 8 | 0.20 | 19.59 | 0.02 | 2.34 | 0.31 | 30.78 | 0.14 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 6, 1996-07-31 to 1997-02-28 |

| 6 | Cycle 7 | 1997-02-28 | 1997-09-30 | 8 | 0.22 | 22.02 | 0.03 | 2.63 | 0.35 | 34.78 | 0.18 | 0.00 | 25.00 | 0.00 | 37.50 | Cycle 7, 1997-02-28 to 1997-09-30 |

| 7 | Cycle 8 | 1997-09-30 | 1998-08-31 | 12 | 0.08 | 8.09 | 0.01 | 0.81 | 0.08 | 8.09 | 0.20 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 8, 1997-09-30 to 1998-08-31 |

| 8 | Cycle 9 | 1998-08-31 | 1999-05-31 | 10 | 0.18 | 17.55 | 0.02 | 1.85 | 0.21 | 21.42 | 0.24 | -0.01 | -75.00 | -0.01 | -90.00 | Cycle 9, 1998-08-31 to 1999-05-31 |

| 9 | Cycle 10 | 1999-05-31 | 2000-11-30 | 19 | 0.00 | 0.40 | 0.00 | 0.13 | 0.00 | 0.25 | 0.16 | 0.02 | 175.00 | 0.01 | 110.53 | Cycle 10, 1999-05-31 to 2000-11-30 |

| 10 | Cycle 11 | 2000-11-30 | 2000-12-31 | 2 | -0.07 | -7.43 | -0.04 | -3.70 | -0.37 | -37.09 | 0.21 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 11, 2000-11-30 to 2000-12-31 |

| 11 | Cycle 12 | 2000-12-31 | 2002-06-30 | 19 | -0.23 | -23.11 | -0.01 | -1.25 | -0.15 | -15.29 | 0.17 | -0.05 | -475.00 | -0.03 | -300.00 | Cycle 12, 2000-12-31 to 2002-06-30 |

| 12 | Cycle 13 | 2002-06-30 | 2002-10-31 | 5 | -0.16 | -16.41 | -0.03 | -3.27 | -0.35 | -34.96 | 0.28 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 13, 2002-06-30 to 2002-10-31 |

| 13 | Cycle 14 | 2002-10-31 | 2003-12-31 | 15 | 0.40 | 39.54 | 0.02 | 2.33 | 0.31 | 30.55 | 0.14 | -0.01 | -75.00 | -0.01 | -60.00 | Cycle 14, 2002-10-31 to 2003-12-31 |

| 14 | Cycle 15 | 2003-12-31 | 2004-05-31 | 6 | 0.07 | 6.79 | 0.01 | 1.13 | 0.14 | 14.04 | 0.09 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 15, 2003-12-31 to 2004-05-31 |

| 15 | Cycle 16 | 2004-05-31 | 2006-12-31 | 32 | 0.35 | 34.57 | 0.01 | 0.95 | 0.12 | 11.78 | 0.07 | 0.04 | 425.00 | 0.02 | 159.38 | Cycle 16, 2004-05-31 to 2006-12-31 |

| 16 | Cycle 17 | 2006-12-31 | 2007-08-31 | 9 | 0.07 | 6.67 | 0.01 | 0.75 | 0.09 | 8.99 | 0.09 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 17, 2006-12-31 to 2007-08-31 |

| 17 | Cycle 18 | 2007-08-31 | 2009-07-31 | 24 | -0.29 | -28.84 | -0.01 | -1.19 | -0.16 | -15.64 | 0.23 | -0.05 | -500.00 | -0.03 | -250.00 | Cycle 18, 2007-08-31 to 2009-07-31 |

| 18 | Cycle 19 | 2009-07-31 | 2015-11-30 | 77 | 1.59 | 159.04 | 0.01 | 1.31 | 0.16 | 15.99 | 0.13 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 19, 2009-07-31 to 2015-11-30 |

| 19 | Cycle 20 | 2015-11-30 | 2016-06-30 | 8 | 0.03 | 2.50 | 0.00 | 0.36 | 0.04 | 3.78 | 0.11 | 0.00 | 25.00 | 0.00 | 37.50 | Cycle 20, 2015-11-30 to 2016-06-30 |

| 20 | Cycle 21 | 2016-06-30 | 2016-11-30 | 6 | 0.06 | 6.01 | 0.01 | 1.00 | 0.12 | 12.38 | 0.08 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 21, 2016-06-30 to 2016-11-30 |

| 21 | Cycle 22 | 2016-11-30 | 2019-06-30 | 32 | 0.46 | 46.03 | 0.01 | 1.26 | 0.15 | 15.26 | 0.13 | 0.02 | 200.00 | 0.01 | 75.00 | Cycle 22, 2016-11-30 to 2019-06-30 |

| 22 | Cycle 23 | 2019-06-30 | 2019-07-31 | 2 | 0.09 | 8.59 | 0.04 | 4.24 | 0.64 | 63.93 | 0.14 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 23, 2019-06-30 to 2019-07-31 |

| 23 | Cycle 24 | 2019-07-31 | 2020-09-30 | 15 | 0.17 | 17.10 | 0.01 | 1.23 | 0.13 | 13.46 | 0.21 | -0.02 | -225.00 | -0.02 | -180.00 | Cycle 24, 2019-07-31 to 2020-09-30 |

| 24 | Cycle 25 | 2020-09-30 | 2022-02-28 | 18 | 0.28 | 27.73 | 0.01 | 1.46 | 0.18 | 17.72 | 0.15 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 25, 2020-09-30 to 2022-02-28 |

| 25 | Cycle 26 | 2022-02-28 | 2024-01-31 | 24 | 0.11 | 10.89 | 0.01 | 0.58 | 0.05 | 5.31 | 0.19 | 0.05 | 525.00 | 0.03 | 262.50 | Cycle 26, 2022-02-28 to 2024-01-31 |

| 26 | Cycle 27 | 2024-01-31 | 2024-08-31 | 8 | 0.20 | 19.53 | 0.02 | 2.29 | 0.31 | 30.68 | 0.10 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 27, 2024-01-31 to 2024-08-31 |

| 27 | Cycle 28 | 2024-08-31 | 2025-06-30 | 11 | 0.14 | 13.78 | 0.01 | 1.24 | 0.15 | 15.12 | 0.13 | -0.01 | -100.00 | -0.01 | -109.09 | Cycle 28, 2024-08-31 to 2025-06-30 |

| 28 | Cycle 29 | 2025-06-30 | 2025-08-31 | 3 | 0.10 | 9.62 | 0.03 | 3.12 | 0.44 | 44.41 | 0.06 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 29, 2025-06-30 to 2025-08-31 |

| 29 | Cycle 30 | 2025-08-31 | 2026-01-31 | 6 | 0.10 | 10.13 | 0.02 | 1.63 | 0.21 | 21.29 | 0.05 | -0.01 | -75.00 | -0.01 | -150.00 | Cycle 30, 2025-08-31 to 2026-01-31 |

This gives us the following data points:

- Cycle start date

- Cycle end date

- Number of months in the cycle

- Cumulative return during the cycle (decimal and percent)

- Average monthly return during the cycle (decimal and percent)

- Annualized return during the cycle (decimal and percent)

- Return volatility during the cycle

- Cumulative change in FFR during the cycle (decimal and basis points)

- Annualized change in FFR during the cycle (decimal and basis points)

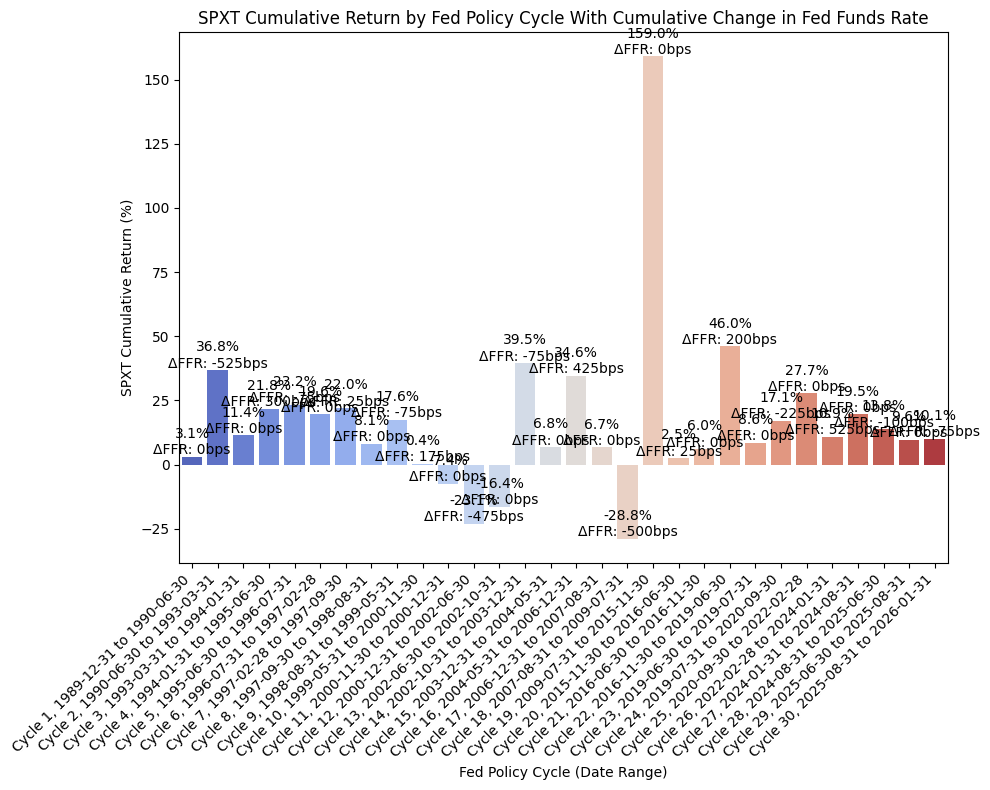

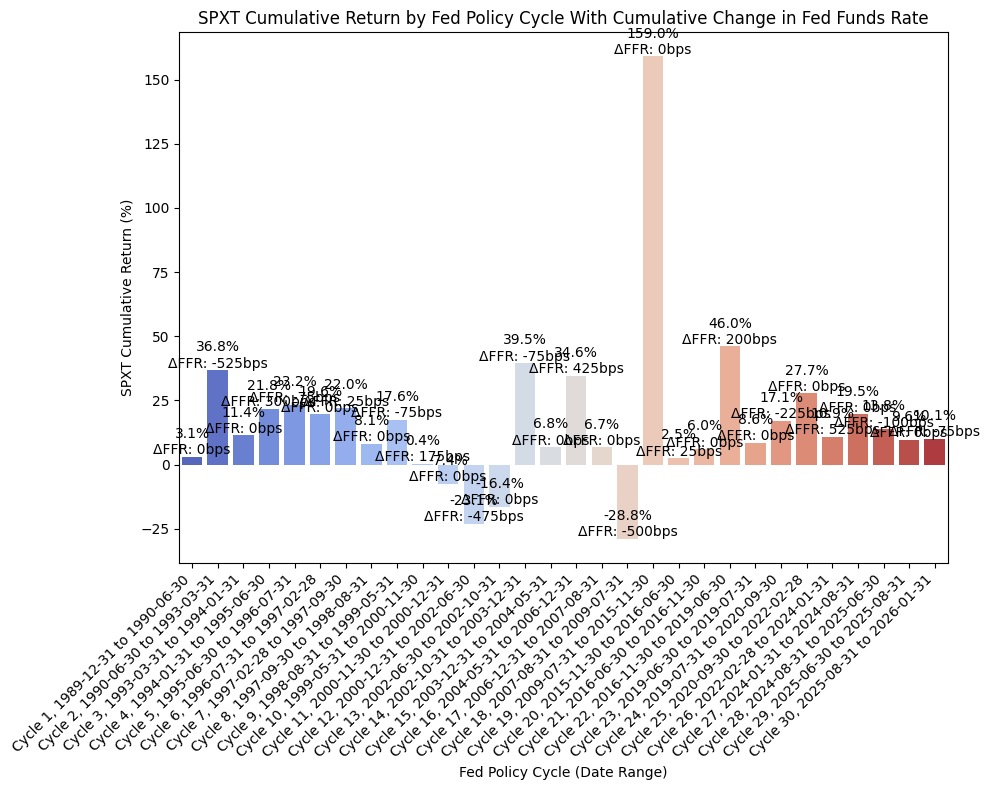

From the above DataFrame, we can then plot the cumulative and annualized returns for each cycle in a bar chart. First, the cumulative returns along with the cumulative change in FFR:

plot_bar_returns_ffr_change(

cycle_df=spxt_cycles,

asset_label="SPXT",

annualized_or_cumulative="Cumulative",

)

And then the annualized returns along with the annualized change in FFR:

plot_bar_returns_ffr_change(

cycle_df=spxt_cycles,

asset_label="SPXT",

annualized_or_cumulative="Annualized",

)

The cumulative returns plot is not particularly insightful, but there are some interesting observations to be gained from the annualized returns plot. During the past two (2) rate cutting cycles (cycles 11/12/13/14 and 18), stocks have exhibited negative returns during the rate cutting cycle. However, after the rate cutting cycle was complete, returns during the following cycle (when rates were usually flat) were quite strong and higher than the historical mean return for the S&P 500. The economic intuition for this behavior is valid; as the economy weakens, investors are concerned about the pricing of equities, the returns become negative, and the Fed responds with cutting rates. The exact timing of when the Fed begins cutting rates is one of the unknowns; the Fed could be ahead of the curve, cutting rates as economic data begins to prompt that action, or behind the curve, where the ecomony rolls over rapidly and even the Fed’s actions are not enough to halt the economic contraction.

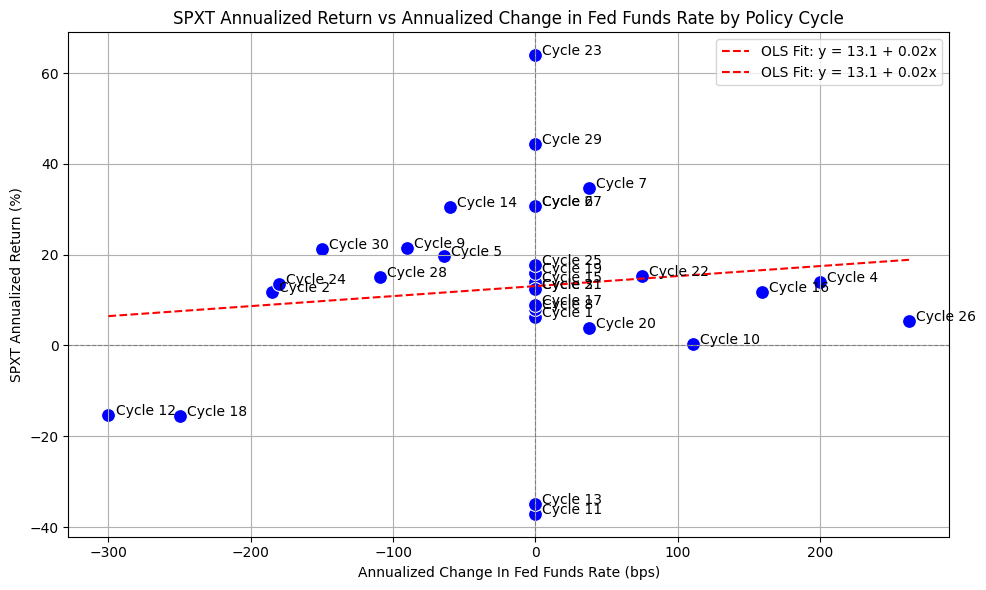

Finally, we can run an OLS regression to check fit:

df = spxt_cycles

#=== Don't modify below this line ===

# Run OLS regression with statsmodels

X = df["FFR_AnnualizedChange_bps"]

y = df["AnnualizedReturnPct"]

X = sm.add_constant(X)

model = sm.OLS(y, X).fit()

print(model.summary())

print(f"Intercept: {model.params[0]}, Slope: {model.params[1]}") # Intercept and slope

# Calc X and Y values for regression line

X_vals = np.linspace(X.min(), X.max(), 100)

Y_vals = model.params[0] + model.params[1] * X_vals

OLS Regression Results

===============================================================================

Dep. Variable: AnnualizedReturnPct R-squared: 0.017

Model: OLS Adj. R-squared: -0.018

Method: Least Squares F-statistic: 0.4786

Date: Mon, 23 Mar 2026 Prob (F-statistic): 0.495

Time: 22:08:21 Log-Likelihood: -132.24

No. Observations: 30 AIC: 268.5

Df Residuals: 28 BIC: 271.3

Df Model: 1

Covariance Type: nonrobust

============================================================================================

coef std err t P>|t| [0.025 0.975]

--------------------------------------------------------------------------------------------

const 13.0760 3.792 3.448 0.002 5.308 20.844

FFR_AnnualizedChange_bps 0.0221 0.032 0.692 0.495 -0.043 0.087

==============================================================================

Omnibus: 4.070 Durbin-Watson: 1.523

Prob(Omnibus): 0.131 Jarque-Bera (JB): 2.894

Skew: -0.320 Prob(JB): 0.235

Kurtosis: 4.381 Cond. No. 120.

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Intercept: 13.076015539043272, Slope: 0.022056651501767076

And then plot the regression line along with the values:

plot_scatter_regression_ffr_vs_returns(

cycle_df=spxt_cycles,

asset_label="SPXT",

x_vals=X_vals,

y_vals=Y_vals,

intercept=model.params[0],

slope=model.params[1],

)

Here we can see the data points for cycles 11/12/13/14 and 18 as mentioned above. Interestingly, cycles 28/29/30 (which is the current rate cutting cycle) appears to be an outlier. Of course, the book is not yet finished for cycles 28/29/30, and we could certainly see a bear market in stocks over the next several years.

Bonds #

Next, we’ll run a similar process for medium term bonds using SPBDU10T_S&P US Treasury Bond 7-10 Year Total Return Index.

First, we pull data with the following:

bb_clean_data(

base_directory=DATA_DIR,

fund_ticker_name="SPBDU10T_S&P US Treasury Bond 7-10 Year Total Return Index",

source="Bloomberg",

asset_class="Indices",

excel_export=True,

pickle_export=True,

output_confirmation=False,

)

treas_10y = load_data(

base_directory=DATA_DIR,

ticker="SPBDU10T_S&P US Treasury Bond 7-10 Year Total Return Index_Clean",

source="Bloomberg",

asset_class="Indices",

timeframe="Daily",

file_format="pickle",

)

# Filter TREAS_10Y to date range

treas_10y = treas_10y[(treas_10y.index >= pd.to_datetime(start_date)) & (treas_10y.index <= pd.to_datetime(end_date))]

# Drop everything except the "close" column

treas_10y = treas_10y[["Close"]]

# Resample to monthly frequency

treas_10y_monthly = treas_10y.resample("M").last()

treas_10y_monthly["Monthly_Return"] = treas_10y_monthly["Close"].pct_change()

treas_10y_monthly = treas_10y_monthly.dropna()

display(treas_10y_monthly)

| Close | Monthly_Return | |

|---|---|---|

| Date | ||

| 1990-01-31 | 98.01 | -0.02 |

| 1990-02-28 | 97.99 | -0.00 |

| 1990-03-31 | 97.99 | -0.00 |

| 1990-04-30 | 96.61 | -0.01 |

| 1990-05-31 | 99.65 | 0.03 |

| ... | ... | ... |

| 2025-09-30 | 645.58 | 0.01 |

| 2025-10-31 | 650.00 | 0.01 |

| 2025-11-30 | 656.64 | 0.01 |

| 2025-12-31 | 652.29 | -0.01 |

| 2026-01-31 | 650.17 | -0.00 |

433 rows × 2 columns

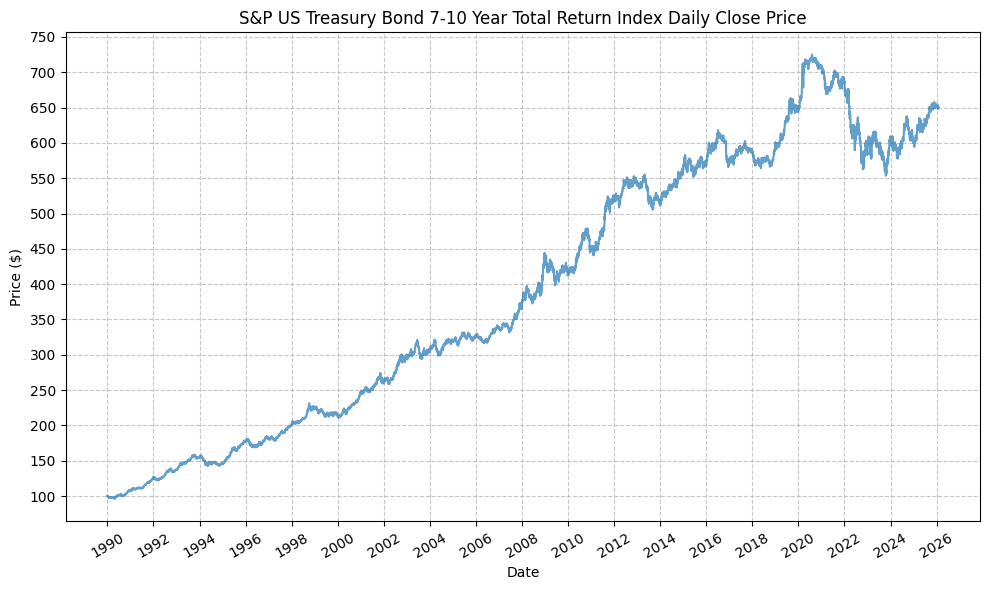

Next, we can plot the price history before calculating the cycle performance:

plot_time_series(

df=treas_10y,

plot_start_date=None,

plot_end_date=None,

plot_columns=["Close"],

title="S&P US Treasury Bond 7-10 Year Total Return Index Daily Close Price",

x_label="Date",

x_format="Year",

x_tick_spacing=2,

x_tick_rotation=30,

y_label="Price ($)",

y_format="Decimal",

y_format_decimal_places=0,

y_tick_spacing=50,

y_tick_rotation=0,

grid=True,

legend=False,

export_plot=False,

plot_file_name=None,

)

Next, we will calculate the performance for SPY based on the pre-defined Fed cycles:

treas_10y_cycles = calc_fed_cycle_asset_performance(

start_date=cycle_ranges["start_date"],

end_date=cycle_ranges["end_date"],

label=cycle_ranges["cycle_label"],

fed_funds_change=cycle_ranges["fed_funds_change"],

monthly_returns=treas_10y_monthly,

)

display(treas_10y_cycles)

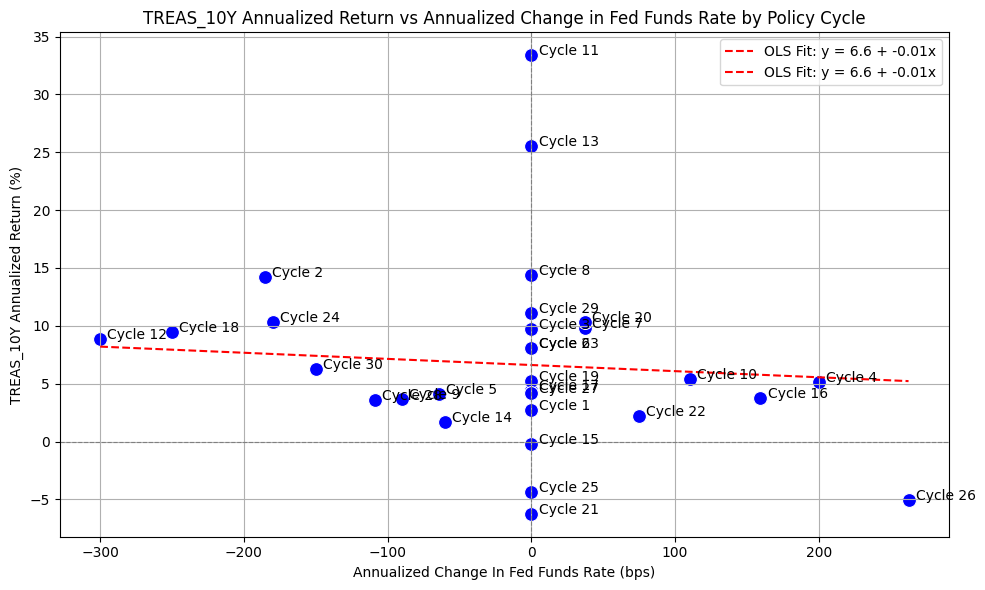

| Cycle | Start | End | Months | CumulativeReturn | CumulativeReturnPct | AverageMonthlyReturn | AverageMonthlyReturnPct | AnnualizedReturn | AnnualizedReturnPct | Volatility | FedFundsChange | FedFundsChange_bps | FFR_AnnualizedChange | FFR_AnnualizedChange_bps | Label | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | Cycle 1 | 1989-12-31 | 1990-06-30 | 6 | 0.01 | 1.36 | 0.00 | 0.24 | 0.03 | 2.74 | 0.07 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 1, 1989-12-31 to 1990-06-30 |

| 1 | Cycle 2 | 1990-06-30 | 1993-03-31 | 34 | 0.46 | 45.68 | 0.01 | 1.12 | 0.14 | 14.20 | 0.05 | -0.05 | -525.00 | -0.02 | -185.29 | Cycle 2, 1990-06-30 to 1993-03-31 |

| 2 | Cycle 3 | 1993-03-31 | 1994-01-31 | 11 | 0.09 | 8.88 | 0.01 | 0.78 | 0.10 | 9.72 | 0.04 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 3, 1993-03-31 to 1994-01-31 |

| 3 | Cycle 4 | 1994-01-31 | 1995-06-30 | 18 | 0.08 | 7.80 | 0.00 | 0.44 | 0.05 | 5.13 | 0.07 | 0.03 | 300.00 | 0.02 | 200.00 | Cycle 4, 1994-01-31 to 1995-06-30 |

| 4 | Cycle 5 | 1995-06-30 | 1996-07-31 | 14 | 0.05 | 4.78 | 0.00 | 0.34 | 0.04 | 4.09 | 0.05 | -0.01 | -75.00 | -0.01 | -64.29 | Cycle 5, 1995-06-30 to 1996-07-31 |

| 5 | Cycle 6 | 1996-07-31 | 1997-02-28 | 8 | 0.05 | 5.30 | 0.01 | 0.66 | 0.08 | 8.06 | 0.05 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 6, 1996-07-31 to 1997-02-28 |

| 6 | Cycle 7 | 1997-02-28 | 1997-09-30 | 8 | 0.06 | 6.45 | 0.01 | 0.80 | 0.10 | 9.83 | 0.06 | 0.00 | 25.00 | 0.00 | 37.50 | Cycle 7, 1997-02-28 to 1997-09-30 |

| 7 | Cycle 8 | 1997-09-30 | 1998-08-31 | 12 | 0.14 | 14.43 | 0.01 | 1.14 | 0.14 | 14.43 | 0.04 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 8, 1997-09-30 to 1998-08-31 |

| 8 | Cycle 9 | 1998-08-31 | 1999-05-31 | 10 | 0.03 | 3.05 | 0.00 | 0.33 | 0.04 | 3.67 | 0.08 | -0.01 | -75.00 | -0.01 | -90.00 | Cycle 9, 1998-08-31 to 1999-05-31 |

| 9 | Cycle 10 | 1999-05-31 | 2000-11-30 | 19 | 0.09 | 8.74 | 0.00 | 0.45 | 0.05 | 5.44 | 0.04 | 0.02 | 175.00 | 0.01 | 110.53 | Cycle 10, 1999-05-31 to 2000-11-30 |

| 10 | Cycle 11 | 2000-11-30 | 2000-12-31 | 2 | 0.05 | 4.92 | 0.02 | 2.43 | 0.33 | 33.39 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 11, 2000-11-30 to 2000-12-31 |

| 11 | Cycle 12 | 2000-12-31 | 2002-06-30 | 19 | 0.14 | 14.33 | 0.01 | 0.72 | 0.09 | 8.83 | 0.06 | -0.05 | -475.00 | -0.03 | -300.00 | Cycle 12, 2000-12-31 to 2002-06-30 |

| 12 | Cycle 13 | 2002-06-30 | 2002-10-31 | 5 | 0.10 | 9.94 | 0.02 | 1.93 | 0.26 | 25.55 | 0.07 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 13, 2002-06-30 to 2002-10-31 |

| 13 | Cycle 14 | 2002-10-31 | 2003-12-31 | 15 | 0.02 | 2.16 | 0.00 | 0.17 | 0.02 | 1.73 | 0.09 | -0.01 | -75.00 | -0.01 | -60.00 | Cycle 14, 2002-10-31 to 2003-12-31 |

| 14 | Cycle 15 | 2003-12-31 | 2004-05-31 | 6 | -0.00 | -0.09 | 0.00 | 0.01 | -0.00 | -0.18 | 0.08 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 15, 2003-12-31 to 2004-05-31 |

| 15 | Cycle 16 | 2004-05-31 | 2006-12-31 | 32 | 0.10 | 10.27 | 0.00 | 0.31 | 0.04 | 3.73 | 0.04 | 0.04 | 425.00 | 0.02 | 159.38 | Cycle 16, 2004-05-31 to 2006-12-31 |

| 16 | Cycle 17 | 2006-12-31 | 2007-08-31 | 9 | 0.03 | 3.30 | 0.00 | 0.37 | 0.04 | 4.42 | 0.05 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 17, 2006-12-31 to 2007-08-31 |

| 17 | Cycle 18 | 2007-08-31 | 2009-07-31 | 24 | 0.20 | 19.84 | 0.01 | 0.79 | 0.09 | 9.47 | 0.09 | -0.05 | -500.00 | -0.03 | -250.00 | Cycle 18, 2007-08-31 to 2009-07-31 |

| 18 | Cycle 19 | 2009-07-31 | 2015-11-30 | 77 | 0.39 | 38.99 | 0.00 | 0.44 | 0.05 | 5.27 | 0.06 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 19, 2009-07-31 to 2015-11-30 |

| 19 | Cycle 20 | 2015-11-30 | 2016-06-30 | 8 | 0.07 | 6.79 | 0.01 | 0.83 | 0.10 | 10.36 | 0.05 | 0.00 | 25.00 | 0.00 | 37.50 | Cycle 20, 2015-11-30 to 2016-06-30 |

| 20 | Cycle 21 | 2016-06-30 | 2016-11-30 | 6 | -0.03 | -3.17 | -0.01 | -0.51 | -0.06 | -6.25 | 0.08 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 21, 2016-06-30 to 2016-11-30 |

| 21 | Cycle 22 | 2016-11-30 | 2019-06-30 | 32 | 0.06 | 5.92 | 0.00 | 0.19 | 0.02 | 2.18 | 0.05 | 0.02 | 200.00 | 0.01 | 75.00 | Cycle 22, 2016-11-30 to 2019-06-30 |

| 22 | Cycle 23 | 2019-06-30 | 2019-07-31 | 2 | 0.01 | 1.31 | 0.01 | 0.65 | 0.08 | 8.09 | 0.03 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 23, 2019-06-30 to 2019-07-31 |

| 23 | Cycle 24 | 2019-07-31 | 2020-09-30 | 15 | 0.13 | 13.08 | 0.01 | 0.84 | 0.10 | 10.34 | 0.06 | -0.02 | -225.00 | -0.02 | -180.00 | Cycle 24, 2019-07-31 to 2020-09-30 |

| 24 | Cycle 25 | 2020-09-30 | 2022-02-28 | 18 | -0.07 | -6.52 | -0.00 | -0.37 | -0.04 | -4.40 | 0.04 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 25, 2020-09-30 to 2022-02-28 |

| 25 | Cycle 26 | 2022-02-28 | 2024-01-31 | 24 | -0.10 | -9.88 | -0.00 | -0.39 | -0.05 | -5.07 | 0.10 | 0.05 | 525.00 | 0.03 | 262.50 | Cycle 26, 2022-02-28 to 2024-01-31 |

| 26 | Cycle 27 | 2024-01-31 | 2024-08-31 | 8 | 0.03 | 2.75 | 0.00 | 0.36 | 0.04 | 4.15 | 0.07 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 27, 2024-01-31 to 2024-08-31 |

| 27 | Cycle 28 | 2024-08-31 | 2025-06-30 | 11 | 0.03 | 3.29 | 0.00 | 0.31 | 0.04 | 3.60 | 0.06 | -0.01 | -100.00 | -0.01 | -109.09 | Cycle 28, 2024-08-31 to 2025-06-30 |

| 28 | Cycle 29 | 2025-06-30 | 2025-08-31 | 3 | 0.03 | 2.67 | 0.01 | 0.89 | 0.11 | 11.11 | 0.04 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 29, 2025-06-30 to 2025-08-31 |

| 29 | Cycle 30 | 2025-08-31 | 2026-01-31 | 6 | 0.03 | 3.08 | 0.01 | 0.51 | 0.06 | 6.26 | 0.03 | -0.01 | -75.00 | -0.01 | -150.00 | Cycle 30, 2025-08-31 to 2026-01-31 |

This gives us the following data points:

- Cycle start date

- Cycle end date

- Number of months in the cycle

- Cumulative return during the cycle (decimal and percent)

- Average monthly return during the cycle (decimal and percent)

- Annualized return during the cycle (decimal and percent)

- Return volatility during the cycle

- Cumulative change in FFR during the cycle (decimal and basis points)

- Annualized change in FFR during the cycle (decimal and basis points)

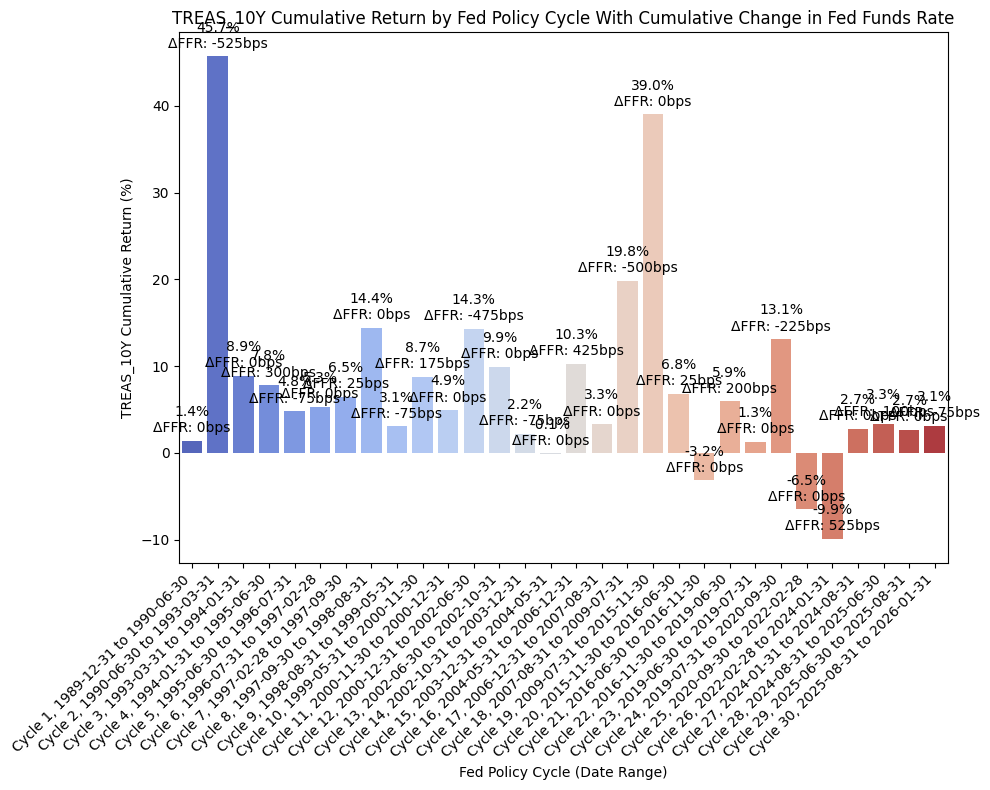

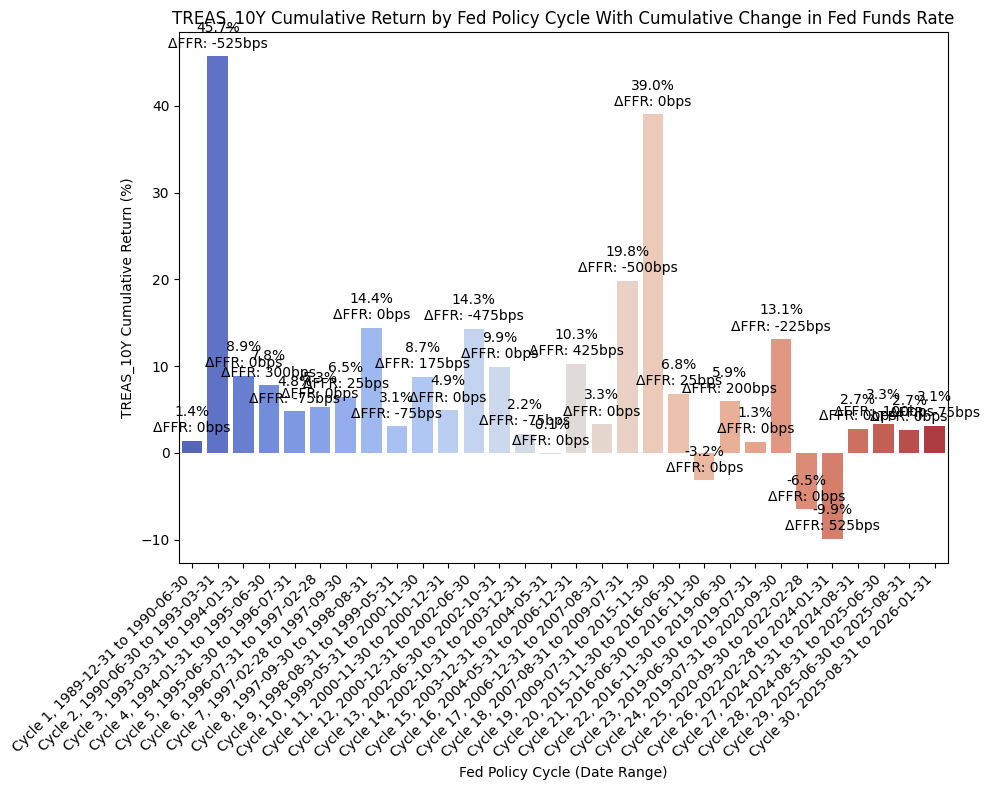

From the above DataFrame, we can then plot the cumulative and annualized returns for each cycle in a bar chart. First, the cumulative returns along with the cumulative change in FFR:

plot_bar_returns_ffr_change(

cycle_df=treas_10y_cycles,

asset_label="TREAS_10Y",

annualized_or_cumulative="Cumulative",

)

And then the annualized returns along with the annualized change in FFR:

plot_bar_returns_ffr_change(

cycle_df=treas_10y_cycles,

asset_label="TREAS_10Y",

annualized_or_cumulative="Annualized",

)

For this dataset, we have cycles 11/12/13/14 exhibiting strong returns, which is consistent with the economic intuition that bonds should perform well during periods of economic weakness and rate cuts. We also see this outcome with cycle 18. It becomes a little more interesting during cycles 25 and 26, where the correlations of stocks and bond returns seemed to align, so we see negative bond returns there. Finally, cycles 28/29/30 also exhibit positive bond returns, which is consistent with our thesis that bonds should perform well during periods of economic weakness and rate cuts.

Finally, we can run an OLS regression to check fit:

df = treas_10y_cycles

#=== Don't modify below this line ===

# Run OLS regression with statsmodels

X = df["FFR_AnnualizedChange_bps"]

y = df["AnnualizedReturnPct"]

X = sm.add_constant(X)

model = sm.OLS(y, X).fit()

print(model.summary())

print(f"Intercept: {model.params[0]}, Slope: {model.params[1]}") # Intercept and slope

# Calc X and Y values for regression line

X_vals = np.linspace(X.min(), X.max(), 100)

Y_vals = model.params[0] + model.params[1] * X_vals

OLS Regression Results

===============================================================================

Dep. Variable: AnnualizedReturnPct R-squared: 0.050

Model: OLS Adj. R-squared: 0.016

Method: Least Squares F-statistic: 1.462

Date: Mon, 23 Mar 2026 Prob (F-statistic): 0.237

Time: 22:08:23 Log-Likelihood: -103.64

No. Observations: 30 AIC: 211.3

Df Residuals: 28 BIC: 214.1

Df Model: 1

Covariance Type: nonrobust

============================================================================================

coef std err t P>|t| [0.025 0.975]

--------------------------------------------------------------------------------------------

const 6.7457 1.462 4.613 0.000 3.751 9.741

FFR_AnnualizedChange_bps -0.0149 0.012 -1.209 0.237 -0.040 0.010

==============================================================================

Omnibus: 19.978 Durbin-Watson: 2.116

Prob(Omnibus): 0.000 Jarque-Bera (JB): 29.185

Skew: 1.582 Prob(JB): 4.60e-07

Kurtosis: 6.651 Cond. No. 120.

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Intercept: 6.745718627069434, Slope: -0.01486255000436152

And then plot the regression line along with the values:

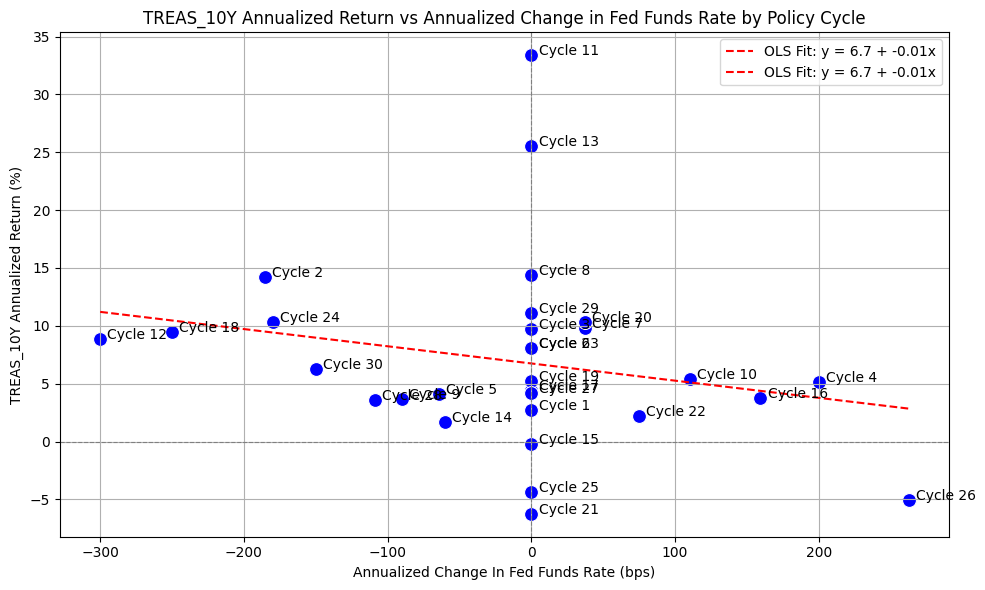

plot_scatter_regression_ffr_vs_returns(

cycle_df=treas_10y_cycles,

asset_label="TREAS_10Y",

x_vals=X_vals,

y_vals=Y_vals,

intercept=model.params[0],

slope=model.params[1],

)

The above plot is intriguing because of how well the OLS regression appears to fit the data. It certainly appears that during rate-cutting cycles, bonds are an asset that performs well.

High Yield Bonds #

Next, we’ll run a similar process for high yield bonds using LF98TRUU_Bloomberg US Corporate High Yield Total Return Index Value Unhedged USD.

First, we pull data with the following:

bb_clean_data(

base_directory=DATA_DIR,

fund_ticker_name="LF98TRUU_Bloomberg US Corporate High Yield Total Return Index Value Unhedged USD",

source="Bloomberg",

asset_class="Indices",

excel_export=True,

pickle_export=True,

output_confirmation=False,

)

hy_bonds = load_data(

base_directory=DATA_DIR,

ticker="LF98TRUU_Bloomberg US Corporate High Yield Total Return Index Value Unhedged USD_Clean",

source="Bloomberg",

asset_class="Indices",

timeframe="Daily",

file_format="pickle",

)

# Filter HY_BONDS to date range

hy_bonds = hy_bonds[(hy_bonds.index >= pd.to_datetime(start_date)) & (hy_bonds.index <= pd.to_datetime(end_date))]

# Drop everything except the "close" column

hy_bonds = hy_bonds[["Close"]]

# Resample to monthly frequency

hy_bonds_monthly = hy_bonds.resample("M").last()

hy_bonds_monthly["Monthly_Return"] = hy_bonds_monthly["Close"].pct_change()

hy_bonds_monthly = hy_bonds_monthly.dropna()

display(hy_bonds_monthly)

| Close | Monthly_Return | |

|---|---|---|

| Date | ||

| 1990-01-31 | 194.21 | -0.02 |

| 1990-02-28 | 190.20 | -0.02 |

| 1990-03-31 | 195.19 | 0.03 |

| 1990-04-30 | 194.86 | -0.00 |

| 1990-05-31 | 198.62 | 0.02 |

| ... | ... | ... |

| 2025-09-30 | 2876.85 | 0.01 |

| 2025-10-31 | 2881.38 | 0.00 |

| 2025-11-30 | 2898.07 | 0.01 |

| 2025-12-31 | 2914.49 | 0.01 |

| 2026-01-31 | 2929.32 | 0.01 |

433 rows × 2 columns

Next, we can plot the price history before calculating the cycle performance:

plot_time_series(

df=hy_bonds,

plot_start_date=None,

plot_end_date=None,

plot_columns=["Close"],

title="Bloomberg US Corporate High Yield Total Return Index Value Unhedged USD Daily Close Price",

x_label="Date",

x_format="Year",

x_tick_spacing=2,

x_tick_rotation=30,

y_label="Price ($)",

y_format="Decimal",

y_format_decimal_places=0,

y_tick_spacing=200,

y_tick_rotation=0,

grid=True,

legend=False,

export_plot=False,

plot_file_name=None,

)

Next, we will calculate the performance of high yield bonds based on the pre-defined Fed cycles:

hy_bonds_cycles = calc_fed_cycle_asset_performance(

start_date=cycle_ranges["start_date"],

end_date=cycle_ranges["end_date"],

label=cycle_ranges["cycle_label"],

fed_funds_change=cycle_ranges["fed_funds_change"],

monthly_returns=hy_bonds_monthly,

)

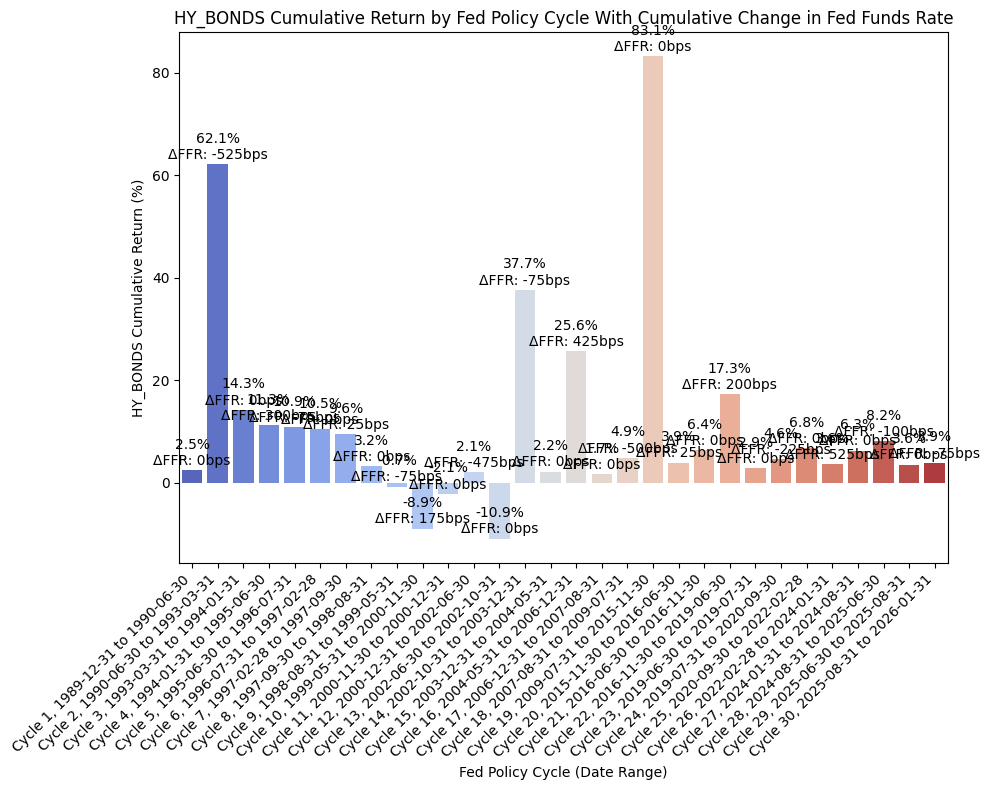

display(hy_bonds_cycles)

| Cycle | Start | End | Months | CumulativeReturn | CumulativeReturnPct | AverageMonthlyReturn | AverageMonthlyReturnPct | AnnualizedReturn | AnnualizedReturnPct | Volatility | FedFundsChange | FedFundsChange_bps | FFR_AnnualizedChange | FFR_AnnualizedChange_bps | Label | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | Cycle 1 | 1989-12-31 | 1990-06-30 | 6 | 0.02 | 2.49 | 0.00 | 0.43 | 0.05 | 5.05 | 0.08 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 1, 1989-12-31 to 1990-06-30 |

| 1 | Cycle 2 | 1990-06-30 | 1993-03-31 | 34 | 0.62 | 62.15 | 0.01 | 1.48 | 0.19 | 18.60 | 0.11 | -0.05 | -525.00 | -0.02 | -185.29 | Cycle 2, 1990-06-30 to 1993-03-31 |

| 2 | Cycle 3 | 1993-03-31 | 1994-01-31 | 11 | 0.14 | 14.26 | 0.01 | 1.22 | 0.16 | 15.66 | 0.02 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 3, 1993-03-31 to 1994-01-31 |

| 3 | Cycle 4 | 1994-01-31 | 1995-06-30 | 18 | 0.11 | 11.25 | 0.01 | 0.61 | 0.07 | 7.37 | 0.06 | 0.03 | 300.00 | 0.02 | 200.00 | Cycle 4, 1994-01-31 to 1995-06-30 |

| 4 | Cycle 5 | 1995-06-30 | 1996-07-31 | 14 | 0.11 | 10.89 | 0.01 | 0.74 | 0.09 | 9.27 | 0.02 | -0.01 | -75.00 | -0.01 | -64.29 | Cycle 5, 1995-06-30 to 1996-07-31 |

| 5 | Cycle 6 | 1996-07-31 | 1997-02-28 | 8 | 0.10 | 10.48 | 0.01 | 1.26 | 0.16 | 16.12 | 0.02 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 6, 1996-07-31 to 1997-02-28 |

| 6 | Cycle 7 | 1997-02-28 | 1997-09-30 | 8 | 0.10 | 9.56 | 0.01 | 1.16 | 0.15 | 14.67 | 0.05 | 0.00 | 25.00 | 0.00 | 37.50 | Cycle 7, 1997-02-28 to 1997-09-30 |

| 7 | Cycle 8 | 1997-09-30 | 1998-08-31 | 12 | 0.03 | 3.22 | 0.00 | 0.28 | 0.03 | 3.22 | 0.07 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 8, 1997-09-30 to 1998-08-31 |

| 8 | Cycle 9 | 1998-08-31 | 1999-05-31 | 10 | -0.01 | -0.73 | -0.00 | -0.04 | -0.01 | -0.87 | 0.09 | -0.01 | -75.00 | -0.01 | -90.00 | Cycle 9, 1998-08-31 to 1999-05-31 |

| 9 | Cycle 10 | 1999-05-31 | 2000-11-30 | 19 | -0.09 | -8.92 | -0.00 | -0.48 | -0.06 | -5.73 | 0.05 | 0.02 | 175.00 | 0.01 | 110.53 | Cycle 10, 1999-05-31 to 2000-11-30 |

| 10 | Cycle 11 | 2000-11-30 | 2000-12-31 | 2 | -0.02 | -2.11 | -0.01 | -1.01 | -0.12 | -11.98 | 0.14 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 11, 2000-11-30 to 2000-12-31 |

| 11 | Cycle 12 | 2000-12-31 | 2002-06-30 | 19 | 0.02 | 2.12 | 0.00 | 0.17 | 0.01 | 1.33 | 0.12 | -0.05 | -475.00 | -0.03 | -300.00 | Cycle 12, 2000-12-31 to 2002-06-30 |

| 12 | Cycle 13 | 2002-06-30 | 2002-10-31 | 5 | -0.11 | -10.87 | -0.02 | -2.22 | -0.24 | -24.14 | 0.13 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 13, 2002-06-30 to 2002-10-31 |

| 13 | Cycle 14 | 2002-10-31 | 2003-12-31 | 15 | 0.38 | 37.66 | 0.02 | 2.17 | 0.29 | 29.14 | 0.07 | -0.01 | -75.00 | -0.01 | -60.00 | Cycle 14, 2002-10-31 to 2003-12-31 |

| 14 | Cycle 15 | 2003-12-31 | 2004-05-31 | 6 | 0.02 | 2.19 | 0.00 | 0.37 | 0.04 | 4.42 | 0.05 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 15, 2003-12-31 to 2004-05-31 |

| 15 | Cycle 16 | 2004-05-31 | 2006-12-31 | 32 | 0.26 | 25.62 | 0.01 | 0.72 | 0.09 | 8.93 | 0.04 | 0.04 | 425.00 | 0.02 | 159.38 | Cycle 16, 2004-05-31 to 2006-12-31 |

| 16 | Cycle 17 | 2006-12-31 | 2007-08-31 | 9 | 0.02 | 1.68 | 0.00 | 0.20 | 0.02 | 2.25 | 0.06 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 17, 2006-12-31 to 2007-08-31 |

| 17 | Cycle 18 | 2007-08-31 | 2009-07-31 | 24 | 0.05 | 4.91 | 0.00 | 0.37 | 0.02 | 2.42 | 0.20 | -0.05 | -500.00 | -0.03 | -250.00 | Cycle 18, 2007-08-31 to 2009-07-31 |

| 18 | Cycle 19 | 2009-07-31 | 2015-11-30 | 77 | 0.83 | 83.15 | 0.01 | 0.81 | 0.10 | 9.89 | 0.07 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 19, 2009-07-31 to 2015-11-30 |

| 19 | Cycle 20 | 2015-11-30 | 2016-06-30 | 8 | 0.04 | 3.95 | 0.01 | 0.52 | 0.06 | 5.98 | 0.09 | 0.00 | 25.00 | 0.00 | 37.50 | Cycle 20, 2015-11-30 to 2016-06-30 |

| 20 | Cycle 21 | 2016-06-30 | 2016-11-30 | 6 | 0.06 | 6.43 | 0.01 | 1.05 | 0.13 | 13.27 | 0.04 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 21, 2016-06-30 to 2016-11-30 |

| 21 | Cycle 22 | 2016-11-30 | 2019-06-30 | 32 | 0.17 | 17.31 | 0.01 | 0.51 | 0.06 | 6.17 | 0.04 | 0.02 | 200.00 | 0.01 | 75.00 | Cycle 22, 2016-11-30 to 2019-06-30 |

| 22 | Cycle 23 | 2019-06-30 | 2019-07-31 | 2 | 0.03 | 2.86 | 0.01 | 1.42 | 0.18 | 18.41 | 0.04 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 23, 2019-06-30 to 2019-07-31 |

| 23 | Cycle 24 | 2019-07-31 | 2020-09-30 | 15 | 0.05 | 4.63 | 0.00 | 0.37 | 0.04 | 3.69 | 0.13 | -0.02 | -225.00 | -0.02 | -180.00 | Cycle 24, 2019-07-31 to 2020-09-30 |

| 24 | Cycle 25 | 2020-09-30 | 2022-02-28 | 18 | 0.07 | 6.77 | 0.00 | 0.37 | 0.04 | 4.47 | 0.05 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 25, 2020-09-30 to 2022-02-28 |

| 25 | Cycle 26 | 2022-02-28 | 2024-01-31 | 24 | 0.04 | 3.58 | 0.00 | 0.19 | 0.02 | 1.77 | 0.10 | 0.05 | 525.00 | 0.03 | 262.50 | Cycle 26, 2022-02-28 to 2024-01-31 |

| 26 | Cycle 27 | 2024-01-31 | 2024-08-31 | 8 | 0.06 | 6.28 | 0.01 | 0.77 | 0.10 | 9.57 | 0.03 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 27, 2024-01-31 to 2024-08-31 |

| 27 | Cycle 28 | 2024-08-31 | 2025-06-30 | 11 | 0.08 | 8.18 | 0.01 | 0.72 | 0.09 | 8.96 | 0.04 | -0.01 | -100.00 | -0.01 | -109.09 | Cycle 28, 2024-08-31 to 2025-06-30 |

| 28 | Cycle 29 | 2025-06-30 | 2025-08-31 | 3 | 0.04 | 3.58 | 0.01 | 1.18 | 0.15 | 15.09 | 0.02 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 29, 2025-06-30 to 2025-08-31 |

| 29 | Cycle 30 | 2025-08-31 | 2026-01-31 | 6 | 0.04 | 3.94 | 0.01 | 0.65 | 0.08 | 8.03 | 0.01 | -0.01 | -75.00 | -0.01 | -150.00 | Cycle 30, 2025-08-31 to 2026-01-31 |

This gives us the following data points:

- Cycle start date

- Cycle end date

- Number of months in the cycle

- Cumulative return during the cycle (decimal and percent)

- Average monthly return during the cycle (decimal and percent)

- Annualized return during the cycle (decimal and percent)

- Return volatility during the cycle

- Cumulative change in FFR during the cycle (decimal and basis points)

- Annualized change in FFR during the cycle (decimal and basis points)

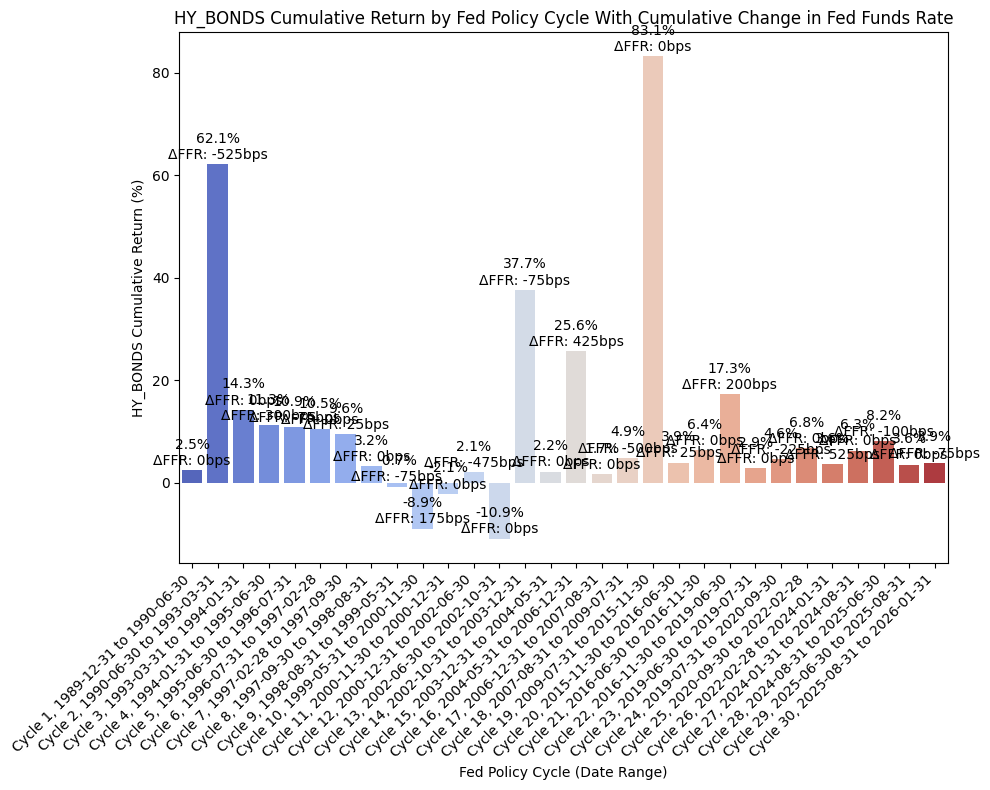

From the above DataFrame, we can then plot the cumulative and annualized returns for each cycle in a bar chart. First, the cumulative returns along with the cumulative change in FFR:

plot_bar_returns_ffr_change(

cycle_df=hy_bonds_cycles,

asset_label="HY_BONDS",

annualized_or_cumulative="Cumulative",

)

And then the annualized returns along with the annualized change in FFR:

plot_bar_returns_ffr_change(

cycle_df=hy_bonds_cycles,

asset_label="HY_BONDS",

annualized_or_cumulative="Annualized",

)

Finally, we can run an OLS regression to check fit:

df = hy_bonds_cycles

#=== Don't modify below this line ===

# Run OLS regression with statsmodels

X = df["FFR_AnnualizedChange_bps"]

y = df["AnnualizedReturnPct"]

X = sm.add_constant(X)

model = sm.OLS(y, X).fit()

print(model.summary())

print(f"Intercept: {model.params[0]}, Slope: {model.params[1]}") # Intercept and slope

# Calc X and Y values for regression line

X_vals = np.linspace(X.min(), X.max(), 100)

Y_vals = model.params[0] + model.params[1] * X_vals

OLS Regression Results

===============================================================================

Dep. Variable: AnnualizedReturnPct R-squared: 0.004

Model: OLS Adj. R-squared: -0.031

Method: Least Squares F-statistic: 0.1171

Date: Mon, 23 Mar 2026 Prob (F-statistic): 0.735

Time: 22:08:25 Log-Likelihood: -110.57

No. Observations: 30 AIC: 225.1

Df Residuals: 28 BIC: 227.9

Df Model: 1

Covariance Type: nonrobust

============================================================================================

coef std err t P>|t| [0.025 0.975]

--------------------------------------------------------------------------------------------

const 6.6113 1.842 3.590 0.001 2.839 10.384

FFR_AnnualizedChange_bps -0.0053 0.015 -0.342 0.735 -0.037 0.026

==============================================================================

Omnibus: 9.087 Durbin-Watson: 1.936

Prob(Omnibus): 0.011 Jarque-Bera (JB): 9.047

Skew: -0.790 Prob(JB): 0.0109

Kurtosis: 5.178 Cond. No. 120.

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Intercept: 6.611340605920211, Slope: -0.005299161729553994

And then plot the regression line along with the values:

plot_scatter_regression_ffr_vs_returns(

cycle_df=treas_10y_cycles,

asset_label="TREAS_10Y",

x_vals=X_vals,

y_vals=Y_vals,

intercept=model.params[0],

slope=model.params[1],

)

Gold #

Finally, we’ll run a similar process for gold using XAU_Gold USD Spot.

First, we pull data with the following:

bb_clean_data(

base_directory=DATA_DIR,

fund_ticker_name="XAU_Gold USD Spot",

source="Bloomberg",

asset_class="Commodities",

excel_export=True,

pickle_export=True,

output_confirmation=False,

)

gold = load_data(

base_directory=DATA_DIR,

ticker="XAU_Gold USD Spot_Clean",

source="Bloomberg",

asset_class="Commodities",

timeframe="Daily",

file_format="pickle",

)

# Filter GOLD to date range

gold = gold[(gold.index >= pd.to_datetime(start_date)) & (gold.index <= pd.to_datetime(end_date))]

# Drop everything except the "close" column

gold = gold[["Close"]]

# Resample to monthly frequency

gold_monthly = gold.resample("M").last()

gold_monthly["Monthly_Return"] = gold_monthly["Close"].pct_change()

gold_monthly = gold_monthly.dropna()

display(gold_monthly)

| Close | Monthly_Return | |

|---|---|---|

| Date | ||

| 1990-01-31 | 415.05 | 0.03 |

| 1990-02-28 | 407.70 | -0.02 |

| 1990-03-31 | 368.50 | -0.10 |

| 1990-04-30 | 367.75 | -0.00 |

| 1990-05-31 | 363.05 | -0.01 |

| ... | ... | ... |

| 2025-09-30 | 3858.96 | 0.12 |

| 2025-10-31 | 4002.92 | 0.04 |

| 2025-11-30 | 4239.43 | 0.06 |

| 2025-12-31 | 4319.37 | 0.02 |

| 2026-01-31 | 4894.23 | 0.13 |

433 rows × 2 columns

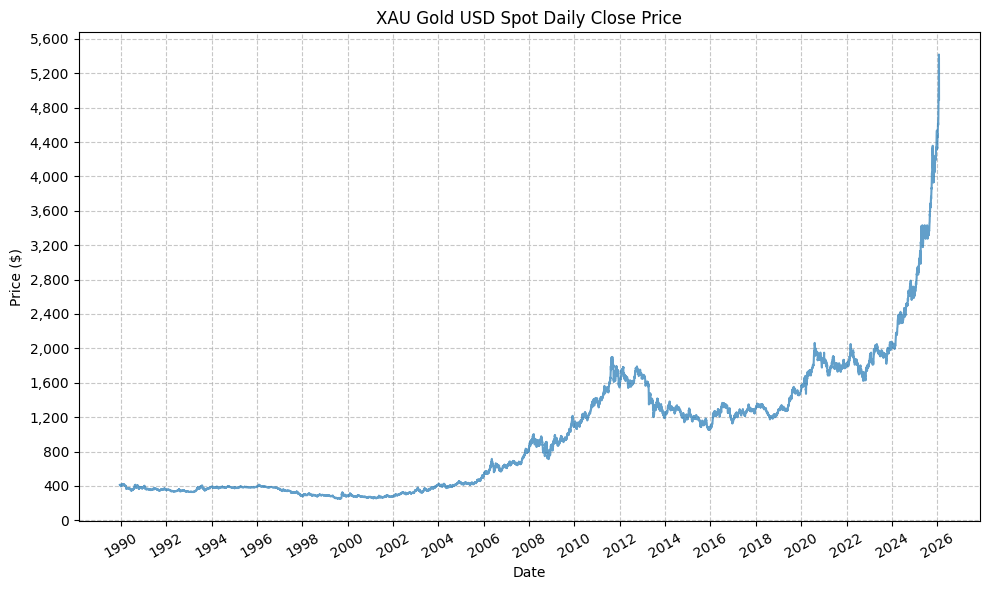

Next, we can plot the price history before calculating the cycle performance:

plot_time_series(

df=gold,

plot_start_date=None,

plot_end_date=None,

plot_columns=["Close"],

title="XAU Gold USD Spot Daily Close Price",

x_label="Date",

x_format="Year",

x_tick_spacing=2,

x_tick_rotation=30,

y_label="Price ($)",

y_format="Decimal",

y_format_decimal_places=0,

y_tick_spacing=400,

y_tick_rotation=0,

grid=True,

legend=False,

export_plot=False,

plot_file_name=None,

)

Next, we will calculate the performance of gold based on the pre-defined Fed cycles:

gold_cycles = calc_fed_cycle_asset_performance(

start_date=cycle_ranges["start_date"],

end_date=cycle_ranges["end_date"],

label=cycle_ranges["cycle_label"],

fed_funds_change=cycle_ranges["fed_funds_change"],

monthly_returns=gold_monthly,

)

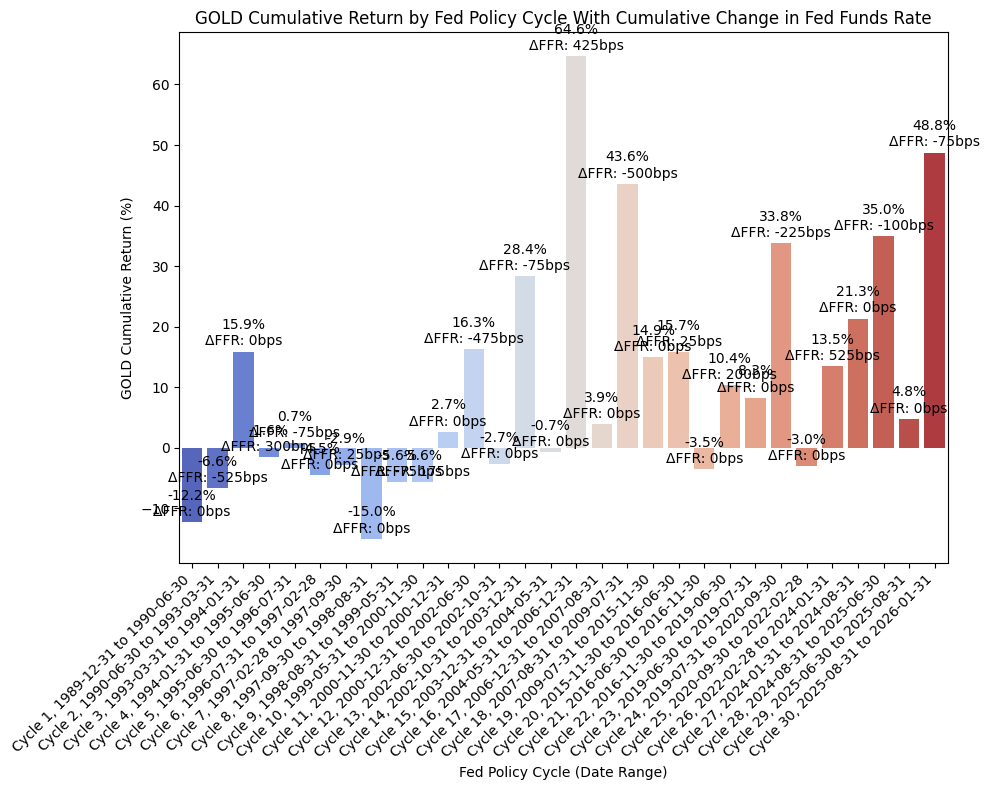

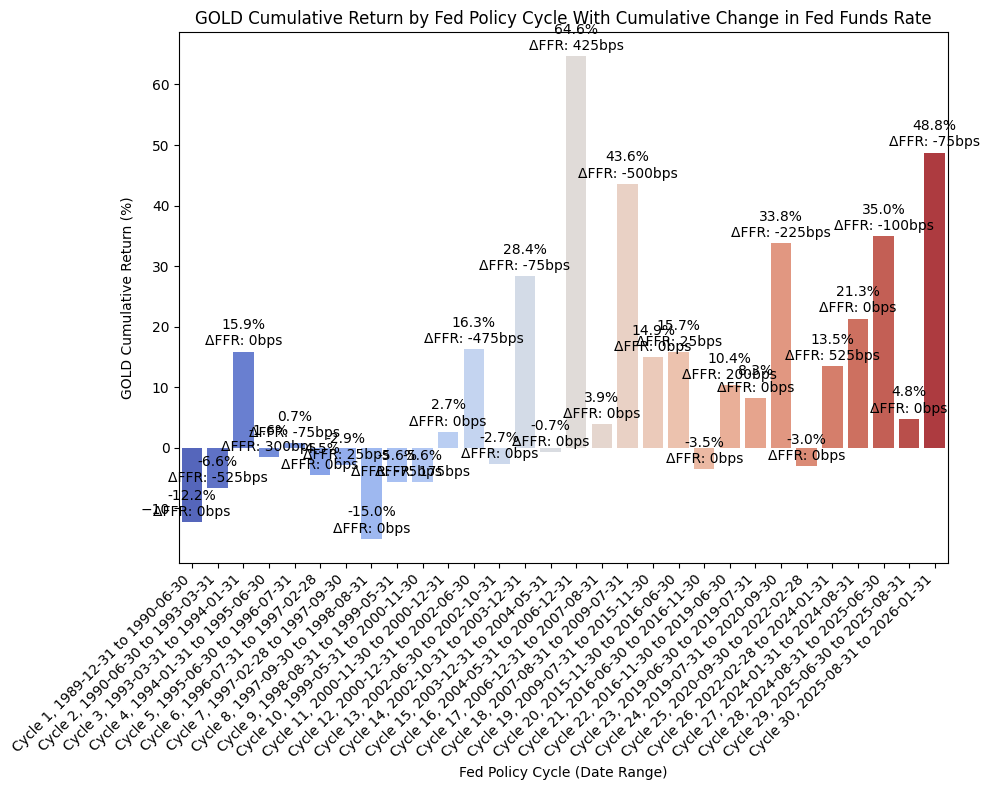

display(gold_cycles)

| Cycle | Start | End | Months | CumulativeReturn | CumulativeReturnPct | AverageMonthlyReturn | AverageMonthlyReturnPct | AnnualizedReturn | AnnualizedReturnPct | Volatility | FedFundsChange | FedFundsChange_bps | FFR_AnnualizedChange | FFR_AnnualizedChange_bps | Label | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | Cycle 1 | 1989-12-31 | 1990-06-30 | 6 | -0.12 | -12.22 | -0.02 | -2.07 | -0.23 | -22.95 | 0.15 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 1, 1989-12-31 to 1990-06-30 |

| 1 | Cycle 2 | 1990-06-30 | 1993-03-31 | 34 | -0.07 | -6.62 | -0.00 | -0.16 | -0.02 | -2.39 | 0.10 | -0.05 | -525.00 | -0.02 | -185.29 | Cycle 2, 1990-06-30 to 1993-03-31 |

| 2 | Cycle 3 | 1993-03-31 | 1994-01-31 | 11 | 0.16 | 15.90 | 0.01 | 1.46 | 0.17 | 17.47 | 0.17 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 3, 1993-03-31 to 1994-01-31 |

| 3 | Cycle 4 | 1994-01-31 | 1995-06-30 | 18 | -0.02 | -1.56 | -0.00 | -0.07 | -0.01 | -1.04 | 0.07 | 0.03 | 300.00 | 0.02 | 200.00 | Cycle 4, 1994-01-31 to 1995-06-30 |

| 4 | Cycle 5 | 1995-06-30 | 1996-07-31 | 14 | 0.01 | 0.72 | 0.00 | 0.07 | 0.01 | 0.61 | 0.06 | -0.01 | -75.00 | -0.01 | -64.29 | Cycle 5, 1995-06-30 to 1996-07-31 |

| 5 | Cycle 6 | 1996-07-31 | 1997-02-28 | 8 | -0.04 | -4.47 | -0.01 | -0.52 | -0.07 | -6.63 | 0.12 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 6, 1996-07-31 to 1997-02-28 |

| 6 | Cycle 7 | 1997-02-28 | 1997-09-30 | 8 | -0.03 | -2.87 | -0.00 | -0.31 | -0.04 | -4.28 | 0.12 | 0.00 | 25.00 | 0.00 | 37.50 | Cycle 7, 1997-02-28 to 1997-09-30 |

| 7 | Cycle 8 | 1997-09-30 | 1998-08-31 | 12 | -0.15 | -14.99 | -0.01 | -1.28 | -0.15 | -14.99 | 0.12 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 8, 1997-09-30 to 1998-08-31 |

| 8 | Cycle 9 | 1998-08-31 | 1999-05-31 | 10 | -0.06 | -5.62 | -0.01 | -0.52 | -0.07 | -6.71 | 0.13 | -0.01 | -75.00 | -0.01 | -90.00 | Cycle 9, 1998-08-31 to 1999-05-31 |

| 9 | Cycle 10 | 1999-05-31 | 2000-11-30 | 19 | -0.06 | -5.62 | -0.00 | -0.19 | -0.04 | -3.59 | 0.17 | 0.02 | 175.00 | 0.01 | 110.53 | Cycle 10, 1999-05-31 to 2000-11-30 |

| 10 | Cycle 11 | 2000-11-30 | 2000-12-31 | 2 | 0.03 | 2.68 | 0.01 | 1.33 | 0.17 | 17.18 | 0.03 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 11, 2000-11-30 to 2000-12-31 |

| 11 | Cycle 12 | 2000-12-31 | 2002-06-30 | 19 | 0.16 | 16.27 | 0.01 | 0.84 | 0.10 | 9.99 | 0.11 | -0.05 | -475.00 | -0.03 | -300.00 | Cycle 12, 2000-12-31 to 2002-06-30 |

| 12 | Cycle 13 | 2002-06-30 | 2002-10-31 | 5 | -0.03 | -2.69 | -0.00 | -0.50 | -0.06 | -6.35 | 0.12 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 13, 2002-06-30 to 2002-10-31 |

| 13 | Cycle 14 | 2002-10-31 | 2003-12-31 | 15 | 0.28 | 28.40 | 0.02 | 1.77 | 0.22 | 22.14 | 0.15 | -0.01 | -75.00 | -0.01 | -60.00 | Cycle 14, 2002-10-31 to 2003-12-31 |

| 14 | Cycle 15 | 2003-12-31 | 2004-05-31 | 6 | -0.01 | -0.65 | 0.00 | 0.04 | -0.01 | -1.30 | 0.21 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 15, 2003-12-31 to 2004-05-31 |

| 15 | Cycle 16 | 2004-05-31 | 2006-12-31 | 32 | 0.65 | 64.63 | 0.02 | 1.65 | 0.21 | 20.56 | 0.15 | 0.04 | 425.00 | 0.02 | 159.38 | Cycle 16, 2004-05-31 to 2006-12-31 |

| 16 | Cycle 17 | 2006-12-31 | 2007-08-31 | 9 | 0.04 | 3.90 | 0.00 | 0.45 | 0.05 | 5.24 | 0.07 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 17, 2006-12-31 to 2007-08-31 |

| 17 | Cycle 18 | 2007-08-31 | 2009-07-31 | 24 | 0.44 | 43.61 | 0.02 | 1.77 | 0.20 | 19.84 | 0.25 | -0.05 | -500.00 | -0.03 | -250.00 | Cycle 18, 2007-08-31 to 2009-07-31 |

| 18 | Cycle 19 | 2009-07-31 | 2015-11-30 | 77 | 0.15 | 14.92 | 0.00 | 0.32 | 0.02 | 2.19 | 0.18 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 19, 2009-07-31 to 2015-11-30 |

| 19 | Cycle 20 | 2015-11-30 | 2016-06-30 | 8 | 0.16 | 15.74 | 0.02 | 2.03 | 0.25 | 24.52 | 0.23 | 0.00 | 25.00 | 0.00 | 37.50 | Cycle 20, 2015-11-30 to 2016-06-30 |

| 20 | Cycle 21 | 2016-06-30 | 2016-11-30 | 6 | -0.03 | -3.47 | -0.00 | -0.45 | -0.07 | -6.81 | 0.20 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 21, 2016-06-30 to 2016-11-30 |

| 21 | Cycle 22 | 2016-11-30 | 2019-06-30 | 32 | 0.10 | 10.36 | 0.00 | 0.36 | 0.04 | 3.77 | 0.11 | 0.02 | 200.00 | 0.01 | 75.00 | Cycle 22, 2016-11-30 to 2019-06-30 |

| 22 | Cycle 23 | 2019-06-30 | 2019-07-31 | 2 | 0.08 | 8.29 | 0.04 | 4.13 | 0.61 | 61.24 | 0.19 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 23, 2019-06-30 to 2019-07-31 |

| 23 | Cycle 24 | 2019-07-31 | 2020-09-30 | 15 | 0.34 | 33.79 | 0.02 | 2.04 | 0.26 | 26.22 | 0.15 | -0.02 | -225.00 | -0.02 | -180.00 | Cycle 24, 2019-07-31 to 2020-09-30 |

| 24 | Cycle 25 | 2020-09-30 | 2022-02-28 | 18 | -0.03 | -2.99 | -0.00 | -0.08 | -0.02 | -2.00 | 0.15 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 25, 2020-09-30 to 2022-02-28 |

| 25 | Cycle 26 | 2022-02-28 | 2024-01-31 | 24 | 0.13 | 13.49 | 0.01 | 0.61 | 0.07 | 6.53 | 0.14 | 0.05 | 525.00 | 0.03 | 262.50 | Cycle 26, 2022-02-28 to 2024-01-31 |

| 26 | Cycle 27 | 2024-01-31 | 2024-08-31 | 8 | 0.21 | 21.35 | 0.02 | 2.49 | 0.34 | 33.68 | 0.11 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 27, 2024-01-31 to 2024-08-31 |

| 27 | Cycle 28 | 2024-08-31 | 2025-06-30 | 11 | 0.35 | 34.95 | 0.03 | 2.82 | 0.39 | 38.68 | 0.13 | -0.01 | -100.00 | -0.01 | -109.09 | Cycle 28, 2024-08-31 to 2025-06-30 |

| 28 | Cycle 29 | 2025-06-30 | 2025-08-31 | 3 | 0.05 | 4.82 | 0.02 | 1.61 | 0.21 | 20.74 | 0.10 | 0.00 | 0.00 | 0.00 | 0.00 | Cycle 29, 2025-06-30 to 2025-08-31 |

| 29 | Cycle 30 | 2025-08-31 | 2026-01-31 | 6 | 0.49 | 48.76 | 0.07 | 6.93 | 1.21 | 121.31 | 0.16 | -0.01 | -75.00 | -0.01 | -150.00 | Cycle 30, 2025-08-31 to 2026-01-31 |

This gives us the following data points:

- Cycle start date

- Cycle end date

- Number of months in the cycle

- Cumulative return during the cycle (decimal and percent)

- Average monthly return during the cycle (decimal and percent)

- Annualized return during the cycle (decimal and percent)

- Return volatility during the cycle

- Cumulative change in FFR during the cycle (decimal and basis points)

- Annualized change in FFR during the cycle (decimal and basis points)

From the above DataFrame, we can then plot the cumulative and annualized returns for each cycle in a bar chart. First, the cumulative returns along with the cumulative change in FFR:

plot_bar_returns_ffr_change(

cycle_df=gold_cycles,

asset_label="GOLD",

annualized_or_cumulative="Cumulative",

)

And then the annualized returns along with the annualized change in FFR:

plot_bar_returns_ffr_change(

cycle_df=gold_cycles,

asset_label="GOLD",

annualized_or_cumulative="Annualized",

)

We see strong returns for gold across several different Fed cycles, so it is difficult to draw any kind of initial conclusion based on the bar charts.

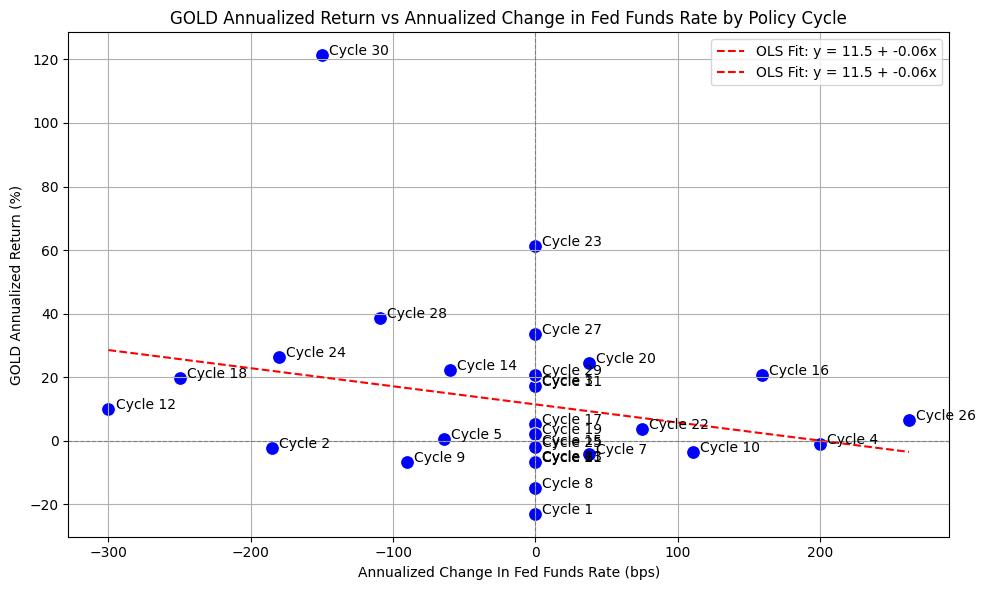

Finally, we can run an OLS regression to check fit:

df = gold_cycles

#=== Don't modify below this line ===

# Run OLS regression with statsmodels

X = df["FFR_AnnualizedChange_bps"]

y = df["AnnualizedReturnPct"]

X = sm.add_constant(X)

model = sm.OLS(y, X).fit()

print(model.summary())

print(f"Intercept: {model.params[0]}, Slope: {model.params[1]}") # Intercept and slope

# Calc X and Y values for regression line

X_vals = np.linspace(X.min(), X.max(), 100)

Y_vals = model.params[0] + model.params[1] * X_vals

OLS Regression Results

===============================================================================

Dep. Variable: AnnualizedReturnPct R-squared: 0.064

Model: OLS Adj. R-squared: 0.030

Method: Least Squares F-statistic: 1.900

Date: Mon, 23 Mar 2026 Prob (F-statistic): 0.179

Time: 22:08:28 Log-Likelihood: -140.03

No. Observations: 30 AIC: 284.1

Df Residuals: 28 BIC: 286.9

Df Model: 1

Covariance Type: nonrobust

============================================================================================

coef std err t P>|t| [0.025 0.975]

--------------------------------------------------------------------------------------------

const 11.4670 4.917 2.332 0.027 1.396 21.539

FFR_AnnualizedChange_bps -0.0570 0.041 -1.378 0.179 -0.142 0.028

==============================================================================

Omnibus: 28.991 Durbin-Watson: 1.081

Prob(Omnibus): 0.000 Jarque-Bera (JB): 62.894

Skew: 2.093 Prob(JB): 2.20e-14

Kurtosis: 8.727 Cond. No. 120.

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Intercept: 11.467013480569243, Slope: -0.056974234027166226

And then plot the regression line along with the values:

plot_scatter_regression_ffr_vs_returns(

cycle_df=gold_cycles,

asset_label="GOLD",

x_vals=X_vals,

y_vals=Y_vals,

intercept=model.params[0],

slope=model.params[1],

)

It’s difficult to draw any strong conclusions with the above plot. Gold has traditionally been considered a hedge for inflation, and while one of the Fed’s mandates is to manage inflation, there may not be a conclusion to draw in relationship to the historical returns that gold has exhibited.

Asset Allocation #

With the above analysis (somewhat) complete, let’s look at the optimal allocation for a portfolio based on the data and the hypythetical historical results.

We have to be careful with our criteria for when to hold stocks, bonds, or gold, as hindsight bias is certainly possible. So, without overanalyzing the results, let’s assume that we hold stocks as the default position during tightening cycles, and then hold bonds during easing cycles when the Fed starts cutting rates, and then resume holding stocks when the Fed stops cutting rates. If there is not any change in FFR, then we still hold stocks.

We can then combine the return series based on the above with the following:

# Shift the "cycle_filled" column down by one row to create a new column called "cycle_invested" that represents the cycle label that an investor would be invested in for each month (i.e. the cycle label from the previous month)

fedfunds_grouped_cycles['cycle_invested'] = fedfunds_grouped_cycles['cycle_filled'].shift(1)

display(fedfunds_grouped_cycles)

| start_date | fed_funds_start | end_date | fed_funds_end | fed_funds_change | cycle | cycle_filled | group | cycle_invested | |

|---|---|---|---|---|---|---|---|---|---|

| 0 | 1989-12-31 | 0.08 | 1990-01-31 | 0.08 | 0.00 | Neutral | Modified Tightening | 1 | None |

| 1 | 1990-01-31 | 0.08 | 1990-02-28 | 0.08 | 0.00 | Neutral | Modified Tightening | 1 | Modified Tightening |

| 2 | 1990-02-28 | 0.08 | 1990-03-31 | 0.08 | 0.00 | Neutral | Modified Tightening | 1 | Modified Tightening |

| 3 | 1990-03-31 | 0.08 | 1990-04-30 | 0.08 | 0.00 | Neutral | Modified Tightening | 1 | Modified Tightening |

| 4 | 1990-04-30 | 0.08 | 1990-05-31 | 0.08 | 0.00 | Neutral | Modified Tightening | 1 | Modified Tightening |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 429 | 2025-09-30 | 0.04 | 2025-10-31 | 0.04 | -0.00 | Easing | Easing | 30 | Easing |

| 430 | 2025-10-31 | 0.04 | 2025-11-30 | 0.04 | 0.00 | Neutral | Easing | 30 | Easing |

| 431 | 2025-11-30 | 0.04 | 2025-12-31 | 0.04 | -0.00 | Easing | Easing | 30 | Easing |

| 432 | 2025-12-31 | 0.04 | 2026-01-31 | 0.04 | 0.00 | Neutral | Easing | 30 | Easing |

| 433 | 2026-01-31 | 0.04 | NaT | NaN | NaN | Neutral | Easing | 30 | Easing |

434 rows × 9 columns

# Reset index to merge on date

stocks_merged = pd.merge_asof(

spxt_monthly.reset_index(),

fedfunds_grouped_cycles[['start_date', 'end_date', 'cycle_invested', 'group']],

left_on='Date',

right_on='start_date',

direction='backward'

)

# Drop rows where the date falls outside the cycle's end_date

stocks_merged = stocks_merged[stocks_merged['Date'] <= stocks_merged['end_date']]

display(stocks_merged)

| Date | Close | Monthly_Return | start_date | end_date | cycle_invested | group | |

|---|---|---|---|---|---|---|---|

| 0 | 1990-01-31 | 353.94 | -0.07 | 1990-01-31 | 1990-02-28 | Modified Tightening | 1 |

| 1 | 1990-02-28 | 358.50 | 0.01 | 1990-02-28 | 1990-03-31 | Modified Tightening | 1 |

| 2 | 1990-03-31 | 368 | 0.03 | 1990-03-31 | 1990-04-30 | Modified Tightening | 1 |

| 3 | 1990-04-30 | 358.81 | -0.02 | 1990-04-30 | 1990-05-31 | Modified Tightening | 1 |

| 4 | 1990-05-31 | 393.80 | 0.10 | 1990-05-31 | 1990-06-30 | Modified Tightening | 1 |

| ... | ... | ... | ... | ... | ... | ... | ... |

| 427 | 2025-08-31 | 14304.68 | 0.02 | 2025-08-31 | 2025-09-30 | Modified Tightening | 30 |

| 428 | 2025-09-30 | 14826.80 | 0.04 | 2025-09-30 | 2025-10-31 | Easing | 30 |

| 429 | 2025-10-31 | 15173.95 | 0.02 | 2025-10-31 | 2025-11-30 | Easing | 30 |

| 430 | 2025-11-30 | 15211.14 | 0.00 | 2025-11-30 | 2025-12-31 | Easing | 30 |

| 431 | 2025-12-31 | 15220.45 | 0.00 | 2025-12-31 | 2026-01-31 | Easing | 30 |

432 rows × 7 columns

# Reset index to merge on date

bonds_merged = pd.merge_asof(

treas_10y_monthly.reset_index(),

fedfunds_grouped_cycles[['start_date', 'end_date', 'cycle_invested', 'group']],

left_on='Date',

right_on='start_date',

direction='backward'

)

# Drop rows where the date falls outside the cycle's end_date

bonds_merged = bonds_merged[bonds_merged['Date'] <= bonds_merged['end_date']]

display(bonds_merged)

| Date | Close | Monthly_Return | start_date | end_date | cycle_invested | group | |

|---|---|---|---|---|---|---|---|

| 0 | 1990-01-31 | 98.01 | -0.02 | 1990-01-31 | 1990-02-28 | Modified Tightening | 1 |

| 1 | 1990-02-28 | 97.99 | -0.00 | 1990-02-28 | 1990-03-31 | Modified Tightening | 1 |

| 2 | 1990-03-31 | 97.99 | -0.00 | 1990-03-31 | 1990-04-30 | Modified Tightening | 1 |

| 3 | 1990-04-30 | 96.61 | -0.01 | 1990-04-30 | 1990-05-31 | Modified Tightening | 1 |

| 4 | 1990-05-31 | 99.65 | 0.03 | 1990-05-31 | 1990-06-30 | Modified Tightening | 1 |

| ... | ... | ... | ... | ... | ... | ... | ... |

| 427 | 2025-08-31 | 641.26 | 0.02 | 2025-08-31 | 2025-09-30 | Modified Tightening | 30 |

| 428 | 2025-09-30 | 645.58 | 0.01 | 2025-09-30 | 2025-10-31 | Easing | 30 |

| 429 | 2025-10-31 | 650.00 | 0.01 | 2025-10-31 | 2025-11-30 | Easing | 30 |

| 430 | 2025-11-30 | 656.64 | 0.01 | 2025-11-30 | 2025-12-31 | Easing | 30 |

| 431 | 2025-12-31 | 652.29 | -0.01 | 2025-12-31 | 2026-01-31 | Easing | 30 |

432 rows × 7 columns

# Select the appropriate return based on cycle

stocks_merged['strategy_return'] = stocks_merged.apply(

lambda row: row['Monthly_Return'] if row['cycle_invested'] in ['Tightening', 'Modified Tightening'] else None,

axis=1

)

bonds_merged['strategy_return'] = bonds_merged.apply(

lambda row: row['Monthly_Return'] if row['cycle_invested'] == 'Easing' else None,

axis=1

)

# Combine

strategy = pd.concat([stocks_merged, bonds_merged]).dropna(subset=['strategy_return'])

strategy = strategy.sort_values('Date')

display(strategy.head(20))

| Date | Close | Monthly_Return | start_date | end_date | cycle_invested | group | strategy_return | |

|---|---|---|---|---|---|---|---|---|

| 0 | 1990-01-31 | 353.94 | -0.07 | 1990-01-31 | 1990-02-28 | Modified Tightening | 1 | -0.07 |

| 1 | 1990-02-28 | 358.50 | 0.01 | 1990-02-28 | 1990-03-31 | Modified Tightening | 1 | 0.01 |

| 2 | 1990-03-31 | 368 | 0.03 | 1990-03-31 | 1990-04-30 | Modified Tightening | 1 | 0.03 |

| 3 | 1990-04-30 | 358.81 | -0.02 | 1990-04-30 | 1990-05-31 | Modified Tightening | 1 | -0.02 |

| 4 | 1990-05-31 | 393.80 | 0.10 | 1990-05-31 | 1990-06-30 | Modified Tightening | 1 | 0.10 |

| 5 | 1990-06-30 | 391.14 | -0.01 | 1990-06-30 | 1990-07-31 | Modified Tightening | 2 | -0.01 |

| 6 | 1990-07-31 | 102.84 | 0.01 | 1990-07-31 | 1990-08-31 | Easing | 2 | 0.01 |

| 7 | 1990-08-31 | 100.78 | -0.02 | 1990-08-31 | 1990-09-30 | Easing | 2 | -0.02 |

| 8 | 1990-09-30 | 101.74 | 0.01 | 1990-09-30 | 1990-10-31 | Easing | 2 | 0.01 |

| 9 | 1990-10-31 | 103.65 | 0.02 | 1990-10-31 | 1990-11-30 | Easing | 2 | 0.02 |

| 10 | 1990-11-30 | 106.43 | 0.03 | 1990-11-30 | 1990-12-31 | Easing | 2 | 0.03 |

| 11 | 1990-12-31 | 108.25 | 0.02 | 1990-12-31 | 1991-01-31 | Easing | 2 | 0.02 |

| 12 | 1991-01-31 | 109.53 | 0.01 | 1991-01-31 | 1991-02-28 | Easing | 2 | 0.01 |

| 13 | 1991-02-28 | 110.10 | 0.01 | 1991-02-28 | 1991-03-31 | Easing | 2 | 0.01 |

| 14 | 1991-03-31 | 110.43 | 0.00 | 1991-03-31 | 1991-04-30 | Easing | 2 | 0.00 |

| 15 | 1991-04-30 | 111.60 | 0.01 | 1991-04-30 | 1991-05-31 | Easing | 2 | 0.01 |

| 16 | 1991-05-31 | 112.08 | 0.00 | 1991-05-31 | 1991-06-30 | Easing | 2 | 0.00 |

| 17 | 1991-06-30 | 111.50 | -0.01 | 1991-06-30 | 1991-07-31 | Easing | 2 | -0.01 |

| 18 | 1991-07-31 | 113.05 | 0.01 | 1991-07-31 | 1991-08-31 | Easing | 2 | 0.01 |

| 19 | 1991-08-31 | 116.06 | 0.03 | 1991-08-31 | 1991-09-30 | Easing | 2 | 0.03 |

# Calculate cumulative returns and drawdown for spxt

spxt_monthly['Cumulative_Return'] = (1 + spxt_monthly['Monthly_Return']).cumprod() - 1

spxt_monthly['Cumulative_Return_Plus_One'] = 1 + spxt_monthly['Cumulative_Return']

spxt_monthly['Rolling_Max'] = spxt_monthly['Cumulative_Return_Plus_One'].cummax()

spxt_monthly['Drawdown'] = spxt_monthly['Cumulative_Return_Plus_One'] / spxt_monthly['Rolling_Max'] - 1

spxt_monthly.drop(columns=['Cumulative_Return_Plus_One', 'Rolling_Max'], inplace=True)

# Calculate cumulative returns and drawdown for treas_10y

treas_10y_monthly['Cumulative_Return'] = (1 + treas_10y_monthly['Monthly_Return']).cumprod() - 1

treas_10y_monthly['Cumulative_Return_Plus_One'] = 1 + treas_10y_monthly['Cumulative_Return']

treas_10y_monthly['Rolling_Max'] = treas_10y_monthly['Cumulative_Return_Plus_One'].cummax()

treas_10y_monthly['Drawdown'] = treas_10y_monthly['Cumulative_Return_Plus_One'] / treas_10y_monthly['Rolling_Max'] - 1

treas_10y_monthly.drop(columns=['Cumulative_Return_Plus_One', 'Rolling_Max'], inplace=True)

# Convert to DataFrame

portfolio_monthly = strategy[['Date', 'strategy_return']].copy().set_index('Date')

portfolio_monthly = portfolio_monthly.rename(columns={'strategy_return': 'Portfolio_Monthly_Return'})

# Calculate cumulative returns and drawdown for the portfolio

portfolio_monthly['Portfolio_Cumulative_Return'] = (1 + portfolio_monthly['Portfolio_Monthly_Return']).cumprod() - 1

portfolio_monthly['Portfolio_Cumulative_Return_Plus_One'] = 1 + portfolio_monthly['Portfolio_Cumulative_Return']

portfolio_monthly['Portfolio_Rolling_Max'] = portfolio_monthly['Portfolio_Cumulative_Return_Plus_One'].cummax()

portfolio_monthly['Portfolio_Drawdown'] = portfolio_monthly['Portfolio_Cumulative_Return_Plus_One'] / portfolio_monthly['Portfolio_Rolling_Max'] - 1

portfolio_monthly.drop(columns=['Portfolio_Cumulative_Return_Plus_One', 'Portfolio_Rolling_Max'], inplace=True)

# Merge "spxt_monthly" and "treas_10y_monthly" into "portfolio_monthly" to compare cumulative returns

portfolio_monthly = portfolio_monthly.join(

spxt_monthly['Monthly_Return'].rename('SPXT_Monthly_Return'),

how='left'

).join(

spxt_monthly['Cumulative_Return'].rename('SPXT_Cumulative_Return'),

how='left'

).join(

spxt_monthly['Drawdown'].rename('SPXT_Drawdown'),

how='left'

).join(

treas_10y_monthly['Monthly_Return'].rename('10Y_Monthly_Return'),

how='left'

).join(

treas_10y_monthly['Cumulative_Return'].rename('10Y_Cumulative_Return'),

how='left'

).join(

treas_10y_monthly['Drawdown'].rename('10Y_Drawdown'),

how='left'

)

display(portfolio_monthly)

| Portfolio_Monthly_Return | Portfolio_Cumulative_Return | Portfolio_Drawdown | SPXT_Monthly_Return | SPXT_Cumulative_Return | SPXT_Drawdown | 10Y_Monthly_Return | 10Y_Cumulative_Return | 10Y_Drawdown | |

|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||

| 1990-01-31 | -0.07 | -0.07 | 0.00 | -0.07 | -0.07 | 0.00 | -0.02 | -0.02 | 0.00 |

| 1990-02-28 | 0.01 | -0.06 | 0.00 | 0.01 | -0.06 | 0.00 | -0.00 | -0.02 | -0.00 |

| 1990-03-31 | 0.03 | -0.03 | 0.00 | 0.03 | -0.03 | 0.00 | -0.00 | -0.02 | -0.00 |

| 1990-04-30 | -0.02 | -0.05 | -0.02 | -0.02 | -0.05 | -0.02 | -0.01 | -0.03 | -0.01 |

| 1990-05-31 | 0.10 | 0.04 | 0.00 | 0.10 | 0.04 | 0.00 | 0.03 | -0.00 | 0.00 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 2025-08-31 | 0.02 | 42.29 | 0.00 | 0.02 | 36.70 | 0.00 | 0.02 | 5.41 | -0.11 |

| 2025-09-30 | 0.01 | 42.58 | 0.00 | 0.04 | 38.08 | 0.00 | 0.01 | 5.46 | -0.11 |

| 2025-10-31 | 0.01 | 42.88 | 0.00 | 0.02 | 38.99 | 0.00 | 0.01 | 5.50 | -0.10 |

| 2025-11-30 | 0.01 | 43.32 | 0.00 | 0.00 | 39.09 | 0.00 | 0.01 | 5.57 | -0.09 |

| 2025-12-31 | -0.01 | 43.03 | -0.01 | 0.00 | 39.12 | 0.00 | -0.01 | 5.52 | -0.10 |

432 rows × 9 columns

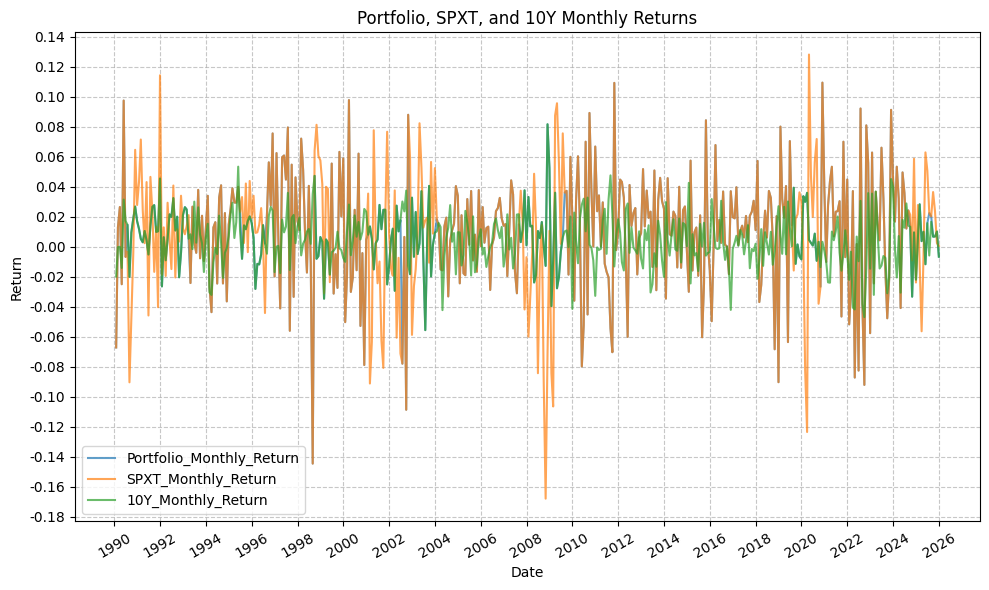

Next, we’ll look at performance for the assets and portfolio.

Performance Statistics #

We can then plot the monthly returns:

plot_time_series(

df=portfolio_monthly,

plot_start_date=start_date,

plot_end_date=end_date,

plot_columns=["Portfolio_Monthly_Return", "SPXT_Monthly_Return", "10Y_Monthly_Return"],

title="Portfolio, SPXT, and 10Y Monthly Returns",

x_label="Date",

x_format="Year",

x_tick_spacing=2,

x_tick_rotation=30,

y_label="Return",

y_format="Decimal",

y_format_decimal_places=2,

y_tick_spacing=0.02,

y_tick_rotation=0,

grid=True,

legend=True,

export_plot=False,

plot_file_name=None,

)

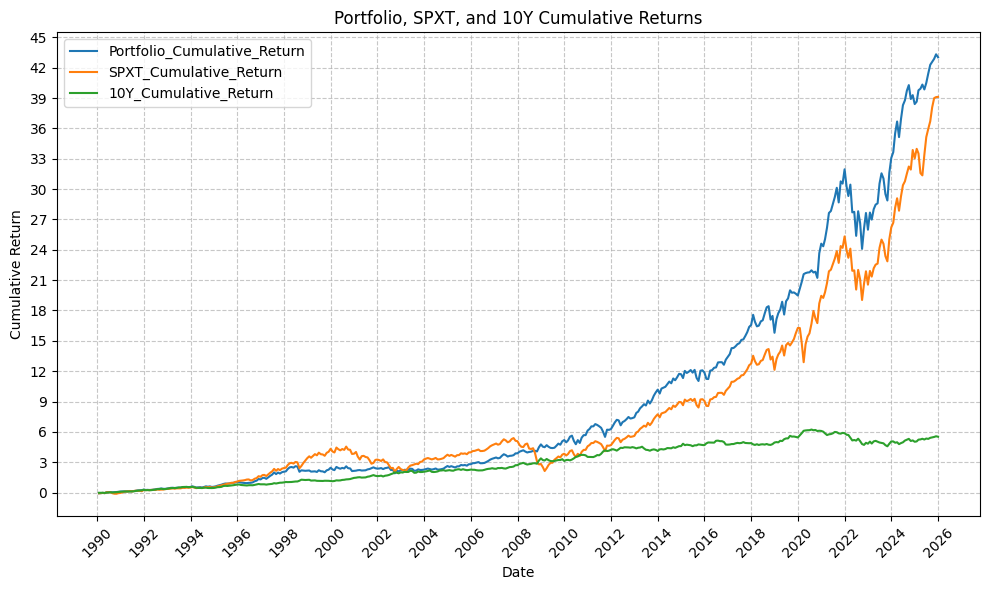

And cumulative returns:

plot_time_series(

df=portfolio_monthly,

plot_start_date=start_date,

plot_end_date=end_date,