Post Updates

Update 4/8/2025: Added plot for signals for each year. VIX data through 4/7/25.Update 4/9/2025: VIX data through 4/8/25.Update 4/12/2025: VIX data through 4/10/25.Update 4/22/2025: VIX data through 4/18/25.Update 4/23/2025: VIX data through 4/22/25.Update 4/25/2025: VIX data through 4/23/25. Added section for trade history, including open and closed positions.Update 4/28/2025: VIX data through 4/25/25.

Introduction

From the CBOE VIX website:

“Cboe Global Markets revolutionized investing with the creation of the Cboe Volatility Index® (VIX® Index), the first benchmark index to measure the market’s expectation of future volatility. The VIX Index is based on options of the S&P 500® Index, considered the leading indicator of the broad U.S. stock market. The VIX Index is recognized as the world’s premier gauge of U.S. equity market volatility.”

In this tutorial, we will investigate finding a signal to use as a basis to trade the VIX.

VIX Data

I don’t have access to data for the VIX through Nasdaq Data Link, but for our purposes Yahoo Finance is sufficient.

Using the yfinance python module, we can pull what we need and quicky dump it to excel to retain it for future use.

Python Functions

Typical Functions

First, the typical set of functions I use:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

| from pathlib import Path

def export_track_md_deps(

dep_file: Path,

md_filename: str,

content: str,

) -> None:

"""

Export Markdown content to a file and track it as a dependency.

This function writes the provided content to the specified Markdown file and

appends the filename to the given dependency file (typically `index_dep.txt`).

This is useful in workflows where Markdown fragments are later assembled

into a larger document (e.g., a Hugo `index.md`).

Parameters:

-----------

dep_file : Path

Path to the dependency file that tracks Markdown fragment filenames.

md_filename : str

The name of the Markdown file to export.

content : str

The Markdown-formatted content to write to the file.

Returns:

--------

None

Example:

--------

>>> export_track_md_deps(Path("index_dep.txt"), "01_intro.md", "# Introduction\n...")

✅ Exported and tracked: 01_intro.md

"""

Path(md_filename).write_text(content)

with dep_file.open("a") as f:

f.write(md_filename + "\n")

print(f"✅ Exported and tracked: {md_filename}")

|

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

| from IPython.display import display

def df_info(df) -> None:

"""

Display summary information about a pandas DataFrame.

This function prints:

- The DataFrame's column names, shape, and data types via `df.info()`

- The first 5 rows using `df.head()`

- The last 5 rows using `df.tail()`

It uses `display()` for better output formatting in environments like Jupyter notebooks.

Parameters:

-----------

df : pd.DataFrame

The DataFrame to inspect.

Returns:

--------

None

Example:

--------

>>> df_info(my_dataframe)

"""

print("The columns, shape, and data types are:")

print(df.info())

print("The first 5 rows are:")

display(df.head())

print("The last 5 rows are:")

display(df.tail())

|

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

| import io

import pandas as pd

def df_info_markdown(df: pd.DataFrame) -> str:

"""

Generate a Markdown-formatted summary of a pandas DataFrame.

This function captures and formats the output of `df.info()`, `df.head()`,

and `df.tail()` in Markdown for easy inclusion in reports, documentation,

or web-based rendering (e.g., Hugo or Jupyter export workflows).

Parameters:

-----------

df : pd.DataFrame

The DataFrame to summarize.

Returns:

--------

str

A string containing the DataFrame's info, head, and tail

formatted in Markdown.

Example:

--------

>>> print(df_info_markdown(df))

```text

The columns, shape, and data types are:

<output from df.info()>

```

The first 5 rows are:

| | col1 | col2 |

|---|------|------|

| 0 | ... | ... |

The last 5 rows are:

...

"""

buffer = io.StringIO()

# Capture df.info() output

df.info(buf=buffer)

info_str = buffer.getvalue()

# Convert head and tail to Markdown

head_str = df.head().to_markdown()

tail_str = df.tail().to_markdown()

markdown = [

"```text",

"The columns, shape, and data types are:\n",

info_str,

"```",

"\nThe first 5 rows are:\n",

head_str,

"\nThe last 5 rows are:\n",

tail_str

]

return "\n".join(markdown)

|

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

| import pandas as pd

def pandas_set_decimal_places(decimal_places: int) -> None:

"""

Set the number of decimal places displayed for floating-point numbers in pandas.

Parameters:

----------

decimal_places : int

The number of decimal places to display for float values in pandas DataFrames and Series.

Example:

--------

>>> dp(3)

>>> pd.DataFrame([1.23456789])

0

0 1.235

"""

pd.set_option('display.float_format', lambda x: f'%.{decimal_places}f' % x)

|

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

| import pandas as pd

from pathlib import Path

def load_data(

base_directory: str,

ticker: str,

source: str,

asset_class: str,

timeframe: str,

) -> pd.DataFrame:

"""

Load data from a CSV or Excel file into a pandas DataFrame.

This function attempts to read a file first as a CSV, then as an Excel file

(specifically looking for a sheet named 'data' and using the 'calamine' engine).

If both attempts fail, a ValueError is raised.

Parameters:

-----------

base_directory : str

Root path to read data file.

ticker : str

Ticker symbol to read.

source : str

Name of the data source (e.g., 'Yahoo').

asset_class : str

Asset class name (e.g., 'Equities').

timeframe : str

Timeframe for the data (e.g., 'Daily', 'Month_End').

Returns:

--------

pd.DataFrame

The loaded data.

Raises:

-------

ValueError

If the file could not be loaded as either CSV or Excel.

Example:

--------

>>> df = load_data(DATA_DIR, "^VIX", "Yahoo_Finance", "Indices")

"""

# Build file paths using pathlib

csv_path = Path(base_directory) / source / asset_class / timeframe / f"{ticker}.csv"

xlsx_path = Path(base_directory) / source / asset_class / timeframe / f"{ticker}.xlsx"

# Try CSV

try:

df = pd.read_csv(csv_path)

return df

except Exception:

pass

# Try Excel

try:

df = pd.read_excel(xlsx_path)

return df

except Exception:

pass

raise ValueError(f"❌ Unable to load file: {ticker}. Ensure it's a valid CSV or Excel file with a 'data' sheet.")

|

Project Specific Functions

Here’s the code for the function to pull the VIX data and export to Excel:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

| import yfinance as yf

import os

from IPython.display import display

def yf_pull_data(

base_directory: str,

ticker: str,

source: str,

asset_class: str,

excel_export: bool,

pickle_export: bool,

) -> None:

"""

Download daily price data from Yahoo Finance and export it.

Parameters:

-----------

base_directory : str

Root path to store downloaded data.

ticker : str

Ticker symbol to download.

source : str

Name of the data source (e.g., 'Yahoo').

asset_class : str

Asset class name (e.g., 'Equities').

excel_export : bool

If True, export data to Excel format.

pickle_export : bool

If True, export data to Pickle format.

Returns:

--------

None

"""

# Download data from YF

df = yf.download(ticker)

# Drop the column level with the ticker symbol

df.columns = df.columns.droplevel(1)

# Reset index

df = df.reset_index()

# Remove the "Price" header from the index

df.columns.name = None

# Reset date column

df['Date'] = df['Date'].dt.tz_localize(None)

# Set 'Date' column as index

df = df.set_index('Date', drop=True)

# Drop data from last day because it's not accrate until end of day

df = df.drop(df.index[-1])

# Create directory

directory = f"{base_directory}/{source}/{asset_class}/Daily"

os.makedirs(directory, exist_ok=True)

# Export to excel

if excel_export == True:

df.to_excel(f"{directory}/{ticker}.xlsx", sheet_name="data")

else:

pass

# Export to pickle

if pickle_export == True:

df.to_pickle(f"{directory}/{ticker}.pkl")

else:

pass

# Print confirmation and display the first and last date

# of data

print(f"The first and last date of data for {ticker} is: ")

display(df[:1])

display(df[-1:])

print(f"Yahoo Finance data complete for {ticker}")

return print(f"--------------------")

|

Data Overview

Acquire CBOE Volatility Index (VIX) Data

First, let’s get the data:

1

| yf_data_updater('^VIX')

|

Set Decimal Places

Let’s set the number of decimal places to something sane (like 2):

1

| pandas_set_decimal_places(2)

|

Load Data

Now that we have the data, let’s load it up and take a look:

1

2

3

4

5

6

7

8

9

10

11

| # VIX

vix = load_data('^VIX.xlsx')

# Set 'Date' column as datetime

vix['Date'] = pd.to_datetime(vix['Date'])

# Drop 'Volume'

vix.drop(columns = {'Volume'}, inplace = True)

# Set Date as index

vix.set_index('Date', inplace = True)

|

Check For Missing Values & Forward Fill Any Missing Values

1

2

3

4

5

| # Check to see if there are any NaN values

vix[vix['High'].isna()]

# Forward fill to clean up missing data

vix['High'] = vix['High'].ffill()

|

VIX DataFrame Info

Now, running:

Gives us the following:

1

2

3

4

5

6

7

8

9

10

11

12

13

| The columns, shape, and data types are:

<class 'pandas.core.frame.DataFrame'>

DatetimeIndex: 8895 entries, 1990-01-02 to 2025-04-25

Data columns (total 4 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Close 8895 non-null float64

1 High 8895 non-null float64

2 Low 8895 non-null float64

3 Open 8895 non-null float64

dtypes: float64(4)

memory usage: 347.5 KB

|

The first 5 rows are:

| Date | Close | High | Low | Open |

|---|

| 1990-01-02 00:00:00 | 17.24 | 17.24 | 17.24 | 17.24 |

| 1990-01-03 00:00:00 | 18.19 | 18.19 | 18.19 | 18.19 |

| 1990-01-04 00:00:00 | 19.22 | 19.22 | 19.22 | 19.22 |

| 1990-01-05 00:00:00 | 20.11 | 20.11 | 20.11 | 20.11 |

| 1990-01-08 00:00:00 | 20.26 | 20.26 | 20.26 | 20.26 |

The last 5 rows are:

| Date | Close | High | Low | Open |

|---|

| 2025-04-21 00:00:00 | 33.82 | 35.75 | 31.79 | 32.75 |

| 2025-04-22 00:00:00 | 30.57 | 32.68 | 30.08 | 32.61 |

| 2025-04-23 00:00:00 | 28.45 | 30.29 | 27.11 | 28.75 |

| 2025-04-24 00:00:00 | 26.47 | 29.66 | 26.36 | 28.69 |

| 2025-04-25 00:00:00 | 24.84 | 27.20 | 24.84 | 26.22 |

Statistics

Some interesting statistics jump out at us when we look at the mean, standard deviation, minimum, and maximum values. The following code:

1

2

3

4

5

6

7

8

9

| vix_stats = vix.describe()

num_std = [-1, 0, 1, 2, 3, 4, 5]

for num in num_std:

vix_stats.loc[f"mean + {num} std"] = {

'Open': vix_stats.loc['mean']['Open'] + num * vix_stats.loc['std']['Open'],

'High': vix_stats.loc['mean']['High'] + num * vix_stats.loc['std']['High'],

'Low': vix_stats.loc['mean']['Low'] + num * vix_stats.loc['std']['Low'],

'Close': vix_stats.loc['mean']['Close'] + num * vix_stats.loc['std']['Close'],

}

|

Gives us:

| Close | High | Low | Open |

|---|

| count | 8895.00 | 8895.00 | 8895.00 | 8895.00 |

| mean | 19.49 | 20.40 | 18.82 | 19.58 |

| std | 7.85 | 8.41 | 7.40 | 7.92 |

| min | 9.14 | 9.31 | 8.56 | 9.01 |

| 25% | 13.86 | 14.53 | 13.40 | 13.93 |

| 50% | 17.64 | 18.35 | 17.06 | 17.68 |

| 75% | 22.84 | 23.83 | 22.14 | 22.97 |

| max | 82.69 | 89.53 | 72.76 | 82.69 |

| mean + -1 std | 11.65 | 11.99 | 11.42 | 11.66 |

| mean + 0 std | 19.49 | 20.40 | 18.82 | 19.58 |

| mean + 1 std | 27.34 | 28.81 | 26.22 | 27.51 |

| mean + 2 std | 35.19 | 37.21 | 33.62 | 35.43 |

| mean + 3 std | 43.03 | 45.62 | 41.02 | 43.35 |

| mean + 4 std | 50.88 | 54.03 | 48.42 | 51.27 |

| mean + 5 std | 58.73 | 62.43 | 55.82 | 59.20 |

Deciles

And the levels for each decile:

1

2

| vix_deciles = vix.quantile(np.arange(0, 1.1, 0.1))

display(vix_deciles)

|

Gives us:

| Close | High | Low | Open |

|---|

| 0.00 | 9.14 | 9.31 | 8.56 | 9.01 |

| 0.10 | 12.12 | 12.62 | 11.72 | 12.13 |

| 0.20 | 13.24 | 13.87 | 12.85 | 13.30 |

| 0.30 | 14.59 | 15.28 | 14.07 | 14.67 |

| 0.40 | 16.09 | 16.75 | 15.55 | 16.12 |

| 0.50 | 17.64 | 18.35 | 17.06 | 17.68 |

| 0.60 | 19.55 | 20.38 | 19.00 | 19.68 |

| 0.70 | 21.64 | 22.64 | 20.99 | 21.79 |

| 0.80 | 24.32 | 25.36 | 23.51 | 24.39 |

| 0.90 | 28.73 | 30.02 | 27.80 | 28.88 |

| 1.00 | 82.69 | 89.53 | 72.76 | 82.69 |

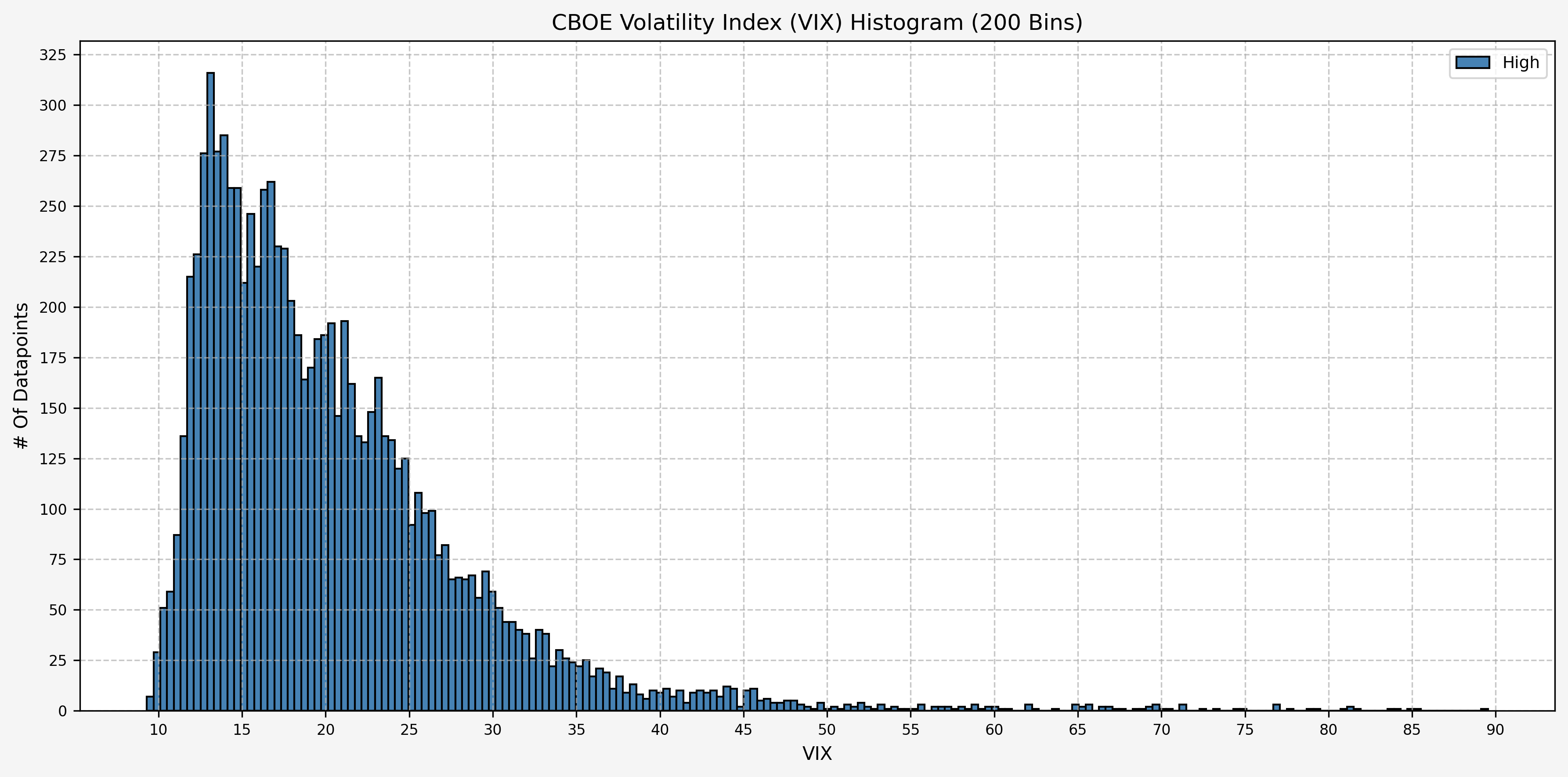

Histogram Distribution

A quick histogram gives us the distribution for the entire dataset:

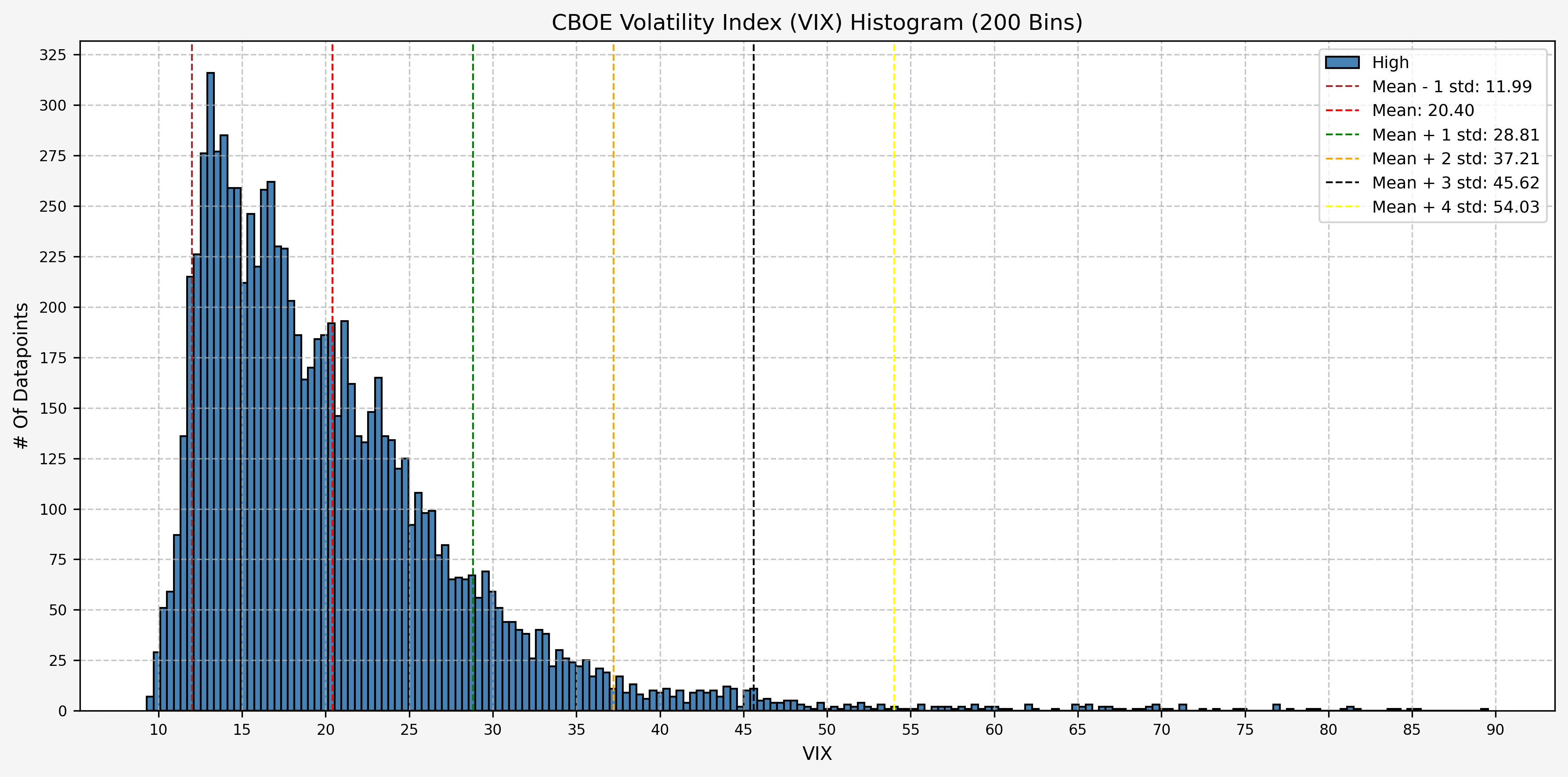

Now, let’s add the levels for the mean, mean plus 1 standard deviation, mean minus 1 standard deviation, and mean plus 2 standard deviations:

Plots

Historical VIX Data

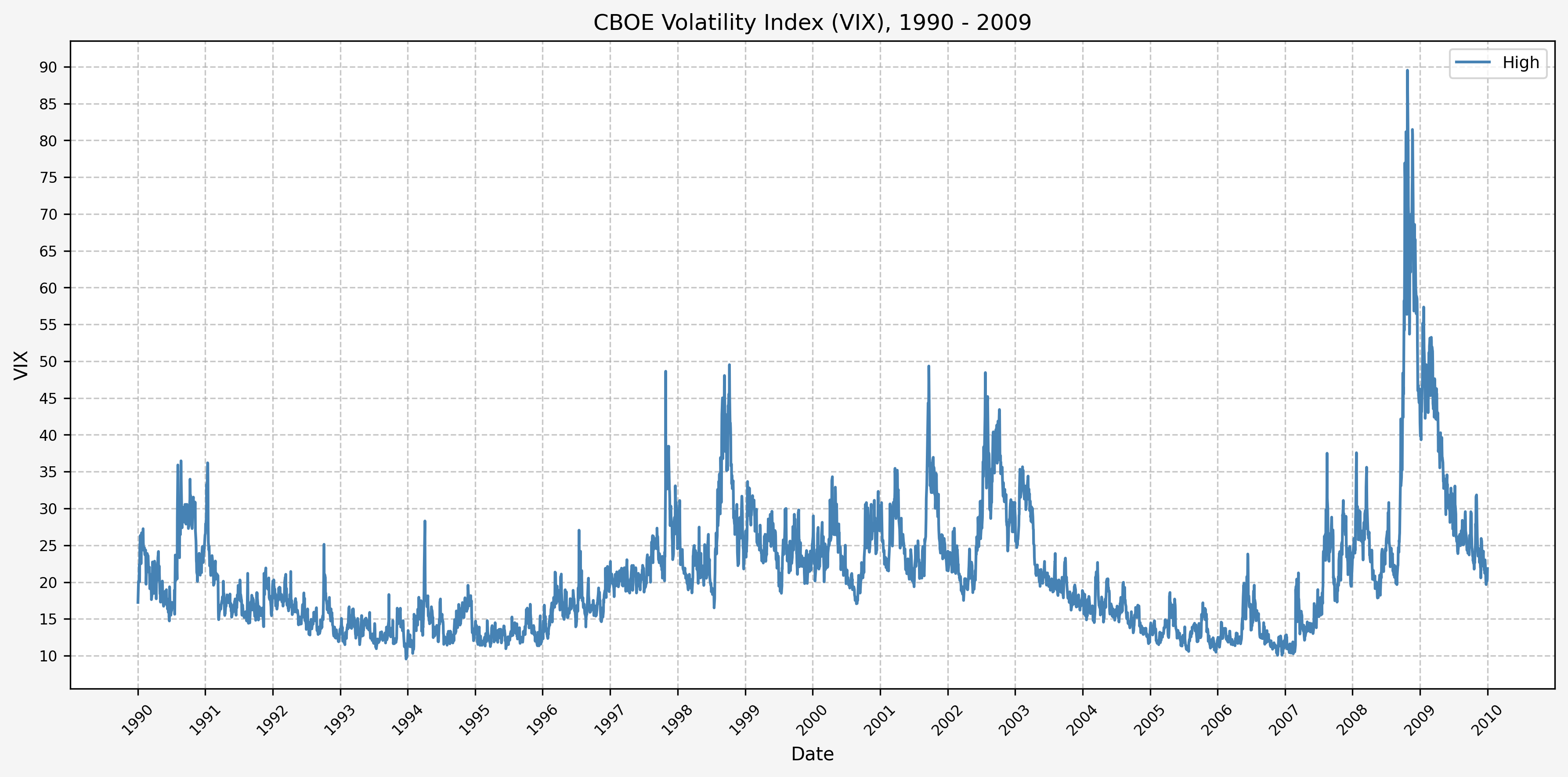

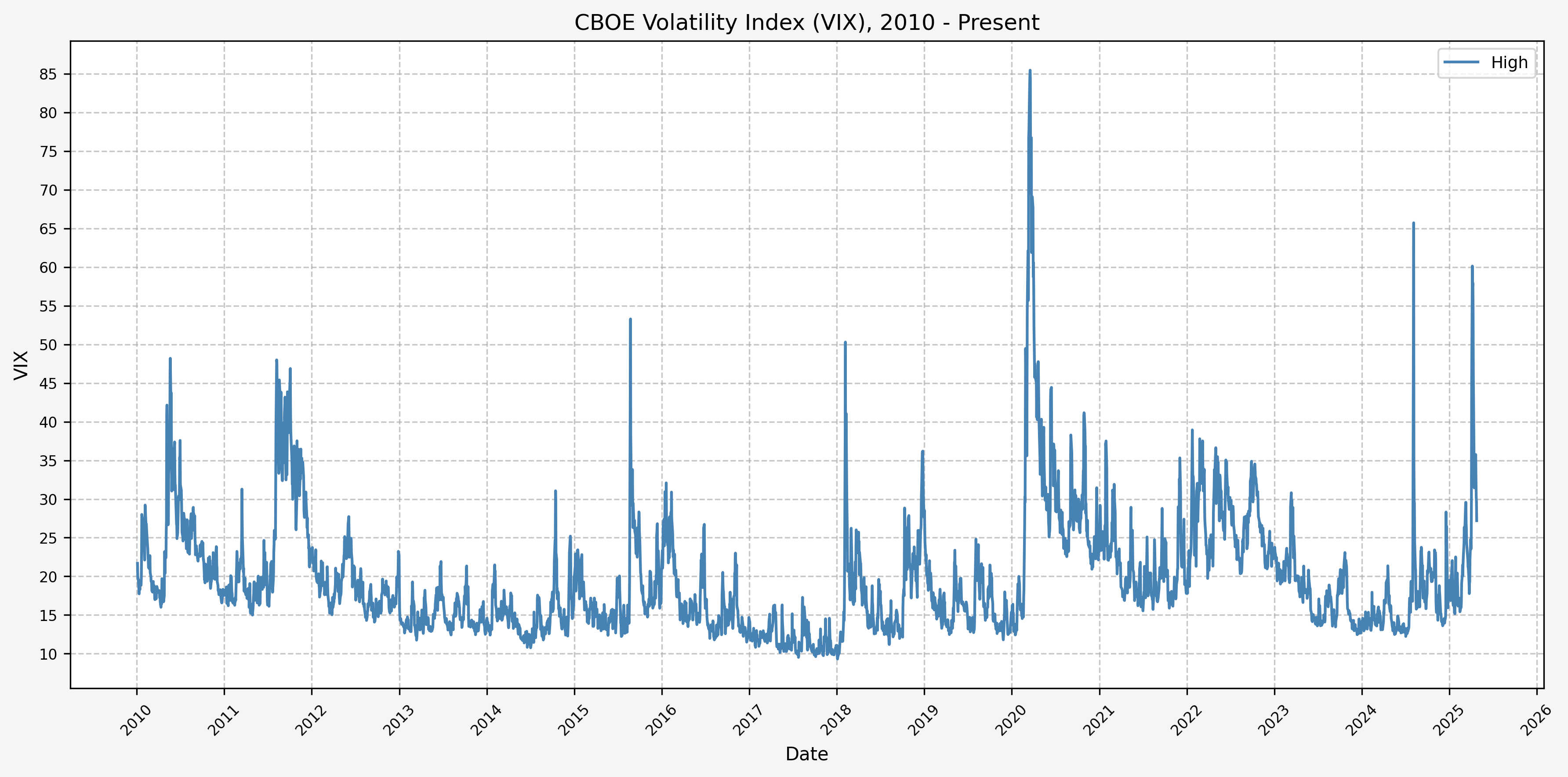

Here’s two plots for the dataset. The first covers 1990 - 2009, and the second 2010 - 2024. This is the daily high level:

1990 - 2009

2010 - Present

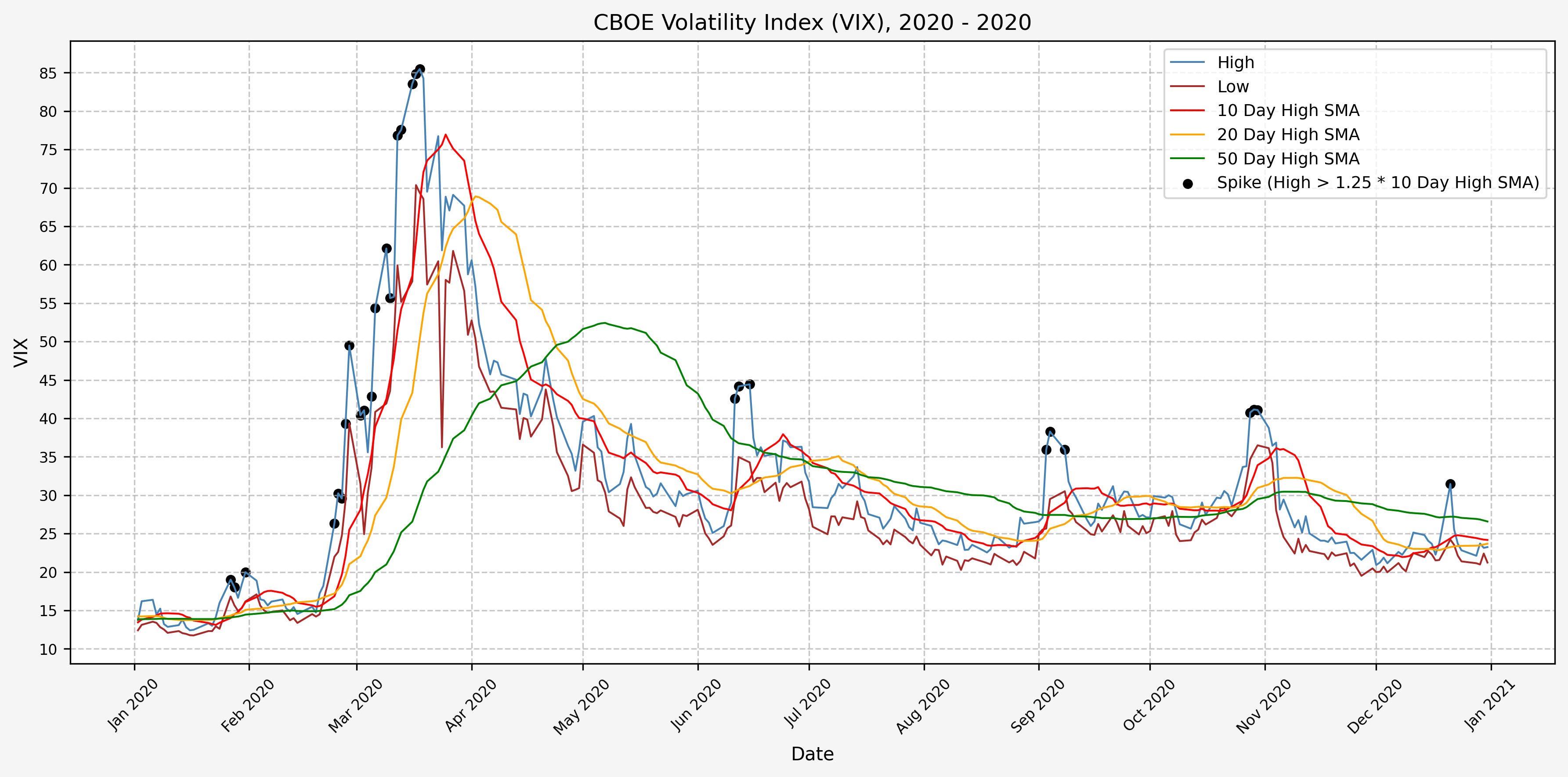

From these plots, we can see the following:

- The VIX has really only jumped above 50 several times (GFC, COVID, recently in August of 2024)

- The highest levels (> 80) occured only during the GFC & COVID

- Interestingly, the VIX did not ever get above 50 during the .com bubble

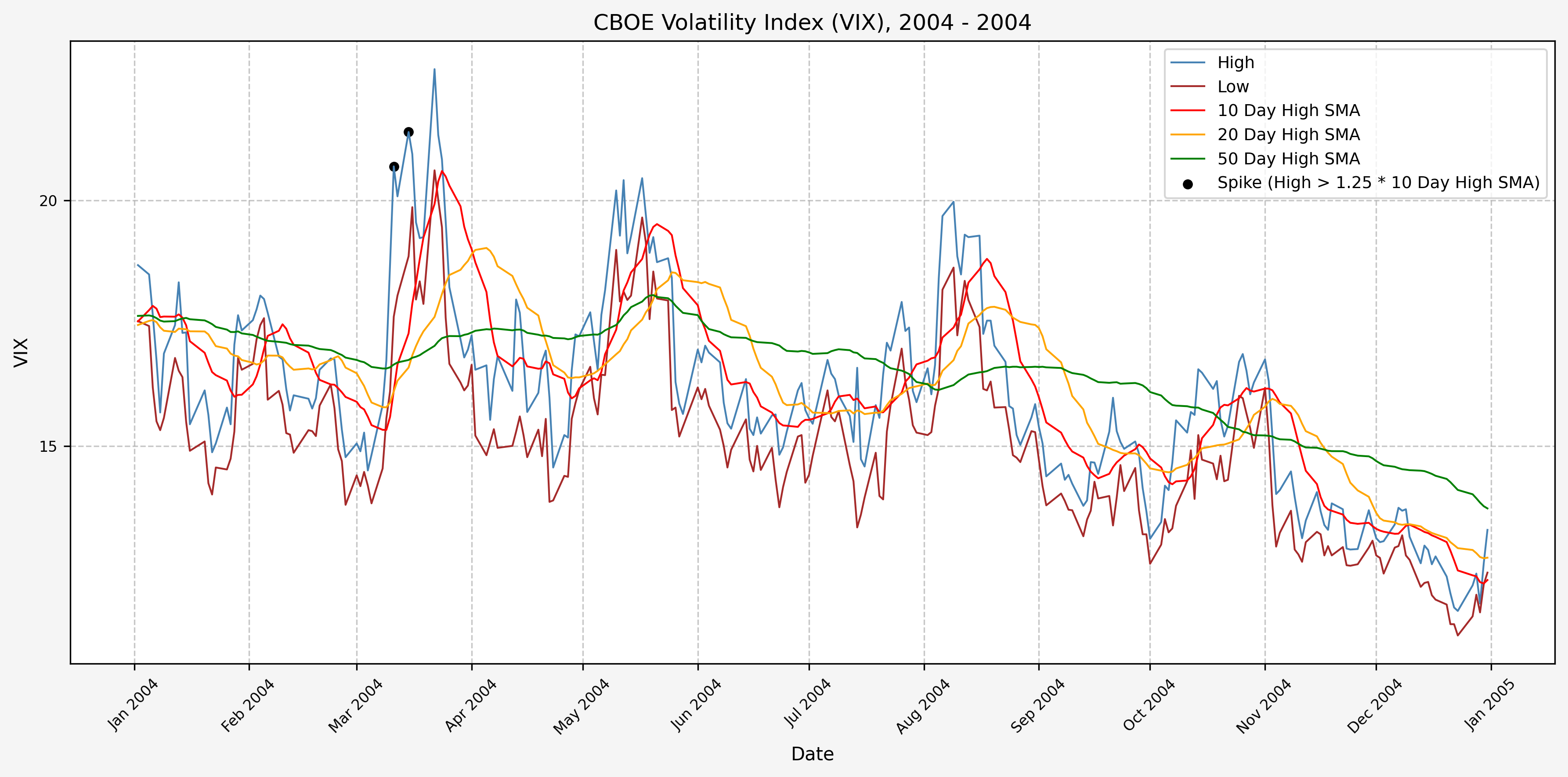

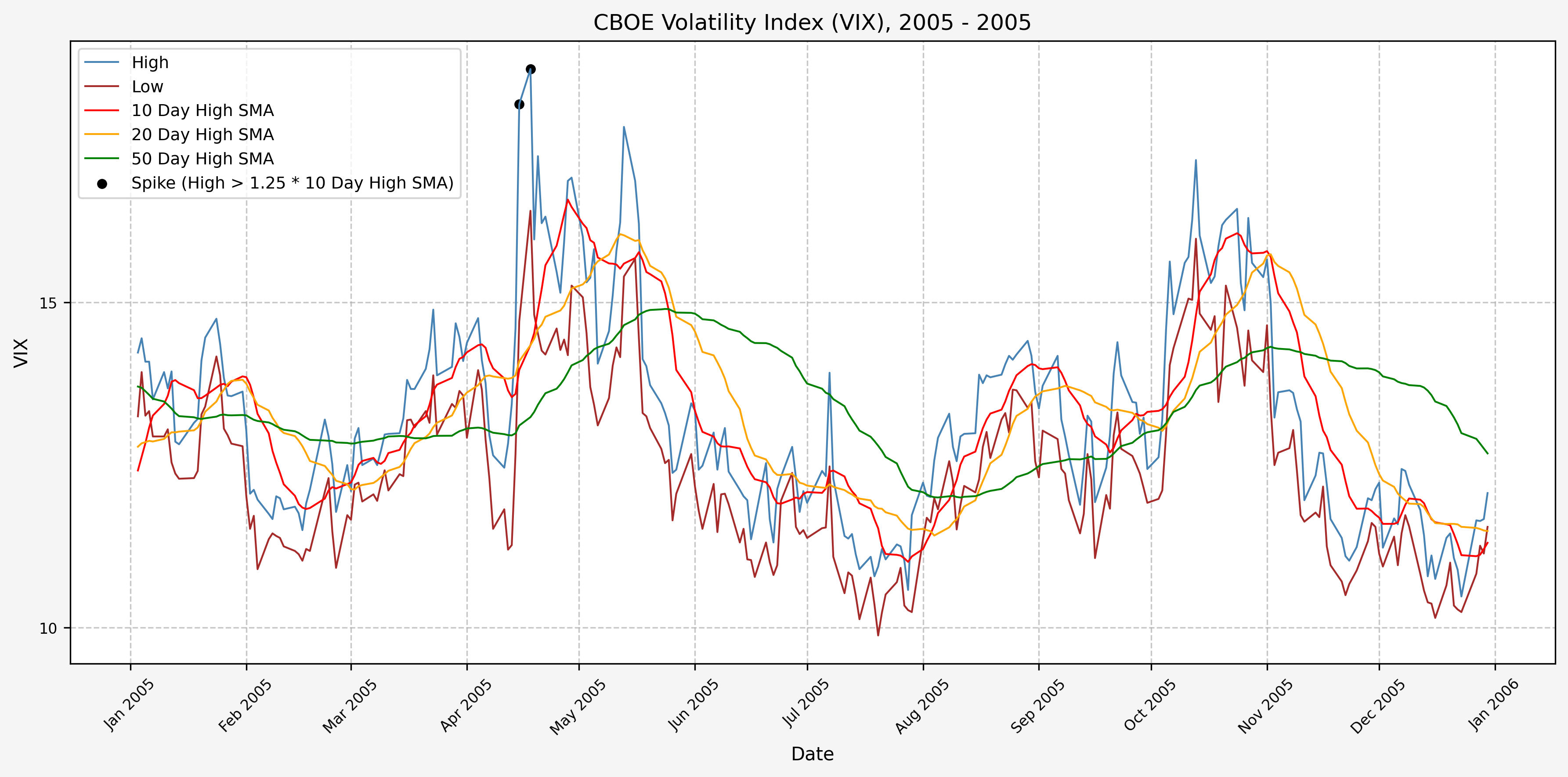

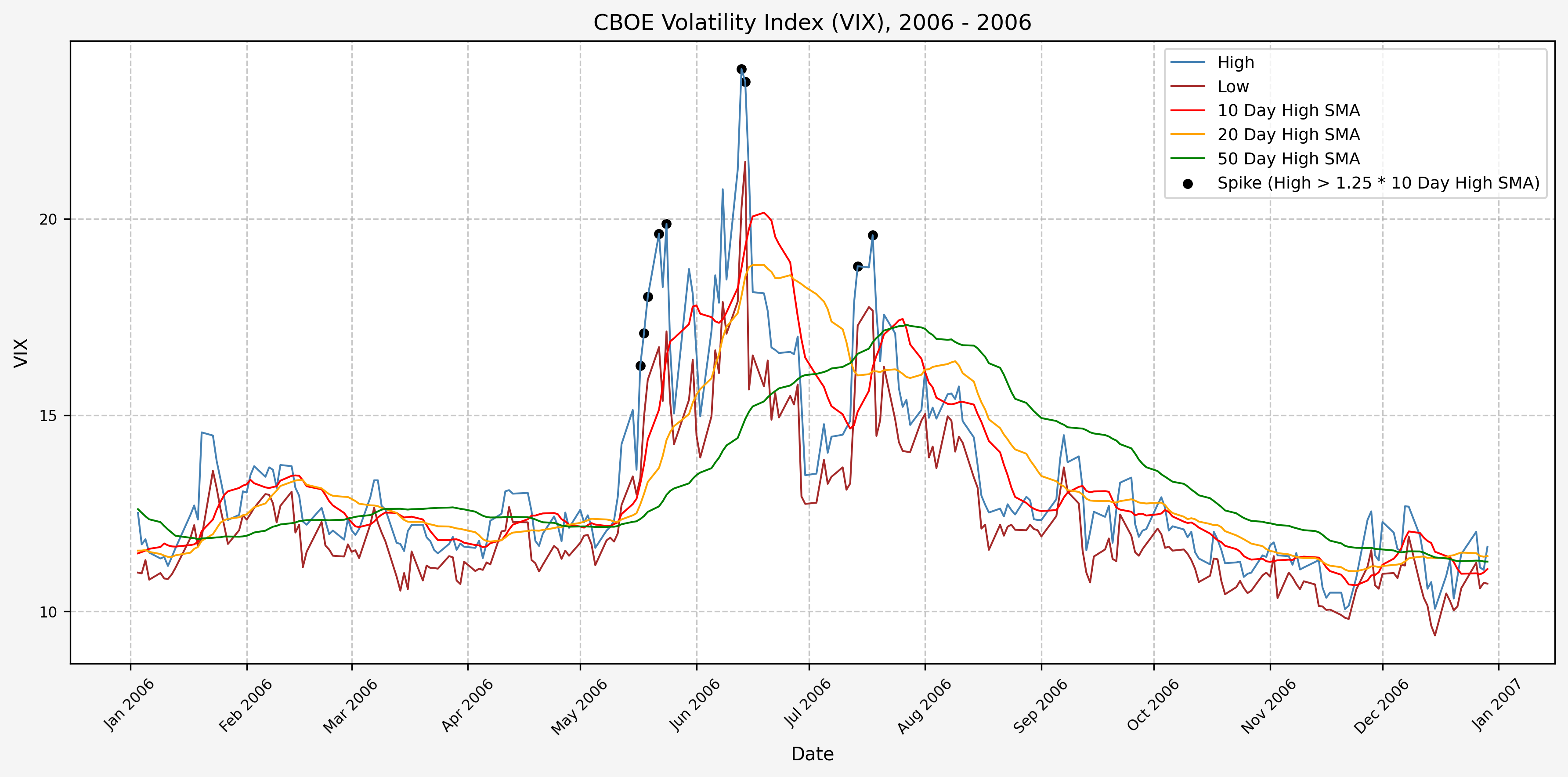

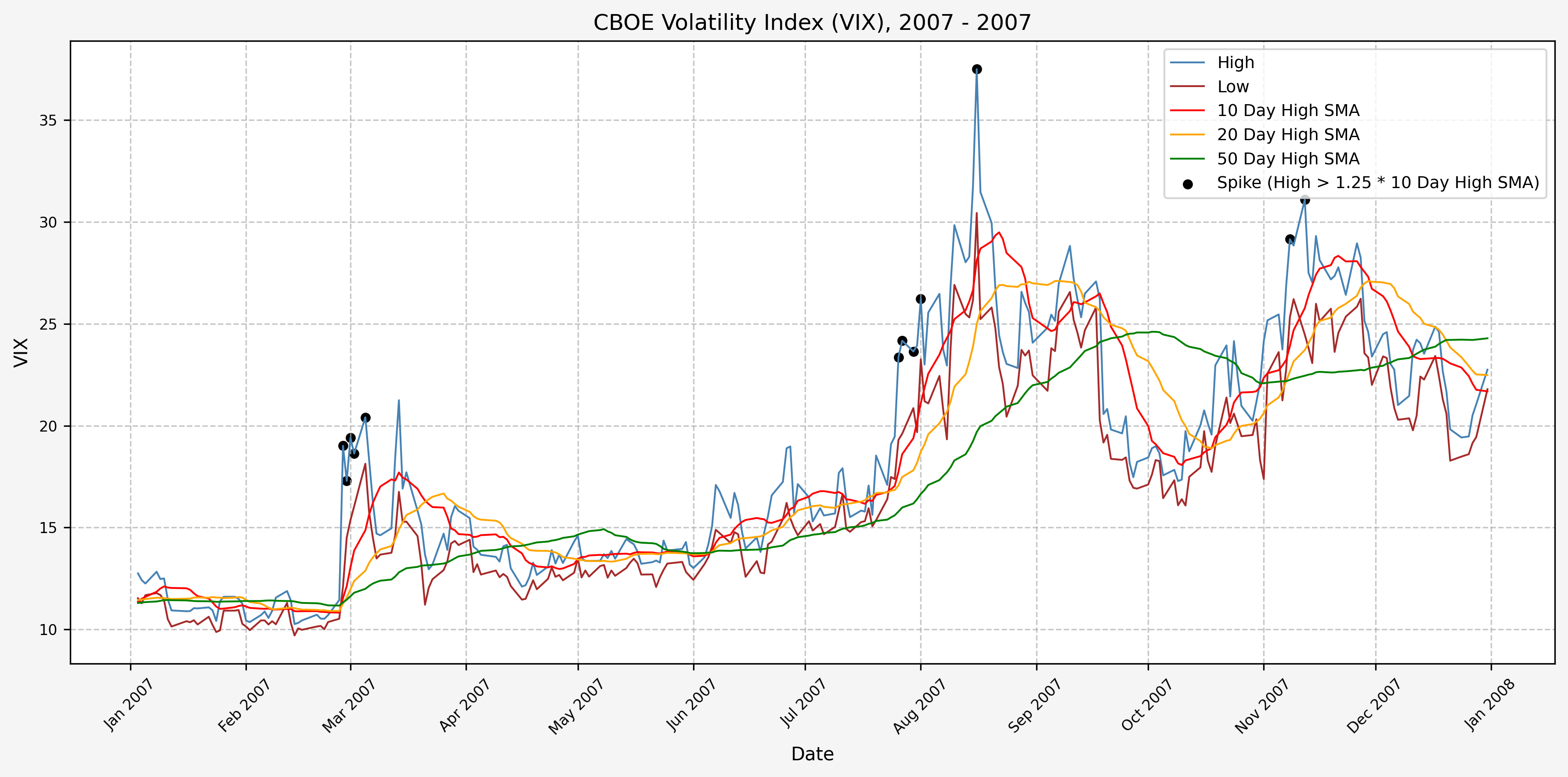

Investigating A Signal

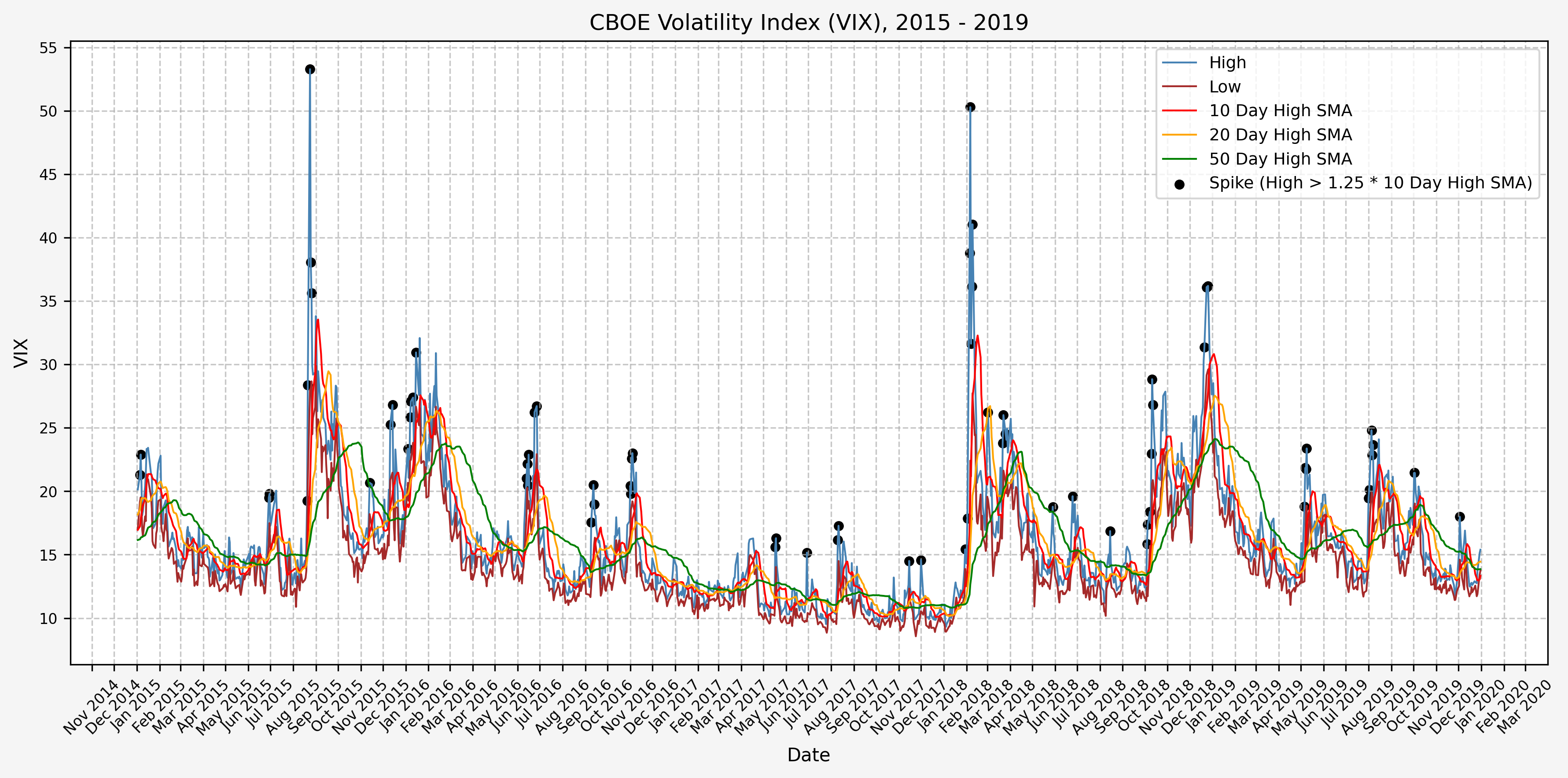

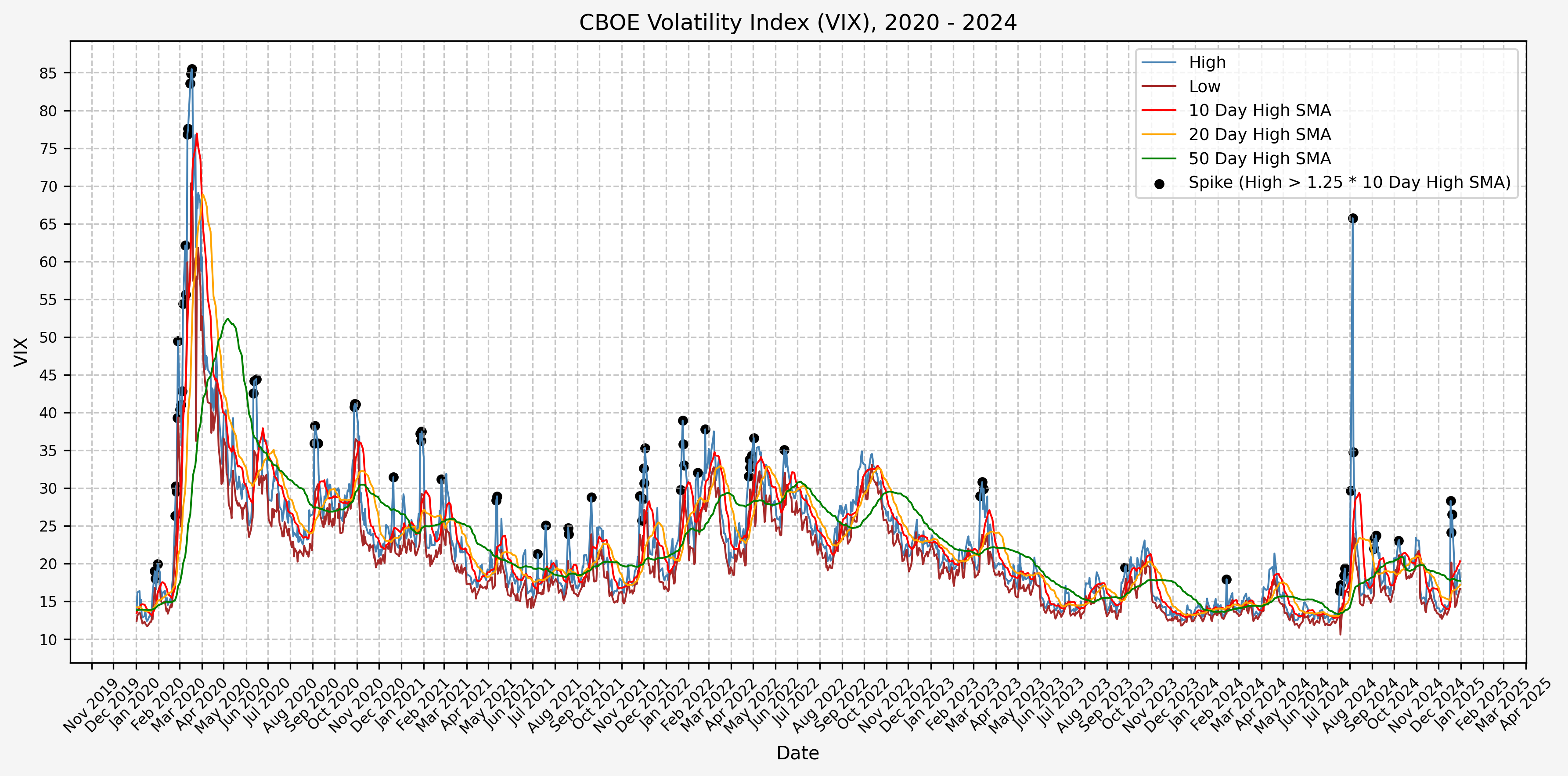

Next, we will consider the idea of a spike level in the VIX and how we might use a spike level to generate a signal. These elevated levels usually occur during market sell-off events or longer term drawdowns in the S&P 500. Sometimes the VIX reverts to recent levels after a spike, but other times levels remain elevated for weeks or even months.

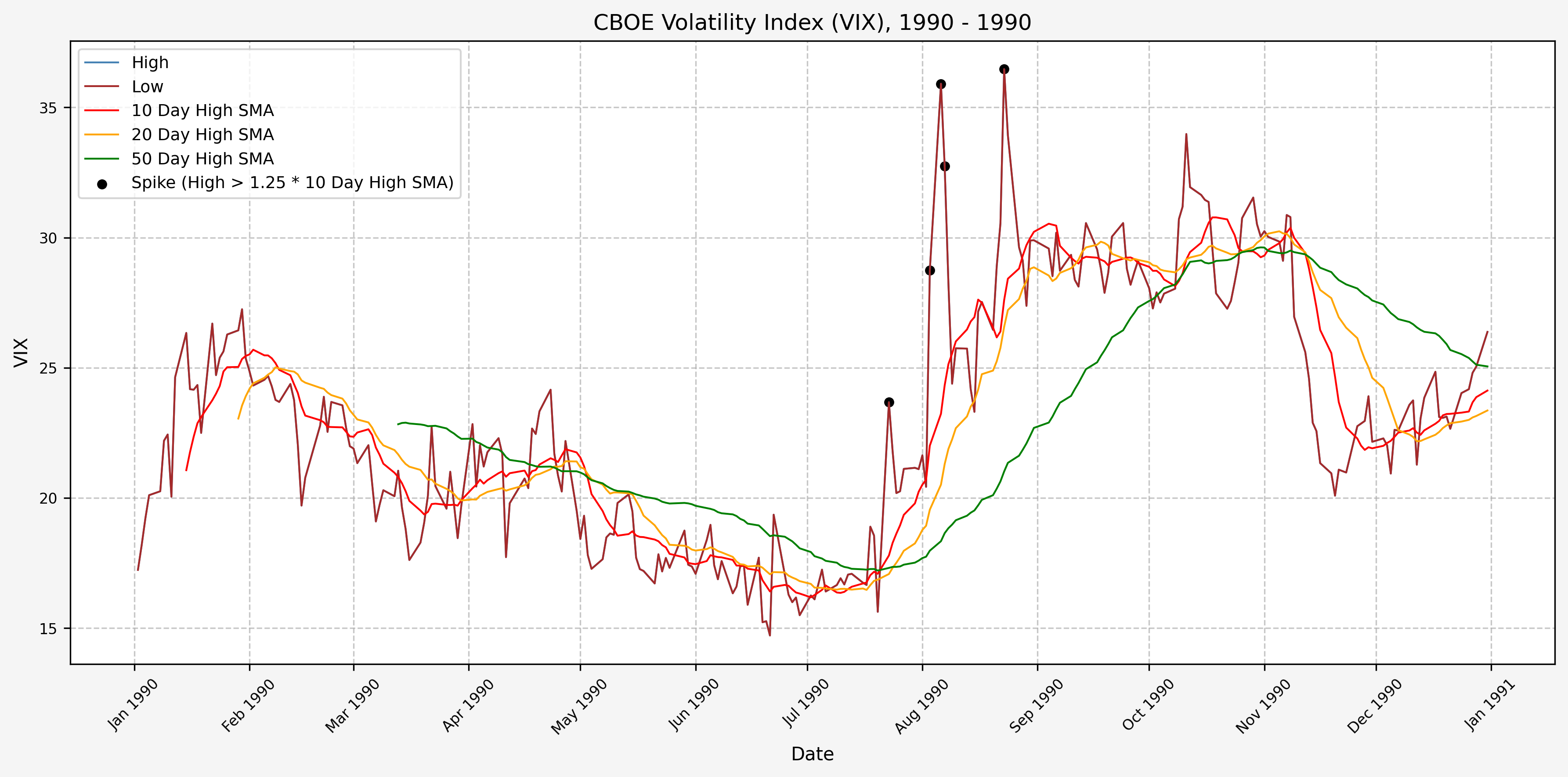

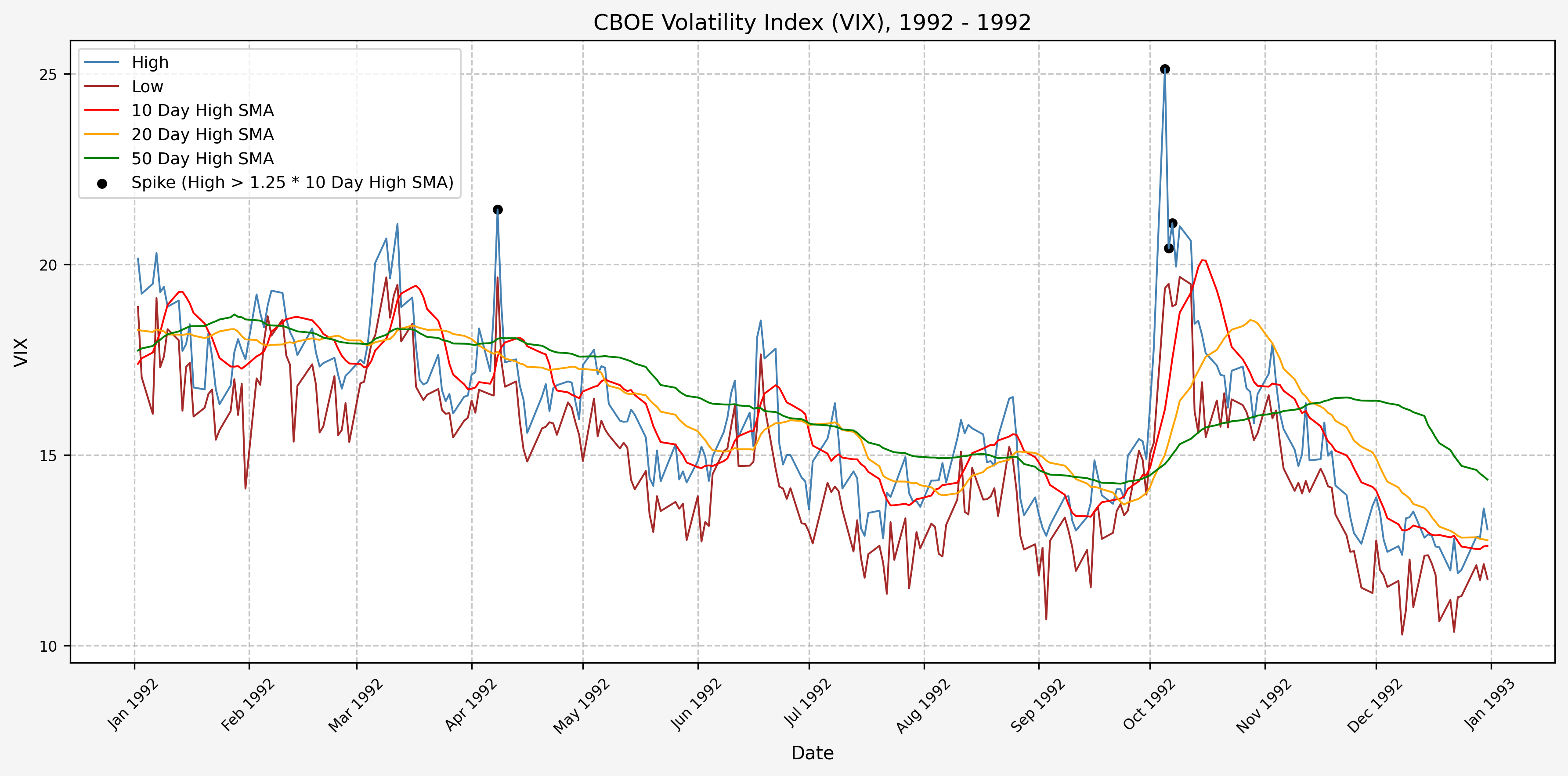

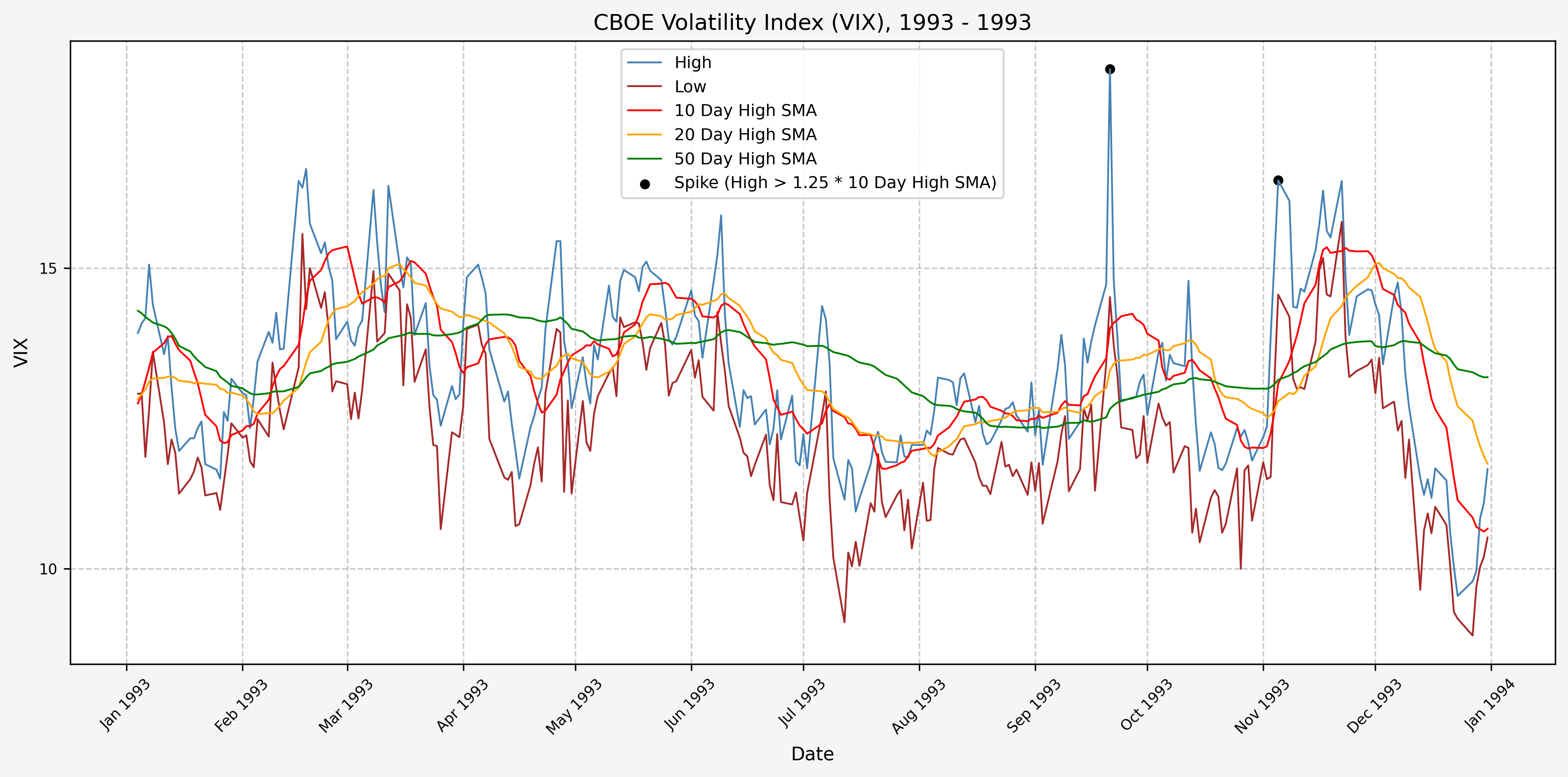

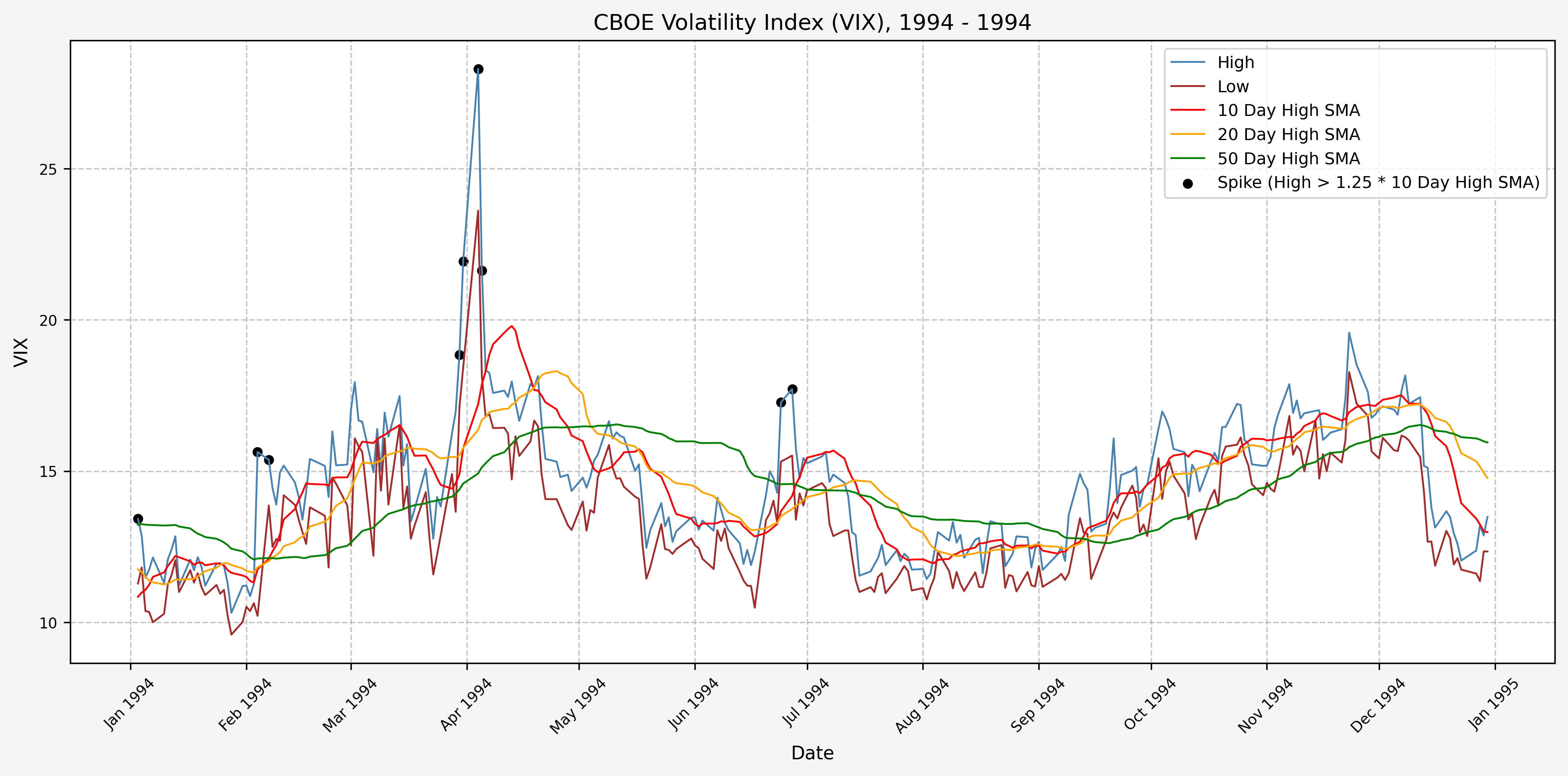

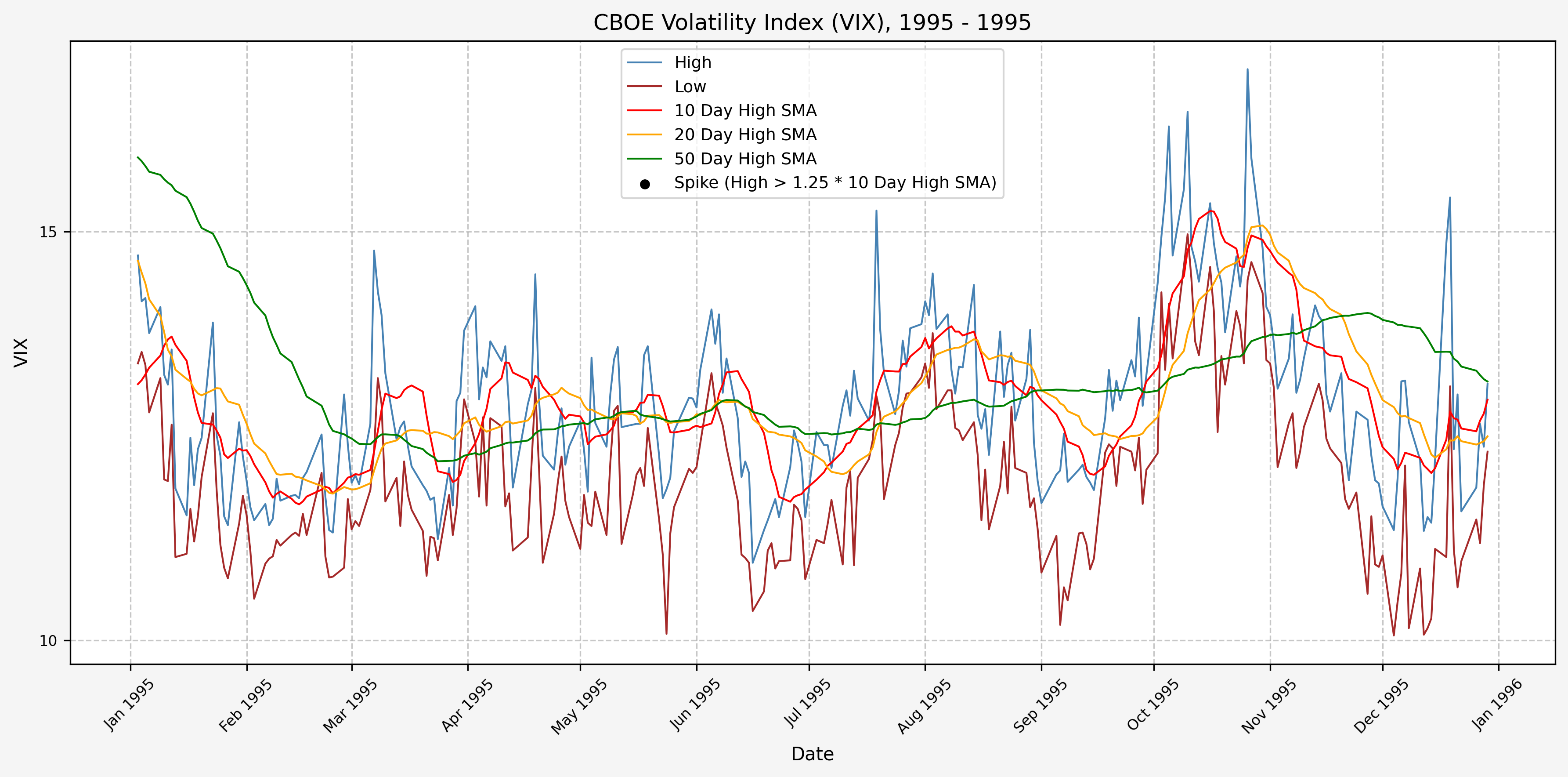

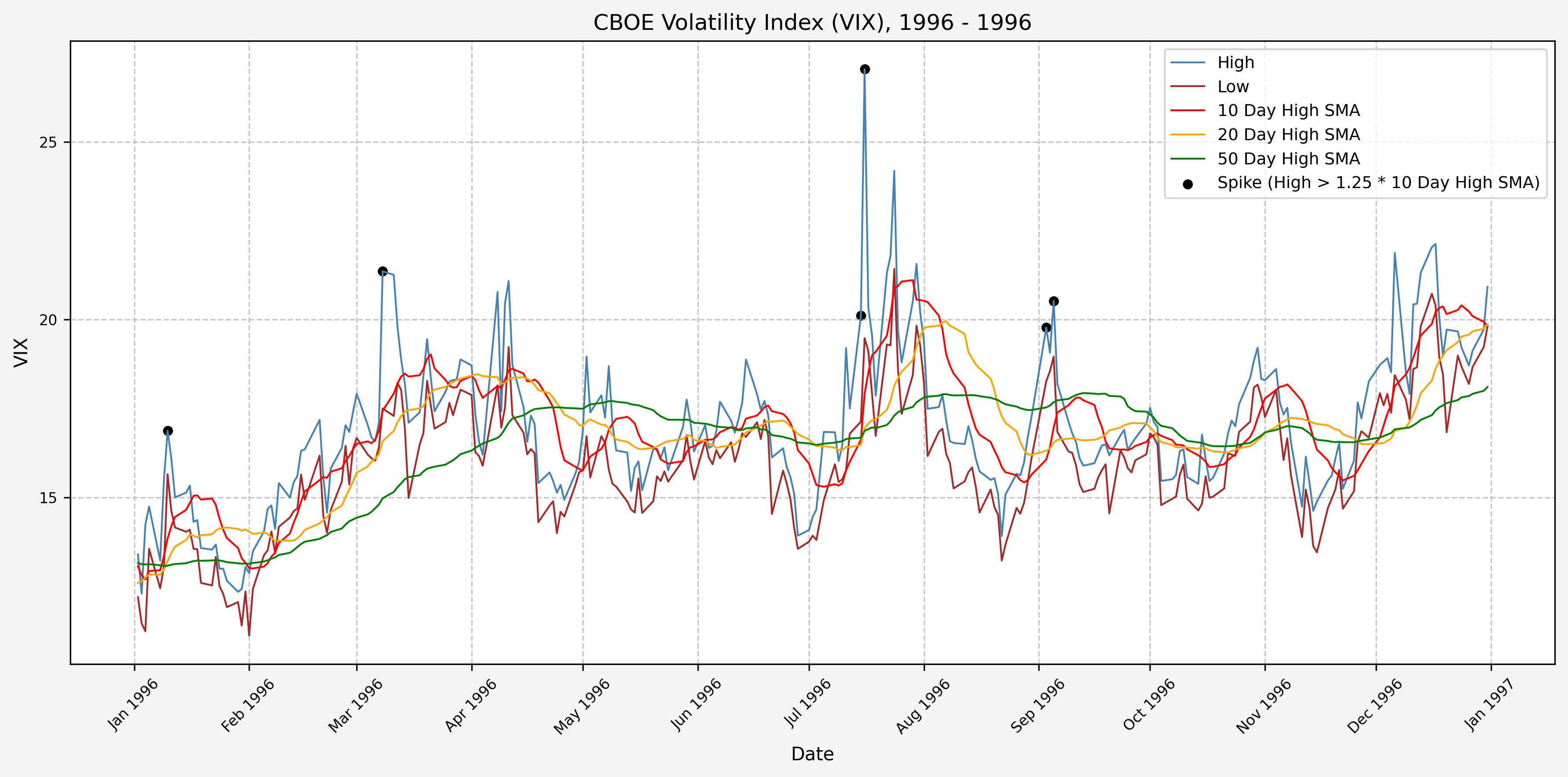

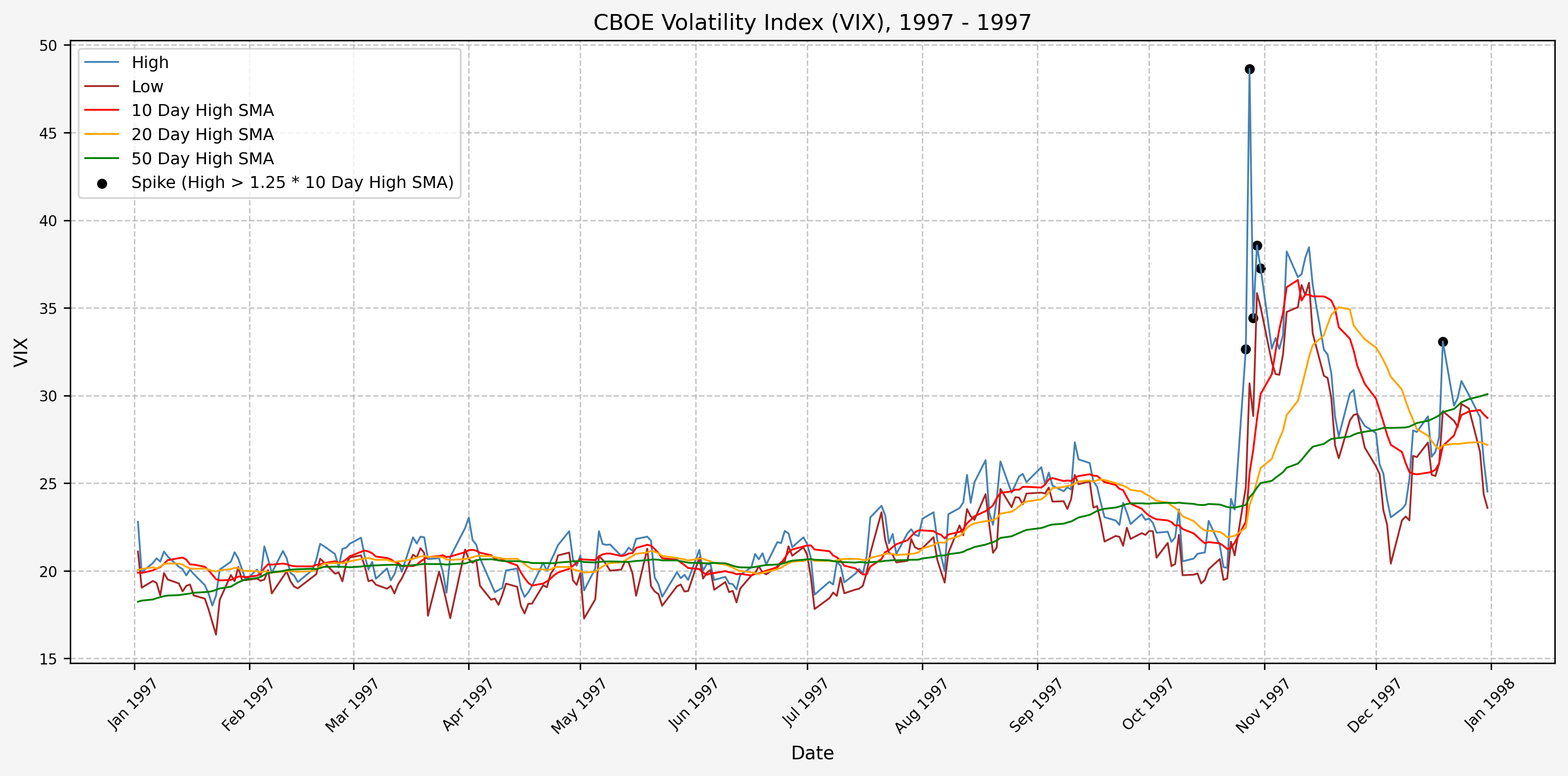

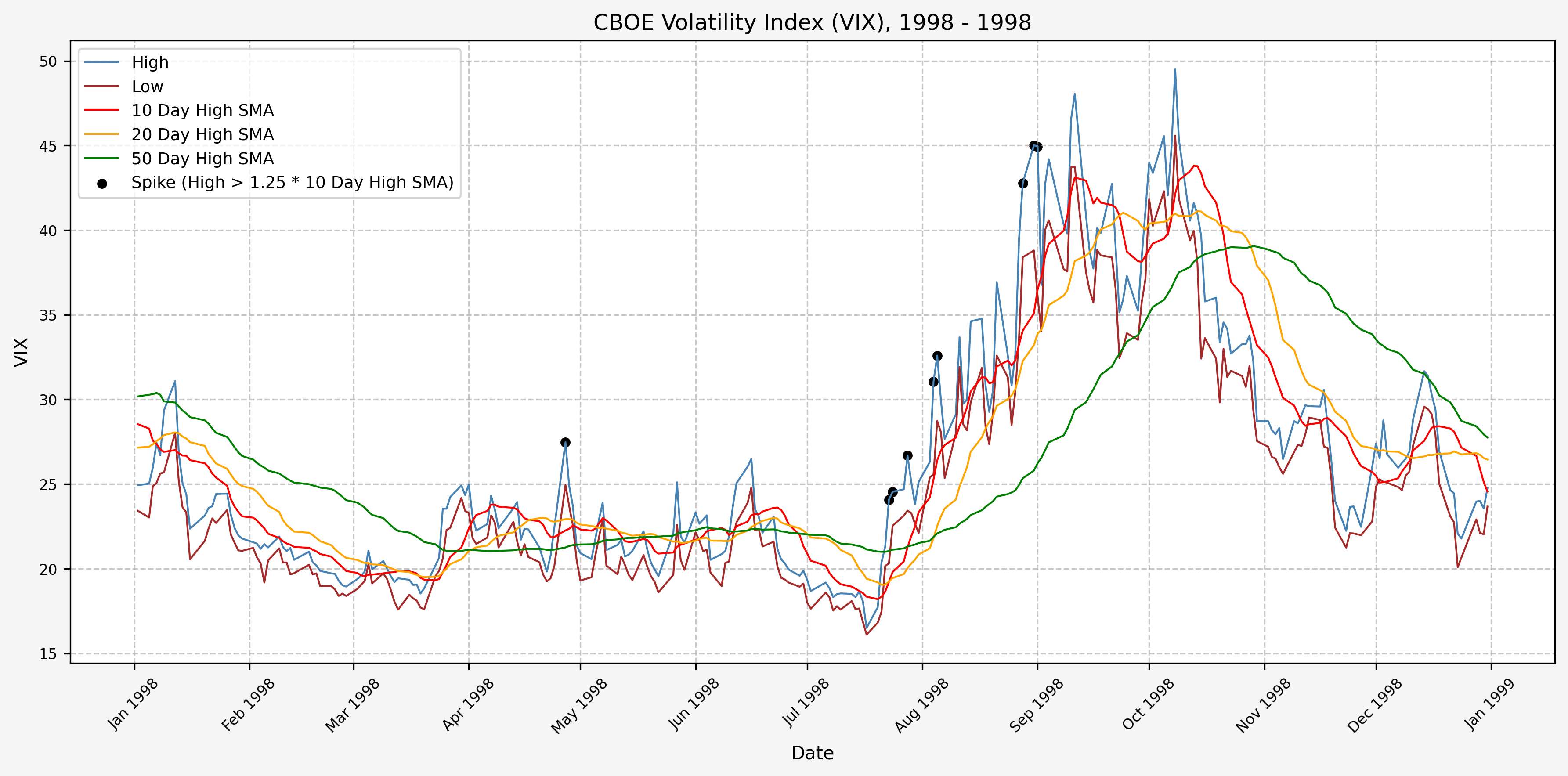

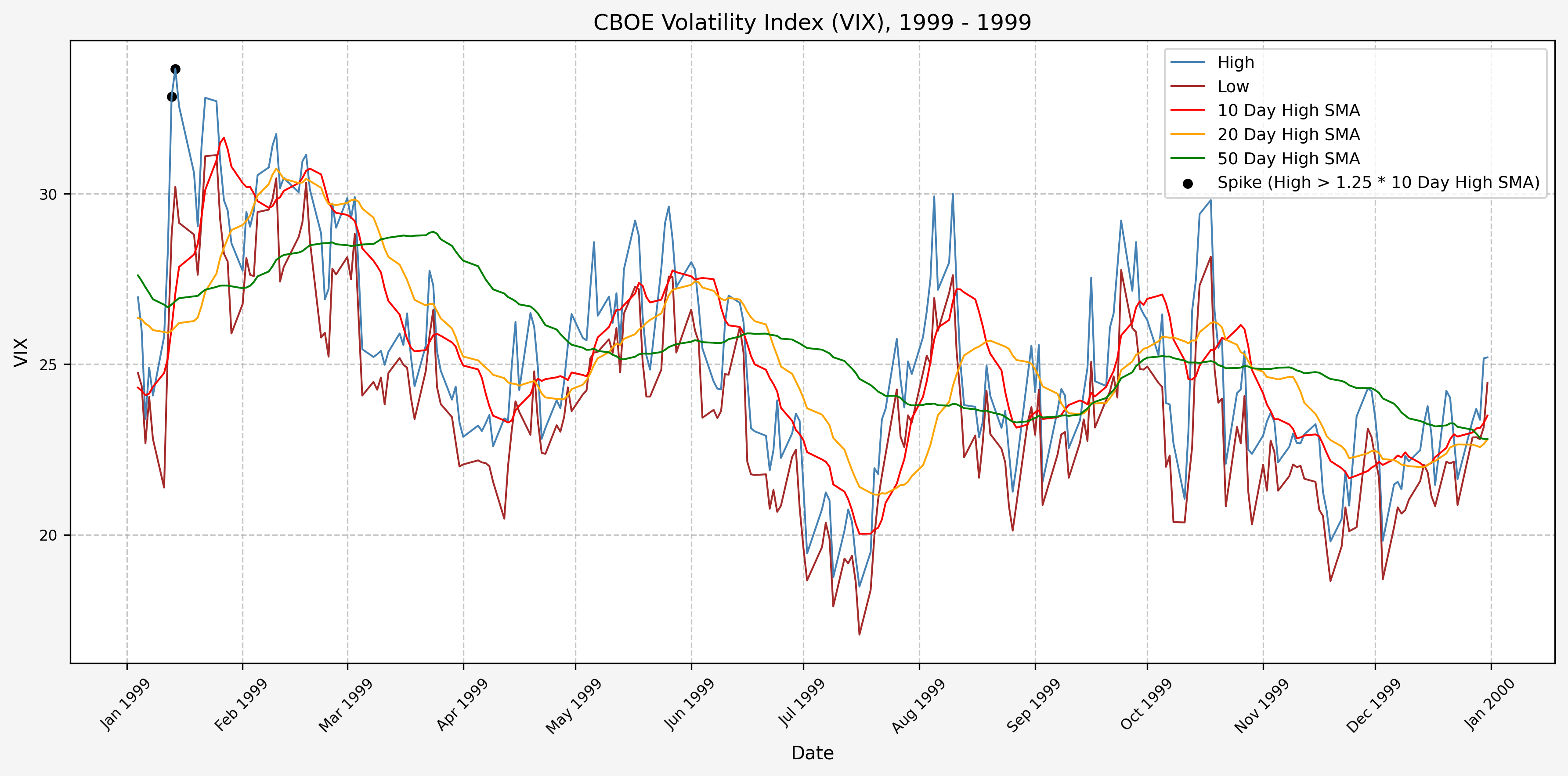

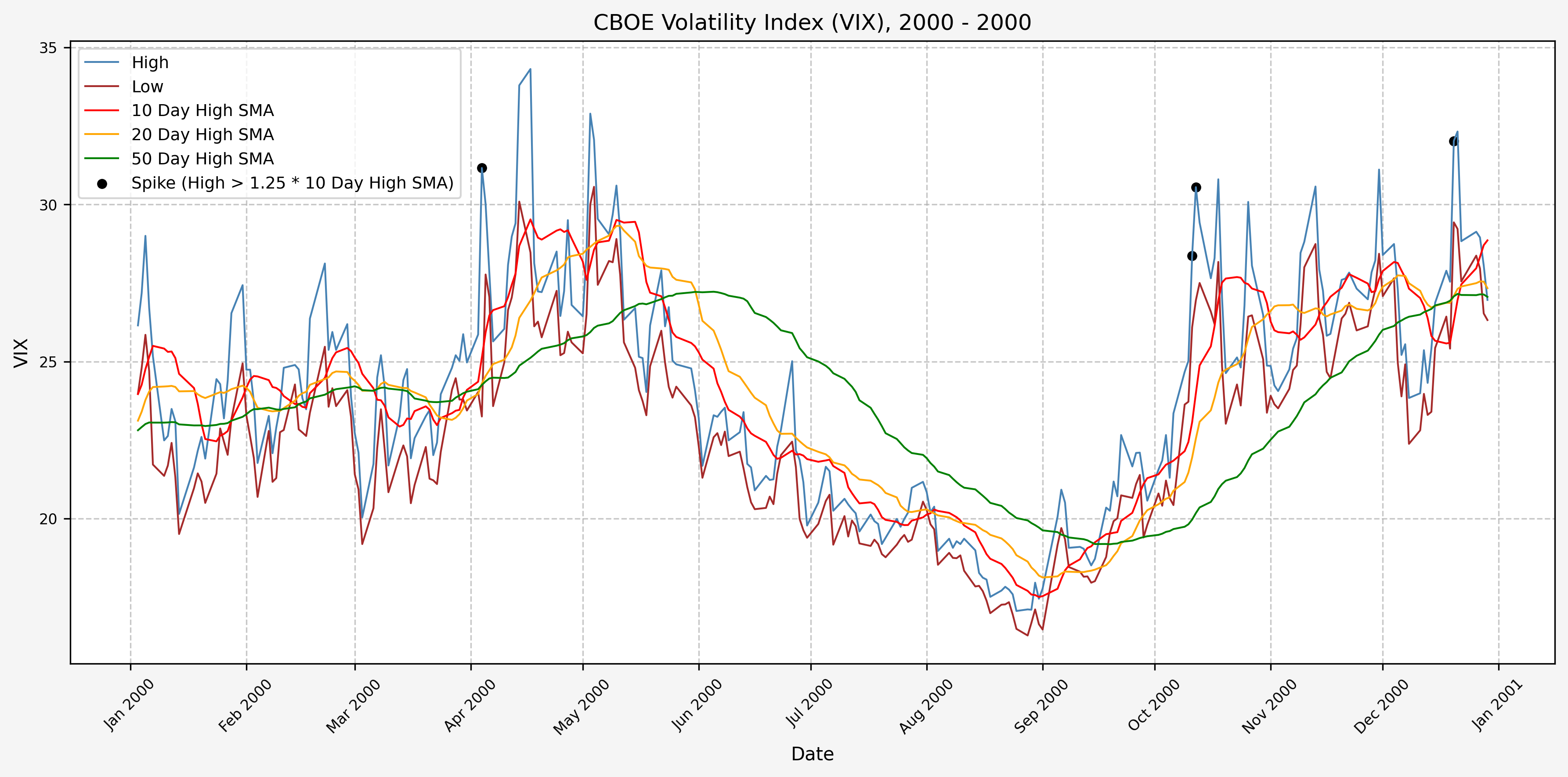

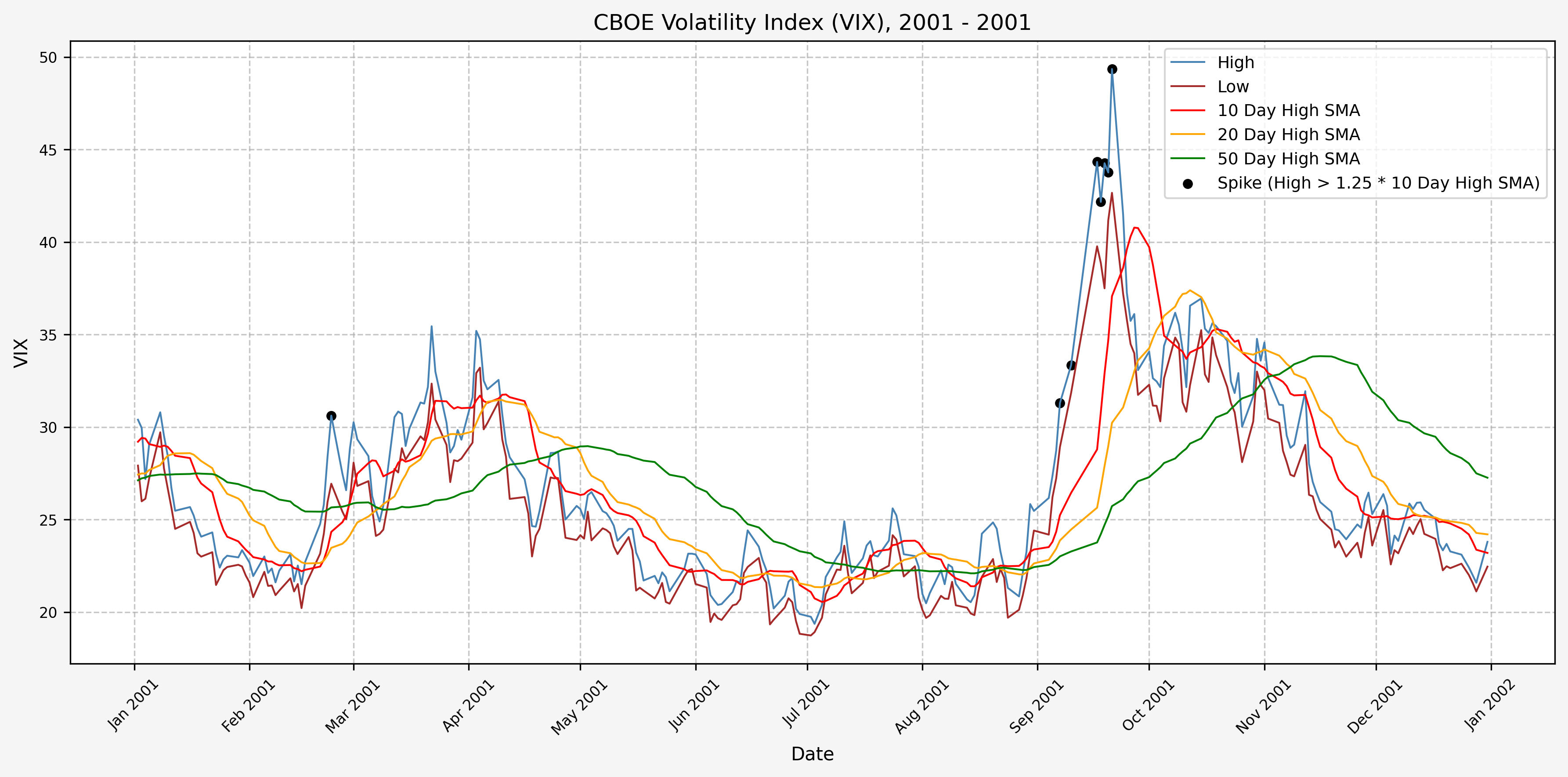

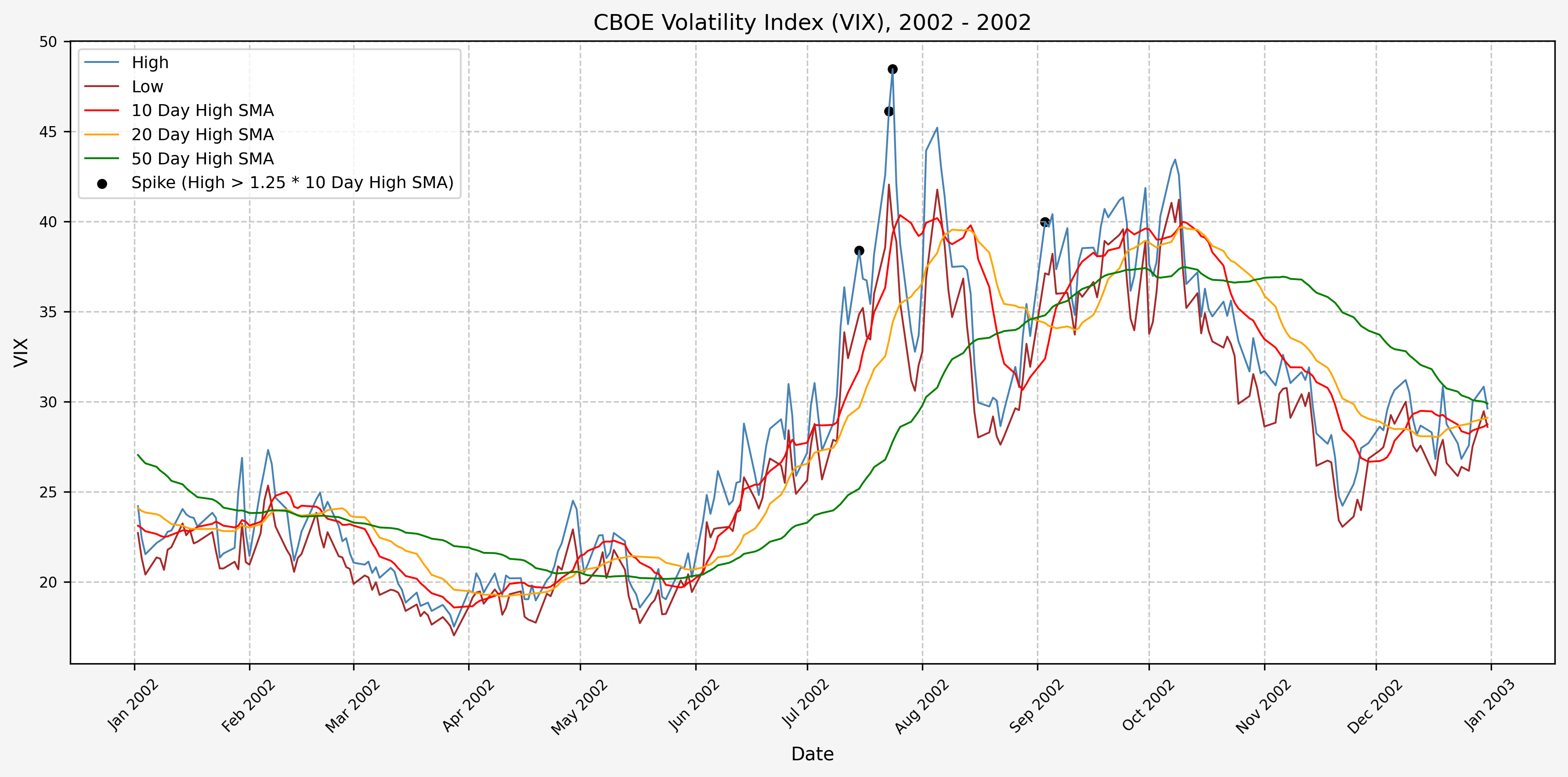

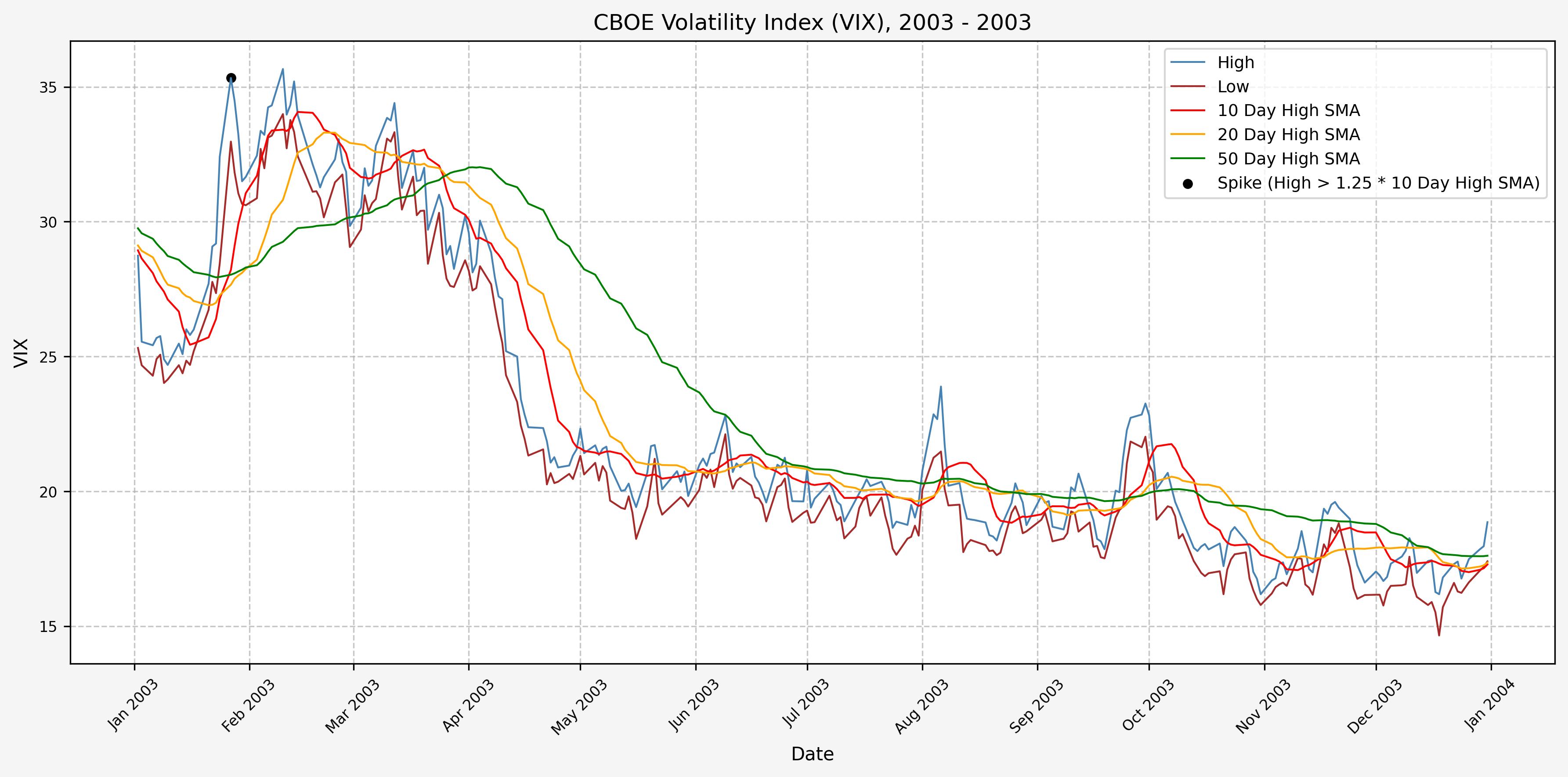

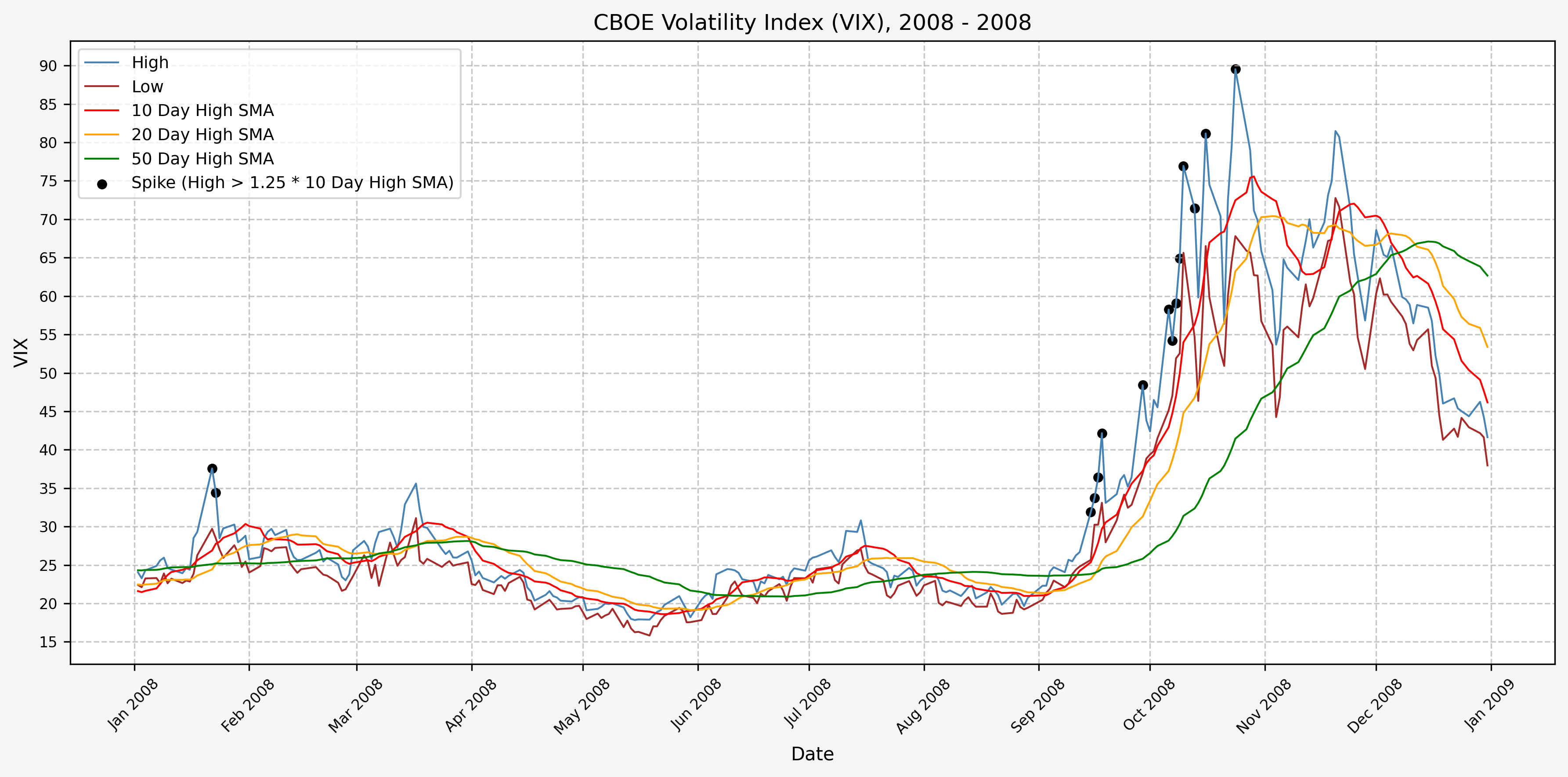

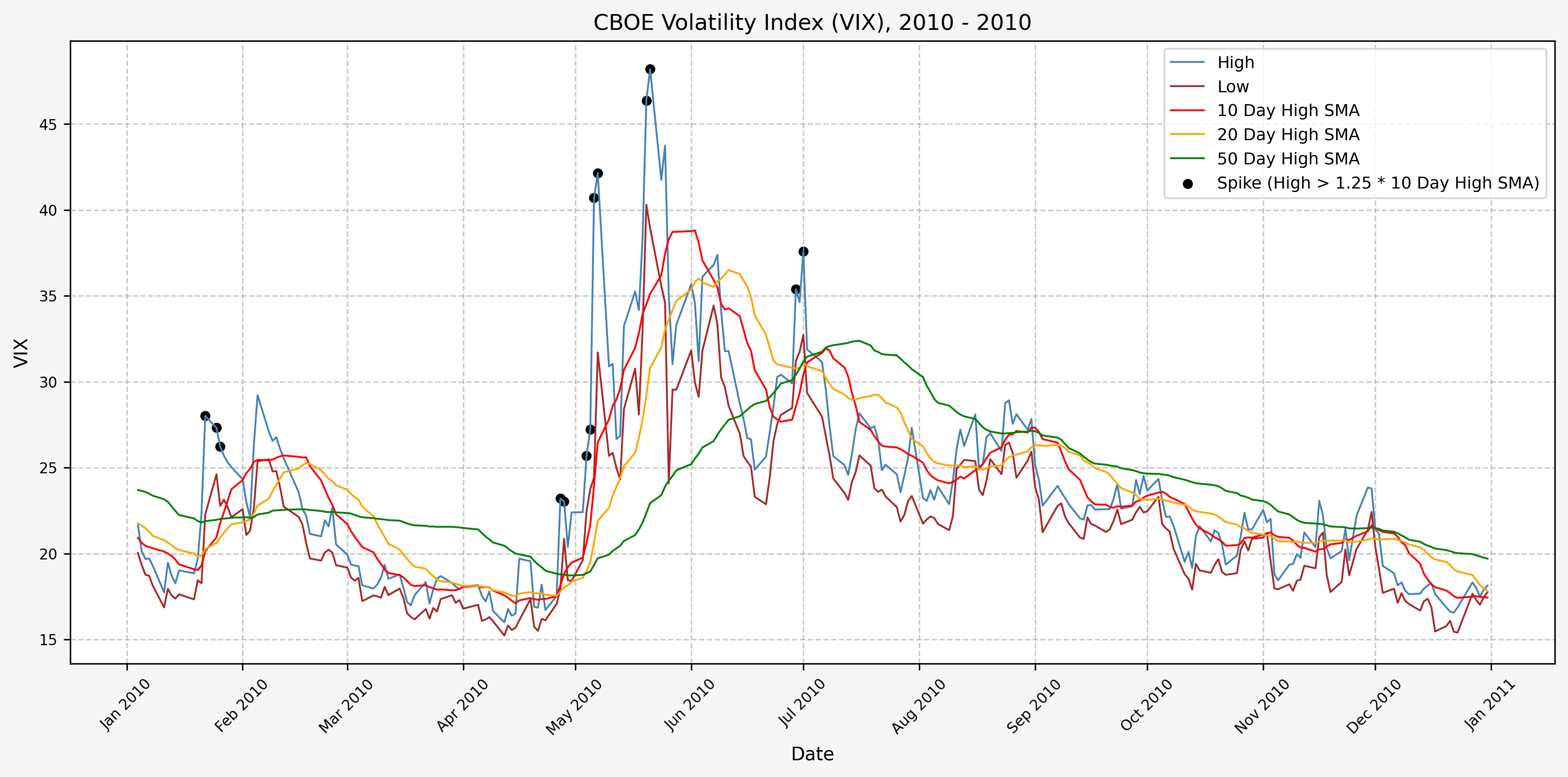

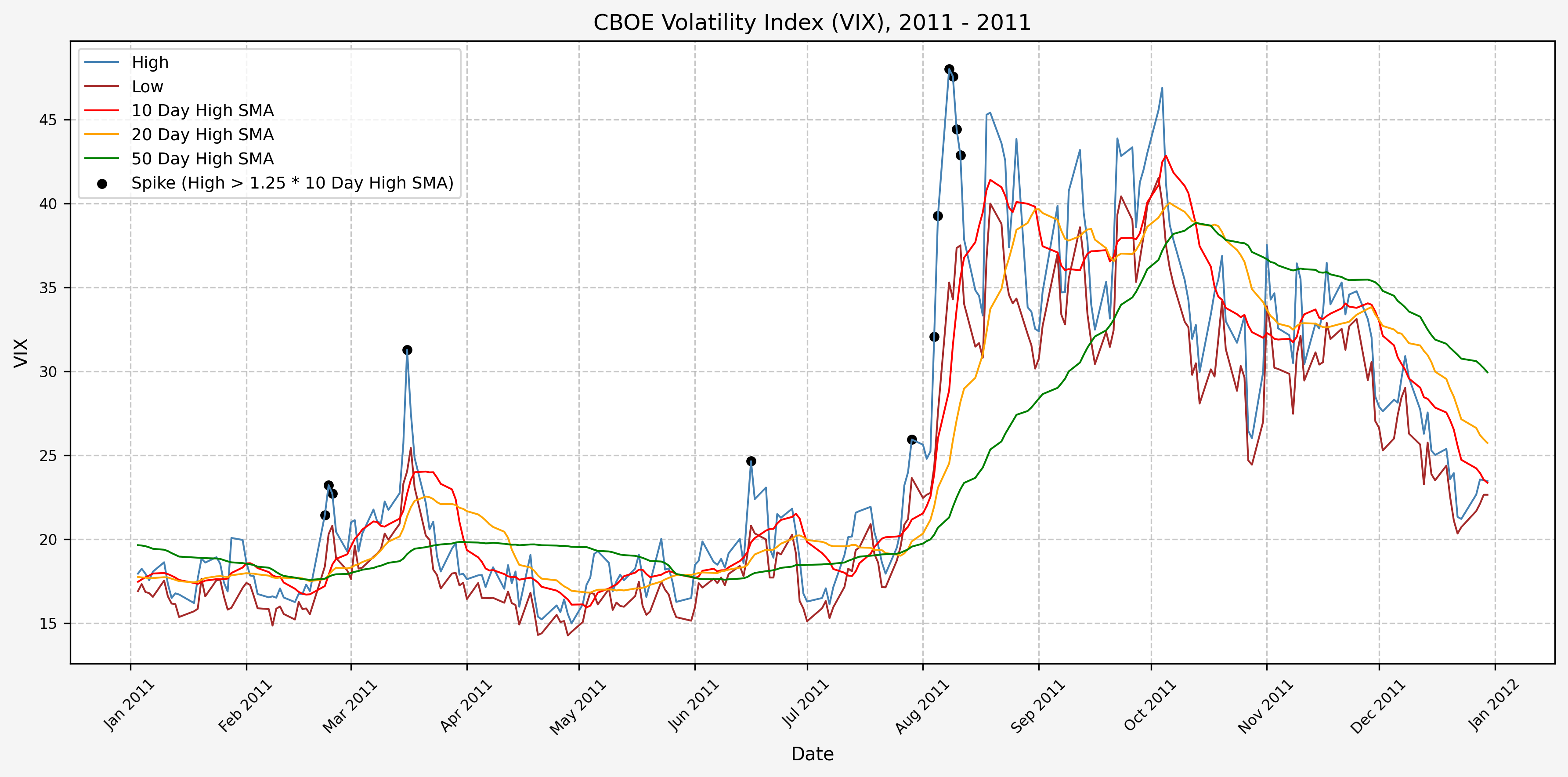

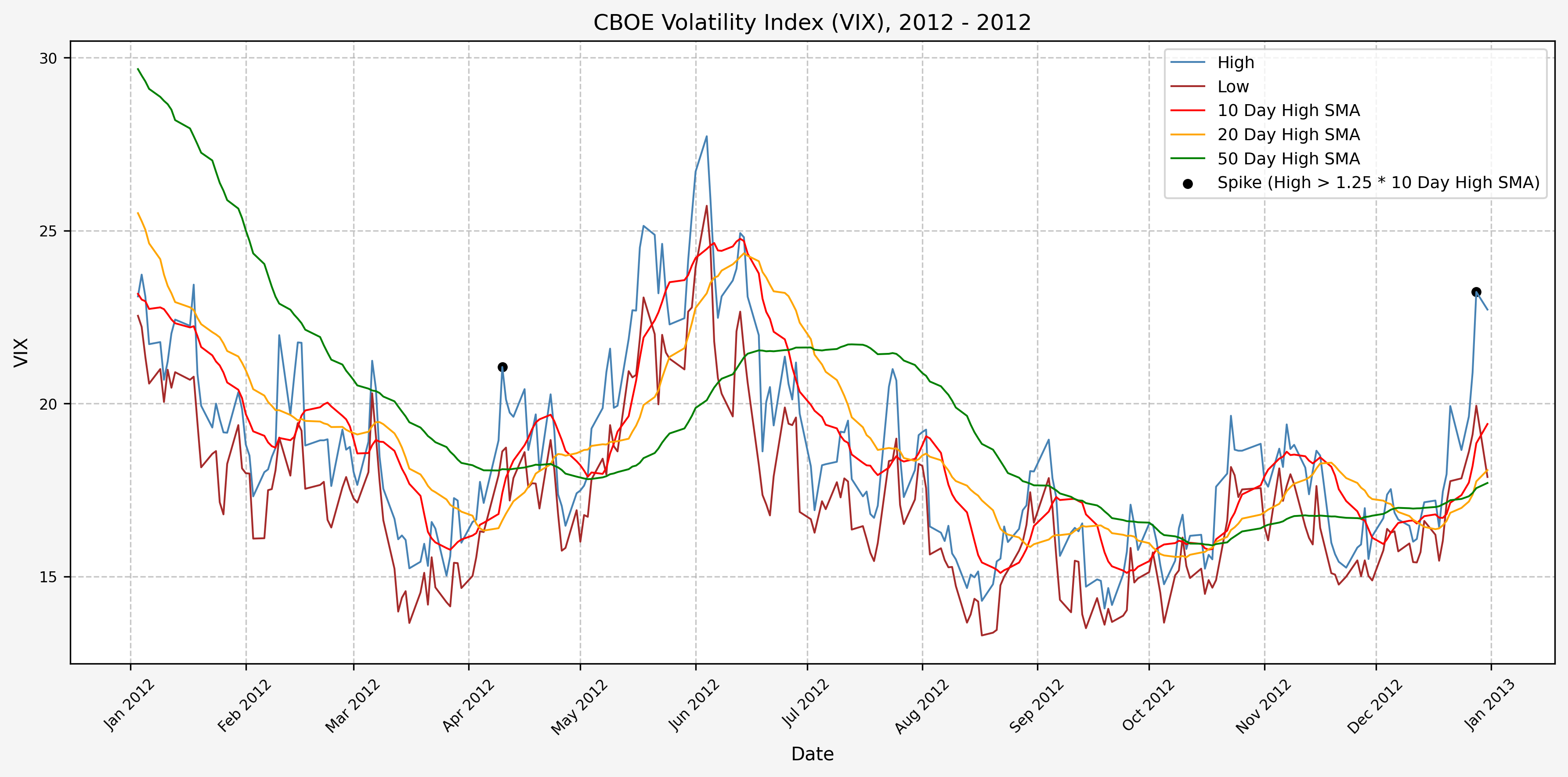

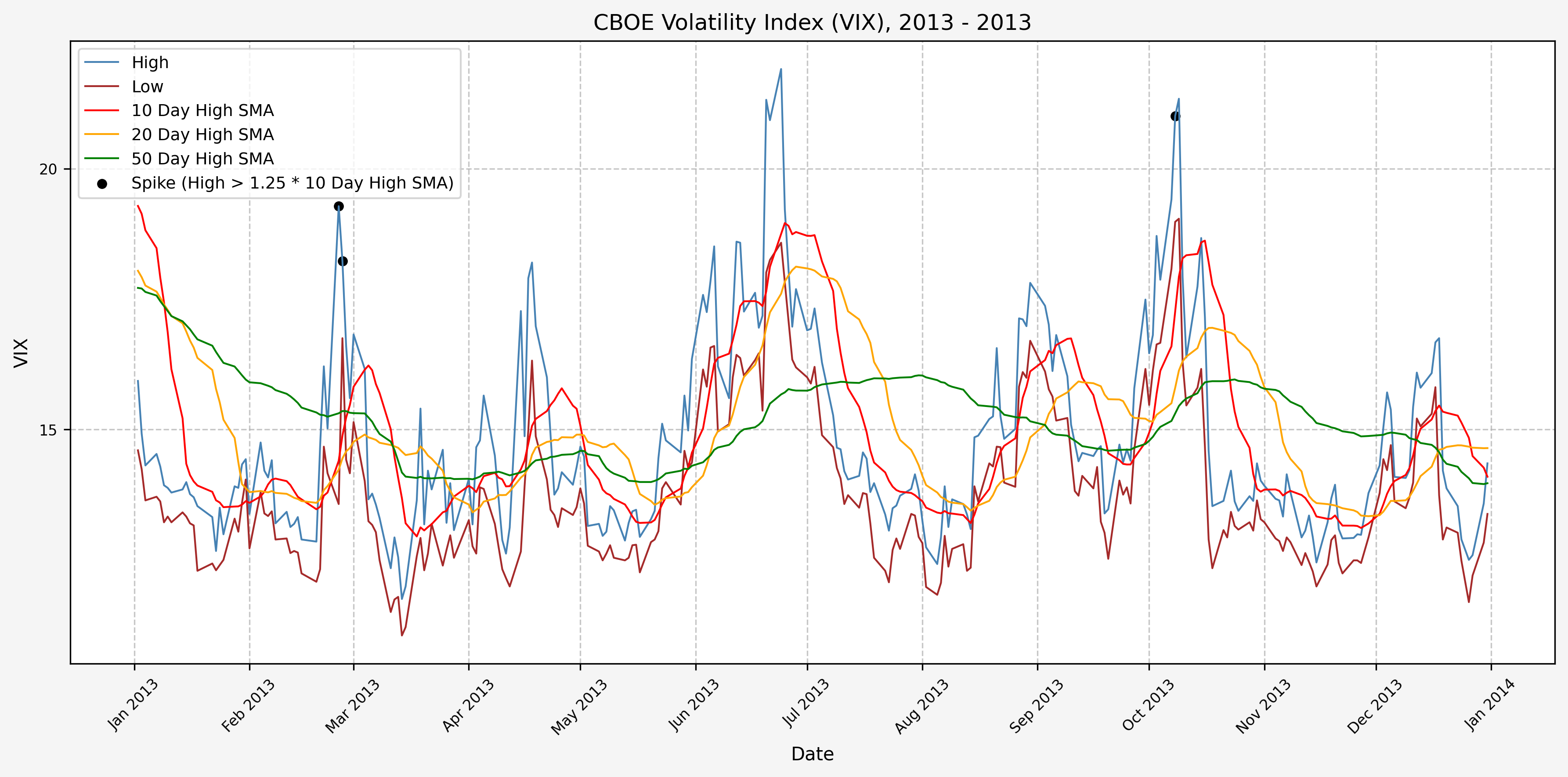

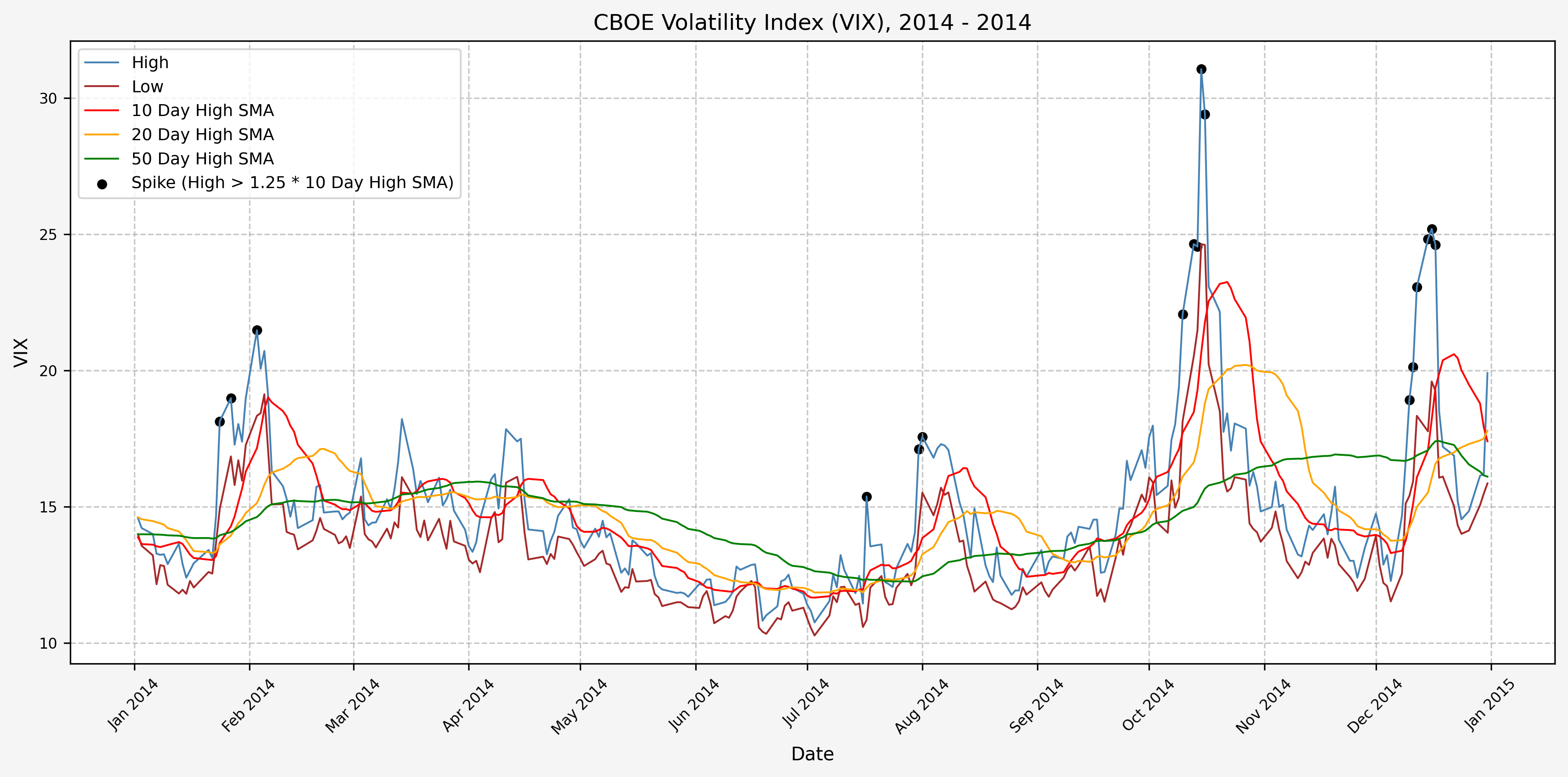

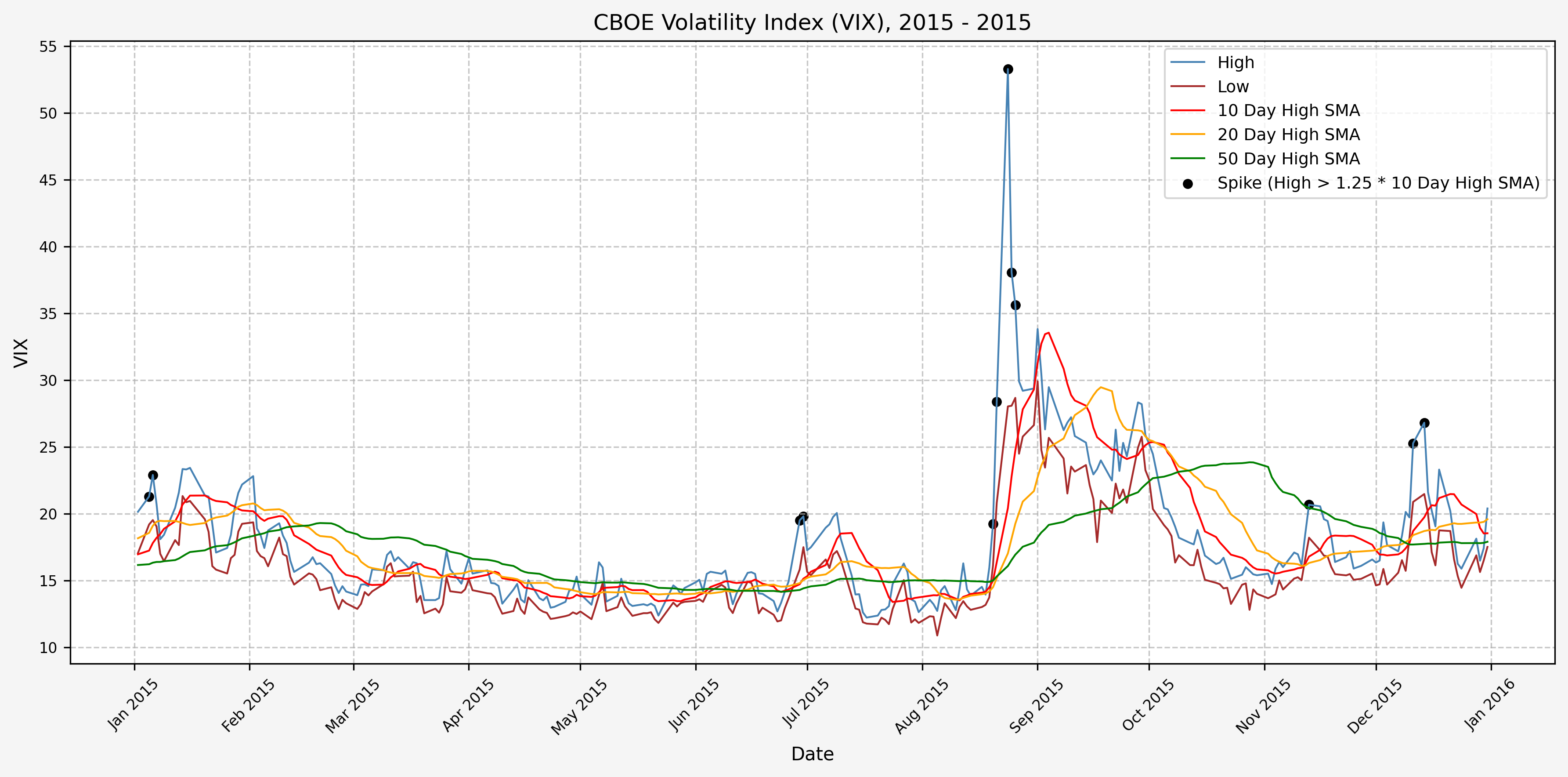

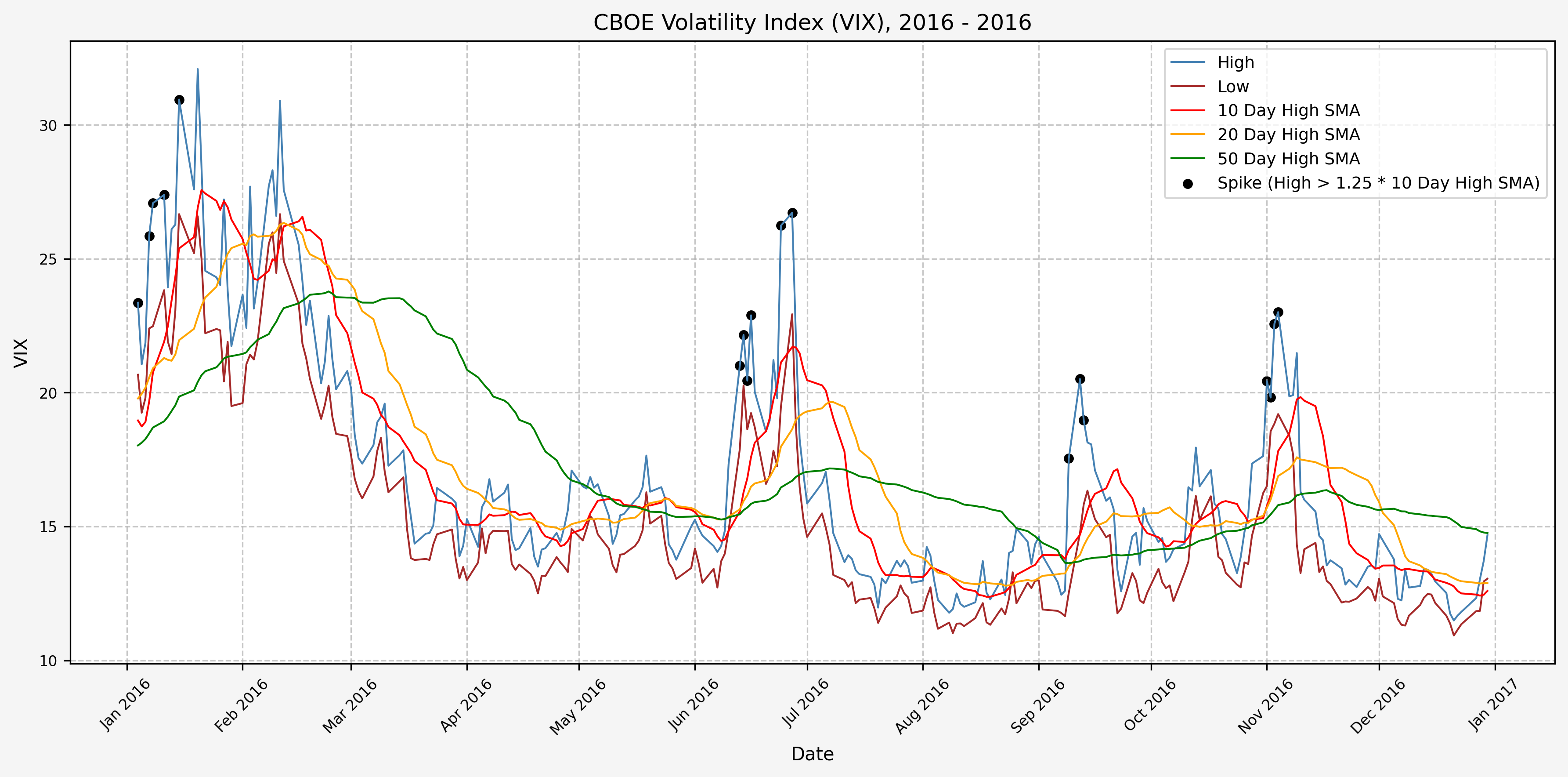

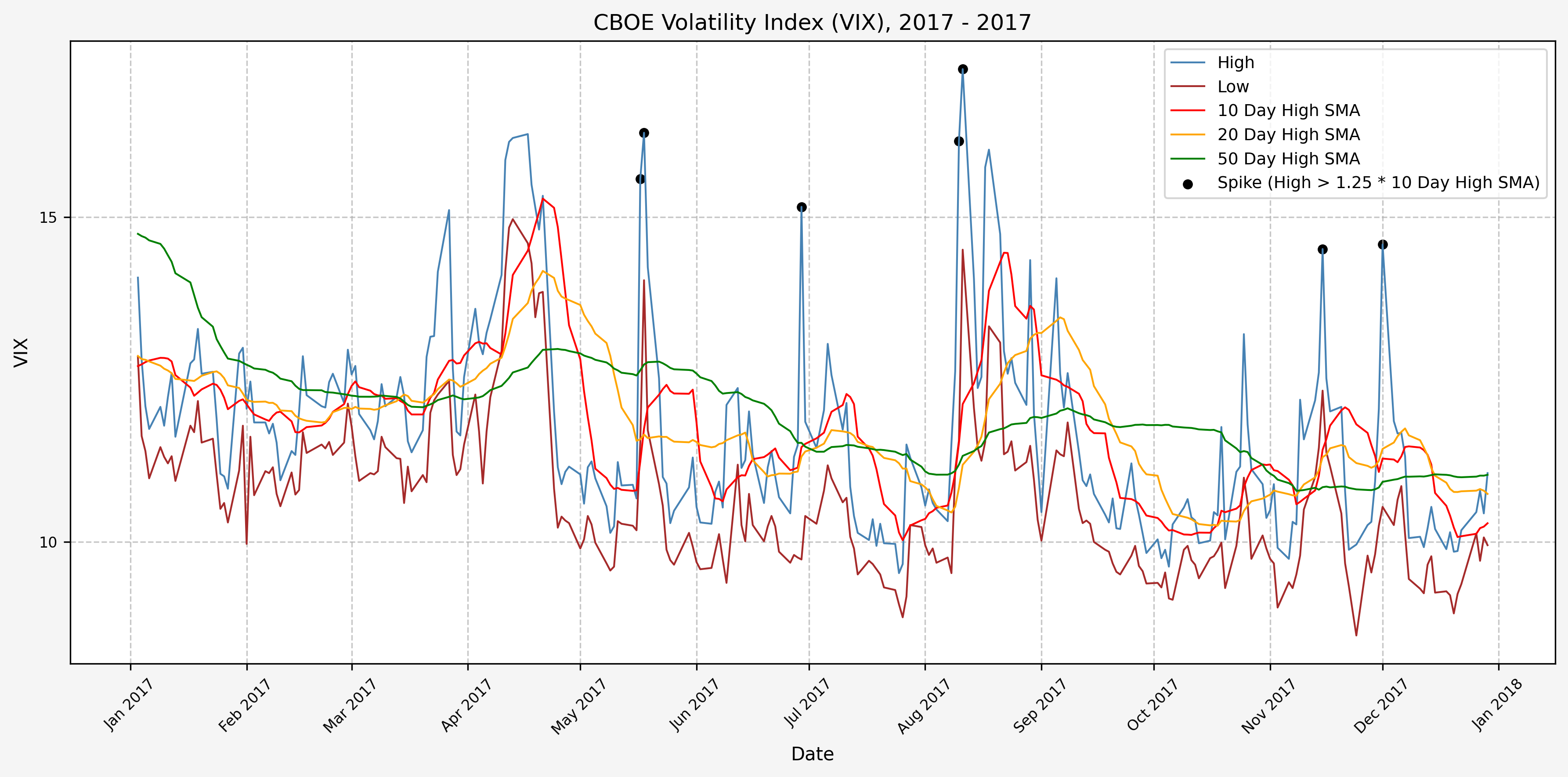

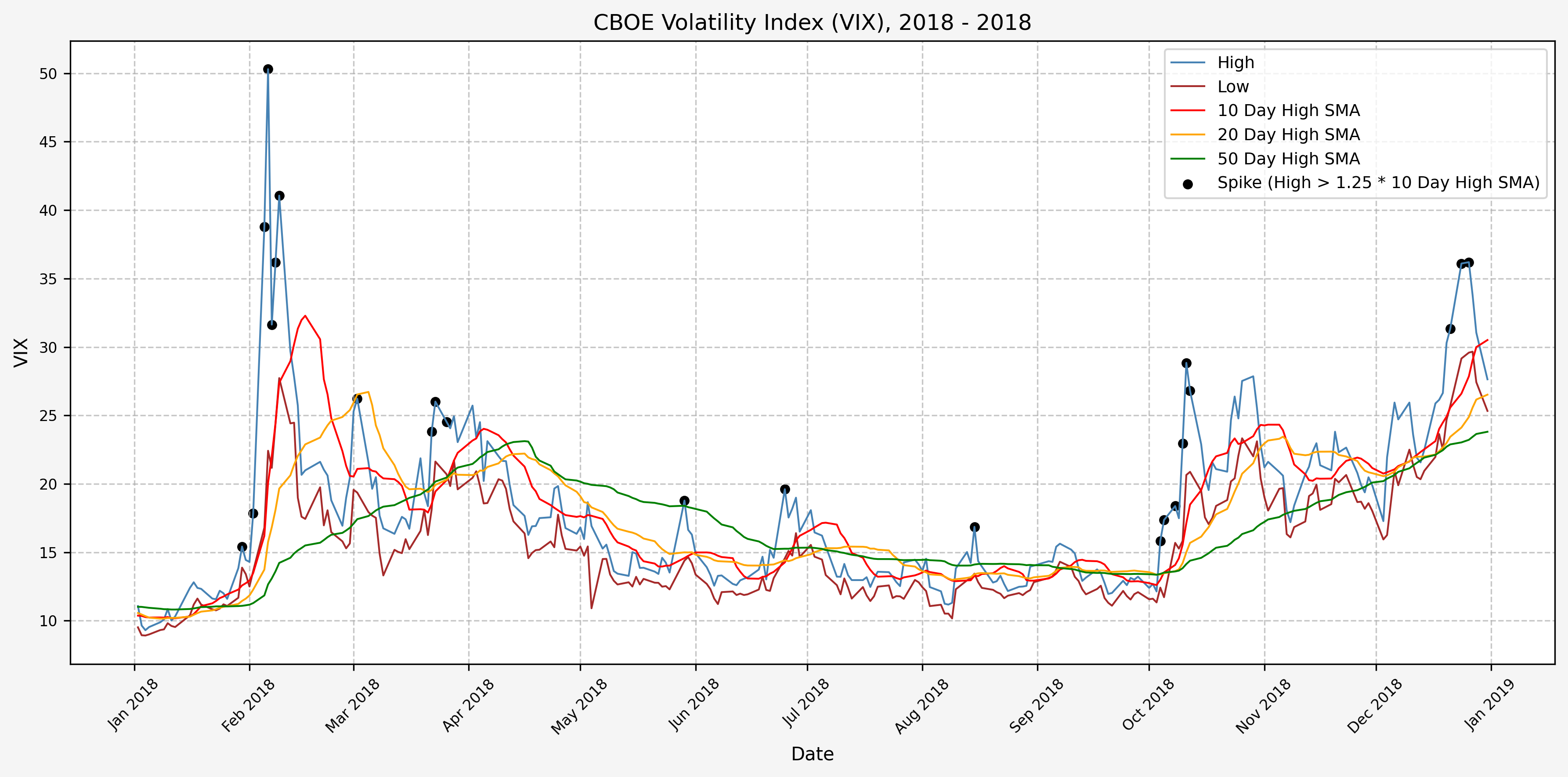

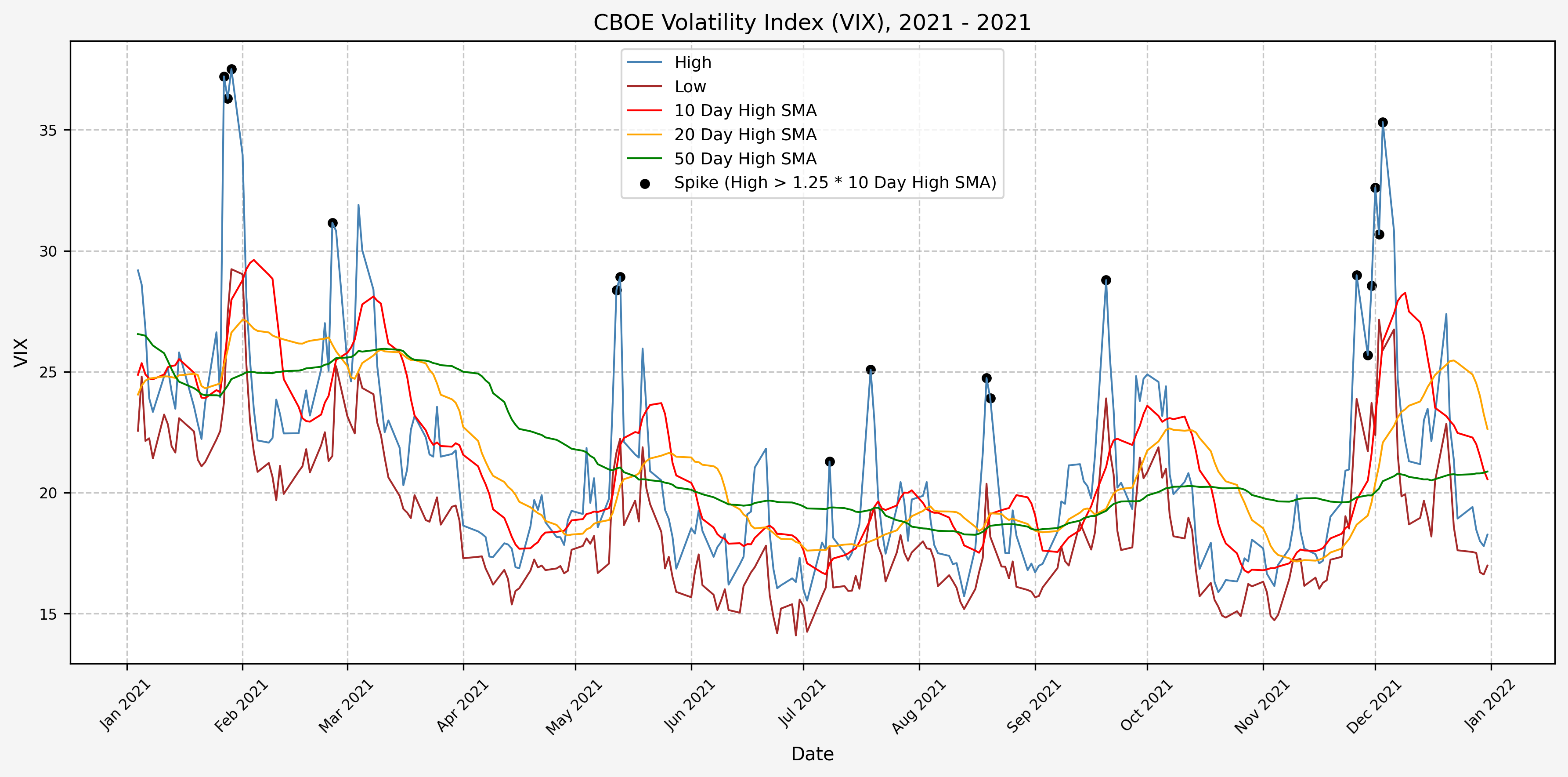

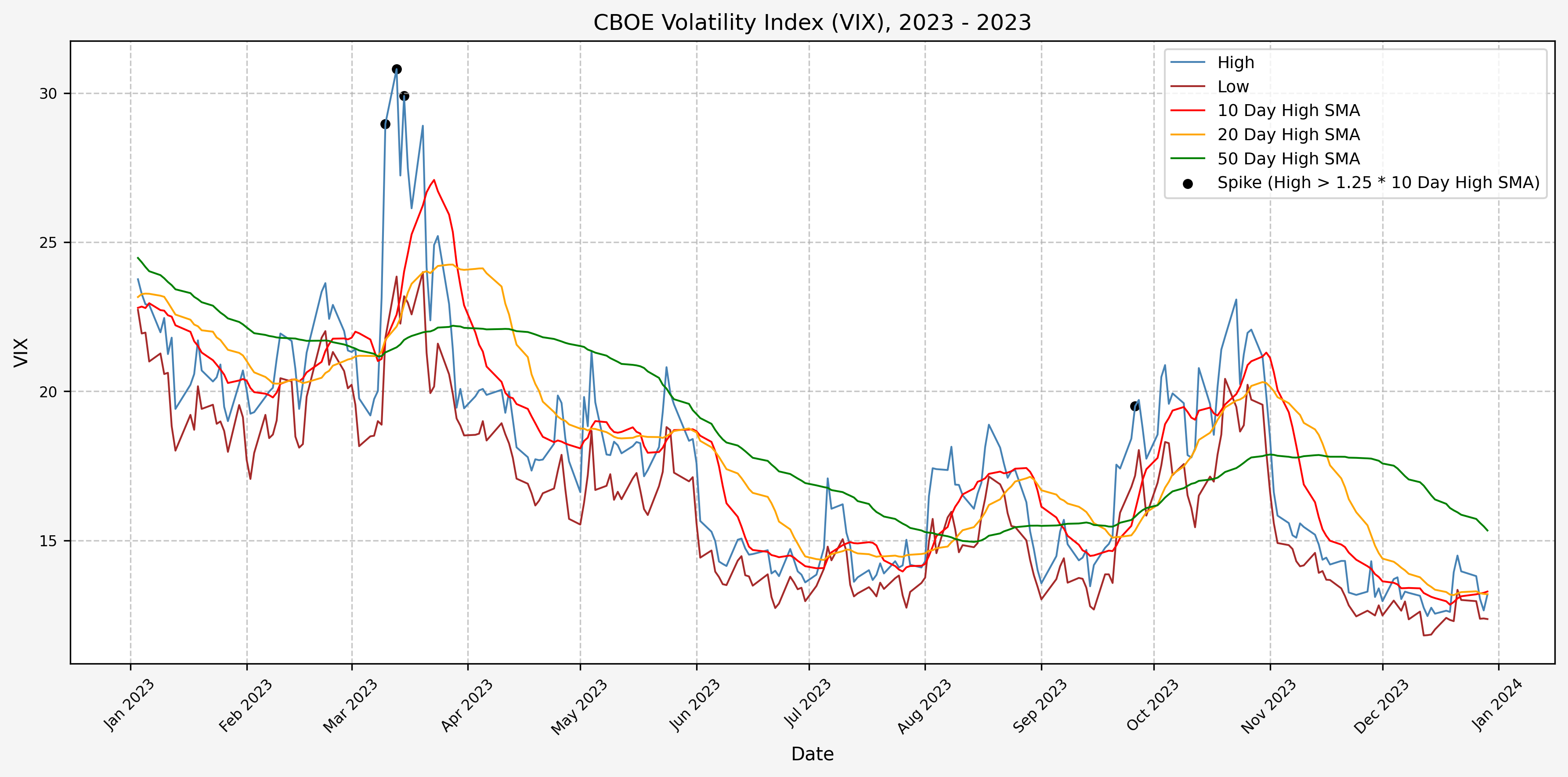

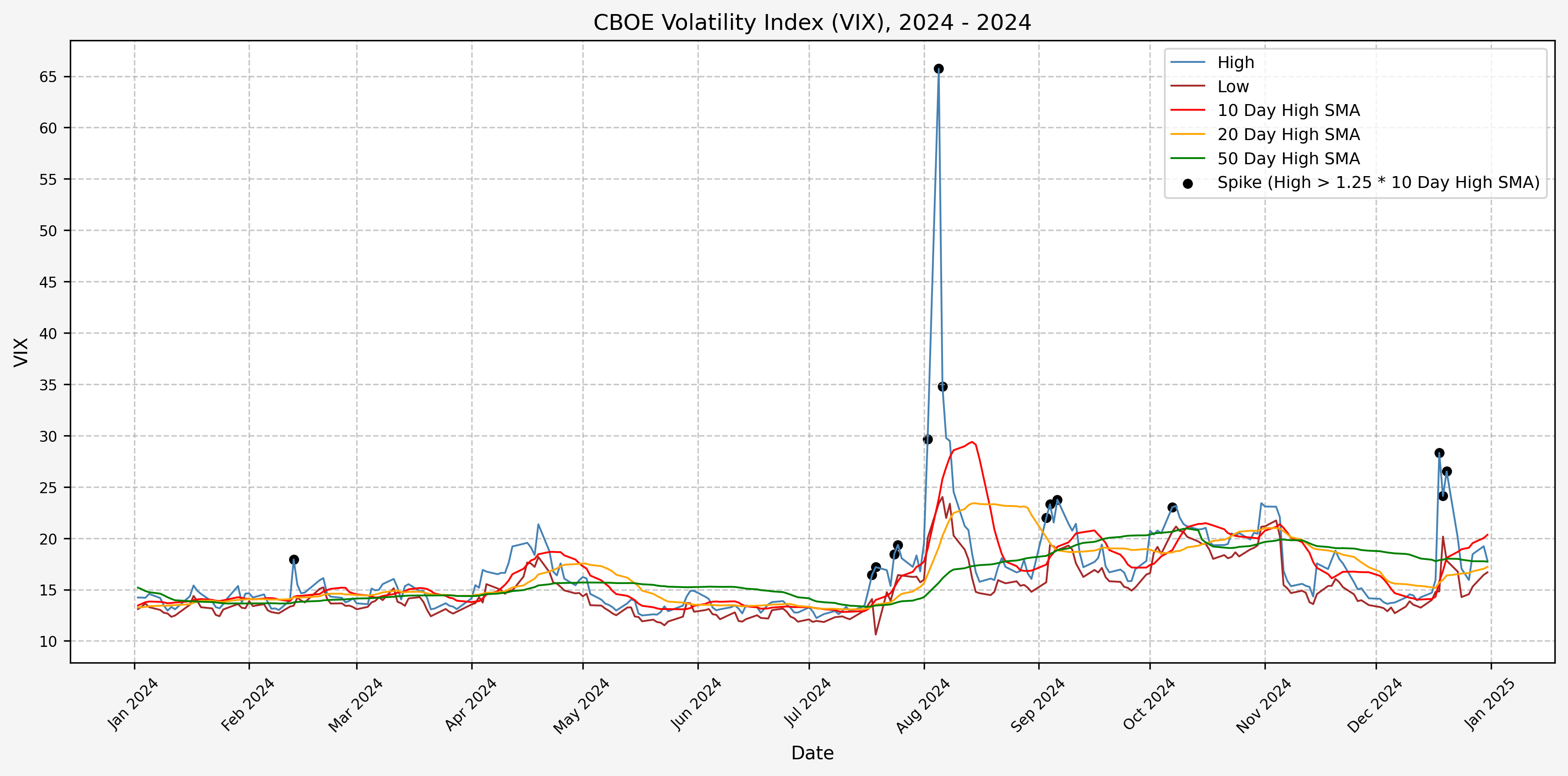

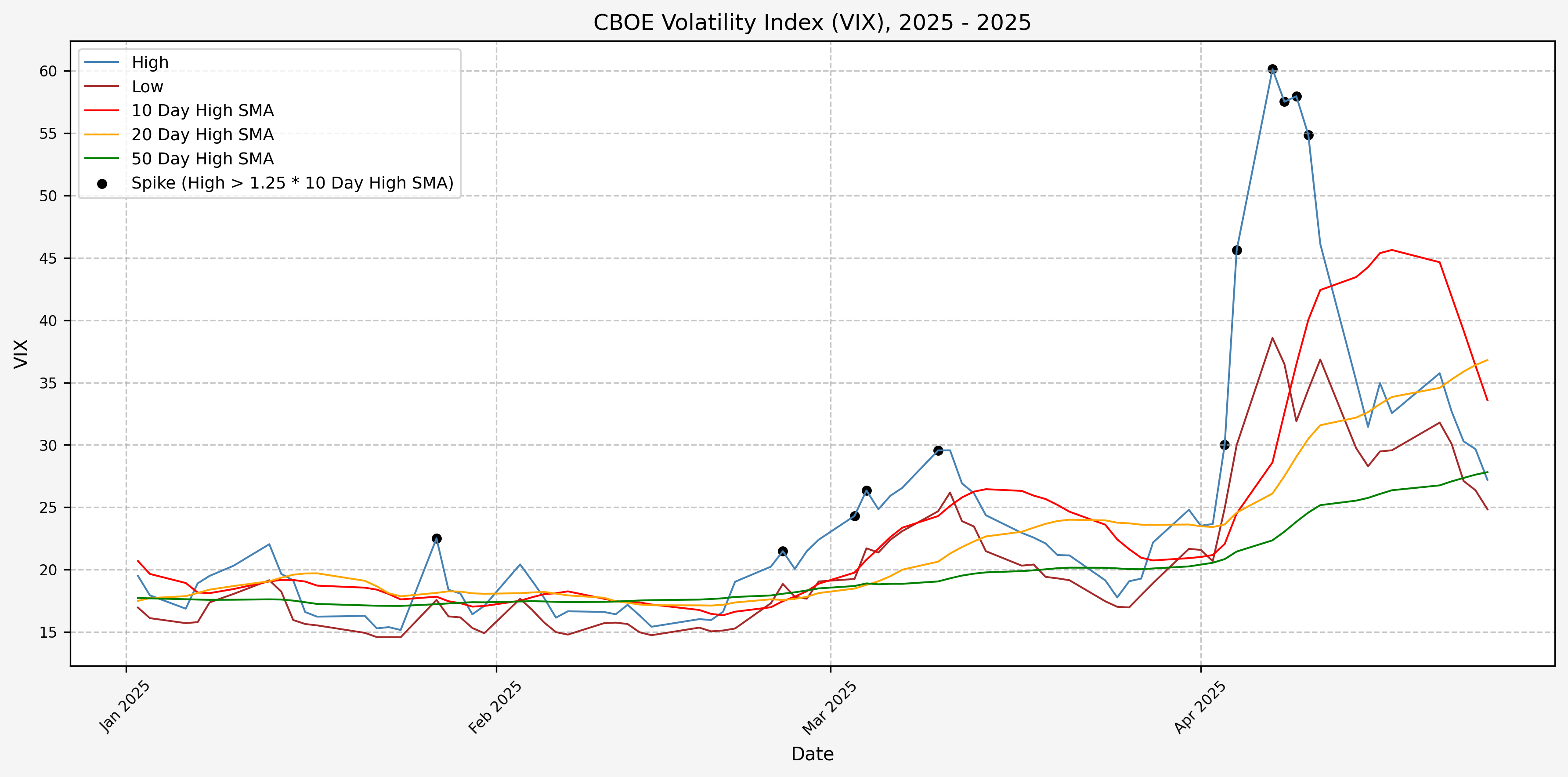

Determining A Spike Level

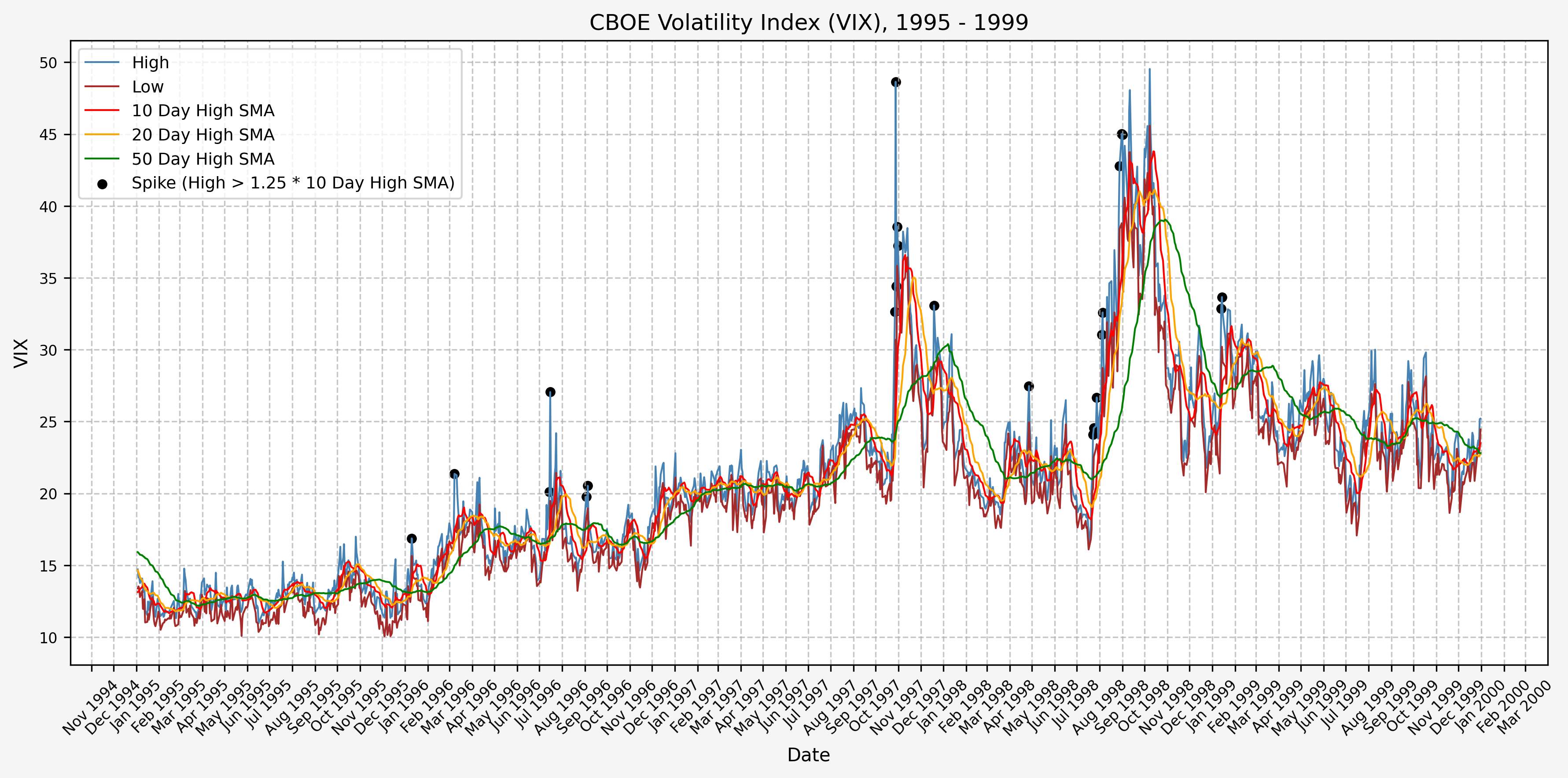

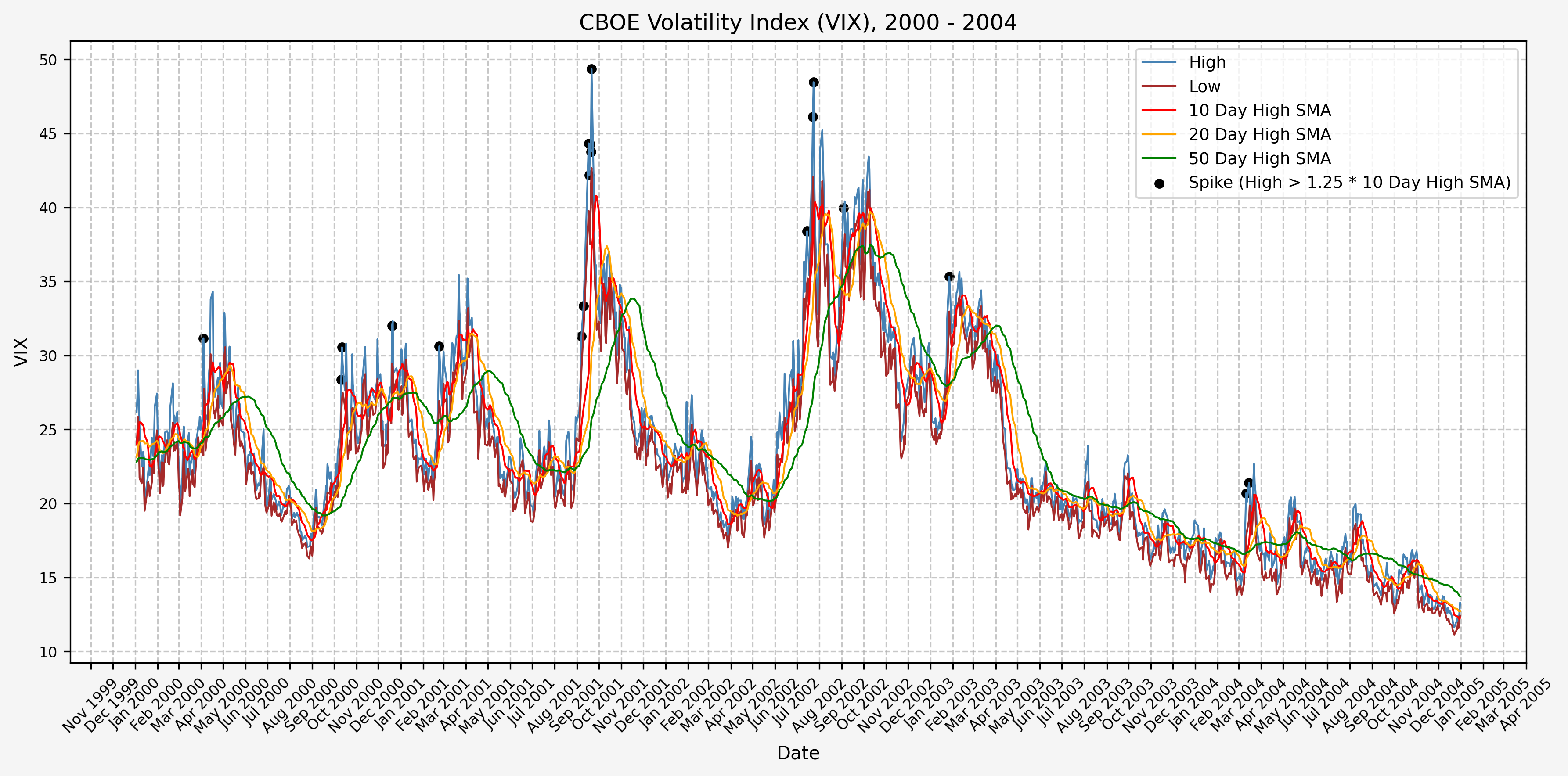

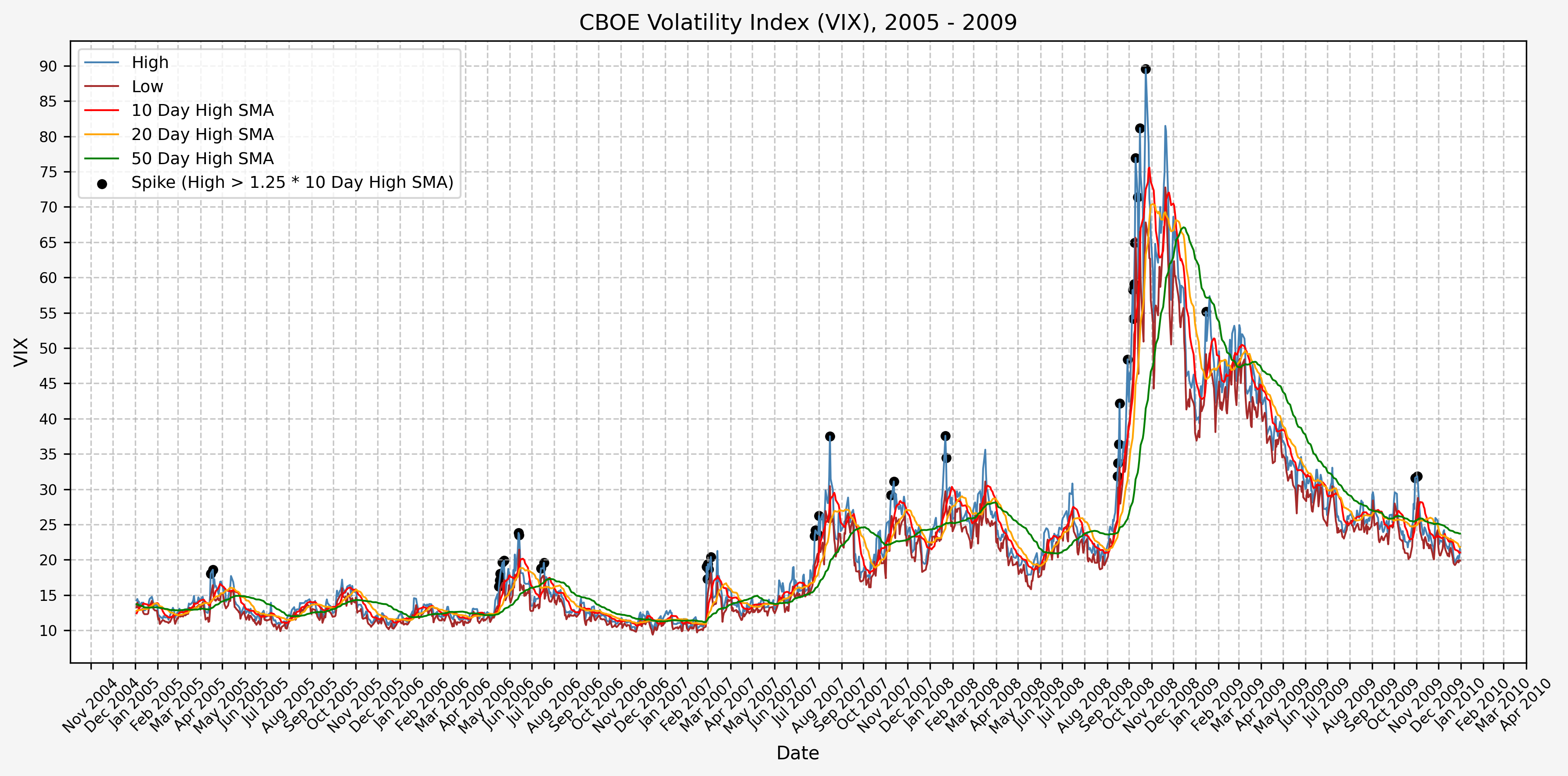

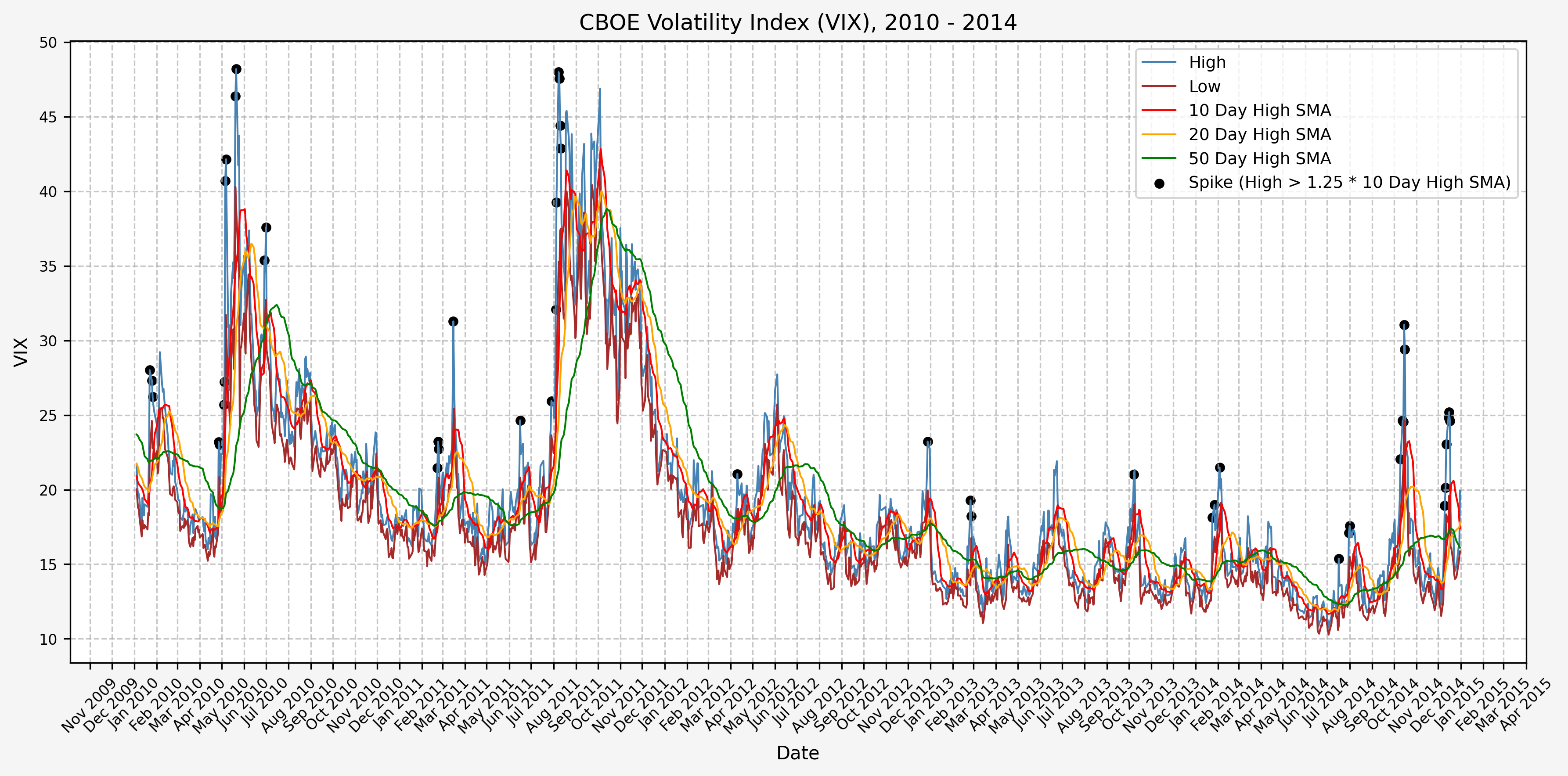

We will start the 10 day simple moving average (SMA) of the daily high level to get an idea of what is happening recently with the VIX. We’ll then pick an arbitrary spike level (25% above the 10 day SMA), and our signal is generated if the VIX hits a level that is above the spike threshold.

The idea is that the 10 day SMA will smooth out the recent short term volatility in the VIX, and therefore any gradual increases in the VIX are not interpreted as spike events.

We also will generate the 20 and 50 day SMAs for reference, and again to see what is happening with the level of the VIX over slightly longer timeframes.

Here’s the code for the above:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

| # Define the spike multiplier for detecting significant spikes

spike_level = 1.25

# =========================

# Simple Moving Averages (SMA)

# =========================

# Calculate 10-period SMA of 'High'

vix['High_SMA_10'] = vix['High'].rolling(window=10).mean()

# Shift the 10-period SMA by 1 to compare with current 'High'

vix['High_SMA_10_Shift'] = vix['High_SMA_10'].shift(1)

# Calculate the spike level based on shifted SMA and spike multiplier

vix['Spike_Level_SMA'] = vix['High_SMA_10_Shift'] * spike_level

# Calculate 20-period SMA of 'High'

vix['High_SMA_20'] = vix['High'].rolling(window=20).mean()

# Determine if 'High' exceeds the spike level (indicates a spike)

vix['Spike_SMA'] = vix['High'] >= vix['Spike_Level_SMA']

# Calculate 50-period SMA of 'High' for trend analysis

vix['High_SMA_50'] = vix['High'].rolling(window=50).mean()

# =========================

# Exponential Moving Averages (EMA)

# =========================

# Calculate 10-period EMA of 'High'

vix['High_EMA_10'] = vix['High'].ewm(span=10, adjust=False).mean()

# Shift the 10-period EMA by 1 to compare with current 'High'

vix['High_EMA_10_Shift'] = vix['High_EMA_10'].shift(1)

# Calculate the spike level based on shifted EMA and spike multiplier

vix['Spike_Level_EMA'] = vix['High_EMA_10_Shift'] * spike_level

# Calculate 20-period EMA of 'High'

vix['High_EMA_20'] = vix['High'].ewm(span=20, adjust=False).mean()

# Determine if 'High' exceeds the spike level (indicates a spike)

vix['Spike_EMA'] = vix['High'] >= vix['Spike_Level_EMA']

# Calculate 50-period EMA of 'High' for trend analysis

vix['High_EMA_50'] = vix['High'].ewm(span=50, adjust=False).mean()

|

For this exercise, we will use simple moving averages.

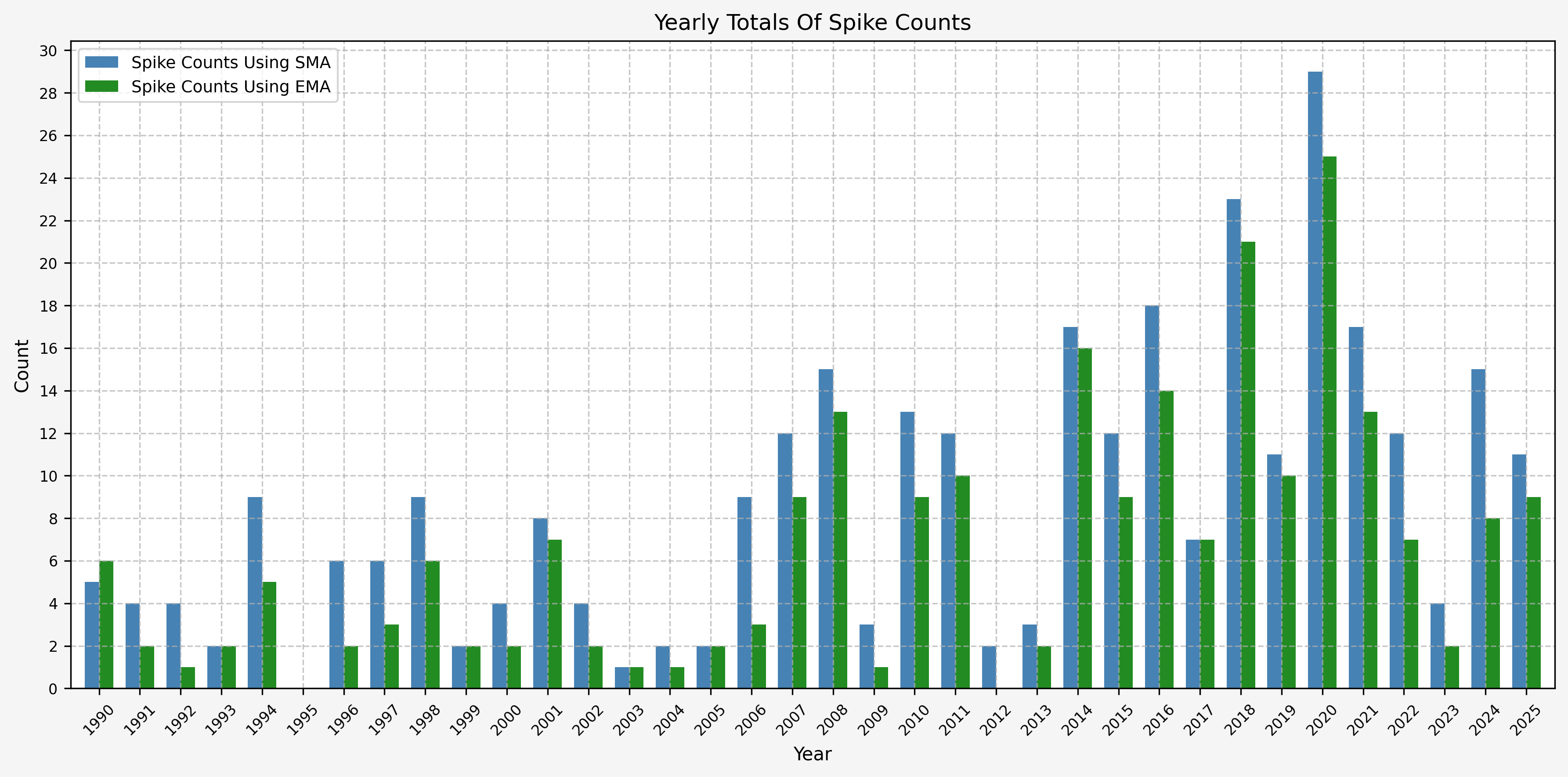

Spike Counts (Signals) By Year

To investigate the number of spike events (or signals) that we receive on a yearly basis, we can run the following:

1

2

3

4

5

6

7

8

9

10

| # Ensure the index is a DatetimeIndex

vix.index = pd.to_datetime(vix.index)

# Create a new column for the year extracted from the date index

vix['Year'] = vix.index.year

# Group by year and the "Spike_SMA" and "Spike_EMA" columns, then count occurrences

spike_count_SMA = vix.groupby(['Year', 'Spike_SMA']).size().unstack(fill_value=0)

spike_count_SMA

|

Which gives us the following:

| Year | False | True |

|---|

| 1990 | 248 | 5 |

| 1991 | 249 | 4 |

| 1992 | 250 | 4 |

| 1993 | 251 | 2 |

| 1994 | 243 | 9 |

| 1995 | 252 | 0 |

| 1996 | 248 | 6 |

| 1997 | 247 | 6 |

| 1998 | 243 | 9 |

| 1999 | 250 | 2 |

| 2000 | 248 | 4 |

| 2001 | 240 | 8 |

| 2002 | 248 | 4 |

| 2003 | 251 | 1 |

| 2004 | 250 | 2 |

| 2005 | 250 | 2 |

| 2006 | 242 | 9 |

| 2007 | 239 | 12 |

| 2008 | 238 | 15 |

| 2009 | 249 | 3 |

| 2010 | 239 | 13 |

| 2011 | 240 | 12 |

| 2012 | 248 | 2 |

| 2013 | 249 | 3 |

| 2014 | 235 | 17 |

| 2015 | 240 | 12 |

| 2016 | 234 | 18 |

| 2017 | 244 | 7 |

| 2018 | 228 | 23 |

| 2019 | 241 | 11 |

| 2020 | 224 | 29 |

| 2021 | 235 | 17 |

| 2022 | 239 | 12 |

| 2023 | 246 | 4 |

| 2024 | 237 | 15 |

| 2025 | 67 | 11 |

And the plot to aid with visualization. Based on the plot, it seems as though volatility has increased since the early 2000’s:

Spike Counts (Signals) Plots By Year

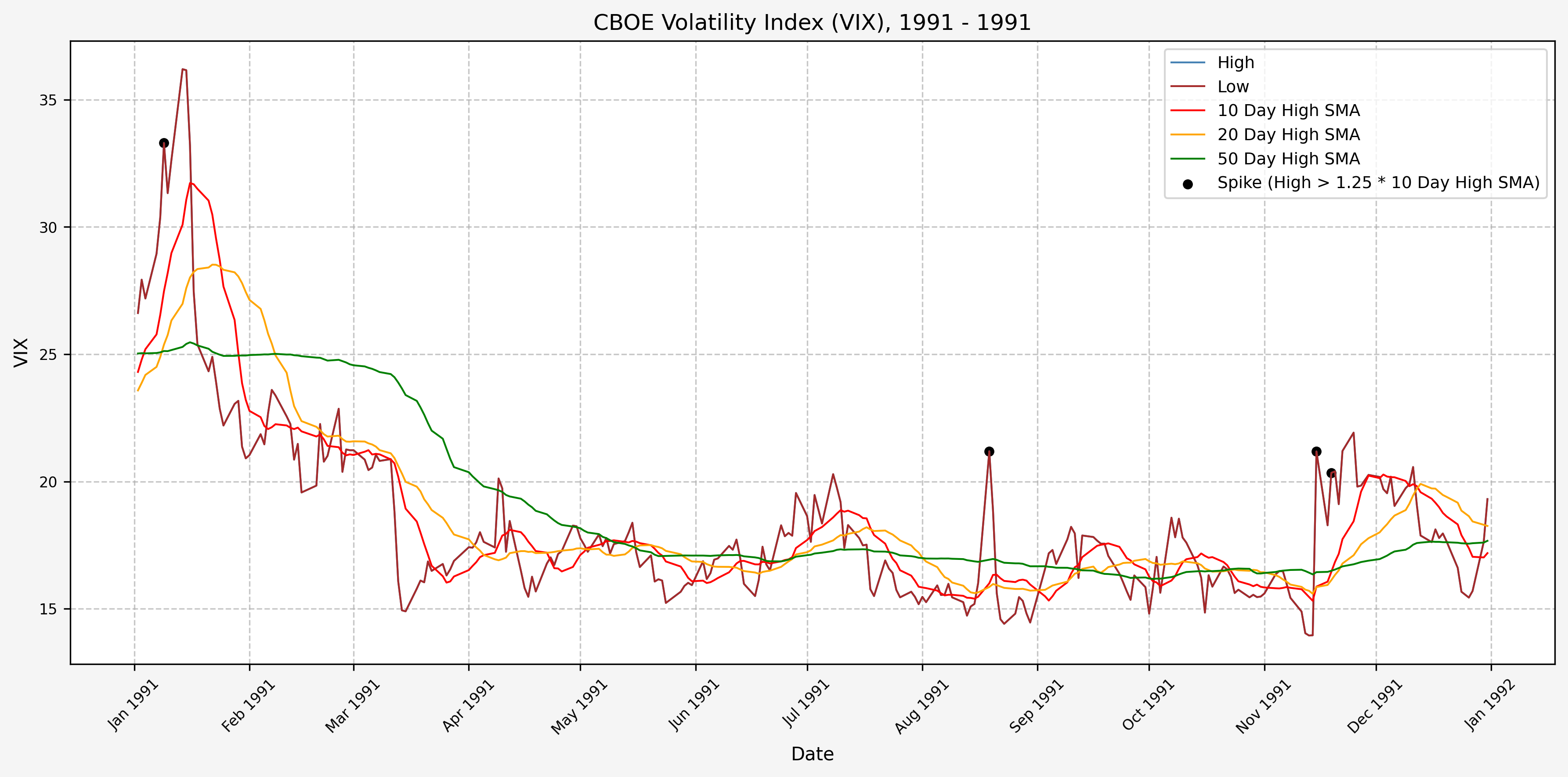

Here are the yearly plots for when signals are generated:

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

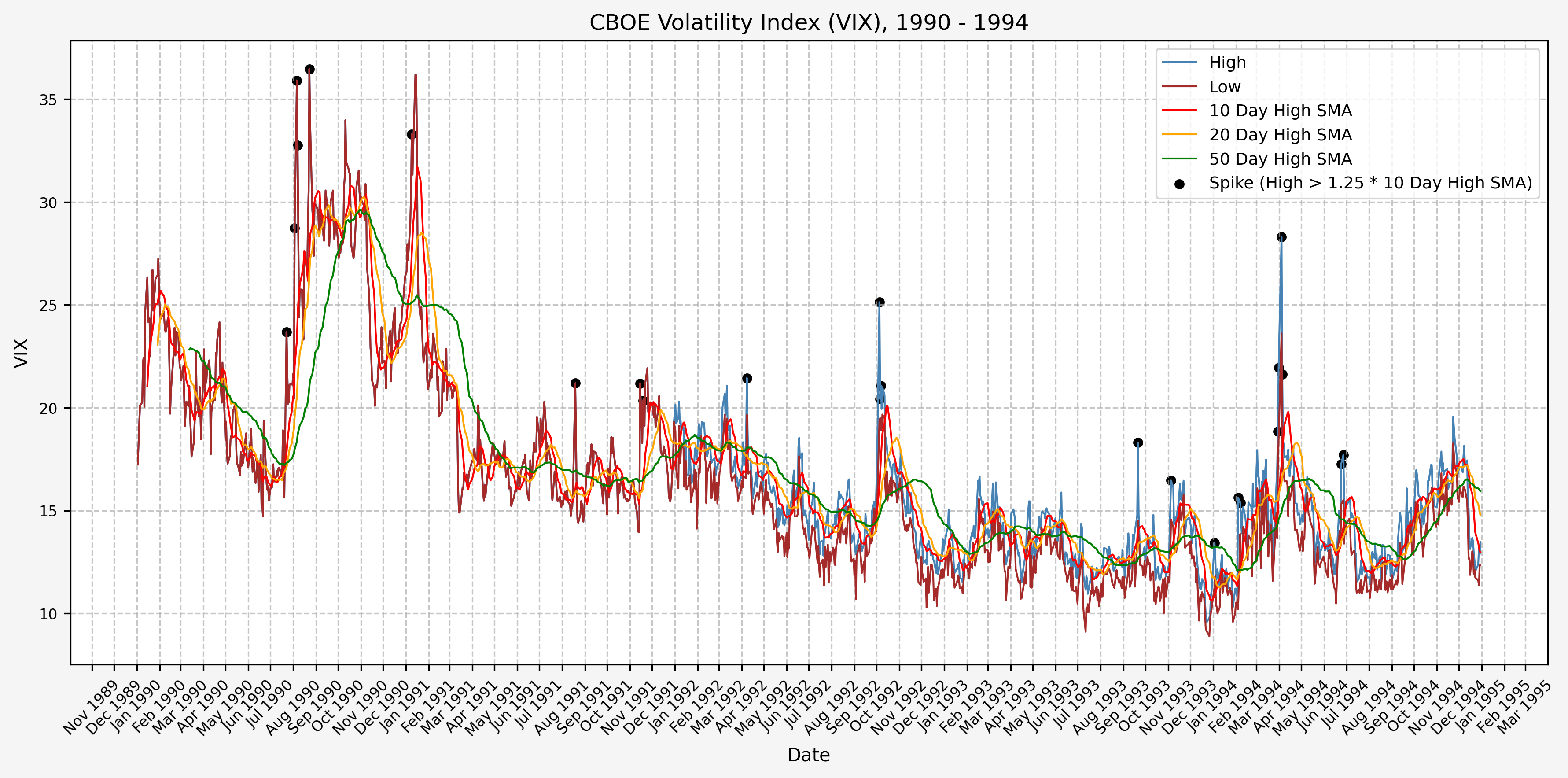

Spike Counts (Signals) Plots By Decade

And here are the plots for the signals generated over the past 3 decades:

1990 - 1994

1995 - 1999

2000 - 2004

2005 - 2009

2010 - 2014

2015 - 2019

2020 - 2024

2025 - Present

Trading History

I’ve begun trading based on the above ideas, opening positions during the VIX spikes and closing them as volatility comes back down. The executed trades, closed positions, and open positions listed below are all automated updates from the transaction history exports from Schwab. The exported CSV files are available in the GitHub repository.

Trades Executed

Here are the trades executed to date:

| Trade_Date | Action | Symbol | Quantity | Price | Fees & Comm | Amount |

|---|

| 2024-08-05 00:00:00 | Buy to Open | VIX 09/18/2024 34.00 P | 1 | 10.95 | 1.08 | 1096.08 |

| 2024-08-21 00:00:00 | Sell to Close | VIX 09/18/2024 34.00 P | 1 | 17.95 | 1.08 | 1793.92 |

| 2024-08-05 00:00:00 | Buy to Open | VIX 10/16/2024 40.00 P | 1 | 16.35 | 1.08 | 1636.08 |

| 2024-09-18 00:00:00 | Sell to Close | VIX 10/16/2024 40.00 P | 1 | 21.54 | 1.08 | 2152.92 |

| 2024-08-07 00:00:00 | Buy to Open | VIX 11/20/2024 25.00 P | 2 | 5.90 | 2.16 | 1182.16 |

| 2024-11-04 00:00:00 | Sell to Close | VIX 11/20/2024 25.00 P | 2 | 6.10 | 2.16 | 1217.84 |

| 2024-08-06 00:00:00 | Buy to Open | VIX 12/18/2024 30.00 P | 1 | 10.25 | 1.08 | 1026.08 |

| 2024-11-27 00:00:00 | Sell to Close | VIX 12/18/2024 30.00 P | 1 | 14.95 | 1.08 | 1493.92 |

| 2025-03-04 00:00:00 | Buy to Open | VIX 04/16/2025 25.00 P | 5 | 5.65 | 5.40 | 2830.40 |

| 2025-03-24 00:00:00 | Sell to Close | VIX 04/16/2025 25.00 P | 5 | 7.00 | 5.40 | 3494.60 |

| 2025-03-10 00:00:00 | Buy to Open | VIX 05/21/2025 26.00 P | 5 | 7.10 | 5.40 | 3555.40 |

| 2025-04-04 00:00:00 | Buy to Open | VIX 05/21/2025 26.00 P | 10 | 4.10 | 10.81 | 4110.81 |

| 2025-04-04 00:00:00 | Buy to Open | VIX 05/21/2025 37.00 P | 3 | 13.20 | 3.24 | 3963.24 |

| 2025-04-08 00:00:00 | Buy to Open | VIX 05/21/2025 50.00 P | 2 | 21.15 | 2.16 | 4232.16 |

| 2025-04-24 00:00:00 | Sell to Close | VIX 05/21/2025 50.00 P | 1 | 25.30 | 1.08 | 2528.92 |

| 2025-04-24 00:00:00 | Sell to Close | VIX 05/21/2025 26.00 P | 7 | 3.50 | 7.57 | 2442.43 |

| 2025-04-25 00:00:00 | Sell to Close | VIX 05/21/2025 50.00 P | 1 | 25.65 | 1.08 | 2563.92 |

| 2025-04-03 00:00:00 | Buy to Open | VIX 06/18/2025 27.00 P | 8 | 7.05 | 8.65 | 5648.65 |

| 2025-04-04 00:00:00 | Buy to Open | VIX 06/18/2025 36.00 P | 3 | 13.40 | 3.24 | 4023.24 |

| 2025-04-07 00:00:00 | Buy to Open | VIX 06/18/2025 45.00 P | 2 | 18.85 | 2.16 | 3772.16 |

| 2025-04-08 00:00:00 | Buy to Open | VIX 06/18/2025 27.00 P | 4 | 4.55 | 4.32 | 1824.32 |

| 2025-04-03 00:00:00 | Buy to Open | VIX 07/16/2025 29.00 P | 5 | 8.55 | 5.40 | 4280.40 |

| 2025-04-04 00:00:00 | Buy to Open | VIX 07/16/2025 36.00 P | 3 | 13.80 | 3.24 | 4143.24 |

| 2025-04-07 00:00:00 | Buy to Open | VIX 07/16/2025 45.00 P | 2 | 21.55 | 2.16 | 4312.16 |

| 2025-04-07 00:00:00 | Buy to Open | VIX 08/20/2025 45.00 P | 2 | 21.75 | 2.16 | 4352.16 |

Closed Positions

Here are the closed positions:

| Symbol | Amount_Buy | Quantity_Buy | Amount_Sell | Quantity_Sell | Realized_PnL | Profit_Percent |

|---|

| VIX 09/18/2024 34.00 P | 1096.08 | 1 | 1793.92 | 1 | 697.84 | 0.64 |

| VIX 10/16/2024 40.00 P | 1636.08 | 1 | 2152.92 | 1 | 516.84 | 0.32 |

| VIX 11/20/2024 25.00 P | 1182.16 | 2 | 1217.84 | 2 | 35.68 | 0.03 |

| VIX 12/18/2024 30.00 P | 1026.08 | 1 | 1493.92 | 1 | 467.84 | 0.46 |

| VIX 04/16/2025 25.00 P | 2830.40 | 5 | 3494.60 | 5 | 664.20 | 0.23 |

| VIX 05/21/2025 50.00 P | 4232.16 | 2 | 5092.84 | 2 | 860.68 | 0.20 |

Net profit and loss percentage: 27.02%Net profit and loss: $3,243.08

Open Positions

Here are the positions that are currently open:

| Symbol | Amount_Buy | Quantity_Buy |

|---|

| VIX 05/21/2025 26.00 P | 7666.21 | 15 |

| VIX 05/21/2025 37.00 P | 3963.24 | 3 |

| VIX 06/18/2025 27.00 P | 7472.97 | 12 |

| VIX 06/18/2025 36.00 P | 4023.24 | 3 |

| VIX 06/18/2025 45.00 P | 3772.16 | 2 |

| VIX 07/16/2025 29.00 P | 4280.40 | 5 |

| VIX 07/16/2025 36.00 P | 4143.24 | 3 |

| VIX 07/16/2025 45.00 P | 4312.16 | 2 |

| VIX 08/20/2025 45.00 P | 4352.16 | 2 |

References

https://www.cboe.com/tradable_products/vix/https://github.com/ranaroussi/yfinance

Code

The jupyter notebook with the functions and all other code is available here.The html export of the jupyter notebook is available here.The pdf export of the jupyter notebook is available here.